From 'Africa's Mobile Phone King' to Energy Storage Player: Is Tecno's Second Growth Curve Reliable?

06/09 2026

06/09 2026

512

512

[Abstract] As mobile phone business growth slows and profits plummet, 'Africa's Mobile Phone King,' Tecno, is accelerating its search for a second growth curve.

In 2025, Tecno Mobile's net profit attributable to shareholders fell 53.49% year-on-year, marking its largest decline since listing. Meanwhile, its long-relied-upon African smartphone market is gradually entering a phase of stock competition (inventory competition). Faced with brands like Xiaomi, Honor, and OPPO continuously penetrating the mid-to-low-end market, Tecno has no choice but to seek new growth spaces.

Among these, energy storage is seen as the most promising area. On one hand, Africa's weak power infrastructure and growing demand for off-grid and backup power solutions persist; on the other, the global energy storage industry is rapidly entering a 'system competition' phase, with core barriers shifting from channels to battery cells, BMS, PCS, and system integration capabilities.

The question remains: Is Tecno replicating its smartphone market expansion methodology, or is it merely entering a 'low-barrier assembly track'? When 'channel dividends' clash with 'technical barriers,' Tecno's second growth curve may not be as easy as in the mobile phone era.

The following is the main text:

After smartphone growth peaks, Tecno begins searching for a second growth curve

'Africa's Mobile Phone King,' Tecno, is experiencing its most challenging year since listing.

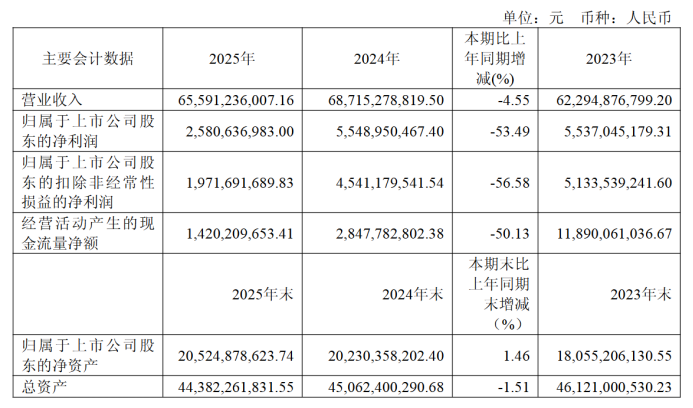

According to Tecno Mobile's 2025 annual report, the company achieved total revenue of 65.591 billion yuan, down 4.5% year-on-year; net profit attributable to shareholders was 2.581 billion yuan, a 53.49% decline. Despite maintaining high shipment volumes, profitability has come under significant pressure.

Source: Tecno Mobile 2025 Annual Report

Financials show that Tecno shipped approximately 169 million mobile phones in 2025, with its three major brands—TECNO, itel, and Infinix—maintaining high market shares in emerging markets like Africa, Pakistan, and Bangladesh.

However, scale has not translated into continued profit growth. On one hand, rising prices of core components like memory continue to drive up hardware costs; on the other, competition in Africa's smartphone market has intensified, with Chinese brands like Xiaomi, Honor, realme, and OPPO penetrating the mid-to-low-end price segments. For Tecno, which has long relied on a high-cost-performance route, this means further compression of profit margins.

Meanwhile, to maintain product competitiveness, Tecno continues to increase R&D and marketing investments. The annual report mentions heightened R&D spending on terminal user experience and increased brand promotion and market expansion efforts, with both R&D and sales expenses rising year-on-year.

Rising costs, intensified competition, and increased expenses are now simultaneously pressuring this smartphone manufacturer, which has long relied on emerging market dividends for growth.

More importantly, smartphone penetration in Africa is itself increasing. GSMA data shows that while mobile internet users in Sub-Saharan Africa continue to grow, the rate has slowed significantly compared to the rapid shift from feature phones to smartphones. For Tecno, which has long depended on the low-end market, this means the era of rapid growth through 'feature phone to smartphone' upgrades is gradually ending.

Against this backdrop, Tecno has begun to significantly accelerate its diversification strategy. In recent years, Tecno has expanded beyond mobile phones to include TVs, air conditioners, small appliances, wearables, two-wheelers, and more, leveraging its established channel network in Africa. Its itel brand even sells home appliances like refrigerators and washing machines.

Source: Tecno Mobile Official Website

These businesses share a common trait: heavy reliance on offline channels and local distribution networks. Tecno hopes to replicate its dealership system from the mobile phone era, upgrading from 'selling phones' to 'selling consumer electronics.' This approach mirrors the expansion strategies of early Chinese home appliance companies in lower-tier markets.

Among these new ventures, energy storage undoubtedly garners the most attention.

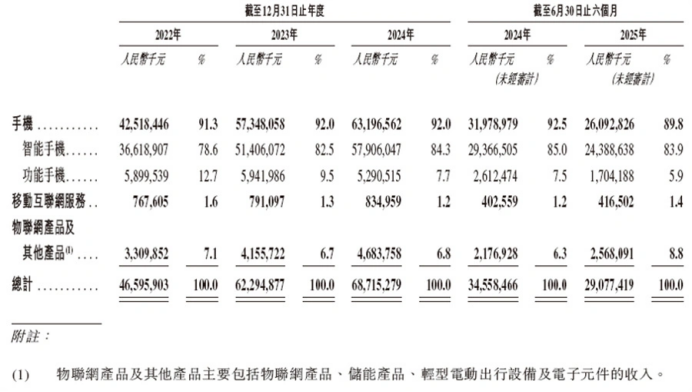

According to Tecno's Hong Kong IPO prospectus, in the first half of 2025, revenue from its 'IoT products and others' segment reached 2.568 billion yuan, accounting for about 8.8% of total revenue. This includes not only energy storage products but also smart hardware, electronic components, and light electric two-wheelers.

Source: Tecno Mobile Hong Kong IPO Prospectus

While currently a small portion of revenue, energy storage—compared to traditional consumer electronics like home appliances and wearables—carries both the industry growth driven by energy transition and a direct link to Africa's persistent power shortages. Thus, Tecno's focus on this segment is understandable.

What does Africa's energy storage market entail?

Tecno's focus on energy storage is understandable.

Compared to the smartphone market, now in a phase of stock competition (inventory competition), Africa's energy infrastructure remains inadequate, with persistent issues of insufficient power supply and frequent blackouts. In this context, many companies view energy storage as the next growth opportunity.

Power shortages have spurred significant demand for off-grid and backup power solutions. In many African countries, diesel generators remain a key power source for households, small businesses, and factories, but high fuel and maintenance costs continue to drive up operating expenses. Meanwhile, rapid declines in the prices of solar panels and lithium batteries in recent years have made residential energy storage increasingly economically viable.

This has shaped Africa's energy storage market into one distinct from China and Europe. In China, energy storage growth is primarily driven by large-scale and grid-side projects; in Europe and the U.S., demand leans more toward residential storage and energy independence. In Africa, energy storage products often resemble consumer electronics-style energy solutions.

Users typically do not purchase large-scale energy storage systems but rather smaller residential systems, portable power stations, and solar-storage all-in-one units. These devices usually have modest capacity but emphasize low cost, easy installation, and off-grid capabilities, while adapting to local environments with frequent blackouts and unstable grids.

In recent years, Chinese companies like Anker Innovations, EcoFlow, and Hello Tech have accelerated their layout (market expansion) in portable and residential storage; inverter and system providers like Sungrow and Deye are also expanding their African channels.

For Chinese companies, the market's greatest appeal lies in its maturing supply chain. Currently, most small-to-medium-sized energy storage products rely on core battery cells from upstream manufacturers like CATL, EVE Energy, and Hithium; PCS, inverters, and BMS have also formed relatively complete industrial support. For channel-focused companies, integrating the supply chain and establishing brand and sales networks offer opportunities for rapid market entry.

This explains why more consumer electronics companies are entering the energy storage sector, hoping to replicate channel expansion strategies from the consumer electronics industry.

From a product perspective, Tecno's entry into energy storage carries distinct consumer electronics characteristics.

Currently, Tecno operates two major energy storage brands: itel Energy and Dyque Energy. itel Energy targets households and small commercial users, offering portable storage, home backup power, and solar-storage integration products; Dyque Energy positions itself as higher-end, covering residential and commercial storage scenarios.

Source: itel Energy Official Website

Notably, Tecno's promotion and sales logic for energy storage products closely resembles its mobile phone business. Application scenarios—such as home lighting, phone charging, TV power, and small appliance use—mostly revolve around household consumer electronics. Some products are even displayed alongside phones and TVs, featuring strong ecosystem synergy and channel reuse.

In a sense, Tecno is not approaching energy storage from the perspective of an energy company but attempting to make it a new category within its consumer electronics ecosystem.

However, energy storage is not a mobile phone, TV, or home appliance. Compared to the mature supply chain divisions in consumer electronics, the energy storage industry demands much higher system integration, safety management, and long-term operation and maintenance capabilities.

Energy storage is not a low-barrier business. Especially in overseas markets, energy storage devices involve long-term charging/discharging, safety management, thermal runaway control, and complex after-sales maintenance. Fire incidents, battery degradation, or system failures not only entail compensation risks but could also damage brand reputation.

Thus, competition in the energy storage industry is gradually shifting from channel expansion to system capabilities. Battery cell consistency, BMS algorithms, PCS efficiency, thermal management, and local after-sales systems directly impact product stability and lifespan.

This differs markedly from the smartphone industry. Smartphone supply chains are highly standardized, with brands competing primarily on channels and product definition; energy storage remains in rapid iteration, where safety and system reliability hold greater importance.

For Tecno, its African channels remain a key advantage, but channels do not automatically translate into technical barriers in energy storage. This means Tecno's real competition is no longer just 'who can sell products in Africa' but who can balance low cost, stability, and safety.

That said, genuine demand in Africa's energy storage market remains somewhat controversial.

Unlike residential storage demand in mature grid markets like Europe and the U.S., many African regions first face 'power shortages' rather than 'energy storage needs.' IEA data shows that a large population in Sub-Saharan Africa still lacks stable electricity access. In some underdeveloped areas, basic power generation needs—such as solar or diesel—still take precedence over storage.

AFSIA data indicates that Africa's installed energy storage capacity reached approximately 1.64 GWh in 2024, with the overall market remaining small and concentrated in relatively economically developed countries like South Africa, Egypt, and Morocco.

This means that while Tecno may find opportunities selling portable and small residential storage products in Africa, demand maturity for commercial and large-scale storage may remain limited.

Market potential exists, but demand requires cultivation—a defining feature of Africa's energy storage market. In this environment, whether Tecno can convert its channel advantages into competitive strengths in energy storage will determine the viability of its second growth curve.

What are Tecno's strengths and weaknesses in energy storage?

For Tecno, energy storage is not an entirely unfamiliar market.

Over the past decade, the company's core capability has not been hardware R&D but building a localized operational system across Africa. From channel distribution and after-sales maintenance to offline retail networks, Tecno has established strong coverage in multiple African countries.

According to public data, Tecno boasts a vast network of distributors and retail stores across Africa, with offline presence even in many low-tier cities and rural areas. This explains its long-term leadership in Africa's mobile phone market share.

Energy storage is also a highly channel-dependent industry. Especially in Africa, where consumer awareness of residential and portable storage remains limited, offline display, installation, after-sales service, and local repair capabilities directly influence sales. This means Tecno's accumulated channel resources hold certain reuse value.

Compared to many Chinese energy storage companies entering Africa for the first time, Tecno has at least solved the 'how to enter the market' problem. This is its biggest distinction from most energy storage startups.

Source: Tecno Mobile Official Website

The issue, however, is that channel advantages do not equate to energy storage capabilities.

In the smartphone industry, brands rely heavily on supply chain integration, product definition, and channel operations; they can establish market share even without core chip technologies. But the energy storage industry demands much higher system stability and safety, with many link (links) lacking the mature, standardized industrial divisions seen in smartphones.

Especially in the African market, which experiences high temperatures and frequent power grid fluctuations, energy storage equipment often operates in complex environments for extended periods. In the event of thermal runaway, battery degradation, or system failures, not only are after-sales costs high, but brand reputation may also be directly impacted.

From currently available public information, it appears that Transsion leans more toward a channel and branding role in the energy storage sector. Its related products rely heavily on external supply chain integration, including battery cells, inverters, and some system solutions, primarily provided by partner manufacturers.

According to its Hong Kong stock exchange prospectus, in addition to some smartphones, the company's portion of IoT products and other items are mainly produced by ODM and OEM suppliers, and this business already includes products such as energy storage and two-wheeled electric vehicles. This indicates that Transsion currently assumes more of a branding, channel, and sales function rather than possessing core system capabilities.

Compared to companies like CATL, Sungrow, and Deye, which have established technological systems, Transsion’s accumulation in foundational capabilities such as BMS, PCS, and thermal management remains limited. This suggests that its energy storage business currently follows a 'consumer electronics-style' expansion path: rapidly launching products by relying on a mature supply chain and then leveraging channel capabilities to complete market penetration.

This model can help companies quickly enter the market in the short term but also makes them more vulnerable to price competition. In the past few years, the portable energy storage industry has seen a similar situation, with many brands expanding rapidly through ODMs. However, as competition intensified, product homogenization and price wars emerged swiftly, leading to a noticeable decline in profit margins for many companies.

Furthermore, the energy storage industry demands far higher long-term after-sales and operational capabilities than consumer electronics. While mobile phones typically have a lifecycle of only two to three years, energy storage equipment often needs to operate stably for five years or even longer. For Transsion, which has long operated under a consumer electronics logic, there remains uncertainty about whether it possesses the capabilities for long-term energy equipment services.

More importantly, the energy storage industry is rapidly entering a phase of technological upgrading. With stricter overseas certification standards and rising user demands for safety and cycle life, relying solely on a 'channel + assembly' model will struggle to create genuine barriers in the future. Once profit distribution in the upstream supply chain is realigned, the bargaining power of channel brands may be further compressed.

This is the biggest doubt surrounding Transsion’s energy storage business: Is it building long-term energy capabilities, or is it merely hoping to replicate the 'channel expansion' model from its heyday in the mobile phone era?

If Transsion can gradually establish system R&D and product capabilities, it may secure long-term market space. However, if it remains stuck in channel and assembly roles, its energy storage business will likely be confined to low-margin competition.

Epilogue

Epilogue

From feature phones to smartphones, Transsion once seized the window of opportunity before the widespread adoption of mobile internet in Africa. By leveraging channel sink (channel penetration), localized operations, and supply chain integration, the company established its own moat in a market long overlooked by international phone manufacturers.

But today, the African smartphone market has gradually entered a phase of stock competition (market saturation competition). The waning dividend (dividends) of low-end models and shrinking profit margins have forced Transsion to seek new growth avenues. Home appliances, two-wheelers, and energy storage all follow the same underlying logic: reusing existing channel networks to continue selling more products to African consumers.

Among these, energy storage offers the greatest room for imagination (imagination space) but also poses the highest barriers. Unlike consumer electronics, energy storage relies more heavily on long-term technological accumulation, system safety capabilities, and supply chain coordination. While channels can help companies quickly penetrate the market, they are difficult to directly translate into technological barriers.

For Transsion, the greatest test of its energy storage business may not be whether a market exists but whether it can bridge the capability gap between being a 'channel-driven consumer electronics company' and becoming a 'system-driven energy enterprise.' Compared to selling phones back then, this is clearly a tougher battle.

- XINLIU -

-

![]()

Qianwen’s Version of ‘Being Inside the Nails’

-

![]()

Unbelievable! Chery’s Rumor Refutation Disappears—Who’s Behind the Chaos?

-

![]()

Force Robotics Acquires Atomix: Empowering Robots to Develop Data Flywheels in Real-World Business Environments

-

![]()

Is India Acquiring Electric Vehicle Tech from China? Chery Responds

-

![]()

Struggling to Compete? Japanese Automakers Shift Focus to India, a Market Even Musk Avoids

-

![]()

Why Haven’t We Seen Any Automakers Go Bankrupt Yet, Even as 2026 Reaches Its Midpoint?

-

![]()

Saido Is in Need of a 'Primary Responsible Entity'

-

![]()

Shanghai Robot Brain’s Debut Share: Second Bid for HKEX Listing