Storage Price Increases Weigh on Industry! Global Smartphone Production Set to Decline by 16.2% by 2026

06/09 2026

06/09 2026

568

568

Kuaikeji, June 9th - The global smartphone industry has embarked on a production reduction cycle, propelled by sustained and substantial hikes in memory prices, according to the latest report from TrendForce.

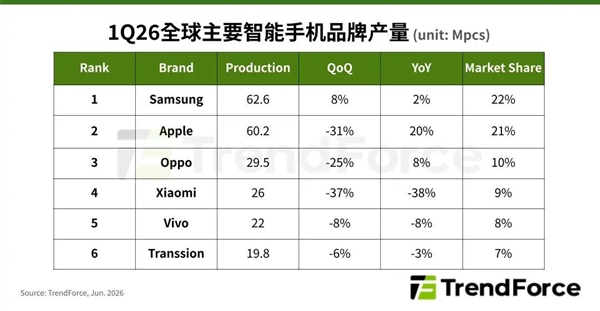

In the first quarter of 2026, global smartphone production reached approximately 284 million units, marking a modest year-on-year decrease of 1.7%.

During this timeframe, the repercussions of storage price surges on the industry were relatively contained. This was primarily because major brands were still working through their inventories of previously low-priced memory. Meanwhile, consumers, anticipating impending price rises in end products, somewhat stimulated market demand, thereby mitigating some of the adverse effects.

However, as low-priced inventories dwindle and significant memory price increases over multiple successive quarters eat into brand profits, the entire industry is poised to witness a substantial production cut in the second quarter of 2026.

Looking at the entire year, institutions forecast that global smartphone production will decrease to 1.051 billion units, representing a year-on-year drop of 16.2%.

If memory price increases persist unchecked and brands are compelled to keep raising product prices, there is a looming risk of further exacerbating the annual production decline.

Production strategies among major smartphone manufacturers have displayed significant differences, influenced by product mix, financial robustness, and market positioning. Samsung, Apple, and Huawei, as the top three high-end contenders, exhibit strong resilience and opt to expand despite the trend.

Samsung's production in the first quarter stood at approximately 62.6 million units, securing the top global spot with a slight year-on-year uptick of 2.3%, leveraging group resources and premium product pricing to sustain scale. Apple's production in the same period reached 60.2 million units, ranking second with a notable year-on-year surge of 19.7%, significantly driven by the iPhone 17 series and iPhone 17e new models, maintaining solid profitability. Huawei also demonstrated steady growth with its high-end offerings.

Production by the three major brands, Xiaomi, OPPO, and vivo, experienced seasonal declines in the first quarter. Hampered by storage costs, their profit margins are under strain, leading to cautious full-year production plans with the potential for significant capacity cuts.

Transsion's production in the first quarter amounted to 19.8 million units, roughly unchanged year-on-year. Focusing on entry-level models with slim profit margins and insufficient low-priced inventories, the brand has been significantly impacted by this round of price hikes. Nevertheless, robust demand in emerging markets still offers some support.

In summary, high-end brands leverage their pricing power and comprehensive strengths to withstand cost pressures, while mid-to-low-end brands rein in production capacity amid the dual pressures of costs and competition, making the Matthew effect in the industry increasingly pronounced.

-

![]()

Cook’s ‘Curtain Call’: Has Apple AI Finally ‘Set Sail’? | Apple WWDC 2026 Highlights

-

![]()

Cook's 'Curtain Call': Apple AI 'Sets Sail'? | Apple 2026 WWDC Highlights

-

![]()

Storage Price Increases Weigh on Industry! Global Smartphone Production Set to Decline by 16.2% by 2026

-

![]()

Large Models Reignite Big Tech's 'Healthcare Dreams'

-

![]()

Siri AI Takes Center Stage, VisionOS Steps Back: Can Cook Secure Victory in the AI Showdown?

-

![]()

Tencent and JD.com Forge Alliance: AI Agent Achieves Transaction Breakthrough

-

![]()

Auto Market Sees Increasing Polarization amid 'Moderate Recovery,' SAIC Volkswagen Leads Transformation with Five New Energy Models

-

![]()

Automotive-Grade Chip Prices Skyrocket by 180% in Three Months, Prompting NEVs to Stealthily Hike Prices Again