Saido Is in Need of a 'Primary Responsible Entity'

06/09 2026

06/09 2026

352

352

Landi Rebrands, Saido Seeks a 'Guiding Force'

Seres is finally rolling out a new brand.

On June 8, as per reports from

According to Tianyancha, on May 29, Chongqing Landi Technology Co., Ltd. underwent a name change to Chongqing Saido Technology Co., Ltd. This transformation was not merely nominal; the equity structure also underwent significant alterations.

Prior to the change, Landi Auto was under the control of Seres Group. Post-change, Chongqing Shaci Zhiyuan New Energy Technology Partnership emerged as the largest shareholder, with a 34.5% stake, while Seres Automobile Hubei Co., Ltd., controlled by Seres Group, became the second-largest shareholder, holding a 32.96% stake.

In essence, Seres remains a participant but no longer wields controlling power.

This also implies that from its inception, Saido Auto is confronted with a question that many once hoped Aito would address: Whose vehicle is it, truly?

01 Seres Steps Back, Landi Undergoes a Transformation

Seres has consciously taken a step back.

As per

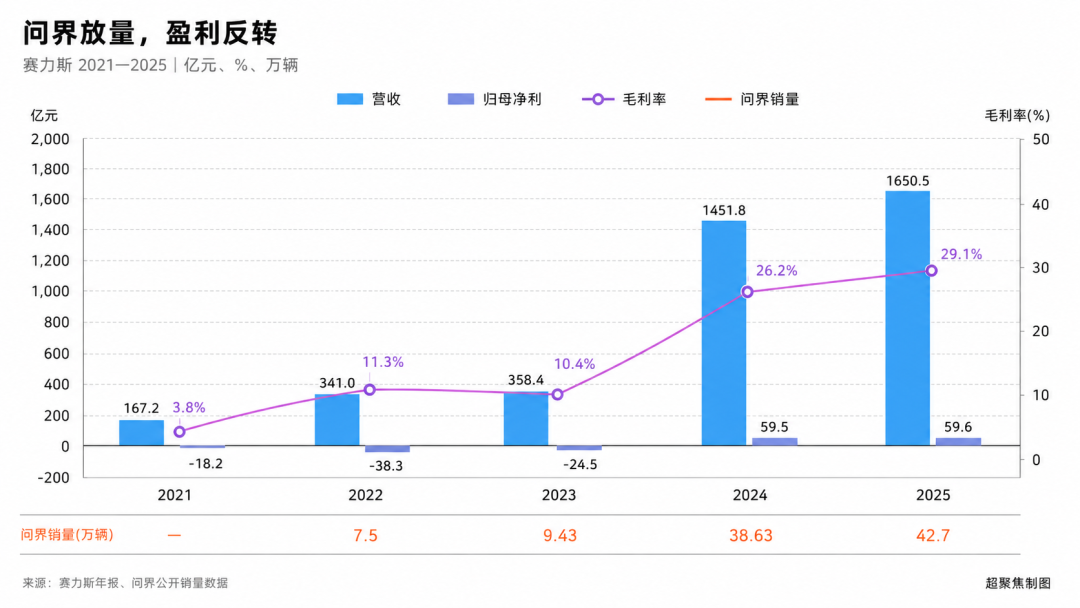

In 2023, Seres reported an annual revenue of RMB 35.84 billion, with a net loss attributable to the parent company of RMB 2.45 billion. By 2024, with Aito gaining momentum, Seres' revenue surged to RMB 145.18 billion, marking a year-on-year increase of 305.04%, and a net profit attributable to the parent company of RMB 5.95 billion, signaling a shift from 'transformation' to 'profitability.'

By 2025, Seres' revenue continued to climb to RMB 165.05 billion, with Aito delivering 427,000 vehicles for the year, at an average transaction price of RMB 391,000.

When you consider this price range, delivery volume, and profit performance, it essentially boils down to one point:

Seres' current success owes much to Aito.

Thus, Seres' decision to relinquish control appears to be a strategic move to differentiate Aito and Saido: Aito remains at the forefront, while Saido is relegated to the sidelines, given a new name, a new set of shareholders, and a fresh start.

However, as Seres steps down from its position as the largest shareholder, Saido has welcomed Chongqing state-owned capital and industrial capital. Chongqing Shaci Zhiyuan has assumed the role of the largest shareholder, with Seres stepping back to become the second-largest shareholder. Related parties of CATL, component companies, and intelligent suppliers have also been incorporated into this new narrative.

But building cars is not akin to hosting a party—more attendees do not necessarily equate to a more vibrant atmosphere.

Previously, when Landi was part of the Seres ecosystem, poor sales could be overlooked. Now, as Saido becomes a new venture controlled by state-owned capital, with Seres as a shareholder and co-built by industrial capital, Seres' ability to provide manufacturing capabilities, engineering experience, and supply chain foundations is no longer the decisive factor.

Aito is the main narrative; Landi was a side story. Aito is intricately linked to Seres' profits, valuation, and high-end branding, while Saido represents more of an asset revitalization and new brand experiment. Landi, previously under the Seres umbrella, neither achieved robust sales nor secured Aito-level resources.

Now, with a new name and the infusion of state-owned and industrial capital, at least a new narrative can be spun: 'State-owned-controlled, Seres-manufactured, intelligent supply chain-synergized, and overseas-market-oriented.'

But a compelling narrative does not guarantee robust sales. The fundamental difference between Saido and Aito lies here: while Aito is often questioned about 'who exactly builds the car,' consumers actually have a clear answer in mind: Huawei is deeply involved in its definition, while Seres handles manufacturing. Huawei's brand, distribution channels, product definition, and user perception have all significantly contributed to Aito's success.

Saido has Seres in its corner, but Seres cannot abandon Aito; Saido has the imagination of Doubao and Volcano Engine, but ByteDance is not an automaker; Saido has Yuanrong Qixing, but Yuanrong is merely an intelligent driving supplier; Saido has Chongqing state-owned capital, but state-owned capital can provide resources, not necessarily product and user definition.

Thus, Saido's real challenge is not whether there is anyone to assist, but to what extent they will assist.

Seres assists because it needs to provide new avenues of imagination beyond Aito, such as a lower-cost intelligent route, products more tailored for overseas markets, and more flexible equity and industrial synergy. But 'assisting a bit' and 'going all in' are two distinct approaches.

Doubao assists because the automotive cockpit is one of the easiest scenarios for large models to weave a compelling tale. However, with over 90% of mainstream automakers already partnering with Volcano Engine, Saido is far from unique.

This leaves Saido with an inherent sense of contradiction from the outset: it needs Seres' manufacturing capabilities but cannot expect Seres to treat it like Aito; it needs intelligent suppliers to provide selling points, but suppliers won't shoulder the sales burden for it; it needs state-owned resources, but resources do not equate to market success.

Changing Landi to Saido is not merely a name change—it's also a shift in direction, but the question remains unanswered:

Who, precisely, is the 'primary responsible entity' for this vehicle?

02 The Last Brand with All the Resources Was Called Jiyue

Saido bears a closer resemblance to Jiyue than to Aito.

When Jiyue first emerged, its narrative was equally compelling: Baidu would handle AI, intelligent driving, mapping, and software, while Geely would manage the platform, manufacturing, supply chain, and vehicle engineering. One had the brains, the other had the body—together, they seemed like the ideal partnership for the smart car era.

Jiyue's product strength was undeniable; even nearly two years after its market exit, some owners were still listing their used cars for nearly RMB 130,000, quickly attracting numerous inquiries—a residual value rate even more impressive than some surviving new forces.

But market recognition did not translate into tangible sales—by September 2024, cumulative sales of the Jiyue 01 and Jiyue 07 models stood at a mere 9,767 units.

This was clearly detrimental to the high-turnover, high-supply automotive industry. By the end of 2024, Jiyue began seeking new financing, merging redundant departments, cutting projects that couldn't contribute financial returns in the short term, and faced employee wage disputes and supplier payment pressures, ultimately fading from the market.

This is Saido's greatest challenge.

Many new brands love to boast about their resources at the outset: who provides intelligent driving, who provides the cockpit, who provides the batteries, who provides manufacturing, who provides funding, who provides distribution channels. It seems like every piece has an owner, and the whole vehicle will naturally come together.

But a car is not a product you can rush to market by simply attaching four wheels to a large smartphone.

Consumers won't place orders just because your supplier list is extensive, nor will they pay deposits just because your shareholder background is strong. What users truly care about when purchasing a car is whether it's worth the money, reliable, who will handle repairs, and who will still be around years later.

Baidu's AI capabilities were commendable, and Geely's car-building capabilities were equally impressive. The issue was that Jiyue, as a brand, failed to translate these capabilities into stable sales, user perception, and sustainable operating capabilities. Once sales didn't pick up, financing, organizational, employee, and supplier issues all surfaced simultaneously.

Saido now finds itself at a similar crossroads.

It also boasts an impressive resource list: Seres provides the manufacturing foundation, Yuanrong Qixing provides intelligent driving, Yitu Technology handles the cockpit, Doubao offers AI imagination, related parties of CATL provide industrial credibility, and Chongqing state-owned capital offers shareholder endorsement. Each of these can be showcased in a launch event PPT, but making it onto the PPT is not the same as making it into orders.

What Saido truly needs to address is not 'who is behind me,' but 'who is ultimately responsible for me.' Who defines the product, who sets the price, who handles distribution, who manages after-sales, who continues to invest when sales fall short of expectations, who steps up when the market raises doubts.

These questions cannot be answered by state-owned capital, Volcano, suppliers, or now, probably not even by Seres, which has relinquished its controlling stake.

This is the distinction between a 'resource medley' and a 'true automaker.' A resource medley may appear to have everything, but under pressure, everyone can take a step back; a true automaker must have someone step forward.

Thus, what Saido's launch event truly needs to address is not just what the first model looks like, how it's priced, or whose intelligent driving and cockpit it uses. It must answer a much simpler question:

Saido, whose offspring is it, truly?

- END -

-

![]()

Qianwen’s Version of ‘Being Inside the Nails’

-

![]()

Unbelievable! Chery’s Rumor Refutation Disappears—Who’s Behind the Chaos?

-

![]()

Force Robotics Acquires Atomix: Empowering Robots to Develop Data Flywheels in Real-World Business Environments

-

![]()

Is India Acquiring Electric Vehicle Tech from China? Chery Responds

-

![]()

Struggling to Compete? Japanese Automakers Shift Focus to India, a Market Even Musk Avoids

-

![]()

Why Haven’t We Seen Any Automakers Go Bankrupt Yet, Even as 2026 Reaches Its Midpoint?

-

![]()

Saido Is in Need of a 'Primary Responsible Entity'

-

![]()

Shanghai Robot Brain’s Debut Share: Second Bid for HKEX Listing