Why Haven’t We Seen Any Automakers Go Bankrupt Yet, Even as 2026 Reaches Its Midpoint?

06/09 2026

06/09 2026

515

515

Introduction

Introduction

Zhu Jiangming and He Xiaopeng have both raised a pertinent question: How many Chinese auto brands will ultimately weather the storm?

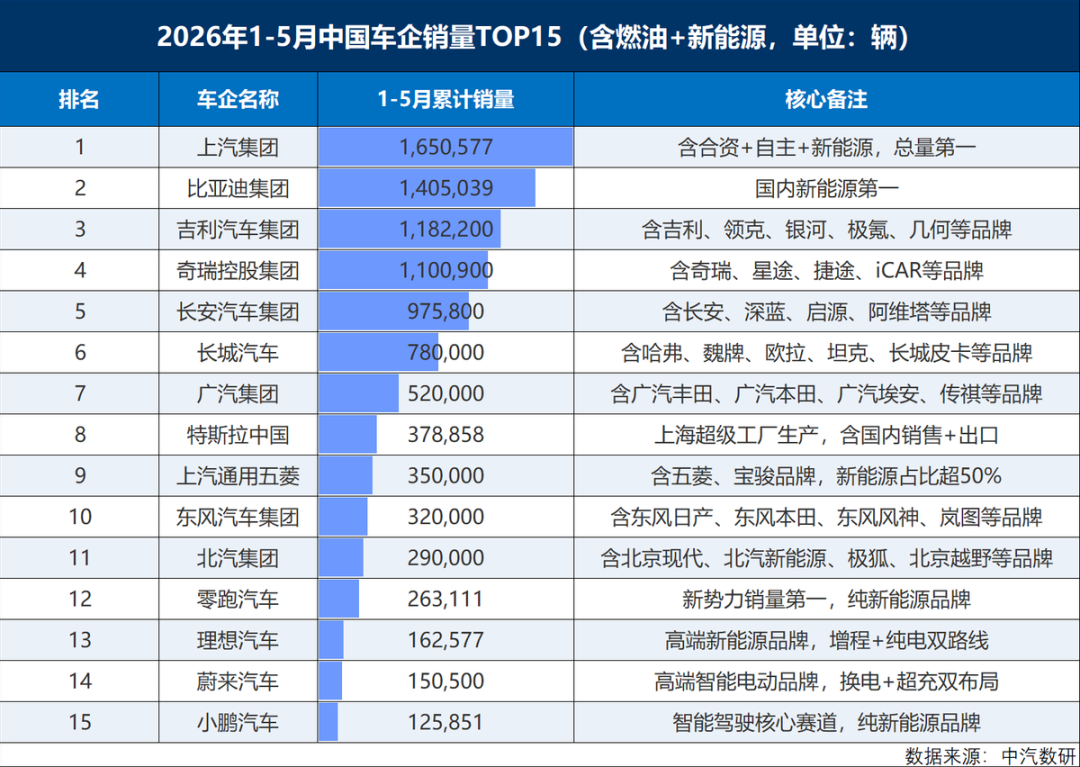

Since 2026, China's automotive market has encountered some challenges. According to data from the China Passenger Car Association (CPCA), retail sales of domestically produced narrow passenger vehicles reached 1.51 million units in May, marking a year-on-year decline of 22.1%. This represents the second consecutive month with a drop exceeding 20%.

The sustained significant declines have resulted in total retail sales of domestically produced narrow passenger vehicles from January to May this year amounting to 7.099 million units, with the year-on-year decline widening to 19.5%.

In layman's terms, competition in the automotive market has intensified, with cars not selling as well as before; consumer demand for purchasing vehicles has also become more sluggish, with fewer people buying cars.

To conceal their growing anxieties, all automakers are continuously launching new models and attempting to use "busyness" as a countermeasure against the overall market decline.

Large six-seater flagship SUVs are flooding the market, joint ventures are also "breaking with tradition" by producing extended-range vehicles, and various boxy off-road vehicles, along with similar-looking GT shooting brakes, are emerging. In short, the market is bustling but also exhausted.

However, beyond these relatively superficial efforts, there is another narrative unfolding in China's automotive market:

FAW Xiali, Brilliance Auto, Zotye, Leopaard, Lifan, Huatai, BAIC Yinxiang (Huansu), and Haima Automobile, which has fully withdrawn from the domestic market, are not included in the latest list of motor vehicle manufacturers released by the Ministry of Industry and Information Technology.

These eight auto brands, which once left a significant mark in China's automotive history, have quietly faded away in the fierce torrent of the new energy vehicle era.

Unlike the sudden collapses of Jiyue and Ziyoujia, these brands had already disappeared from public view for some time.

Abandoned by the times, they are more like entities in a "vegetative state," kept alive by artificial means; now, at this juncture, that artificial support has suddenly dissipated.

Many people applaud the accelerated elimination of such auto brands. They believe that there are too many domestic auto brands, with severe product homogenization, wasting resources while also creating a chaotic market.

So, the further question arises:

Besides the silent demise of "old and outdated" brands, why hasn't there been a sudden "collapse" of any automaker this year, despite the market's poor performance and multiple pressures?

01 Automaker Reshuffle: The Industry Has Long Predicted This

When we extend the timeline, it becomes apparent that there truly aren't many new developments under the sun. As early as 17 years ago in 2009, Sergio Marchionne, CEO of Fiat Chrysler Automobiles (FCA), made a prediction:

In the future, there may only be six automakers worldwide: one American company, one German company, one European-Japanese alliance, one Chinese company, one Japanese company, and one potential European company.

Today, in China's automotive industry, the notion of only a select few automaker brands surviving is also very prevalent.

"Future competition will be even fiercer than today. In the next five years, only about five Chinese brands may survive in the Chinese market, while those ranked sixth to tenth may survive but not thrive."

At the 8th Global Automotive Forum closing plenary session in 2017, Zhu Huarong, then president of Changan Automobile, made a "radical" judgment.

In fact, from another perspective, if it weren't for the "delay" caused by the pandemic a few years ago, which postponed the "final battle" in the automotive market, Zhu Huarong's prediction might have already come true by now.

Now, with the continuous expansion of the new energy vehicle market and the sustained "fierce attacks" from cross-industry newcomers like Huawei and Xiaomi, China's automotive industry is also facing many "uncertainties."

In 2022, before the launch of Xiaomi's first car, Lei Jun had publicly declared on social media:

"When the electric vehicle industry matures, the top five global brands will occupy more than 80% of the market share. The only way for Xiaomi Auto to succeed is to become one of the top five and ship more than 10 million units annually. Competition will be brutal."

Xiaomi Auto's excellence is evident to all. However, when it comes to the maturity of the electric vehicle industry, Lei Jun himself probably didn't expect that this day would come so quickly.

Data from the CPCA shows that the average penetration rate of new energy passenger vehicles from January to May this year was 52.2%. In May, it climbed to 63%, setting a new monthly record; among them, pure electric models accounted for 68%, indicating the accelerated arrival of the pure electric vehicle era.

On one hand, new energy vehicles are "advancing rapidly," while on the other hand, the overall automotive market is sluggish. In this contradictory automotive landscape, the logic of competition has changed—it's no longer a "welfare game" where everyone does well, but a bloody struggle for survival.

02 Zhu Jiangming and He Xiaopeng Are Also Warning

"Now, when all the chairmen of Chinese automakers meet, there are only 17 of them. In fact, China can't accommodate 17. The opponents are getting stronger, and the weak ones are being eliminated, leaving only the strong."

In March this year, Zhu Jiangming, founder, chairman, and CEO of Leapmotor, expressed his views on the large number of Chinese auto brands during a group interview after the launch of the Leapmotor A10.

A month later, during a group interview at the launch of the Leapmotor D19, Zhu Jiangming once again bluntly stated:

"Six new models are being launched tonight, so can you say it's not intense competition? It really is! Because of the fierce competition, the knockout phase hasn't ended yet. We believe the next two to three years will be the norm."

"Making cars is really difficult. I believe that in two to three years, we won't see six new models launched in a day. This is a process of regression through competition."

Although Zhu Jiangming's hints are not overt, please note that this doesn't mean automakers will be out of the woods after surviving these two to three years. With intense market competition, auto brands will accelerate their elimination, and the final battle will also determine the winners in the coming years.

Regarding the winners, the current consensus in the industry is "five." For example, in a recent interview, He Xiaopeng reiterated the "five" argument:

"By 2030, there may only be five large-scale automotive companies left in China. This doesn't mean other companies will go bankrupt, but the decline in scale will make it increasingly difficult to enter ultra-high-intensity competition."

Earlier this year in May, He Xiaopeng spoke even more bluntly at the "18th XuanYuan Automotive Blue Book Forum":

"Most brands operating in the Chinese market, including foreign ones, will be eliminated. In the future, there will probably be around five Chinese automakers with significant sales volumes."

Some may think He Xiaopeng is exaggerating or deliberately creating industry anxiety to push weaker brands out.

But the reality is clear: today's automotive market can no longer accommodate so many automakers, nor does it need a large number of visually and functionally similar products.

Evidently, the decline in automotive market sales this year is just a prelude to the final battle.

As Li Bin of NIO said, the upcoming brand confusion period will transition into a brand clarification period, moving from single-point competition to systematic competition, where R&D, supply chain, manufacturing, quality, and customer service are all indispensable.

03 Which Auto Brands Will Be Eliminated?

According to estimates by consulting firm AlixPartners, in the coming years, 15 automaker groups will monopolize most of the industry's profits. These 15 brands will occupy 75% of China's new energy passenger vehicle market share, with annual sales reaching 1.02 million units.

From a sales ranking perspective, even strong new forces like NIO, Leapmotor, Li Auto, and XPENG are only barely among the top 15.

According to incomplete statistics, by the end of 2025, there will be 129 pure electric and plug-in hybrid vehicle brands competing in the Chinese market.

Of course, there are some "historical issues" at play here. After all, the government provided substantial subsidies in the past, leading to a surge in the number of auto brands. Additionally, the bubble in the number of brands from automakers like FAW Xiali, Brilliance Auto, and Zotye is evident.

So, returning to our initial question, why hasn't there been a collapse of any automaker when 2026 is half over?

Firstly, it's certain that some brands are silently dying, without even a single announcement or farewell letter, leaving only the owners to bear the consequences. Although they may have been glorious in the past, they ultimately couldn't withstand the trend of the new energy vehicle era.

Secondly, new forces like NIO and WM Motor, which have some backing, are not without the possibility of "rebirth." Recently, rumors circulated that Shanshi Hi-Tech would take over NIO, causing its stock price to soar.

However, capital takeovers are only a means of extending life and cannot address core shortcomings. In today's highly competitive new energy sector, lacking technological barriers and weak product iteration make it difficult to regain peak performance even with financial support.

Moreover, many "zombie automakers" that rely on local resources are also awaiting elimination. These brands are deeply tied to local state-owned assets, production capacity, land, employment, and taxation, with complex interest relationships.

To revive idle production capacity, stabilize employment, and avoid asset bad debts, local governments often delay their exit through financial relief, policy support, and resource integration, artificially prolonging the industry reshuffle period. This is the core reason for the "seemingly collapse-free but actually continuous elimination" in the automotive market.

But market laws never fail, and policy support can only delay the outcome, not reverse it.

Before 2030, there may not be another dramatic wave of collapses, but continuous silent eliminations will certainly occur. After all, among the so-called 129 brands in chaos, no more than 20 truly have combat effectiveness.

Editor-in-Chief: Cao Jiadong Editor: He Zengrong

THE END

-

![]()

Qianwen’s Version of ‘Being Inside the Nails’

-

![]()

Unbelievable! Chery’s Rumor Refutation Disappears—Who’s Behind the Chaos?

-

![]()

Force Robotics Acquires Atomix: Empowering Robots to Develop Data Flywheels in Real-World Business Environments

-

![]()

Is India Acquiring Electric Vehicle Tech from China? Chery Responds

-

![]()

Struggling to Compete? Japanese Automakers Shift Focus to India, a Market Even Musk Avoids

-

![]()

Why Haven’t We Seen Any Automakers Go Bankrupt Yet, Even as 2026 Reaches Its Midpoint?

-

![]()

Saido Is in Need of a 'Primary Responsible Entity'

-

![]()

Shanghai Robot Brain’s Debut Share: Second Bid for HKEX Listing