Is India Acquiring Electric Vehicle Tech from China? Chery Responds

06/09 2026

06/09 2026

417

417

A recent Reuters report has sparked significant discussion within China's automotive sector. According to informed sources, India's Tata Motors is planning to adopt the complete vehicle manufacturing platform of China's Chery Automobile, aiming to boost its previously sluggish high-end electric vehicle (EV) development.

Does this imply that Chery Automobile will be transferring new technologies to Tata Motors?

Let's delve into the original Reuters report for clarity. It states:

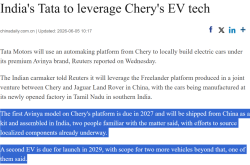

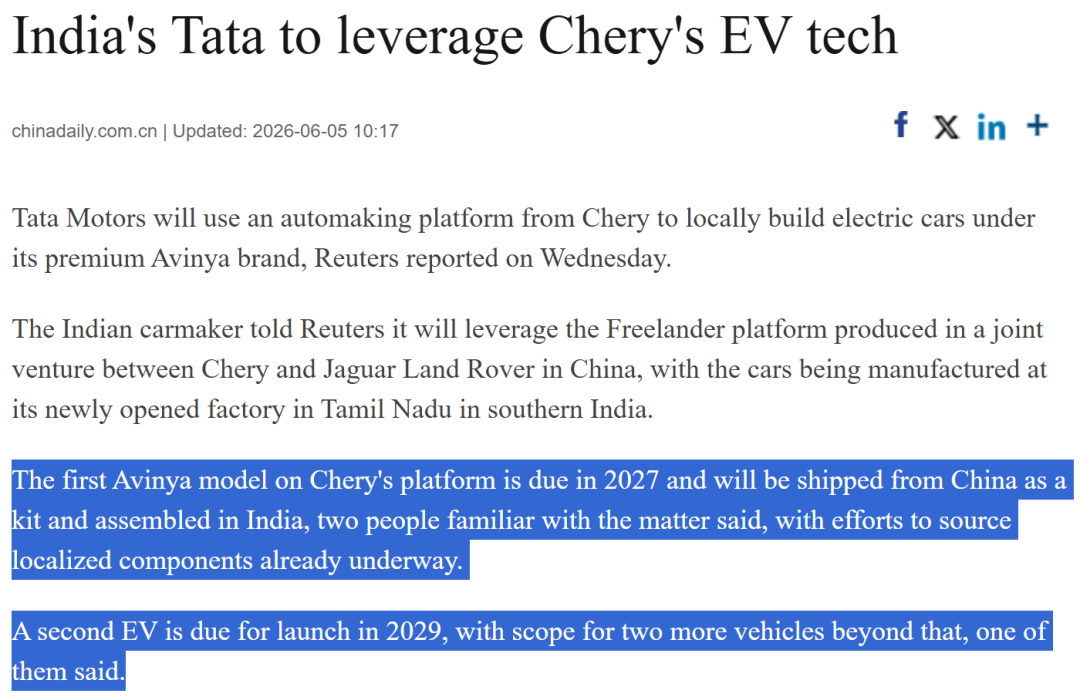

"The inaugural Avinya model, built on Chery's platform, is slated for 2027 and will be exported from China in kit form for assembly in India, with efforts already underway to localize component sourcing. A second EV is expected to launch in 2029, with plans for two additional models thereafter, according to one source."

"Two individuals familiar with the matter revealed that the first Avinya model, utilizing Chery's platform, is set to debut in 2027. The vehicle will be shipped from China to India as a complete knock-down (CKD) kit for assembly, with ongoing efforts to localize component procurement. Another source indicated that a second EV model is planned for 2029, with two more models to follow."

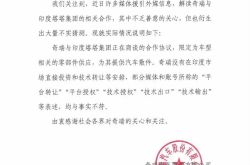

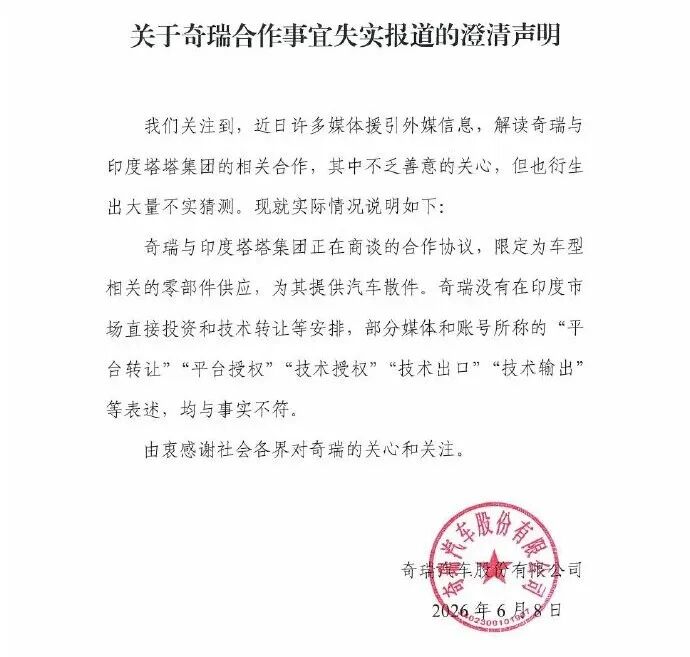

From the Reuters report, it seems Chery intends to export EVs to India in CKD assembly form. In a statement released on June 8, Chery clarified:

Recently, numerous media outlets have referenced foreign media reports to speculate on Chery's collaboration with India's Tata Group. While some coverage reflects genuine concern, it has also led to numerous false assumptions. The cooperation agreement currently under discussion between Chery and Tata Group is strictly confined to the supply of vehicle-related components, specifically automotive CKD kits. Chery has no plans for direct investment or technology transfer in the Indian market. Claims by some media and accounts of "platform transfer," "platform licensing," "technology licensing," "technology export," or "technology output" are all inaccurate.

"Strictly confined to the supply of vehicle-related components, specifically automotive CKD kits." Chery's statement aligns with Reuters' report of "as a kit and assembled in India." Thus, accusations that Chery is voluntarily "exporting technology" to India are indeed baseless. But does this mean Chery's cooperation with Tata will proceed without a hitch?

Let's consider the "precedent" in the photovoltaic (PV) sector.

Public records indicate that India initially had minimal PV manufacturing capacity, relying solely on the installed market. In 2015, during Modi's visit to China, Trina Solar signed a memorandum of understanding (MoU) to establish a 1GW manufacturing plant in India, marking the first significant Chinese investment in the Indian PV sector. In 2018, Sungrow Power Supply constructed a 3GW module factory in Bangalore, sourcing equipment, technology, and personnel from China. Subsequently, numerous Chinese companies, including Longi, JA Solar, Canadian Solar, Microtech, and Jinergy, followed suit. India's PV manufacturing industry gradually took shape.

Unexpectedly, in 2022, India tightened its policies, imposing a 40% tariff on Chinese PV modules and a 25% tariff on Chinese PV cells. It also introduced the Approved List of Models and Manufacturers (ALMM), mandating that only domestically manufactured components could be used in government projects and large-scale power plants, effectively excluding Chinese products. Chinese PV companies faced a dilemma: either withdraw their investments, rendering previous efforts futile, or retain their production lines, technology, and personnel in India to continue operations. Given severe overcapacity in China and the imperative to survive, the vast majority of Chinese companies chose the latter.

From 2022 to 2025, India began purchasing large quantities of critical equipment from China and made significant efforts to promote PV technology localization, ultimately establishing a complete PV manufacturing supply chain.

Coupled with India's anti-dumping measures and U.S. tariffs, China's PV industry faced substantial challenges in the global market. Although the U.S. later imposed high tariffs on Indian PV products as well, this had already diverted a significant portion of the global market share that once belonged to China.

Data reveals that India's PV module production capacity surged from 30GW in 2022 to 172GW by March 2026, a 17-fold increase in eight years, making it the world's second-largest producer. Indian companies such as Reliance and Adani now use Chinese equipment, processes, and engineers to manufacture products labeled "Made in India," competing with Chinese firms for global orders, particularly in the U.S. market.

This is the tale of "cooperation" between India and China in the PV sector. In fact, India has employed similar tactics in other industries, including consumer electronics (e.g., smartphones), ultra-high-voltage/power equipment, batteries, energy storage, and even tunnel boring machines and pharmaceuticals. In some cases, India has successfully acquired key technologies from China.

Today, Chery's announcement of cooperation with India's Tata Motors, albeit in the form of "CKD assembly," bears some resemblance to the 2015 MoU between India and Trina Solar.

Public records show that the 2015 MoU between Trina Solar and India aimed to establish a "vertically integrated manufacturing park" with 1GW of cell and 1GW of module capacity. However, this cooperation never fully materialized; Trina Solar only built a small-scale module CKD assembly line in India, continuing to import critical components such as wafers and cells from China. Nevertheless, this did not prevent India from later comprehensively acquiring some key technologies from China's PV industry and capturing a portion of the global market share.

Today, similar to the PV industry, China's automotive industry is also contending with underutilized capacity and intense competition. Data from 2025 indicates that China's automotive industry capacity utilization stood at 73.20%, operating within the "yellow zone" (a warning level).

According to incomplete statistics, approximately 544 new vehicle models were launched in China from January to May this year, several times more than in the European market. Even when considering only all-new or fully redesigned models, there were still 107 launches—an astonishingly high density.

In terms of sales, Chinese automakers are accelerating their overseas expansion. Taking Chery as an example, the group sold 1.1009 million vehicles from January to May this year, with exports accounting for over 68% (752,700 units). In May alone, Chery sold 247,800 vehicles, including 181,800 in overseas markets and only 65,900 domestically. Given this sales breakdown, establishing more overseas factories, such as CKD plants, appears to be the best and most economically rational choice for Chinese automakers like Chery.

Data shows that Chery currently operates 12 production bases in China and approximately 16 overseas, including wholly owned, joint venture, and CKD assembly facilities, spanning about 12 countries. If Chery's cooperation with India materializes, it will mark the establishment of Chery's 13th overseas production base.

Given China's rapidly rising automotive industry—which surpassed Japan in export volume in 2023 to become the world's largest—and India's massive population and potential consumer market, the cooperation between Chery and Tata Motors seems like an excellent deal from any perspective. The only concern is that Chery's partner this time is India.

Although Chery has stated that the cooperation with Tata Motors does not involve "technology transfer," there remains apprehension about whether India's broader ambitions toward China's automotive industry might exploit this partnership to gain a foothold, ultimately replicating the PV industry scenario and seizing a portion of China's market share.

-

![]()

Qianwen’s Version of ‘Being Inside the Nails’

-

![]()

Unbelievable! Chery’s Rumor Refutation Disappears—Who’s Behind the Chaos?

-

![]()

Force Robotics Acquires Atomix: Empowering Robots to Develop Data Flywheels in Real-World Business Environments

-

![]()

Is India Acquiring Electric Vehicle Tech from China? Chery Responds

-

![]()

Struggling to Compete? Japanese Automakers Shift Focus to India, a Market Even Musk Avoids

-

![]()

Why Haven’t We Seen Any Automakers Go Bankrupt Yet, Even as 2026 Reaches Its Midpoint?

-

![]()

Saido Is in Need of a 'Primary Responsible Entity'

-

![]()

Shanghai Robot Brain’s Debut Share: Second Bid for HKEX Listing