In 2026, Capital is Pricing AI Companies 'Along Industrial Clusters'

04/30 2026

04/30 2026

576

576

For investors, investing in AI has shifted from focusing on models, teams, and narratives to evaluating whether companies can integrate into real industrial systems and achieve implementation through regional supply chains, scenarios, and data. For companies, developing AI is no longer just about creating a technical product but finding the real entry point for integrating industry and AI to enter a system capable of continuous iteration, delivery, and scaling.

The AI industry has entered a phase of 'competition in implementation, delivery, and compound returns.' While AI detached from industrial contexts can still tell compelling stories, companies that truly endure across cycles tend to emerge from regions with the densest industrial clusters and deepest industrial collaboration.

Author | Dou Dou

Editor | Pi Ye

Produced by | Industrial+

In 2026, capital is re-pricing AI companies along industrial clusters.

According to IT Juzi's Q1 venture capital data, 2,865 financing events occurred in Q1 2026, up 2.5% quarter-over-quarter and 52% year-over-year. Transaction volume reached RMB 256 billion, up 11.4% QoQ and 48% YoY.

However, capital distribution is contracting simultaneously.

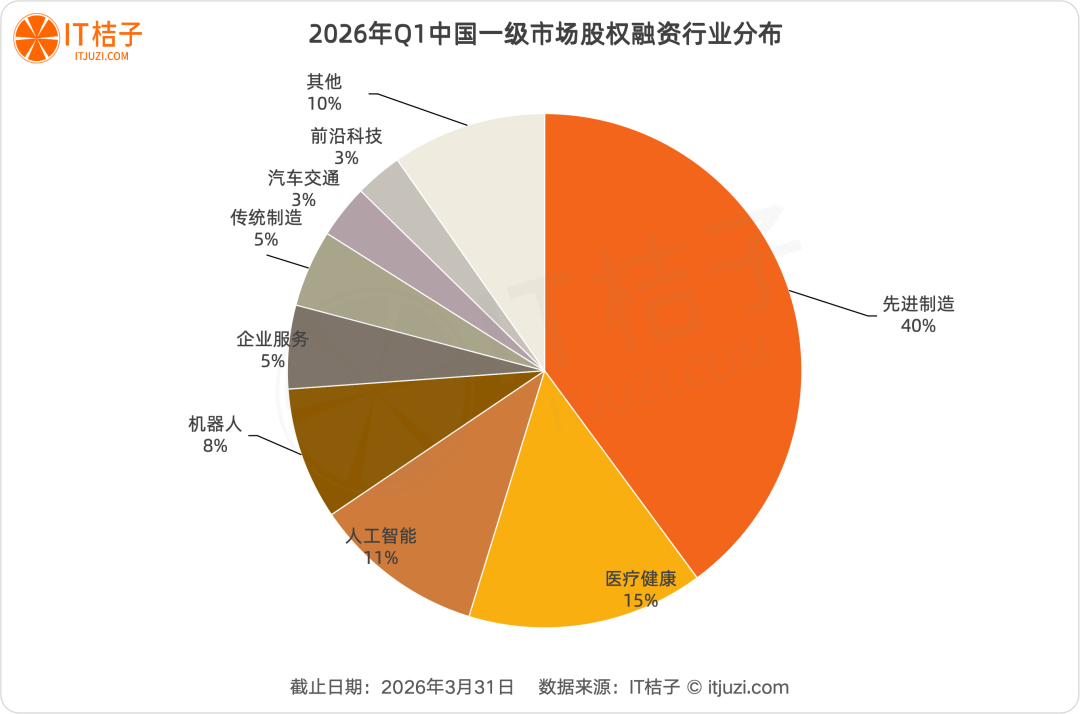

From a sector perspective, advanced manufacturing dominated with 40% of events, becoming the most capital-attractive sector. AI ranked third with 11% of events. This reflects the deep integration of traditional manufacturing with AI and IoT driven by intelligent upgrading demands, forming an 'advanced manufacturing+' investment logic.

Geographically, concentration is more pronounced. Guangdong, Jiangsu, Beijing, Zhejiang, and Shanghai accounted for 74.5% of financing events and 76.3% of financing volume, maintaining high regional concentration in venture capital activities.

At first glance, this appears to be capital doubling down on leading cities. However, a closer look reveals it's not merely a siphoning effect of tier-one cities. Capital is not indiscriminately flowing to big cities but is being allocated more precisely along different industrial belts.

For example, Beijing captures model, algorithm, and high-valuation projects. Shenzhen-Dongguan absorbs robotics, embodied AI, and smart hardware. Suzhou-Shanghai undertake (this Chinese term means "takes on" or "inherits") industrial AI, automotive AI, and enterprise intelligence. In other words, capital now focuses not on 'city tiers' but on the industrial ecosystems behind these cities.

The question arises: What changes have occurred in capital's investment logic in AI? Why has a technology sector that could be highly de-regionalized in the internet era become increasingly reliant on a few industrial belts and urban clusters in the AI era? What changes will traditional industries undergo under this new investment logic?

I. Capital Increasingly Values 'Industrial Networks'

A fact is that AI funding is concentrating along industrial belts, and this concentration is not limited to the financing side.

The 'China Unicorn Enterprise Development Report 2026' shows that as of December 2025, China had 416 unicorn companies, accounting for nearly 30% of the global total and ranking second globally. Hard tech, represented by AI, occupies the most prominent 'C-position' among unicorns. In 2025, the AI sector led with 69 companies and a valuation of USD 638 billion, averaging nearly USD 10 billion per company.

Notably, over 85% of AI unicorns are distributed across the Beijing-Tianjin-Hebei, Yangtze River Delta, and Guangdong-Hong Kong-Macao Greater Bay Area urban clusters.

When financing and leading companies simultaneously contract toward the same regions, explaining this as mere 'coincidence' becomes untenable. The question then becomes: What are capital players seeing in these locations?

Shifting the perspective from 'cities' to 'industrial structures' provides clearer answers. Today's AI landscape is essentially reshaped by several core industrial clusters.

Beijing is a quintessential 'technology-origin cluster.' According to the 'Beijing AI Industry White Paper (2025),' the city's AI core industry scale reached RMB 215.22 billion in H1 2025. By end-2025, Beijing housed over 2,500 AI companies and had 183 registered large models, both national tops. Companies like Zhipu AI, Moonshot AI, and Guanglun Intelligence gather (this Chinese term means "gather" or "cluster") here. This results not just from corporate choices but from the spillover effects of long-term accumulations by Tsinghua University, Peking University, and top-tier research resources, gradually forming a complete chain of 'basic research—model training—application spillover.'

Shanghai is the national hub for AI chip companies, hosting the 'GPU Four Little Dragons': Biren Technology, Enflame Technology, Iluvatar CoreX, and Hanbo Semiconductor (Hanbo Semiconductor).

Shenzhen is a robotics and smart hardware cluster. Companies like DJI, UBTECH, Yuanrong Qixing, and Simbe Robotics benefit from the world's most complete electronic manufacturing supply chain.

Suzhou provides the most typical 'manufacturing scenarios.' With over 1,600 'AI+manufacturing' companies, firms like Jiushi Intelligence, Miga Technology, and AISpeech operate directly alongside production lines. The continuous generation of equipment, process, and production data by thousands of manufacturing companies means AI doesn't need to 'seek scenarios' but naturally exists within them.

Viewing these cities together reveals a commonality: AI companies are not randomly distributed but 'grow' from industrial foundations.

This explains why 'regional concentration' is becoming more pronounced—because industries are essentially screening players.

This point is now explicitly written into capital's investment logic.

According to the 'China Fintech Flame Index Report (2025),' AI companies in the Yangtze River Delta, Beijing-Tianjin-Hebei, and Guangdong-Hong Kong-Macao Greater Bay Area are most attractive to venture capital. Beijing, Shanghai, Hangzhou, and Shenzhen lead in AI venture capital deals.

From this perspective, 'regional binding' of AI companies is actually dependence on industrial clusters. Stronger clusters make it easier for AI companies to access data, scenarios, supply chains, resources, and financing. As capital clusters further, AI companies become increasingly tied to these regions, forming an irreversible pattern of 'strong industrial clusters—AI company concentration—highly concentrated financing.'

A forming consensus is that capital now values not just the companies themselves but the 'industrial networks' behind them.

II. Industrial Clusters: The 'Shortest Physical Path' for AI Commercialization

Why has the investment logic for AI companies changed in this way?

A fundamental shift is occurring: AI is transforming from a 'pure software industry' into a 'semi-real economy' increasingly dependent on the physical world.

In the internet era, software could grow independently of specific scenarios—build products first, then find users. In the AI era, merely developing models is insufficient. They must enter real business processes, undergo repeated calls and continuous validation, and ultimately achieve delivery.

In other words, AI's value no longer lies in whether it can be built but in whether it can operate in the real world and continuously produce results.

This is why capital's evaluation criteria have shifted from 'investing in technological possibility' to 'investing in implementation certainty.' Once implementation becomes the focus, the value of industrial clusters emerges—most visibly in supply chains.

Take the embodied AI sector as an example. Shenzhen's 'Robot Valley' has formed a complete ecosystem spanning sensors, LiDAR, servo systems, 3D vision, and complete machine manufacturing (complete machine manufacturing). Companies like UBTECH, RoboTerra, and RoboSense cluster in the same region, where 'upstairs and downstairs are upstream and downstream,' and industrial parks function as industrial chains.

Dongguan's Songshan Lake complements this by bridging the gap from R&D to productization. XbotPark's shared factory integrates CNC machining, prototyping, trial production, and supply chain organization, offering one-stop manufacturing capabilities from prototypes to products to commodities. In other words, leading companies maintain their edge not just through laboratory model capabilities but through Shenzhen's core component clusters, Songshan Lake's engineering and prototyping capabilities, and the iterative speed supported by the Pearl River Delta's extensive manufacturing scenarios.

Digging deeper, we reach data.

While it's widely believed that AI relies on data and industrial clusters possess data, the critical factor is whether data comes from real, continuous, and repeatedly callable scenarios.

Suzhou's industrial AI exemplifies this. Its core strength lies not in algorithmic superiority but in manufacturing clusters providing continuously operating real-world scenarios. Through industrial internet, smart manufacturing systems, and extensive digital production lines, equipment, process, and production data are continuously generated during real production and repeatedly used for model optimization, forming a cycle of 'scenario-driven—data accumulation—model iteration—feedback optimization.'

For example, the rapid implementation of companies like Jiushi Intelligence highly depends on the real-world scenarios provided by Suzhou Industrial Park. There, its autonomous delivery vehicles conduct regular testing and operations on open roads. These complex road conditions and high-frequency scheduling scenarios continuously provide real data inputs for models. Teams relying solely on historical or simulated data struggle to achieve this continuous iteration capability.

Moreover, data's value lies not in scale but in its binding to specific industrial scenarios. For instance, Dalang Town's knitwear industry bases its AI applications on highly concentrated design styles, production processes, and supply chain data deeply coupled with the local industrial system. Once detached from the cluster, this data's value rapidly declines. Similarly, Ningbo-Zhoushan Port's AI capabilities must attach to real port scheduling, loading/unloading, and shipping scenarios to maximize effectiveness.

This explains why AI companies cluster within industrial zones and why capital heavily invests in AI firms along industrial belts.

Regional concentration isn't a revival of geographic fetishism but capital's search for the shortest path to AI commercialization. Industrial clusters provide this 'shortest physical path.'

III. In the AI Era, New Industrial Belts Begin to Form Closed Loops

Traditionally, AI's relationship with industrial belts was seen as technology attaching to traditional manufacturing to enhance efficiency, optimize processes, or upgrade products.

In the AI era, this relationship is transforming. AI is no longer just an add-on to traditional industries but a core variable restructuring industrial chains and reshaping value chains. In other words, AI is no longer simply attaching to old clusters but driving the birth of new clusters and revitalizing traditional industrial belts.

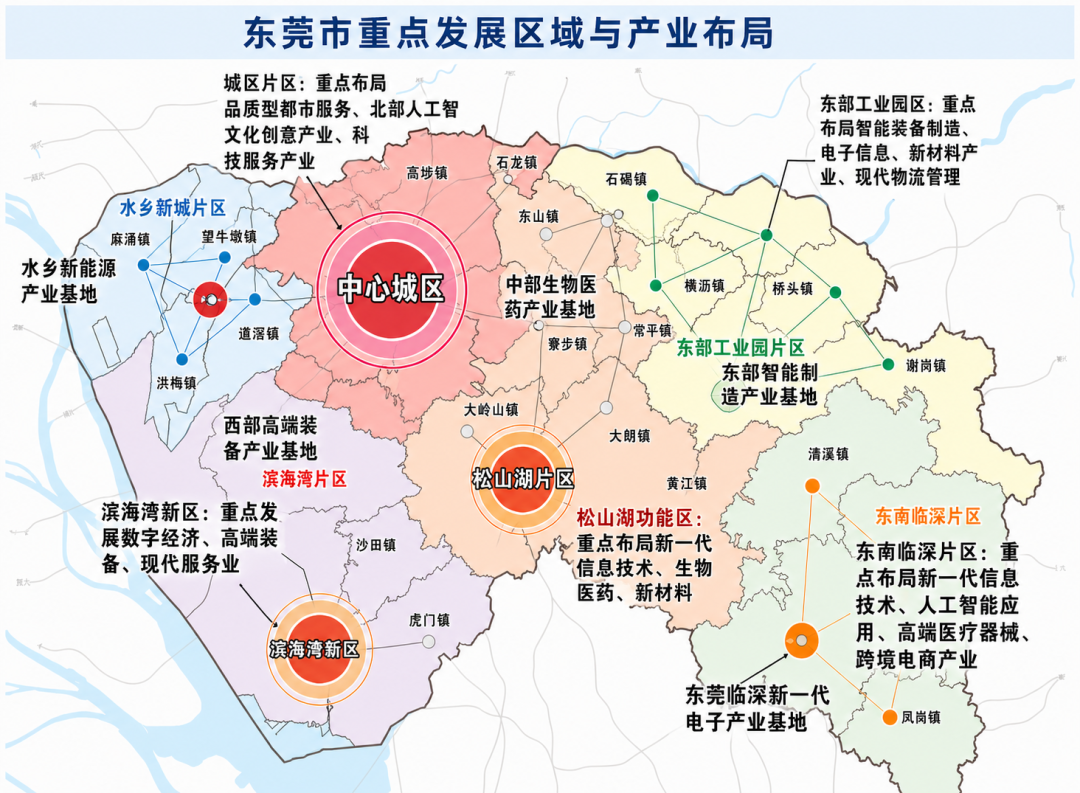

Dongguan exemplifies this transformation.

Historically, Dongguan played the 'world factory' role, growing through low-cost labor, land, and contract manufacturing to become a critical node in global manufacturing chains. However, rising labor costs, relocation of low-end manufacturing, and shrinking profit margins in traditional contract manufacturing once pressured Dongguan toward industrial hollowing—factories remained, orders persisted, but industrial added value and growth momentum localized elsewhere.

Now, AI is revitalizing Dongguan.

In Q1 2026, Dongguan's embodied AI sector saw 12 financing events totaling RMB 2.1 billion. Songshan Lake High-Tech Zone has gathered over 300 robotics and AI companies, gradually forming a complete chain from core components and complete machine manufacturing to system integration.

The key change is that Dongguan is no longer just contract manufacturing for others but has become a core link in the AI hardware and embodied AI industrial chain. Former contract manufacturers now supply robot joints, motors, sensors, controllers, and other critical components. Their once-singular 'processing' capabilities have upgraded to integrated 'R&D+manufacturing+delivery' competencies.

Similar transformations are occurring in Foshan's industrial belt.

Foshan has long been one of China's most mature home appliance industrial belts, with a complete manufacturing system, stable supply chains, and numerous leading companies. However, its maturity also brought persistent challenges: products became increasingly homogenized, markets more competitive, and enterprises easily trapped in price wars. Relying solely on manufacturing efficiency and channel capabilities could no longer create differentiation.

Today, traditional products like refrigerators, air conditioners, and washing machines are evolving from one-time delivered hardware into continuously online, user-demand-understanding, and service-experience-optimizing smart terminals. Consequently, Foshan's home appliance industry's value center of gravity (this Chinese term means "center of gravity") is shifting from manufacturing toward software, data, and services.

The result is that Foshan's home appliance industry no longer competes solely on scale and cost but has opportunities to leverage AI for high-end, intelligent, and branded development, gradually activating growth across the traditional home appliance industrial cluster.

From Dongguan to Foshan, a clearer trend emerges: AI's impact on traditional industrial belts has shifted from 'empowerment' to 'restructuring.' On one hand, it helps the least profitable and most substitutable links in original industrial chains find new positions. On the other, it drives traditional industrial belts toward a new model integrating 'technology, products, and services.'

While land, labor, and costs once determined a city's industrial status, success now increasingly depends on integrating AI into its core industrial systems.

This means that by 2026, AI industry competition will evolve from technological rivalry to industrial cluster competition.

For investors, investing in AI has shifted from focusing on models, teams, and narratives to evaluating whether companies can integrate into real industrial systems and achieve implementation through regional supply chains, scenarios, and data. For companies, developing AI is no longer just about creating a technical product but finding the real entry point for integrating industry and AI to enter a system capable of continuous iteration, delivery, and scaling.

The AI industry has entered a phase of 'competition in implementation, delivery, and compound returns.' While AI detached from industrial contexts can still tell compelling stories, companies that truly endure across cycles tend to emerge from regions with the densest industrial clusters and deepest industrial collaboration.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!