After the Demo: The Next Trillion-Dollar Track for Humanoid Robots Lies Neither in the Brain Nor in the Body

05/22 2026

05/22 2026

618

618

This is my 417th column article.

On May 6, Xinhua News Agency released a set of photos showing 140 humanoid robots from different brands, including Unitree, ZhiYuan, and Leju, receiving training in a facility located above a 4S store in the AI Tech Park of Zhengzhou Central Plains Sci-Tech City.

Trainers are teaching them hand-by-hand how to pick items from supermarket shelves, perform precision assembly on production lines, and fold clothes in simulated home environments. This 4S store combines sales, leasing, maintenance, customization, and data training under one roof.

This news may contain a severely underestimated signal for 2026: The humanoid robot industry is developing a new set of infrastructure. Its importance may surpass that of all the VLA (Vision-Language-Action), world models, and dexterous hands currently being pursued.

The next trillion-dollar track for humanoid robots may lie neither in the brain nor in the body. In this article, let's explore this together.

The Real Issue Lies in Continuous Operation Capability

From 2025 to the first half of 2026, public discourse around humanoid robots has focused on three things: how versatile the models are, how dexterous the bodies are, and how much data is available.

But the most sober (sober-minded) practitioners in the industry are asking a different question.

Liu Yang, co-founder of Infiforce, once publicly stated: 'Customers ask if the robot can operate continuously in a factory for 3 months or 6 months. Can it reduce costs and increase efficiency? Can it be repurchased? Honestly, no company in the industry has fully passed this PoC. This is a survival issue.'

This statement highlights a hidden thread that everyone is avoiding: The bottleneck in transitioning from demonstration to deployment is continuous operation capability.

The data is cold. BMW deployed two Figure 02 robots in its South Carolina plant over 11 months, accumulating 1,250 hours of operation and participating in the production of 30,000 X3 vehicles while handling 90,000 sheet metal parts. This is the best result disclosed in the entire industry.

However, the standard for automotive manufacturers to accept a new robot platform is an average time between failures exceeding 50,000 hours. Dividing 1,250 by 2 and then by 50,000 equals 1.25%. The best result has only completed one-eightieth of the industrial standard.

An even more sobering fact emerged in May 2026 during a pilot at Japan Airlines' Haneda Airport, where Unitree robots could only operate for 2-3 hours on a single charge.

Meanwhile, the industry generally acknowledges that humanoid robots still lag significantly in industrial reliability. Traditional industrial robots from FANUC, ABB, and KUKA can achieve 95-99% uptime on well-maintained production lines, whereas current mainstream humanoid robots require recharging or human intervention after 30-90 minutes of continuous operation in most scenarios.

Why can't algorithms alone bridge this gap? While algorithms can change daily, improving MTBF from 40 hours to 50,000 hours represents a 1,250-fold engineering chasm. Battery life is governed by physical laws, spare parts supply depends on organizational capabilities, and downtime compensation is a financial issue. None of these can be solved by retraining a VLA model.

Crossing this threshold requires an entirely new set of infrastructure that has never been seriously discussed: training data collection, maintenance networks, spare parts supply chains, insurance products, financial leasing, remote takeover, trainer certification, second-hand refurbishment...

This is the iceberg beneath the surface, yet the entire industry is still competing on who looks shinier above the waterline.

Covering 100 Years of Automotive History in 16 Months

If the real battle lies beneath the surface, the most noteworthy phenomenon in this arena is the nonlinear expansion of domestic 'S stores.'

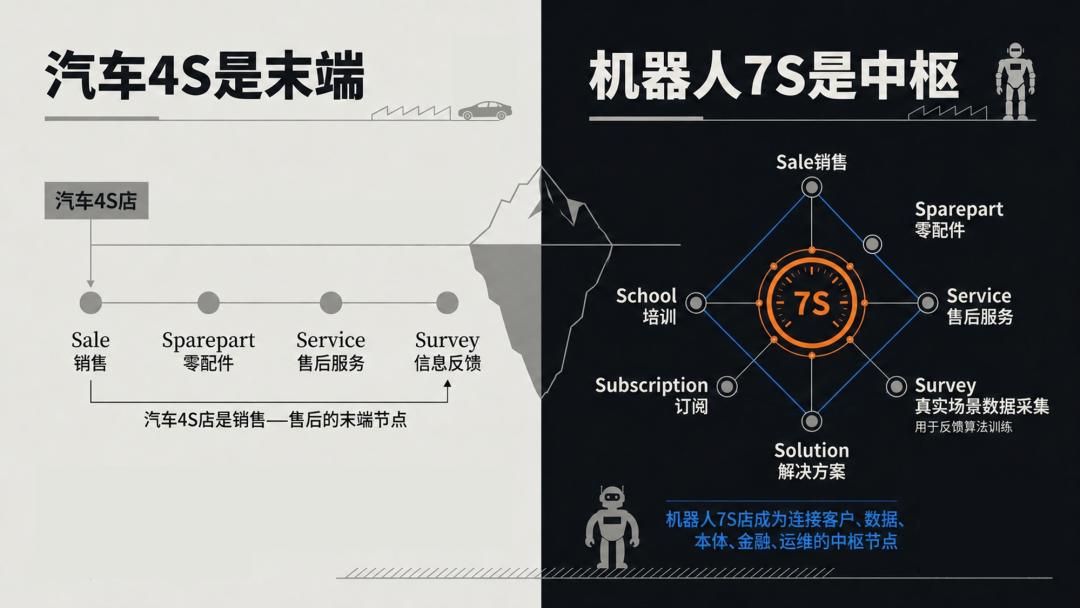

Automotive 4S stores evolved from the first authorized dealerships established by brands like Panhard in late 19th-century France to the standardized four-in-one model (sales, spare parts, service, and survey) that took shape in Asian markets by the 1990s—a process taking nearly a century.

Humanoid robots are evolving at a different pace.

In June 2025, Hangzhou Juwei Technology opened China's first embodied AI 4S store. A month later, Shenzhen Longgang opened the world's first robot 6S store, adding leasing and customization. Another month later, Beijing Yizhuang opened an embodied AI 4S store with integrated financial services including installment plans, loans, insurance, matching, and packaging. In November 2025, Wuhan Optical Valley opened China's first 7S store, incorporating solutions, exhibition, and training into retail nodes. By March 2026, Zhengzhou opened Henan's first heterogeneous 4S store with a front-of-house retail space and back-of-house training facility where 140 multi-brand robots trained in 27 real-world scenarios...

In 16 months, 'S stores' evolved from 4S to 7S. What took the automotive industry a century to achieve, China's humanoid robot industry replicated in just 16 months.

But the real key lies not in the number of 'S stores' but in their functional reversal.

Automotive 4S stores are terminal nodes in the supply chain: selling cars, repairing them, selling spare parts, and collecting feedback—essentially a chain structure from sales to after-sales. Robot 7S stores, by contrast, are central nodes.

The automotive 4S model includes: Sale, Spare part, Service, and Survey.

Robot 7S stores retain four letters from the automotive 4S model, but the meaning of the fourth S, Survey, has completely changed. It no longer refers solely to customer feedback but to real-world data collection that feeds back into algorithm training. Hubei Humanoid completed China's first inter-enterprise humanoid robot training data transaction in early 2026, while the Beijing Humanoid Open Dataset has been downloaded over 2 million times, delivering tens of thousands of hours of real-world robot data.

The three new S's are equally intriguing:

The fifth S stands for Solution.

Customers no longer purchase a robot to figure things out on their own but buy a complete scenario solution. Zhengzhou's 4S store provides 'embodied AI+' packages for supermarket retail, industrial manufacturing, home care, and other fields, while Wuhan's 7S store integrates local supply chains for chips, reducers, dexterous hands, etc., into the store for scenario-based custom assembly. This shifts work previously handled by system integrators to the sales phase.

The sixth S is Subscription.

The Qitian Lease platform initiated by ZhiYuan falls under this category, operating as a 'Meituan + UCar' for robots. Within three weeks of launch, it registered over 200,000 users, averaged 200+ daily orders, connected 600 service providers across 50 cities, and managed 1,000+ multi-brand devices. CEO Li Yiyan projects a market size of 10 billion yuan for 2026. Customers no longer buy a robot but subscribe to capabilities by the day, week, or month.

The seventh S is School.

The Ministry of Human Resources and Social Security has projected that demand for embodied AI roles will exceed 1 million in the next five years. Robot instructors and trainers have emerged as new occupations in CCTV and Xinhua News Agency coverage. A 4S store can house a school on its upper floors, integrating trainer certification, maintenance technician courses, and second-hand refurbishment training.

This system is not merely imitating the automotive model but represents an entirely new industrial metabolic system.

It cultivates organs that took the automotive industry a century to develop—distribution, insurance, leasing, second-hand markets, driving schools, and technicians—simultaneously within 16 months, all positioned adjacent to product sales. Robot 7S stores may skip the traditional paradigm of selling hardware first and services later, directly establishing a new rhythm of 'training + sales + leasing + insurance + services.'

This represents China's most underestimated potential contribution to the global robotics industry—not a specific robot body but an entirely new industrial organizational form.

The Body Manufacturers' Moat May Be Diluting

How will this system rewrite the industry's power structure?

My assessment is that three reverse forces are simultaneously at play.

The first reverse force is the reverse flow of data.

Beijing Humanoid's data hub delivers training data to body manufacturers like Unitree and ZhiYuan; Hubei Humanoid completed inter-enterprise data transactions; JD.com announced plans to build the world's largest embodied AI data collection center.

Body manufacturers are transforming from data producers to data consumers. Those controlling data collection nodes hold the entry tickets to defining general-purpose embodied AI.

Assuming this role are entities like Beijing Humanoid, Hubei Humanoid, Henan Embodied Intelligence, and JD.com—intermediate layers previously overlooked by capital markets.

The second reverse force is reverse pricing of demand.

Qitian Lease's 200,000 users in three weeks, day-by-day insurance premiums, and Wuhan Optical Valley's 5,000 yuan annual premium with maximum coverage of 500,000 yuan have shifted consumer concerns from robot pricing to rental costs, insurance premiums, and downtime duration.

Pricing power has transferred from body manufacturers to combinations of operations, insurance, and leasing. What body manufacturers sell resembles tickets to cash flows from premiums, rentals, and maintenance fees.

The third reverse force is the reverse dilution of brands.

Zhengzhou's 4S store displayed Unitree, ZhiYuan, Leju, and UBTECH robots on its opening day. Qitian Lease manages 1,000+ multi-brand devices. Beijing Humanoid's data hub simultaneously deploys robots from TianGong, TianYi, Aloha, Unitree, Franka, and UR. The automotive 4S model of single-brand stores fails here. Body manufacturers lose brand exclusivity from day one.

The industrial landscape of humanoid robots has always followed an Android model rather than an iOS model. Body manufacturers lack even channel territories, let alone brand premiums.

From this, we can predict that over the next decade, China's humanoid robot industry's largest cash flows may come not from 'selling robots' but from three layers:

Data factor layer (training grounds + data exchanges, the 'Sinopec' of robotics);

Financial factor layer (insurance + financial leasing + RaaS platforms, with Qitian Lease already showing 'Meituan' potential);

Operation and maintenance factor layer (remote takeover + trainers + second-hand refurbishment).

The first Chinese humanoid robot company to reach a market cap of 100 billion yuan may not manufacture robots at all.

Industrial history repeatedly demonstrates this pattern: When a hardware industry enters mass adoption, value systematically shifts from hardware bodies to operation and maintenance networks. There is no reason to believe humanoid robots will be an exception.

Epilogue

When Ford's Model T rolled off the assembly line in 1908, it didn't immediately transform America. What turned the nation into one on wheels were the gas stations, 4S stores, used car dealerships, AAA insurance, and driving schools that quietly emerged in every small town between 1918-1938—a set of underestimated after-sales infrastructure.

Humanoid robots may follow a similar path. We've seen enough demos; the real story begins after the demo.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle