Cloud Computing: Entering an Era of Price Hikes in 2026?

02/25 2026

02/25 2026

508

508

"Alibaba Cloud and Others" Wait and See

Written by / Chen Dengxin

Edited by / Li Wenjie

Layout by / Annalee

The traditional pricing model for cloud computing has undergone subtle changes.

For years, the prevailing trend in the cloud computing sector has been one of price reductions, but after entering 2026, Amazon and Google successively raised prices for their cloud computing services, breaking the traditional perception.

Notably, this wave of price hikes has also reached China.

As a typical representative of small-to-medium-sized cloud computing providers, UCloud announced that starting from March 1, 2026, it would raise prices for all its cloud products and services, affecting both new and renewal customers.

Faced with this wave of price hikes, what will "Alibaba Cloud and others" do?

The Tradition of Price Reductions Only Has Been Broken

There was a time when price reductions were the core narrative of cloud computing.

In 2006, Amazon pioneered cloud computing, becoming the first company globally to enter the sector, exploring the essence of cloud computing by feeling its way forward.

As a pioneer, Amazon AWS not only became the world's largest cloud computing company but also a company skilled at playing the price reduction card, setting pricing rules for the industry: Amazon AWS has cumulatively reduced prices nearly a hundred times over two decades, stating, "Price reductions are our core strategy, and we consider them a normal occurrence."

Against this backdrop, Microsoft Azure and Google Cloud also had to reduce prices to compete, even adopting more aggressive tactics, often implementing reductions exceeding 50%.

The enthusiasm for price wars abroad was matched domestically.

As the leader in domestic cloud computing, Alibaba Cloud frequently played the price reduction card to capture market share, conducting 18 rounds of price reductions in 2016 alone, stunning the outside world.

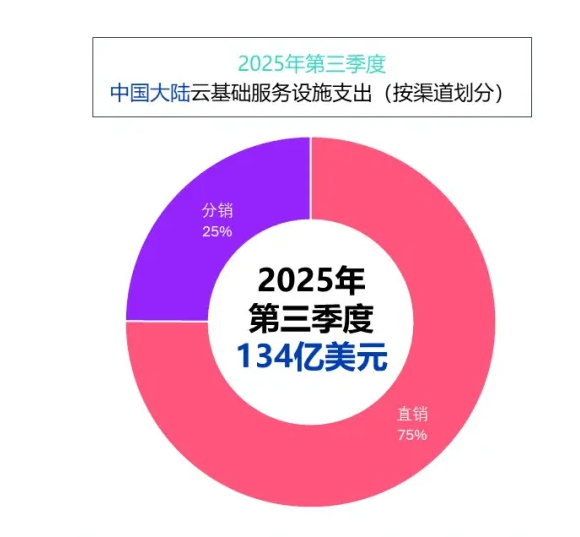

Source: Omdia

The reason for this lies in Moore's Law driving the trend.

Simply put, with the continuous iteration of cloud computing technology and hardware, the industry has seen a trend of increasing performance and decreasing costs.

The Economic Observer stated, "Cloud computing, as a service model highly dependent on hardware and software technology, is also influenced by Moore's Law. With the improvement of server hardware performance, the expansion of network bandwidth, and the innovation of storage technology, the computing power and network costs of cloud computing are constantly decreasing. Therefore, cloud computing service providers lowering prices is both a comply with (shùn yìng, conforming to) trend of Moore's Law and an inevitable result of market competition."

It should be noted that after the rise of AI, competition in cloud computing has become even more intense.

When AI and cloud computing sparked synergy, they became a crucial lever for reshaping traditional industries and were seen as the inevitable path for enterprises to embrace intelligence, thus enticing Alibaba Cloud, JD Cloud, Tencent Cloud, Volcano Engine, and others to significantly reduce prices again starting in 2024.

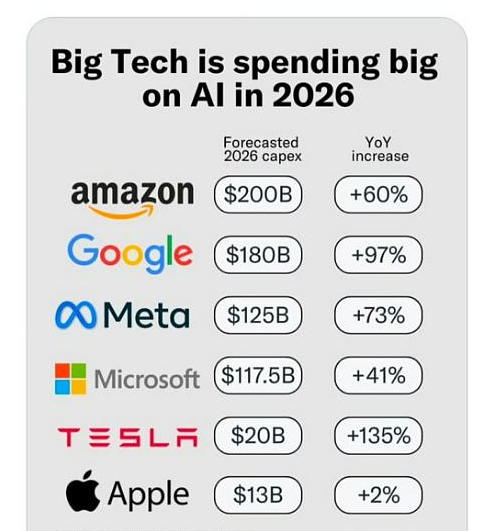

Source: YunToutiao

Unexpectedly, the rules were broken in 2026.

Amazon AWS raised prices by about 15% for its EC2 machine learning capacity block service for large model training, with the hourly charge for p5e.48xlarge, equipped with eight NVIDIA H200 accelerators, increasing from $34.61 to $39.80.

Google Cloud raised prices for its global data transfer service, with the price per GB of data transfer in North America increasing from $0.04 to $0.08, in Europe from $0.05 to $0.08, and in Asia from $0.06 to $0.085.

In short, Amazon AWS and Google Cloud have not implemented comprehensive price hikes for their cloud computing services but have only tested the waters with partial products or services, while domestic player UCloud has taken a one-step approach, initiating a full-scale price increase mode.

Various signs indicate that cloud computing pricing has reached a strategic turning point.

Bearing the Inflationary Pressure of AI

Behind the strategic turning point lies the prominence of AI cloud.

In the past, for various reasons, private deployment became a common choice for many enterprises; however, with the rapid evolution of large models, private deployment has also brought about the issue of outdated versions.

Liu Weiguang, Senior Vice President of Alibaba Cloud Intelligence Group, admitted, "The impact of AI lies in the fact that the iteration cycle of past technological standards was five to ten years, but now it has become two to three years, with large models iterating on a weekly basis."

Furthermore, the efficiency of private deployment is also debatable.

There is a obvious (míng xiǎn de, obvious) tidal phenomenon in computing power utilization, with some demands occurring during the day, some at night, and even some in the early morning hours, and the demands during peak and trough periods may also differ, leading to potential resource waste due to spatial and temporal imbalances, whereas using public clouds can maximize efficiency.

As a result, there has been an explosive growth in demand for AI cloud.

According to IDC, in the first half of 2025, the call volume (diào yòng liàng, invocation volume) of large models on China's public clouds reached 536.7 trillion Tokens, a nearly 400% increase from the entire year of 2024.

And according to Omdia, the market size of China's AI cloud in the first half of 2025 was 22.3 billion yuan, expected to grow to 193 billion yuan by 2030.

Unfortunately, the costs of cloud computing have become increasingly difficult to control.

On one hand, GPU chips face dual challenges of price and supply chain, and storage chips have also entered a seller's market, continuously driving up costs.

SK Hynix stated that storage chip prices would continue to rise in 2026, with the upward trend lasting throughout the year being a certainty, "Currently, the company's overall inventory of DRAM and NAND is only about four weeks, at historically extremely low levels, with all customers, from cloud providers like Google and Microsoft to AI companies like OpenAI, and even consumer electronics terminal manufacturers, unable to obtain sufficient supply, leading to repeat orders that further drive up price expectations."

On the other hand, the consensus in the industry is that computing power ultimately relies on electricity, and with data centers being major electricity consumers, high energy prices have become a concern, with data indicating that the total electricity shortage in the United States could reach as high as 73.2 GW from 2025 to 2030, becoming the biggest weakness in its AI development.

This is evident from chip power consumption.

NVIDIA's A100 chip has a power consumption of 400W, while the B200 chip has exceeded 1000W, with server rack power consumption iterating from 120kW to over 1000kW.

As a result, electricity costs for data centers account for 40% to 60% of total operating costs, posing a significant challenge for "Amazon and others."

In short, cloud computing is bearing the inflationary pressure of AI.

Overseas Tech Giants Increase Capital Expenditures for AI

"Wall Street See" stated, "The global cloud computing industry has consistently achieved continuous service price reductions through economies of scale and technological iteration over the past nearly two decades. However, with the exponential growth in computing power demand in the AI era and the supply chain constraints of key hardware like GPUs not yet fully alleviated, structural changes in supply and demand are pushing the industry into a new pricing cycle."

Despite this, domestic cloud computing giants have remained inactive.

The scale of small-to-medium-sized cloud computing players pales in comparison to internet giants, with not only infrastructure and AI capabilities lagging but also significantly weaker stress resistance (kàng yā néng lì, pressure resistance).

In fact, as competition in cloud computing intensifies, Top players (tóu bù wán jiā, leading players) are also moving downmarket, seizing niche application scenarios and further squeezing the survival space of small-to-medium-sized cloud computing players.

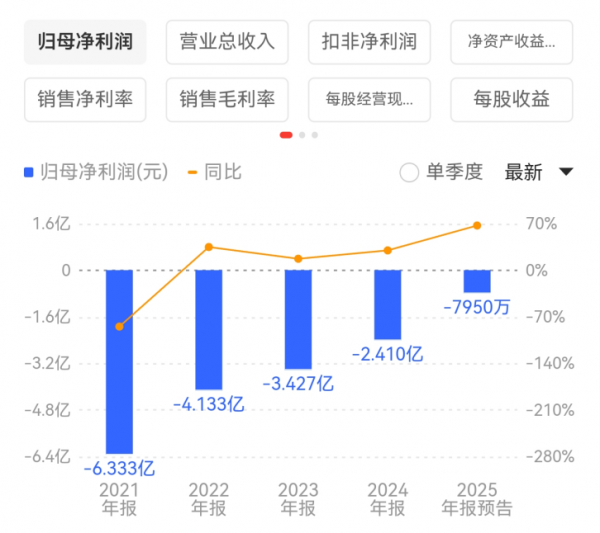

Take "the first A-share cloud computing stock" UCloud as an example; it debuted on the STAR Market on January 20, 2020, with a market capitalization of 30.8 billion yuan, but as of February 25, 2026, its market capitalization has fallen below 18 billion yuan.

UCloud Strives to Reduce Losses

More importantly, "Alibaba Cloud and others" still favor market expansion.

For instance, Baidu Intelligent Cloud set the tone at its internal strategic meeting, raising the target growth rate for AI-related revenue from 100% to 200% in 2026, with all employees striving for high growth and aiming to be the leader in the AI cloud market.

Another example is Alibaba Cloud's new goal of "capturing 80% of the new share in China's AI cloud market in 2026" to consolidate its industry position.",

-

![]()

The World's First Trillionaire Emerges: Is SpaceX's $2 Trillion Valuation Justified?

-

Volkswagen to Implement 19,000 Job Cuts in Germany This Year

-

![]()

Tremble, Humans: AI Continues to Accelerate at Breakneck Speed

-

![]()

A Strategic Vision: Taking a Leaf Out of Apple’s Book in China’s Operation-Intensive Auto Market

-

![]()

Yu Chengdong Declares, ‘Only First Place Exists in My Lexicon.’ Is This Bold Claim or a Promise of Excellence?

-

![]()

Agent OS is Here! HarmonyOS 7 Unveiled, Huawei Redefines OS

-

![]()

Agent OS is Here! Huawei Unveils HarmonyOS 7, Redefining Operating Systems

-

DingTalk’s Evolution and the Dilemma Facing Alibaba