Nvidia: Frenzied Performance vs. Lukewarm Stock Price, Has the Universe's Top Stock Fallen Out of Favor?

02/26 2026

02/26 2026

575

575

Nvidia (NVDA.O) released its Q4 FY2026 earnings report (as of January 2026) after the U.S. market closed in the early morning of February 26, 2026, Beijing time. Key details are as follows:

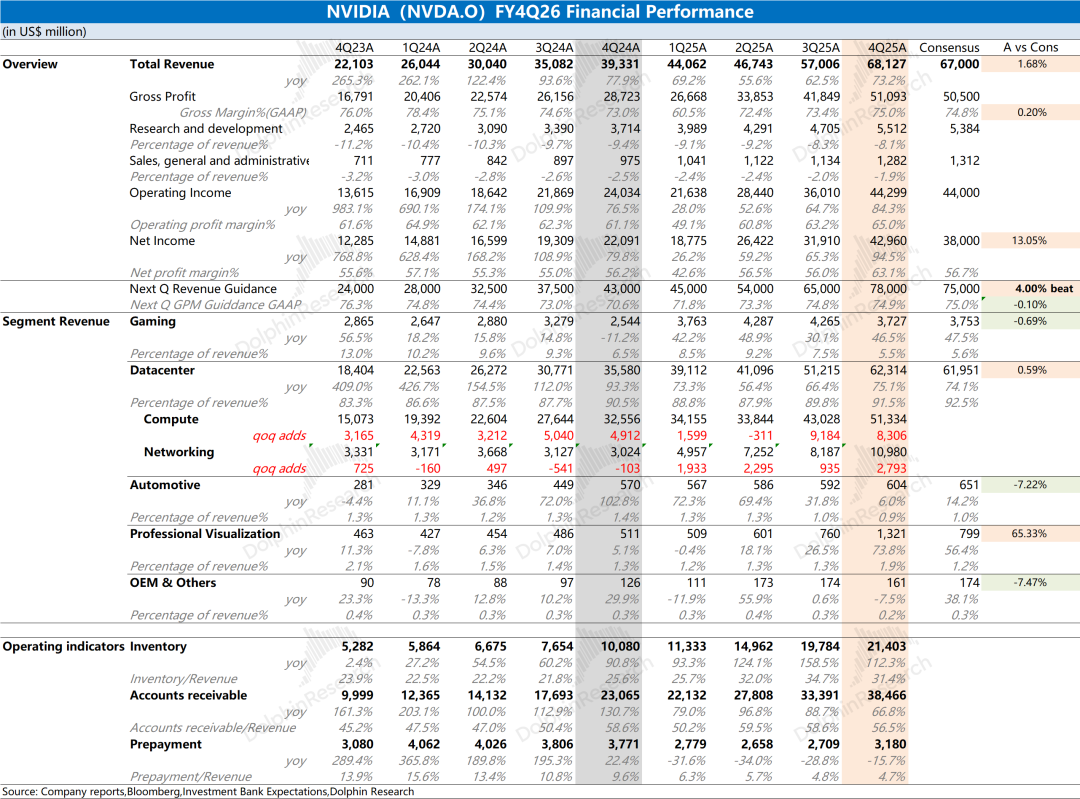

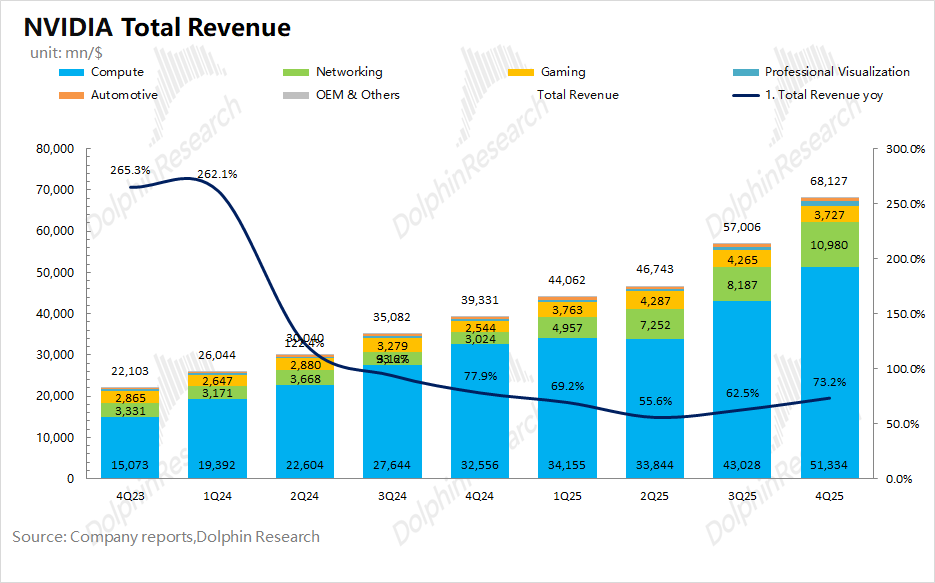

1.Core Operating Metrics: Total revenue reached $68.1 billion, surpassing the raised buyer expectations ($67 billion), with a quarterly sequential increase of $11.1 billion, primarily driven by increased mass production of the Blackwell series in the data center business.

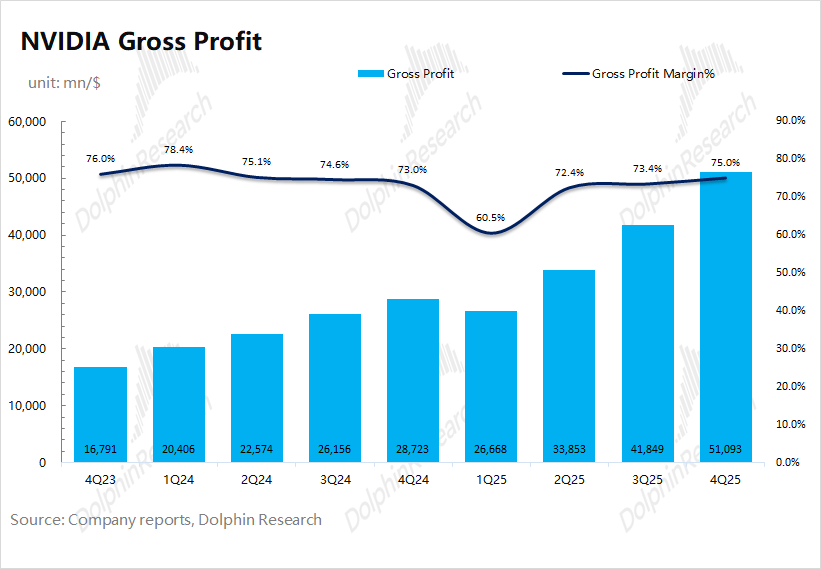

The gross margin for the quarter was 75%, up 1.6 percentage points sequentially, largely in line with market expectations (74.8%). With the ramp-up of B300 mass production, the company's gross margin once again rose to around 75%.

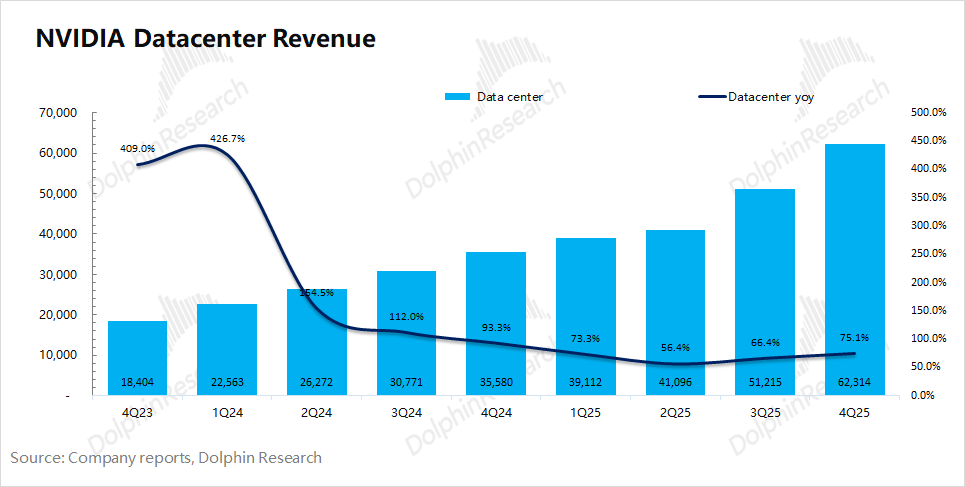

2.Data Center: Revenue for the quarter reached $62.3 billion, with a sequential increase of $11.1 billion, mainly due to increased deliveries of the B300 series chips. The Blackwell architecture has become the dominant product across all client categories.

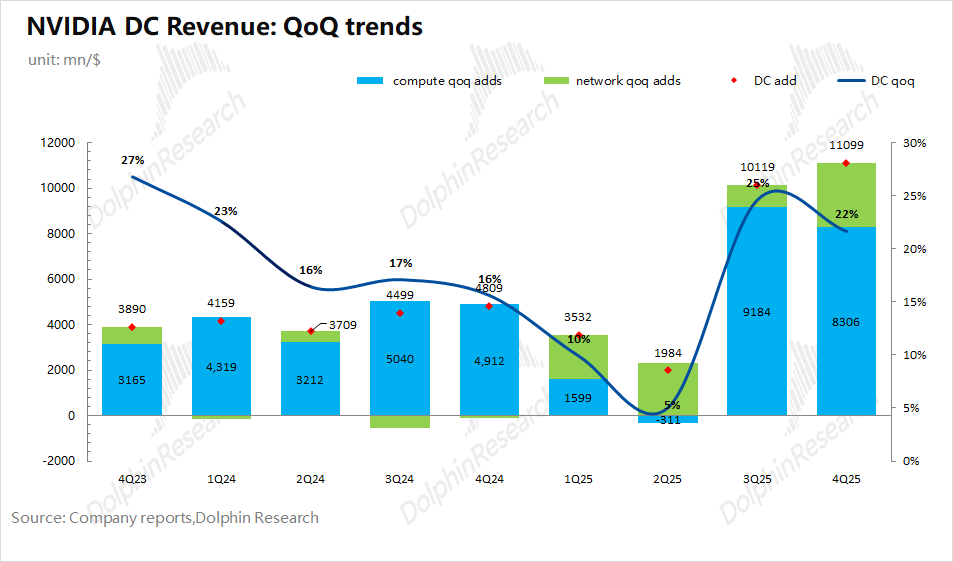

Breakdown: Computing revenue was $51.3 billion, and networking revenue was $11 billion this quarter. The sequential increase in computing revenue rose to $8.3 billion, representing the largest revenue growth increment for the company. With the mass production of the new Rubin products commencing in the second half of the year, the company's data center business is expected to continue its strong growth.

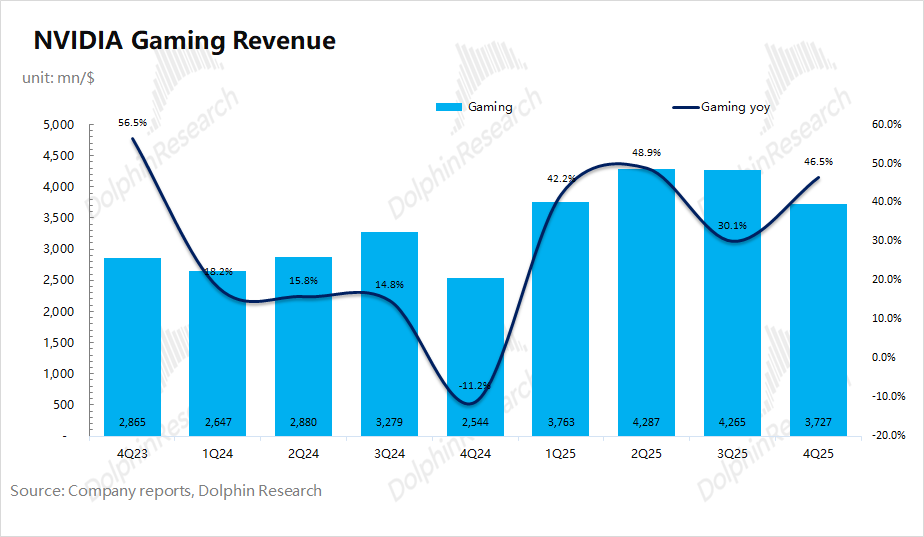

3.Gaming Business: Revenue for the quarter was $3.7 billion, up 46% year-over-year, driven by downstream demand for products such as the company's RTX 50 series. Compared to AMD's quarterly revenue of approximately $800 million, Nvidia still holds a clear advantage in the gaming graphics card market.

4.Profits: The company's core operating profit for the quarter was $44.2 billion, up 84% year-over-year, primarily driven by rapid revenue growth and a rebound in gross margin. The core operating profit margin for the quarter rebounded to 65%.

5.Next Quarter Guidance: The company expects revenue of $78 billion for the first quarter of FY2027 (1Q26), representing a sequential increase of $11 billion (guidance excludes revenue from China's data center computing power), surpassing the raised buyer expectations ($73-76 billion). The next quarter's gross margin (GAAP) is projected at 74.9%, down 0.1 percentage points sequentially, largely in line with market expectations (75%).

Dolphin Research's Overall View: Short-term Performance Excels, but ASIC Competition Remains a 'Potential Danger'

Nvidia's earnings data this time remains quite strong, with a quarterly sequential revenue increase of $11.1 billion, primarily driven by increased mass production of the Blackwell series in the data center business. The company's gross margin has also returned to 75%.

For next quarter's guidance, the company expects revenue to continue rising to $78 billion (±2%), representing another sequential increase of $10 billion, surpassing the raised buyer expectations ($73-76 billion). The company's current main products are the B300/GB300, and with the launch of the new Rubin products in the second half of the year, the company is expected to sustain its high-growth performance.

Since Jensen Huang has already provided an outlook for the company's AI business, expecting cumulative shipments of 20 million Blackwell+Rubin units by the end of 2026 (roughly corresponding to $500 billion in revenue), the market is not overly concerned about the company's performance in FY2027.

Beyond this quarter's earnings and guidance, the market is more concerned about the impact of AI chip competition and client self-research, gross margin trends beyond 2026, and downstream client AI capital expenditures (Capex):

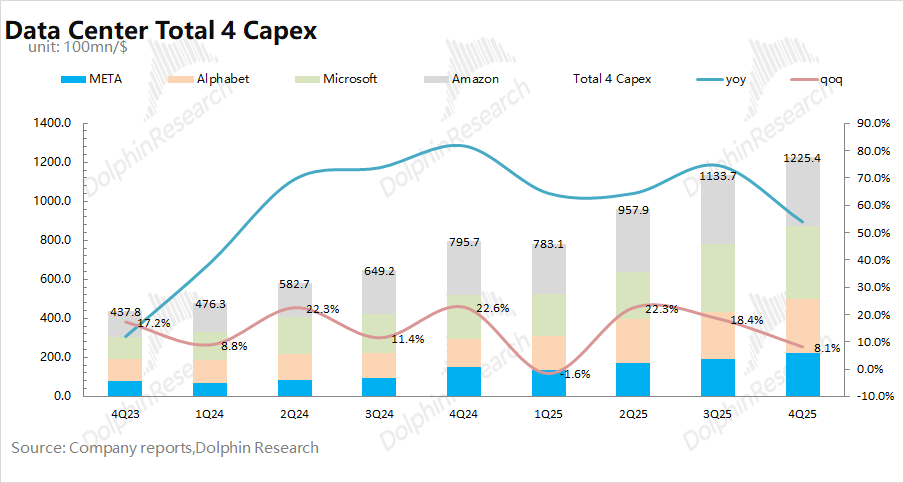

a) Major Players' Capital Expenditures (Primary Buyers): Recently, major players like Google and Meta have indicated in their 2026 outlooks that they will continue to increase their investments in AI Capex.

Combining capital expenditures and outlooks from various companies, Dolphin Research expects the four major core cloud providers (Google, Meta, Microsoft, and Amazon) to increase their capital expenditures to over $660 billion in 2026, up 62% year-over-year.

Cloud service giants are currently the primary buyers of the company's AI chips and represent the core 'foundation' for Nvidia's growth, laying the groundwork for its performance expansion.

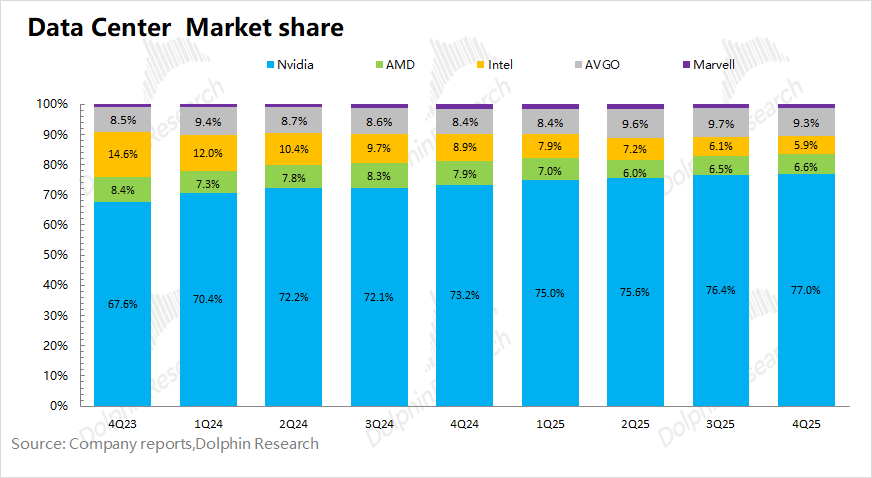

b) Market Competition in AI Chips: When combining the data center revenues of various companies in the AI chip market, Nvidia holds over 70% of the market share, making it the absolute leader in the industry.

On one hand, this reflects Nvidia's strong product capabilities and has allowed it to achieve a high gross margin (70%+). On the other hand, downstream clients may feel that Nvidia is taking all the profits, leading them to seek more 'cost-effective' alternatives such as self-developed chips or custom ASICs.

Recently, AMD and Meta signed a 'similar to Open AI' 6GW cooperation agreement. The first batch of 1GW is expected to begin delivery in the second half of 2026, utilizing MI450-based and sixth-generation AMD EPYC processors. As part of the agreement, AMD will grant Meta a five-year warrant.

Major players (Google, Meta, Microsoft, Amazon, and Open AI) have all begun developing their own AI chips. Especially with the trend of 'shifting from training to inference,' the gap between custom ASICs and Nvidia GPUs is narrowing, with major players focusing more on 'cost-effectiveness.'

Currently, 'Google Gemini + Broadcom' holds nearly a 10% market share, posing a gradual challenge to Nvidia in the AI market and potentially further impacting Nvidia's market share and gross margin in the AI chip market (the market is concerned about a decline in gross margin after 2026).

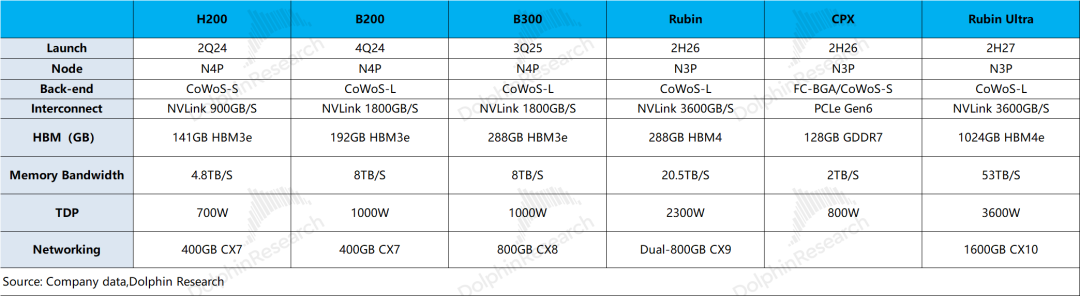

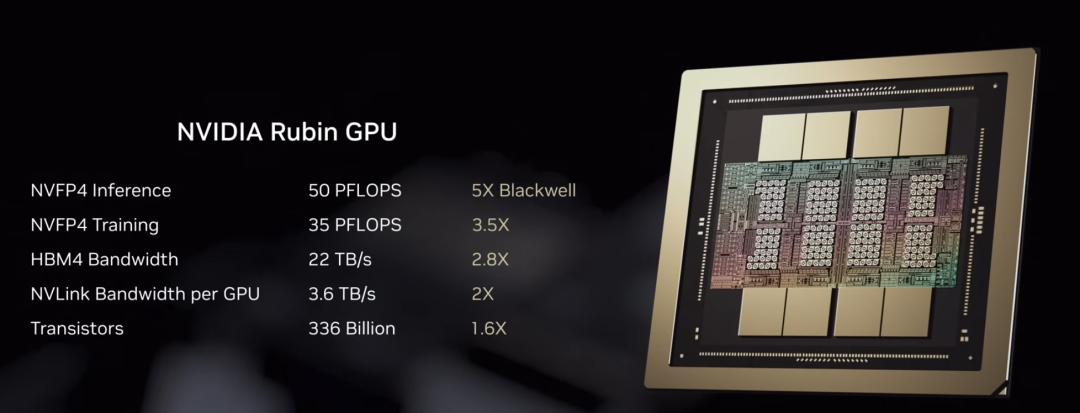

c) Progress of New Rubin Products: Nvidia's current main products are the B300 series, and the company plans to launch Rubin and CPX products in the second half of 2026, which will adopt TSMC's 3nm process. The company will also continue to launch Rubin Ultra products in 2027.

At CES 2026, Jensen Huang disclosed that the computing power of the company's Rubin GPU will reach five times that of the Blackwell series (in NVFP4 inference mode), continuing to lead in the AI chip track (Chinese term for 'field' or 'sector').

Considering (a+b+c), Nvidia currently maintains a clear leading advantage in the AI chip market, but major players' investments must also consider economic viability (return on investment). With Nvidia's gross margin as high as 75%, it implies that Nvidia is capturing most of the profits in the supply chain. Once downstream economic viability is insufficient, it may affect further investments by major players.

As a result, major players are developing their own AI chips and seeking 'cost-effective' solutions. The market also believes that Nvidia's 'dominant' market position is 'unsustainable.' Only when downstream applications materialize and major players' models achieve economic viability can the industry achieve healthy growth.

Since Jensen Huang previously provided an AI business outlook (Blackwell+Rubin), the market consistently expects high growth for the company in FY2027, with disagreements primarily focusing on the period beyond FY2027.

Looking solely at Nvidia's PE, it is notably low within the AI supply chain, primarily due to market uncertainties about the company's performance in FY2028 and beyond (downstream capital expenditures and the company's competitiveness). Especially after the company experiences high growth in FY2027, the market widely expects a significant decline in growth and concerns about market share and gross margin erosion due to competitors like ASIC chips.

As a result, even though major players have recently increased their capital expenditures, the company's stock price has not risen and remains largely range-bound. A more detailed value analysis has been published in the Changqiao App under the 'Dynamic - Depth (Research)' section in an article with the same title.

Compared to downstream capital expenditures, the market hopes that the company's management can clearly alleviate concerns about 'gross margin and market competition,' which would help the company escape its current 'relatively pessimistic valuation' state. On the other hand, even though the company faces increasing concerns about competition from ASICs, short-term earnings certainty provides effective support for the company.

Here is a detailed analysis:

1. Nvidia's Business Overview

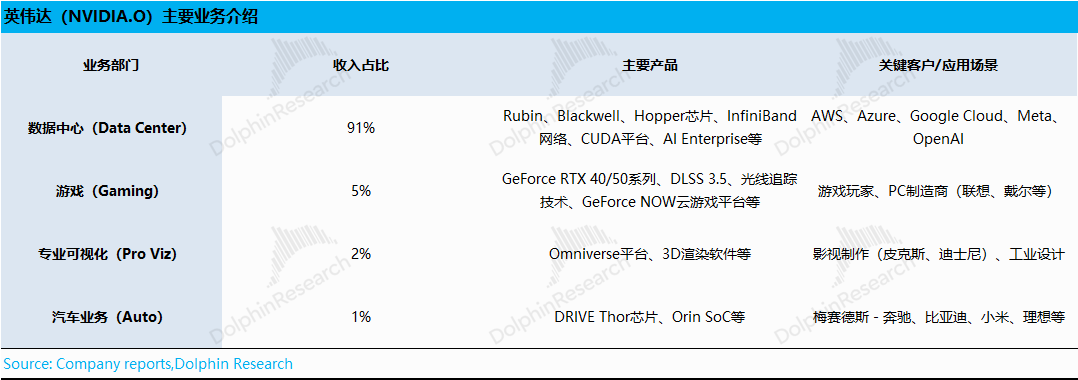

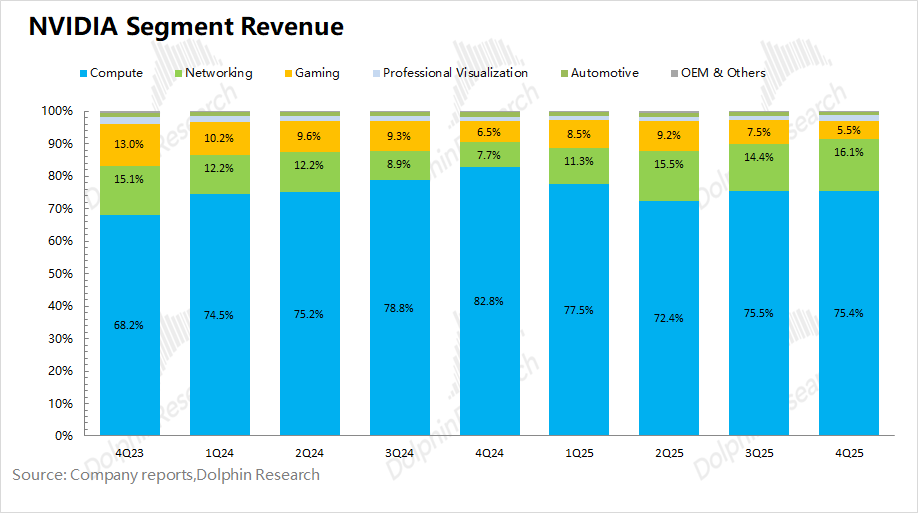

With the sustained growth of Nvidia's data center business, it has now become the largest revenue segment for the company, accounting for nearly 90% of total revenue. The gaming business, which was previously the primary revenue source, now accounts for only about 10%.

Breakdown by business:

1) Data Center Business: This is currently the primary focus, with key products including compute chips like Blackwell and Hopper. The company's core clients are major cloud service providers such as Amazon, Microsoft, and Google.

The company's data center business is currently in the Blackwell product cycle, with the B300/GB300 as the main products. With the mass production of the new Rubin products in the second half of the year, the company's product cycle will shift from the Blackwell series to the Rubin series.

2) Gaming Business: The company remains the leader in the discrete graphics market, with current main products being the RTX 40 and RTX 50 series. Key clients include gamers and PC manufacturers.

3) Professional Visualization and Automotive Business: These two segments currently account for a relatively small portion, each around 1-2%. Key clients in the professional visualization business include Pixar and Disney. The automotive business primarily focuses on Orin and Thor chips, with clients including BYD, Xiaomi, and Li Auto.

2. Core Performance Metrics: Revenue Increases by $10 Billion Sequentially, Gross Margin Rebounds to 75%

2.1 Revenue: In Q4 FY2026 (4Q25), Nvidia achieved revenue of $68.1 billion, up 73% year-over-year, surpassing the raised buyer expectations ($67 billion). The sequential increase of $11 billion in revenue this quarter was primarily driven by the data center business and the ramp-up of Blackwell series mass production.

Looking ahead to next quarter, the company provided revenue guidance of $78 billion, representing a sequential increase of $9.9 billion, surpassing the raised buyer expectations ($73-76 billion). The company's growth next quarter will still be primarily driven by the B300/GB300, while the new Rubin products will commence mass production in the second half of 2026.

2.2 Gross Margin (GAAP): In Q4 FY2026 (4Q25), Nvidia achieved a gross margin (GAAP) of 75%, meeting market expectations (74.8%). The previous 'collapse' in the company's gross margin was primarily due to the impact of the H20 ban.

For next quarter, the company expects a gross margin (GAAP) of 74.9%, in line with market expectations (75%). With the ramp-up of Blackwell mass production, the company's gross margin has rebounded to around 75%.

Company management mentioned in previous communications that the target gross margin for FY2027 is 75%. This has provided some confidence to the market, but concerns remain about a potential decline in gross margin after FY2027.

3. Core Business Progress: Blackwell Product Cycle, Strong Growth in Data Center Business

Driven by AI Capex, the revenue share of Nvidia's data center business (Compute+Networking) has exceeded 90%, while the gaming business's share has been squeezed to below 10%.

3.1 Data Center Business: In Q4 FY2026, Nvidia's data center business achieved revenue of $62.3 billion, up 75% year-over-year. The data center business remains the company's primary focus, with growth this quarter primarily driven by increased mass production of the Blackwell series products, fueled by accelerated computing and artificial intelligence.

Breakdown: (1) Computing revenue was $51.3 billion this quarter, up $8.3 billion sequentially, with the accelerated mass production of the B300 contributing the most significant increment. (2) Networking revenue was $11 billion this quarter, up $2.8 billion sequentially.

Currently, cloud service providers remain the largest buyers of the company's AI chips. Therefore, the capital investments of downstream cloud providers form the basis for the growth of the company's data center business. Based on discussions with the management teams of four companies (Google, Meta, Microsoft, and Amazon), Dolphin Research anticipates that the combined capital expenditures of these four major players could exceed $660 billion in 2026, representing a year-on-year increase of 62%. This provides a strong foundation for the company's high-growth performance in the 2027 fiscal year.

Compared to downstream capital expenditures, the market is actually more concerned about the competitive risks posed by rivals such as ASIC. Therefore, even though major companies have recently increased their capital expenditures, NVIDIA's stock price has not risen.

The key players in the current AI chip market are NVIDIA, Broadcom, and AMD, which together account for over 90% of the market share. Large models consist of two stages: training and inference. While NVIDIA's GPUs still hold a significant advantage in the training phase, the inference phase has lower performance requirements, making customized ASICs from Broadcom or products from AMD more cost-effective choices.

The high gross profit margins of NVIDIA's upstream chips have absorbed a significant portion of the profits in the supply chain, directly impacting downstream economics.

If downstream economics fail to materialize, the sustainability of customers' future AI capital expenditures (Capex) will face challenges. Therefore, from a supply chain perspective, given NVIDIA's exceptionally high gross profit margins, various companies are motivated to develop their own chips or seek alternative solutions such as ASICs to achieve cost reduction.

The market's primary concern revolves around how long the company can sustain its current gross profit margin of 75%, particularly regarding the uncertainty of performance beyond the 2027 fiscal year. Currently, mainstream institutions expect a gradual decline in the company's gross profit margins starting from the 2028 fiscal year and beyond.

3.2 Gaming Business: In the fourth quarter of the 2026 fiscal year, NVIDIA's gaming business achieved revenue of $3.7 billion, up 46% year-on-year, primarily driven by shipments of products such as the RTX 50 series. The gaming business now accounts for less than 10% of the company's total revenue, with the company's current performance focus remaining on its data center business.

In the gaming business, compared to AMD's quarterly gaming revenue of $840 million, NVIDIA still holds a clear leading advantage in the gaming graphics card market.

IV. Key Financial Indicators: Continued Improvement in Profitability Driven by Economies of Scale

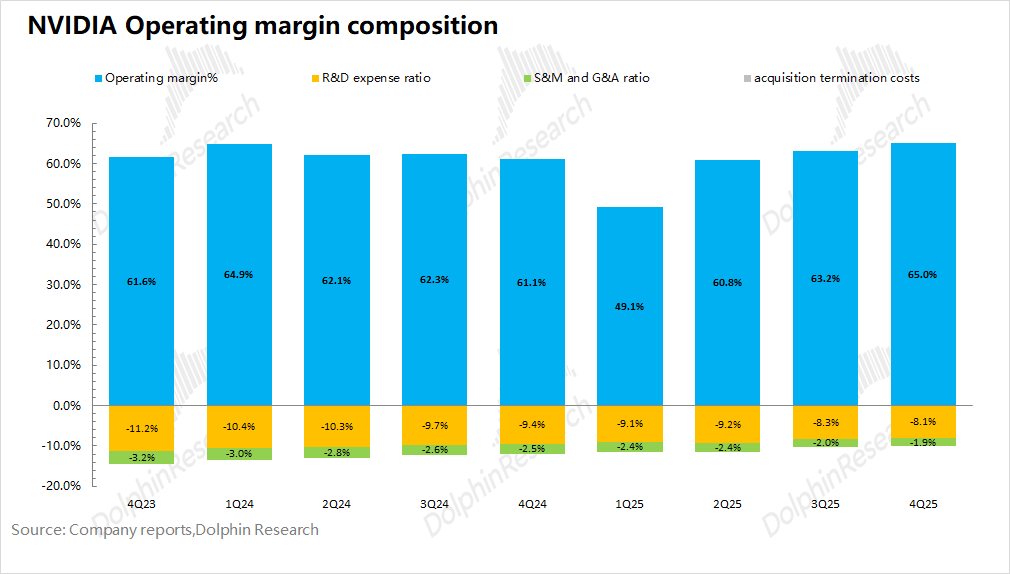

4.1 Core Operating Profit Margin

In the fourth quarter of the 2026 fiscal year, NVIDIA's core operating profit margin reached 65%, continuing to improve, primarily due to the recovery in gross profit margin and a decline in operating expense ratios.

An analysis of the components of the core operating profit margin reveals the following specific changes:

"Core Operating Profit Margin = Gross Profit Margin - R&D Expense Ratio - Sales, Administrative, and Other Expense Ratio"

1) Gross Profit Margin: This quarter, it stood at 75%, up 1.5 percentage points sequentially, primarily driven by the ramp-up in production of the Blackwell series products.

2) R&D Expense Ratio: This quarter, it was 8.1%. Although the company's R&D investment increased by $800 million sequentially, the R&D expense ratio continued to decline due to rapid revenue growth.

3) Sales, Administrative, and Other Expense Ratio: During the Blackwell product cycle, the company's current sales and administrative expenses have remained relatively stable, with this quarter's ratio declining to 1.9% of revenue.

The company expects its operating expense guidance for the next quarter to continue rising to $7.7 billion. Considering the revenue guidance, the operating expense ratio for the next quarter is expected to slightly decline to 9.9%, continuing to be influenced by economies of scale.

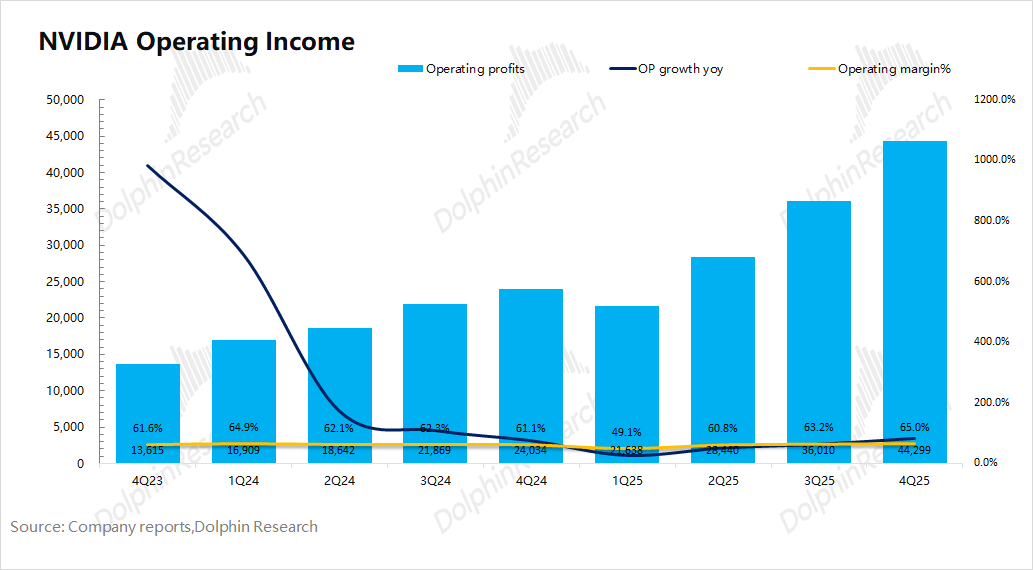

4.2 Core Operating Profit

In the fourth quarter of the 2026 fiscal year, NVIDIA's net profit reached $43 billion, up 94% year-on-year. The net profit margin for this quarter was 63%.

Since net profit is also affected by non-operating items, Dolphin Research focuses more on the company's core operating profit (gross profit - R&D expenses - sales, administrative, and other expenses). The company's core operating profit for this quarter was $44.3 billion, up 84% year-on-year. The core operating profit margin increased to 65%.

The company's current performance growth is primarily driven by the Blackwell product cycle. Based on the company's previous AI business outlook, with the mass production of the new Rubin products in the second half of the year, the company is expected to continue its high-growth performance throughout the 2027 fiscal year.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting is only allowed with authorization.

// Disclaimer and General Disclosure

This report is intended for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions based on the content or information mentioned in this report assumes their own risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the relevant information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute advice, inquiries, or recommendations regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for or intended to be distributed to jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials contradicts applicable laws or regulations, or to citizens or residents of jurisdictions where Dolphin Research and/or its subsidiaries or affiliated companies are required to comply with any registration or licensing requirements in such jurisdictions.

This report only reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) make, copy, reproduce, duplicate, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

The World's First Trillionaire Emerges: Is SpaceX's $2 Trillion Valuation Justified?

-

Volkswagen to Implement 19,000 Job Cuts in Germany This Year

-

![]()

Tremble, Humans: AI Continues to Accelerate at Breakneck Speed

-

![]()

A Strategic Vision: Taking a Leaf Out of Apple’s Book in China’s Operation-Intensive Auto Market

-

![]()

Yu Chengdong Declares, ‘Only First Place Exists in My Lexicon.’ Is This Bold Claim or a Promise of Excellence?

-

![]()

Agent OS is Here! HarmonyOS 7 Unveiled, Huawei Redefines OS

-

![]()

Agent OS is Here! Huawei Unveils HarmonyOS 7, Redefining Operating Systems

-

DingTalk’s Evolution and the Dilemma Facing Alibaba