CoreWeave: Soaring Orders, Plummeting Profits—Can the AI Computing Unicorn Break Free from the Profitability Trap?

03/06 2026

03/06 2026

714

714

AI Cloud Unicorn CoreWeave: On February 27, after the U.S. stock market closed, CoreWeave released its Q4 2025 financial report. Overall, while business and revenue growth remained solid, profit declines were worse than the already lowered guidance.

This suggests the company may be trapped in a cycle where higher revenue leads to even greater losses, heightening concerns among investors already skeptical about its ability to achieve stable profitability in the medium to long term. Key highlights include:

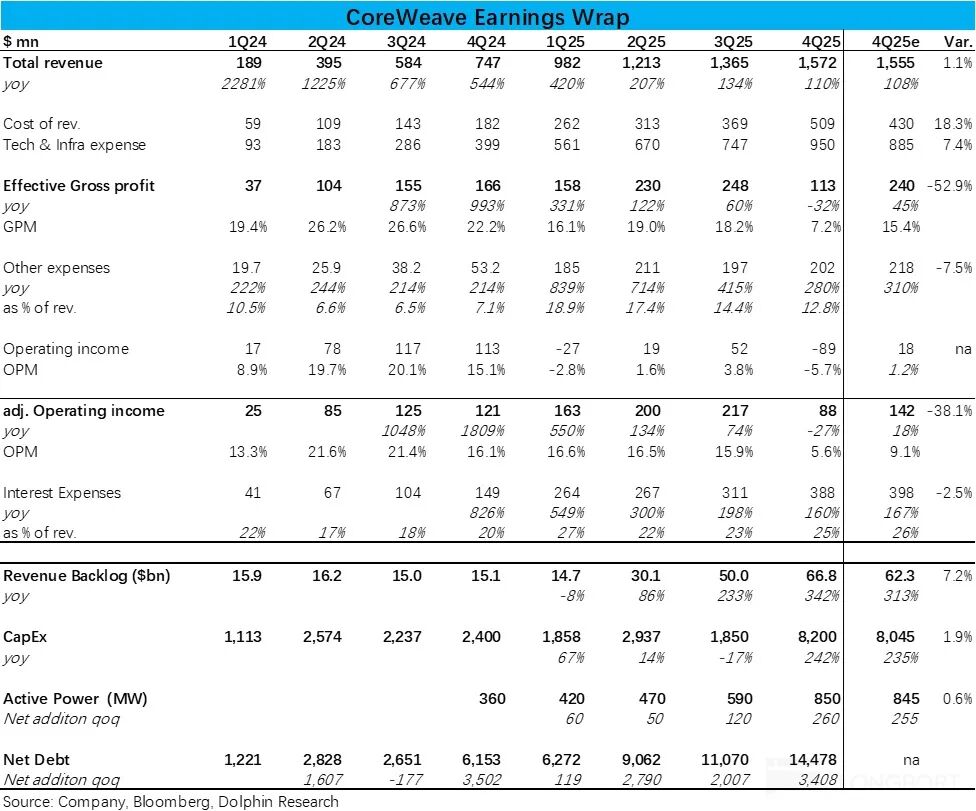

1. Computing Power Deployment Meets Targets: After revising Q4 revenue guidance downward last quarter due to supplier delays, actual revenue reached approximately RMB 1.57 billion this quarter, up 110% year-over-year, slightly exceeding expectations. The delay issue appears largely resolved with no further impact.

The market's most closely watched metric—active computing power capacity—reached 850Mw this quarter, meeting the consensus expectations of top-tier sell-side analysts. Sequentially, net capacity increased by 260Mw, with growth accelerating to 2.2x that of the previous quarter, marking the official entry into a rapid scaling phase.

2. Contract Backlog Growth Exceeds Expectations Amid Customer Diversification: Leading indicator—Remaining Performance Obligations (RPO)—hit RMB 66.8 billion this quarter, significantly surpassing Bloomberg's consensus estimate of RMB 62 billion. With no recent reports of major new deals with tech giants, sell-side analysts generally expected limited growth in new contract backlog this quarter.

However, it actually increased by nearly RMB 17 billion sequentially, not far below last quarter's peak of RMB 20 billion. Dolphin Research speculates this was driven by numerous non-top-tier clients, as the company confirmed during the earnings call that new client additions doubled from the previous peak, including Cognition, Cursor, Mercado Libre, Midjourney, and Runway.

This suggests progress in reducing the company's heavy reliance on a small number of top clients.

3. Profit Decline Worse Than Feared: A critical issue is that while the market expected margin pressure during the rapid computing power scaling phase—with adjusted operating margin expectations lowered to around 8%—actual margins fell to just 5.6%. This sharper-than-expected decline caused adjusted operating profit to decrease by approximately 27% despite revenue doubling.

The primary driver was a collapse in "true" gross margin (excluding cost of revenue and Tech & Infra expenses) to just 7.2%, down from 18% last quarter and far below expectations. Meanwhile, sales and administrative expenses as a percentage of revenue decreased by about 1.6 percentage points sequentially. This indicates that the margin decline stemmed from higher energy costs, depreciation, and upfront investments during the computing power scaling phase.

4. Capex Accelerates Further: Another concern is that while Capex reached RMB 8.2 billion this quarter—roughly in line with, but slightly above, market expectations—it represented a 3x-4x increase from the RMB 2-3 billion in previous quarters. By contrast, the sequential increase in newly deployed computing power was only 2.2x.

This means computing power deployment speed lagged behind Capex growth. While this is not unreasonable given the time required for equipment installation and testing, the mismatch—where investments outpace revenue-generating capacity—will continue to pressure margins.

5. Debt Levels Continue to Rise: Alongside accelerating Capex, the company's total debt increased by approximately RMB 7.5 billion sequentially this quarter. However, as of Q4's end, most of the proceeds remained on the books as wealth management products, resulting in a net increase in interest-bearing debt of only about RMB 3.4 billion.

Even so, interest expenses as a percentage of revenue rose further from 23% last quarter to 25%, suggesting mounting debt pressure ahead.

Dolphin Research Viewpoints:

1. Quarterly Performance: CoreWeave's Q4 results were a mixed bag. On the positive side, new computing power deployments met expectations, the delay issue did not worsen, and revenue growth hit targets. Additionally, new contract values exceeded forecasts, driven by a more diversified client base, alleviating concerns about customer concentration risk.

However, during the rapid computing power scaling phase, the company finds itself in the paradoxical situation where more business leads to greater losses. The time lag between investment and computing power deployment caused Capex growth to far outpace new capacity additions, resulting in a sharp margin decline and pushing the company further from GAAP profitability.

2. Guidance: In the near term, the company expects Q1 revenue to reach RMB 1.9-2.0 billion, up RMB 400-500 million sequentially—still accelerating but notably below consensus estimates of RMB 2.24 billion.

Correspondingly, Capex guidance for Q1 is RMB 6-7 billion, also below the RMB 7.1 billion market expectation. The revenue shortfall likely stems from slower-than-expected computing power deployment.

Profit-wise, adjusted operating profit for Q1 is guided at RMB 0-40 million, further declining from Q4 and well below the RMB 140 million expectation. This confirms the trend of declining profits amid rising revenue.

The underperformance in both revenue and profit guidance for next quarter raises greater concerns.

For the medium to long term, the company expects 2026 revenue to reach RMB 12-13 billion—in line with or slightly exceeding current market expectations—suggesting the Q1 revenue slowdown is temporary.

Profit guidance calls for adjusted operating profit of RMB 900 million to RMB 1.1 billion in 2026, implying margins of 7.5%-8.5% and significant improvement in the second half of the year, broadly aligning with market expectations.

A more alarming issue is the projected total Capex of RMB 30-35 billion for 2026—nearly three times the expected annual revenue. This mirrors the current quarter's dynamic: 2026 revenue would be only slightly more than double Q4's annualized figure, while Capex would be nearly four times Q4's annualized level.

Once again, investment growth is outpacing revenue growth by a wide margin.

3. Forward Guidance: For Q1, gross profit is guided at RMB 2.8 billion, up 22% YoY—a relatively high growth rate and about 3% above expectations. Adjusted operating profit is guided at RMB 600 million, also exceeding the RMB 575 million expectation (implying operating margins in line with expectations, driven by strong gross profit growth). This suggests improving Q1 performance.

For the full year 2026, the company expects gross profit to grow 18% YoY to RMB 12.2 billion, with adjusted operating profit of approximately RMB 3.2 billion and a 26% margin—continuing to improve from Q4's 20.5%. Compared to previous guidance and market expectations, the key adjustment is a higher adjusted operating profit target (previously around RMB 2.7 billion).

For more detailed analysis, refer to the same name article in the 「Dynamic-Depth (Research)」 section of the Changqiao App.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprints require authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for users of Dolphin Research and its affiliates for general reading and data reference. It does not consider the specific investment objectives, product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referencing the content or information in this report are at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect consequences, responsibilities, or losses arising from the use of the data contained herein. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of such information and data.

The information or opinions expressed in this report shall not, under any jurisdiction, be construed as an offer to sell or a solicitation to buy securities, nor as a recommendation, quotation, or endorsement of any securities or related financial instruments. The information, tools, and materials in this report are not intended for distribution to, or use by, any person or resident in any jurisdiction where such distribution, publication, provision, or use would contravene applicable laws or regulations or subject Dolphin Research and/or its affiliates or associated companies to any registration or licensing requirements in that jurisdiction.

This report reflects only the personal views, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright solely owned by Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research, (i) reproduce, copy, duplicate, reprint, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer them to any unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action