Kingsoft Cloud Surges: Is the AI 'Lobster Effect' Reshaping Cloud Valuations?

03/10 2026

03/10 2026

566

566

On March 9, the Hong Kong-listed cloud computing sector suddenly surged, with Kingsoft Cloud's stock price soaring by over 13%.

This surge is the result of three concurrent developments: First, the open-source AI agent framework OpenClaw has gained immense popularity, becoming an infrastructure for the AI application layer. Second, Xiaomi's AI ecosystem is accelerating its rollout, with its first mobile agent product already undergoing small-scale closed beta testing. Third, global cloud providers have rare ly (rarely) initiated computing power price hikes, breaking the two-decade trend of "only decreasing, never increasing" in cloud computing pricing.

The convergence of these three forces has reignited market discussions about whether Kingsoft Cloud is truly approaching a turning point in its performance.

Against the backdrop of the AI industry entering the application phase, this second-tier player, long surviving in the shadows of Alibaba Cloud, Tencent Cloud, and Huawei Cloud, may now be presented with an opportunity for revaluation.

However, controversy is simultaneously heating up: Is this a genuine industrial cycle shift, or merely another round of AI-driven capital narratives?

Why Does the AI Application Boom, Under the 'Lobster Effect,' First Benefit Kingsoft Cloud?

The market's direct explanation for Kingsoft Cloud's recent rally is the so-called 'Lobster Effect.'

Recently, the open-source AI agent framework OpenClaw rapidly gained traction in the developer community. Due to its phonetic similarity, it was nicknamed 'Lobster' on Chinese internet platforms. This project has become a focal point for global developers, with even local policies in China beginning to explore 'Lobster.'

However, what truly piqued capital market interest was not the popularity of an open-source project itself, but the trend it represents: AI is accelerating into the Agent era.

Over the past two years, the core of the large model industry has been competition in training capabilities, while AI applications remained in the technical validation stage. However, 2026 may mark a watershed, with AI transitioning from "answering questions" to "executing tasks," thereby unlocking commercial potential.

This shift directly impacts the demand structure for cloud computing. The computing power consumption model is evolving from "pulsed" to "continuous," suggesting a potential reshaping of the overall growth curve for computing power demand.

Traditional AI applications follow a user-triggered request model, where users ask a question, and the model responds. Computing power consumption exhibits a typical "pulsed" pattern, with spikes during requests and idle resources during lulls.

However, AI Agents require continuous online presence, constant task planning, and repeated API calls. As Guosheng Securities noted in a research report, due to their inherent multi-tool invocation, long context, and multi-process work characteristics, the Token consumption per task for Agents can reach dozens or even hundreds of times that of traditional conversational models.

Against this backdrop, cloud providers' business models are also evolving.

In early 2026, a rare signal emerged in the global cloud computing market.

Amazon Web Services (AWS) raised prices for its EC2 machine learning capacity blocks, marking the first time in nearly two decades that AWS broke the industry norm of "only decreasing, never increasing" prices. Subsequently, Google Cloud also announced price adjustments for multiple services.

For the cloud computing industry, this is a noteworthy turning point. Over the past decade, cloud computing has been in a price competition cycle, with providers using "price cuts for volume gains" strategies to capture market share.

Now, however, computing power resources are regaining pricing power.

This confirms the high Prosperity level (prosperity) of global AI computing power demand and highlights the growing scarcity of resources in the AI cloud supply chain.

Amid these supply chain value shifts, Kingsoft Cloud has emerged as one of the first "winners."

The reason lies in its smaller size and lower base compared to the steady growth curves of industry giants. When computing power demand explodes, smaller cloud providers like Kingsoft Cloud often exhibit greater performance elasticity. Once computing power demand enters an upward trajectory, their revenue and profit growth may outpace larger incumbents.

In this rally, the capital market's pursuit of Kingsoft Cloud reflects, to some extent, this logic: when the tide rises, small boats rock the most.

Of course, this elasticity works both ways, implying both upside potential and volatility risks. So, where does Kingsoft Cloud's true value anchor lie?

Kingsoft Cloud's Revaluation Logic: The 'Invisible Computing Power Foundation' of Xiaomi's AI Ecosystem

While OpenClaw has driven industry expectations, it is the substantive progress of Xiaomi's AI ecosystem that has truly made Kingsoft Cloud a market focal point.

Recently, Xiaomi's self-developed MiMo large model-powered mobile AI agent, Xiaomi Miclaw, began small-scale closed beta testing. Due to its name's similarity to OpenClaw, community users also nicknamed it "Lobster."

However, from a product positioning perspective, Xiaomi's "Lobster" takes a more pragmatic approach. It is not a generic open-source framework but a system-level Agent deeply integrated into Xiaomi's "Human-Vehicle-Home Ecosystem," which spans smartphones, smart homes, and smart vehicles.

Once AI Agents become the unified interaction gateway, the computing power demand across the ecosystem will surge exponentially. Within this ecosystem, Kingsoft Cloud is one of the most core cloud platforms.

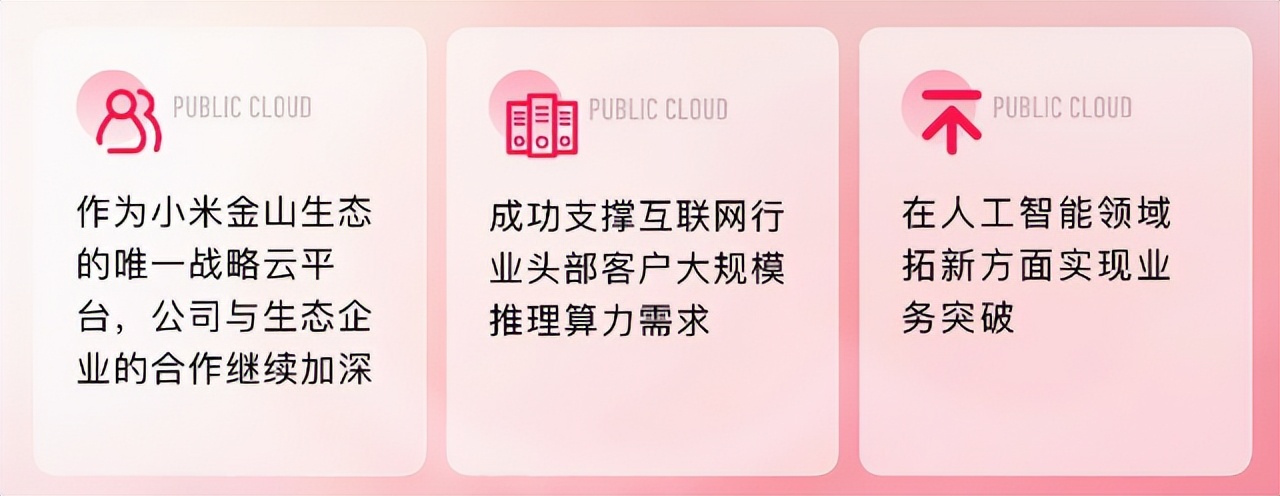

This is why investors immediately revalued Kingsoft Cloud after the "Lobster Effect" erupted. They are betting on the potential dividends from Xiaomi's AI ecosystem explosion. Lei Jun, during a recent public event, mentioned that the combined headcount of "Xiaomi + Kingsoft" in Wuhan has reached over 9,500, nearly achieving the goal of a 10,000-person R&D center, with both sides collaborating deeply in AI and cloud computing.

According to securities research reports, in the third quarter of 2025, Kingsoft Cloud's revenue from the Xiaomi-Kingsoft ecosystem reached RMB 690 million, up 84% year-on-year, accounting for 28% of total revenue. Notably, billing revenue from intelligent computing clouds nearly doubled year-on-year to RMB 780 million, representing 45% of public cloud revenue.

In other words, AI business has become the core growth pillar of Kingsoft Cloud's public cloud segment. Beyond binding with Xiaomi's ecosystem, Kingsoft Cloud is also positioning itself for the next phase of AI computing power through strategic investments.

In early March, Wuhan Kingsoft Cloud, a subsidiary of Kingsoft Cloud, acquired a 20% stake in OneThing Technologies, a Xunlei subsidiary, for RMB 50 million. OneThing Technologies specializes in edge computing and distributed computing power networks, which are considered crucial for reducing inference latency and costs amid rapidly growing AI inference demand.

The market interpreted this deal as Kingsoft Cloud's proactive positioning in the AI era. As AI applications shift from training to inference, low-latency edge computing power will become a new scarce resource.

From Lobster-driven Agent proliferation to demand-driven price hikes and strategic positioning, the capital market is reevaluating Kingsoft Cloud's role: from a cloud computing company to the computing power foundation of Xiaomi's AI ecosystem.

But every coin has two sides. How large is Kingsoft Cloud's imaginative space under this deep integration?

Can Kingsoft Cloud, a Cloud Provider Amidst Giants, Truly Reach an Inflection Point?

Despite the rising AI narrative, which has made Kingsoft Cloud's story much clearer than a year ago, the company's real-world situation remains complex.

The head effect (winner-takes-all effect) in China's cloud computing market has been entrenched for years.

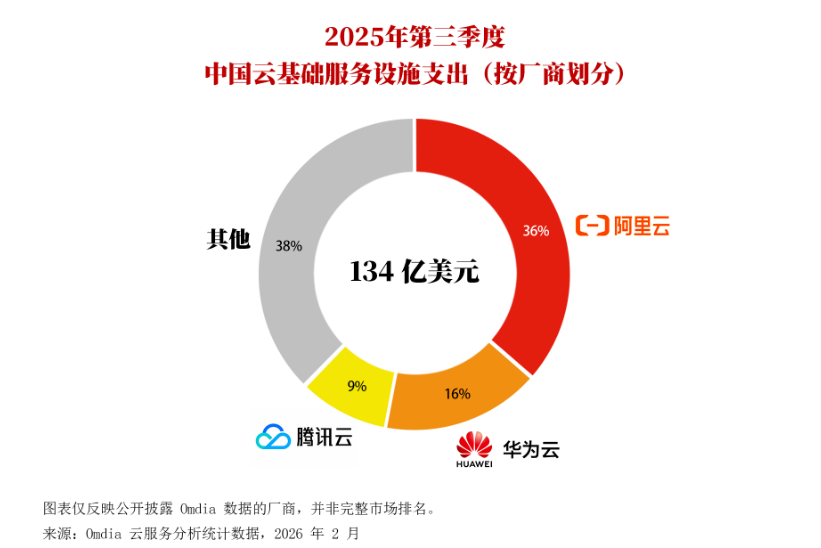

In terms of market share, Alibaba Cloud, Huawei Cloud, and Tencent Cloud dominate, having built deep moats in technological accumulation, product matrices, and sales channels. In contrast, although Kingsoft Cloud was among the earliest cloud service providers, its market share has consistently remained in the second tier.

Over the past few years, Kingsoft Cloud has undergone a challenging adjustment period, proactively scaling back its low-margin CDN business and shifting its strategic focus to AI computing power and intelligent computing centers. This "proactive contraction, resource concentration" strategy has indeed improved financial performance in the short term. In the third quarter of 2025, the company achieved its first adjusted net profit, a noteworthy turning point.

However, this very strategy means the company must find new growth engines in the AI era.

From an industry trend perspective, opportunities are indeed emerging. At the Morgan Stanley TMT Conference, NVIDIA CEO Jensen Huang mentioned that enterprise clients are rapidly adopting multi-cloud architectures.

This trend implies that AI computing power demand will no longer be concentrated among a few leading cloud providers but will be distributed across multiple cloud platforms. For mid-sized cloud providers like Kingsoft Cloud, this structural shift could present new opportunities.

Yet, the market's ultimate concern remains: Is the AI application boom truly sufficient to alter Kingsoft Cloud's performance trajectory?

Currently, mid-term growth space exists.

From an ecosystem perspective, Goldman Sachs estimates that Xiaomi will invest approximately RMB 10 billion in AI in 2026, with Kingsoft Cloud being a primary beneficiary. In the medium term, Kingsoft Cloud can rely on the rigid AI budget expenditures of Xiaomi and Kingsoft Office to generate predictable revenue growth.

However, long-term uncertainties are equally clear. If Xiaomi's AI ecosystem commercialization lags behind expectations, or if Xiaomi adopts a multi-cloud strategy due to cost or strategic considerations, Kingsoft Cloud's performance could face severe volatility.

Over the past year, Kingsoft Cloud's stock price has fluctuated by over 150%, reflecting capital's Repeated games (repeated wagering) on its "success or failure tied to the ecosystem."

So, returning to the original question: Is this a genuine industrial cycle shift, or merely another round of AI-driven capital narratives?

The answer likely lies somewhere in between.

If Xiaomi's AI ecosystem can truly succeed and AI Agents can transition from concept to widespread adoption, Kingsoft Cloud has the opportunity to become a critical computing power infrastructure within this system and capture a share of the industry's multi-cloud trend. However, if the commercialization of AI applications falls short of expectations, the current revaluation may merely represent a Periodic market trend (temporary rally) rather than a trend reversal.

Before the AI industrial cycle truly unfolds, the debate over Kingsoft Cloud's value has only just begun.

Source: Hong Kong Stocks Research Society

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action