Douyin E-commerce, Trapped in the Traffic Loop

08/07 2024

08/07 2024

788

788

Success or Failure, Both Stem from Traffic?

Produced by | Business Show

"I sold 520,000 yuan worth of goods in a week, but in the end, only less than 80,000 yuan was credited to my account."

In March of this year, Lingzi (pseudonym), the manager of a new women's shoe brand entering Douyin e-commerce, began promoting her brand's new products in a Douyin livestream. On that day, breaking the 100,000 sales mark delighted Lingzi, and she began urging the factory to expedite production and shipment.

However, Lingzi soon discovered that other livestreams were selling identical styles to hers, and these 'competitors' had even changed the materials of the shoes, halving their prices, resulting in their sales soaring rapidly.

The bigger issue was that those who impulsively placed orders in the livestream began requesting refunds, ultimately leaving her with only around 80,000 yuan. Lingzi did the math and realized that after deducting product costs, employee salaries, rent, and traffic costs, coupled with the returned inventory in her hands, she ended up losing money instead of making a profit.

"I admit defeat this time, after all, I'm just starting out in Douyin e-commerce. Next month, I'll introduce some new products, and this time I'll do pre-sales and set a goal of 'no more sales after a certain number of pieces are sold.' Let them copy if they want, if there are a lot of returns, then I'll sell slowly. At least I can afford the returns and won't be like this time," Lingzi reflected in an interview with "Business Show."

"After losing so much, would you still choose to continue on Douyin?" "Business Show" pressed further.

"I'm a 'white label' brand. Right now, besides Douyin, which platform can give me so much traffic and allow me to break 100,000 in sales in a day?" Lingzi countered.

Even after suffering losses, Lingzi's experience is not unique. Behind this lies the core factor attracting countless e-commerce merchants to flood into Douyin e-commerce—traffic.

According to QuestMobile data, as of March 2024, Douyin had 763 million monthly active users, with an average daily usage time of 1.92 hours per person. On Douyin, labeled as a "traffic machine," anything is possible. Whether it's the most bizarre products or content, someone seems willing to pay for it amidst the distributed traffic, especially for merchants with genuine products in hand.

However, from the industry's perspective, essentially, Douyin e-commerce's traffic is Douyin's content traffic, and there is an inherent contradiction between the two in logic. Meanwhile, compared to shelf e-commerce, live e-commerce also has inherent "flaws."

In early July of this year, according to 36Kr, which learned from multiple industry insiders, Douyin is reducing the proportion of influencer livestreams and tilt ing traffic towards high-quality short videos and branded store broadcasts. A source close to Douyin said that Douyin aims to continuously expand the proportion of shelf e-commerce. They also stated that the GMV generated by Douyin product cards (including storefronts, search, Douyin Mall, personalized recommendations, etc.) will account for more than 40% of the entire Douyin e-commerce market, with the remainder coming from short videos and livestreams. In 2025, Douyin product cards will account for more than 50%.

Although Douyin later denied this news externally, an indisputable fact is that as Douyin e-commerce's traffic bonus period gradually comes to an end, merchants who came for traffic and Douyin's e-commerce platform, which is trying to shake off its reliance on traffic, inevitably find themselves in a dilemma.

-Business Show-1

The "Inherent Flaws" of Douyin E-commerce

Before this year's 618 shopping festival, "Luola Mima," a leading women's clothing store on Douyin with 5 million shopping fans, announced that it would cease broadcasting and close its store.

The main reasons were twofold: first, the consistently high product return rate, similar to Lingzi's experience at the beginning; second, merchants spent a significant amount of money on traffic on Douyin (the industry has spread the figure at 30%-35% of sales). Even with billions of yuan in sales, it ultimately led to losses due to the massive traffic costs.

The high return rate of Douyin e-commerce is closely related to its natural field attributes and users' consumption habits. For users here, Douyin is still primarily a content platform, not a spending platform. The traffic of Douyin e-commerce is essentially content traffic, not e-commerce traffic with higher conversion rates and more precision.

Therefore, when many users impulsively place orders as the anchor yells "Three, two, one, go!" and links are shared, subsequent high returns follow. Even this behavior of impulse purchases driven by livestream emotions and quick returns after receiving the goods has been ridiculed by many netizens as a "common ailment" of modern livestream shopping.

According to the "2020 China Live E-commerce Industry Research Report," the average return rate for live e-commerce is between 30% and 50%, a significantly higher proportion than the 10%-15% for traditional e-commerce. In July 2023, the return rate for Douyin jewelry merchants was reported to be as high as 90%; in the heavily affected women's clothing sector, e-commerce platforms generally have return rates of around 50%, while on Douyin, they can reach 70%-80%.

This is an inherent problem that has accompanied Douyin since its inception and the development of live e-commerce—when you open Douyin, you originally came for content, but when you enter a livestream to make a purchase, most of the time, your shopping is unplanned. Under this consumption contrast, a high return rate can easily become the norm.

Beyond the high return rate, Douyin e-commerce's content nature also leaves it facing another dilemma—it's difficult to shake off the label of being a "grass-seeding channel" and ends up benefiting other e-commerce platforms.

In March 2018, Douyin began cooperating with Taobao and tested a shopping cart function for million-follower influencer accounts, allowing users to click and jump to Taobao links to make purchases. Thus, the concept of "Douyin plants the seed, and Taobao harvests the crop" emerged.

At the time, the outside world saw that Douyin could drive sales and understood how short the path from content to purchase was in livestream sales. As Douyin ended its cooperation with other e-commerce platforms and built its own e-commerce ecosystem, Douyin e-commerce achieved a complete closed loop from "seed planting" to "harvesting." However, such a closed loop within the Douyin e-commerce platform cannot occupy consumers' minds.

"Kilala," an early Chinese color contact lens brand on Douyin, was the first to achieve monthly sales exceeding 10 million on the platform. Its relevant person in charge told "Business Show" that current e-commerce is a collaborative effort across multiple channels. For example, Pinduoduo belongs to a nurturing channel with relatively low customer acquisition costs and high overall new customer rates; Douyin is relatively complex, capable of customer acquisition, repeat purchases, and balancing mindset education with transactions; while many people's shopping habits are still ingrained in Tmall, so Tmall remains the channel for meeting rigid demands and high-conversion, precise demographics, responsible for retention and maintaining core, long-term customers.

During this year's 618 promotion, "Kilala" became the top Chinese color contact lens brand across all channels and periods. However, "Kilala" only considers Douyin as an important position within its overall channel layout.

This is also the current state of many e-commerce brands: e-commerce bosses all hope to succeed on Douyin because they are well aware of the effects of channel synergy—"If Douyin does well, search volume on Taobao and JD.com will also increase together. Under the commission-based earnings model, Taobao and JD.com can also reap the benefits together."

However, if we delve into the strategies of most brands on e-commerce platforms, Douyin still primarily serves as a "grass-seeding" brand promotion function, balancing on-site transactions. But doing so ultimately leads to traffic spilling over to other platforms.

Many brand merchants surveyed by "Business Show" unanimously agreed that traffic ultimately labels Douyin e-commerce as a "propaganda front."

At the end of 2020, the old Chinese down jacket brand "Yaya" successfully made a comeback on Douyin, and with Douyin's free traffic, one of its stores quickly achieved daily sales of 2 million yuan. By Douyin's 618 in 2021, "Yaya"'s total GMV exceeded 100 million yuan, ranking first on the women's wear list.

However, on November 8, 2021, when "Yaya" officially announced Li Yifeng as its spokesperson, the opening screen and off-site resources still directed traffic to the brand's old stronghold, Tmall. Just three days later, on Singles' Day, within just half an hour of the start, "Yaya"'s Tmall flagship store sales exceeded 200 million yuan.

"On Douyin, users have no brand loyalty," said an e-commerce practitioner. Even though "Yaya"'s comeback is largely attributed to the Douyin platform, its biggest beneficiary turned out to be Tmall.

-Business Show-2

When Traffic Peaks

Like "Luola Mima," Blue Moon is also engaging in a "lose money to make a noise" strategy.

According to Blue Moon's 2024 profit warning announcement, its sales achieved year-on-year growth of over 38%, with sales from new e-commerce channels (primarily Douyin e-commerce) growing by approximately 4.5 times. However, the company expects a loss of approximately 620 million yuan, a substantial increase of nearly 300% compared to the same period in 2023.

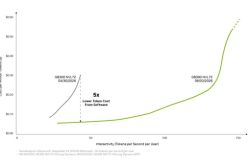

Of course, a core reason behind this is that traffic on Douyin is becoming increasingly expensive.

An industry insider told "Business Show," "In March this year, we realized we had to pay for traffic. Free traffic is becoming scarcer, and merchants' profit margins are being squeezed tighter and tighter. In the past, we spent hundreds of thousands on traffic, but now it's in the millions, and this cost keeps increasing."

In February of this year, Dr. Wen entered the top 10 beauty and skincare rankings on Douyin, a brand that has grown rapidly on the platform.

However, according to calculations by the third-party platform Chan Magic, Dr. Wen's traffic costs amounted to tens of millions of yuan. An article from China Entrepreneur reported that the largest cost for Dr. Wen's brand on Douyin is traffic fees. Industry insiders even claim that merchants' traffic costs can account for 60% or even 70% of sales in certain categories, and with single-digit gross margins, the net profit earned is essentially Douyin's advertising rebates.

The reason behind "losing money to make a noise" is largely believed within the industry to stem from the fact that Douyin e-commerce's traffic is essentially not that of Douyin e-commerce but of Douyin itself. Moreover, the giant traffic pool's distribution rights do not belong to Douyin e-commerce but to Douyin.

But ultimately, Douyin is still a content platform, and everything it does must prioritize content users; otherwise, it would be akin to "draining the pond to catch fish." Just like the successful anchors on Douyin, such as Luo Yonghao, Dong Yuhui, and Xiao Yangge, they all share a common characteristic: their content is highly entertaining and aligns with Douyin's content needs.

As early as April 2022, Douyin made a significant adjustment to its traffic distribution rules: the core essence was that even e-commerce livestreams must also produce good content while selling products, making them enjoyable for users to watch. At the time, Douyin discovered through testing that once more than 8% of the content displayed on Douyin was e-commerce-related, main site users would leave the platform.

This is an awkward situation. Douyin e-commerce relies on Douyin's traffic for its success, but it also harms Douyin's user experience.

Zhuang Shuai, an expert in the retail e-commerce industry and founder of Bailian Consulting, explained to "Business Show" that "essentially, Douyin is still a content platform, and users' habits are those of content users, not e-commerce users. Shopping and product advertisements make users feel like they're spending money, leading to negative feedback."

It is precisely under this logic that, to balance the relationship between content and e-commerce, Douyin has reduced the distribution ratio of e-commerce content.

Another industry insider, who requested anonymity, told "Business Show," "In the past, Douyin didn't have many monetization methods, so e-commerce was crucial, and a lot of traffic (both free and paid) flowed into it. But now that e-commerce growth has slowed, and Douyin's other businesses also need traffic, such as group buying, home delivery, and travel, traffic needs to be redirected to these businesses."

This means that only a portion of Douyin's vast traffic pool will be reserved for commercialization due to its content characteristics, and it will be redistributed among different business lines. As more and more e-commerce merchants enter the fray, and Douyin's other businesses grow, the traffic left for Douyin e-commerce will undoubtedly dwindle.

Therefore, on the one hand, Douyin has begun monetizing the traffic invested in e-commerce as much as possible, with traffic fees accounting for 50% or more of payment GMV becoming the norm; on the other hand, Douyin e-commerce is also placing greater emphasis on the conversion rate of traffic.

According to Caixin, Douyin e-commerce requires brands to achieve a certain annual GMV, and brands will also set annual budgets for advertising to purchase traffic for their products and livestreams.

Regarding related content, "Business Show" inquired with relevant personnel from Douyin e-commerce but did not receive a public response by the time of publication.

-Business Show-3

Can Douyin E-commerce Break Free from the Traffic Loop?

Although Douyin e-commerce is still growing rapidly, the fact is that its growth rate has slowed. According to LatePost, in March of this year, Douyin e-commerce experienced its first year-on-year growth decline, falling below 40%. After the second quarter, the growth rate further dropped to below 30%.

Some media attribute the decline in Douyin e-commerce's GMV growth to its low-price policy. However, in the view of "Business Show," the core reason largely lies in Douyin e-commerce's traffic peaking.

This year, Douyin e-commerce has undertaken numerous initiatives, which "Business Show" summarizes into three main strategies: first, a fluctuating low-price approach; second, more optimized and precise use of traffic (such as reducing the proportion of traffic allocated to influencer livestreams and tilt ing traffic towards high-quality short videos and branded store broadcasts); third, vigorously promoting "shelf e-commerce."

However, these strategies boil down to two cores: first, using existing traffic more efficiently; second, reducing the extent to which its own traffic benefits other e-commerce platforms, thereby achieving a complete closed loop from content to e-commerce and occupying users' minds.

This is particularly evident in the policies related to product cards. Nowadays, for orders where users click on product cards on Douyin or Douyin Lite and proceed to purchase directly or add to their cart from non-livestream, non-short video pages, Douyin e-commerce will directly waive technical service fees.

This means that Douyin e-commerce hopes users will no longer enter through Douyin's traffic pool and that merchants will instead bring e-commerce traffic to the platform themselves.

But this is inherently contradictory. Zhuang Shuai analyzed for "Business Show," "From a market perspective, consumption comes in two main types—one is purposeful shopping, such as when consumers search on Tmall or JD.com; the other is non-purposeful shopping, like browsing or watching videos that lead to purchasing behavior. If Douyin doesn't pursue shelf e-commerce, it will miss out on the larger purposeful shopping market. From a merchant's perspective, the thresholds and operating costs of shelf e-commerce are certainly lower than those of live e-commerce. From a platform perspective, product variety can significantly increase an e-commerce platform's GMV. From an industry competition perspective, shelf e-commerce is also increasing its content investment, posing a threat to Douyin e-commerce."

In essence, no matter the strategy, the question returns to its origins: Why does Douyin e-commerce want to pursue shelf e-commerce?

Obviously, the industry consensus is that shelf e-commerce does not share the "inherent flaws" brought about by live e-commerce's reliance on traffic for its inception. But the question remains: Why do merchants want to do Douyin e-commerce? Naturally, it's because of Douyin e-commerce's traffic.

In a nutshell, Douyin E-commerce wants to take the path of shelf e-commerce, which essentially contradicts the expectations of e-commerce merchants towards Douyin E-commerce.

The cruel reality is that Douyin E-commerce, which wants to break out of this traffic trap, and Douyin merchants who want to tap into the traffic dividend, have arrived at a crucial crossroads.

Of course, when Douyin E-commerce wants to weaken its original live streaming e-commerce attributes, new problems and challenges will only be greater. "What are the differences and advantages of Douyin E-commerce as a shelf e-commerce platform?" This is a question worth pondering. As of press time, Douyin E-commerce has not responded.

"The most common differences in e-commerce and retail are product category differentiation and model differentiation. We now remember Pinduoduo's agricultural products, JD.com's 3C products, Taobao's beauty products and clothing, but all Douyin leaves us with are Dong Yuhui and Xiao Yangge." Zhuang Shuai said. [End]

-

![]()

Is Baidu Now Fostering Its Own 'Yao Shunyu'?

-

![]()

NVIDIA Goes Wild! DeepSeek V4 Inference Costs Slashed by 80%

-

![]()

Preparing for the 6G Era: US Completely Shuts Down 2G Networks, China Unicom Initiates Gradual Decommissioning of WCDMA 3G Networks

-

![]()

Mid-year 2026 Sales Review: Auto Market Shifts from Scale Expansion to Systemic Capabilities for Long-term Positioning

-

![]()

From the ARD Protocol, the Turning Point for the Agent Industry Has Arrived

-

Pinduoduo's Strategic Leap in Xiong'an: Beyond Investment, a Pledge to Flourish

-

Liang Wenfeng Has No Desire to Become Another Sam Altman

-

![]()

Revenue Soars, Losses Mount in Billions, Sales Stumble: Avatr's Hong Kong IPO Bid Amid Breakthroughs and Anxieties