Shopify: Amazon stumbles while independent e-commerce soars?

08/09 2024

08/09 2024

681

681

On the evening of August 7, Beijing time, before the US stock market opened, Shopify, the leading independent e-commerce company in the US, released its financial results for the second quarter of 2024. Overall, core operating metrics for its payment and subscription businesses exceeded expectations, with subscription performance particularly robust. Exaggerated cost control helped the company squeeze out significantly higher-than-expected profits, marking an outstanding performance. Key details are as follows:

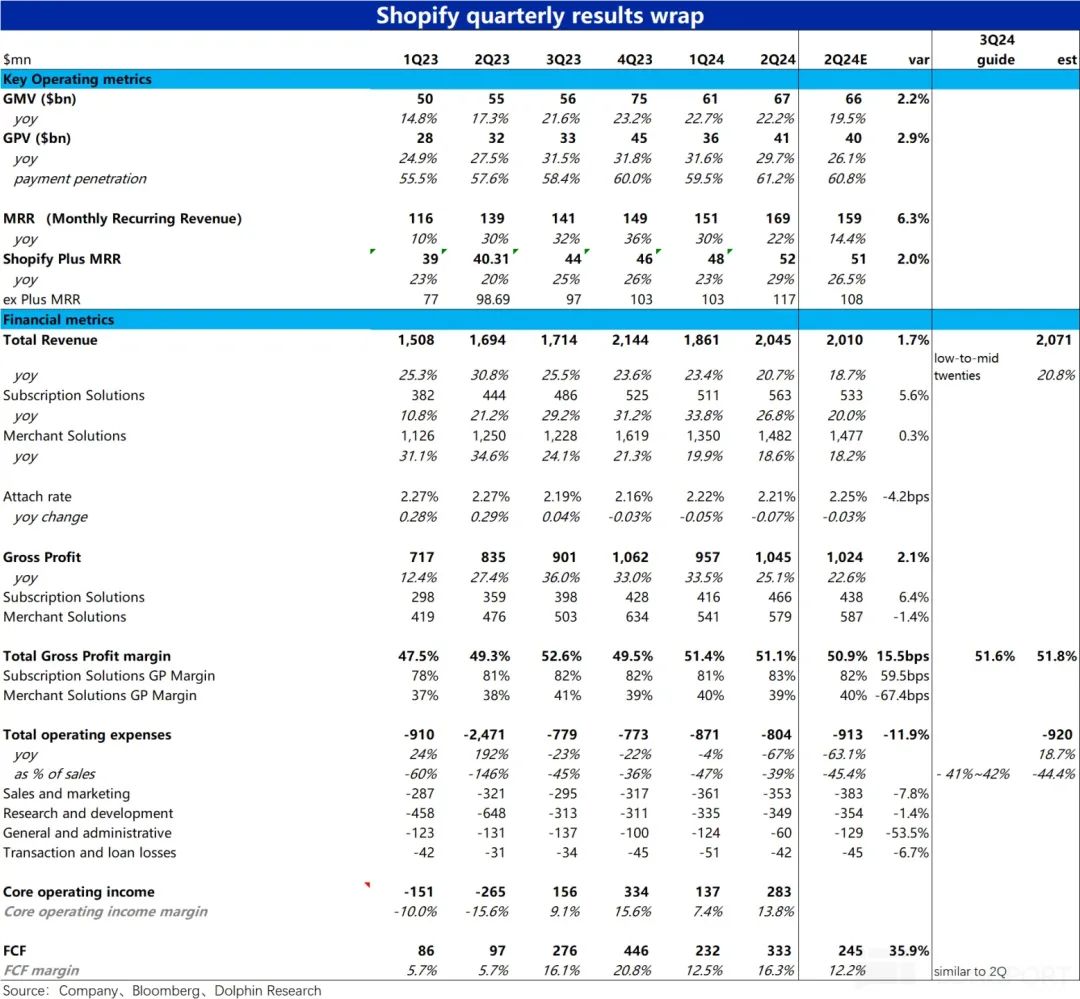

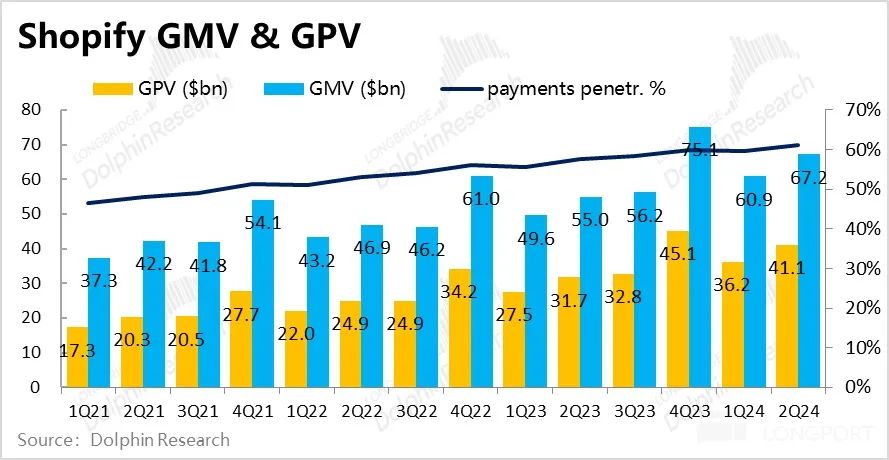

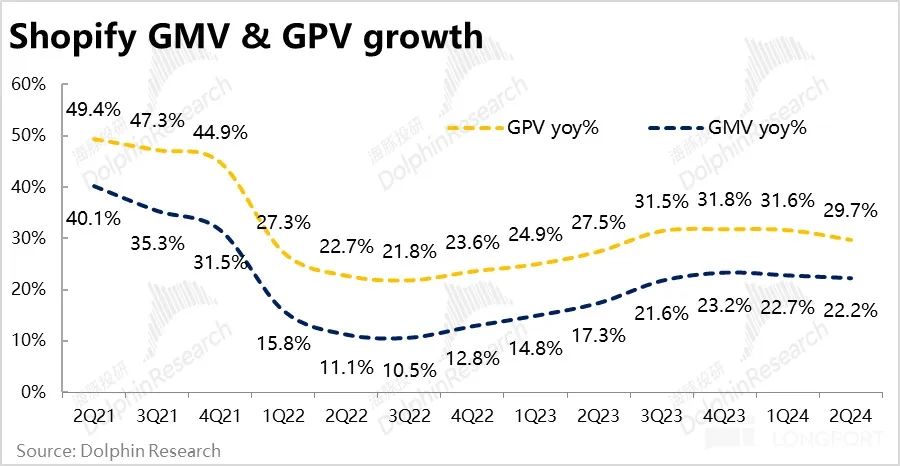

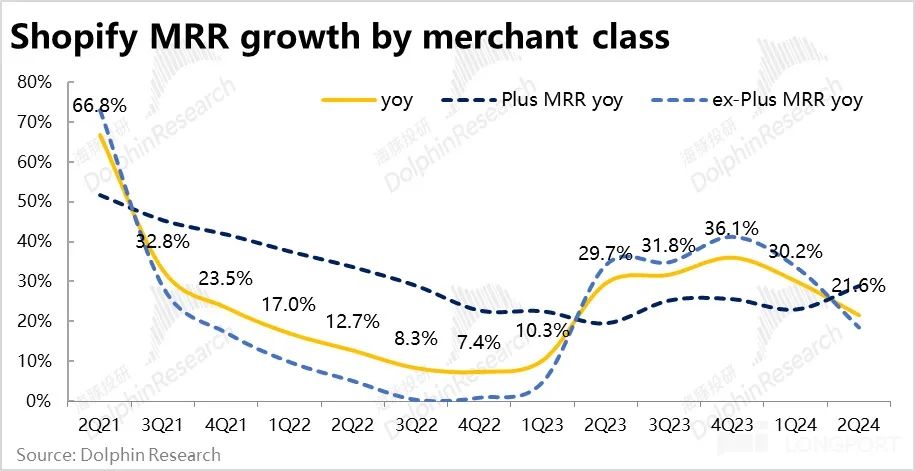

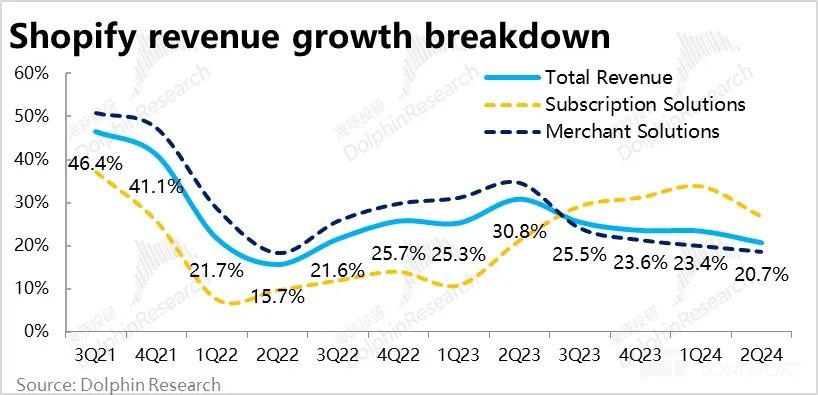

1. Core Operating Metrics: This quarter, Shopify's total gross merchandise volume (GMV) reached $67.2 billion, a year-over-year increase of 22.2%, a steady growth rate that exceeded expectations by approximately $1.5 billion (2.2%). Total payment volume was $41.1 billion, $1.1 billion (+2.9%) higher than expected and up 29.7% year-over-year. The penetration rate of Shopify's own payment channels increased from 59.5% to 61.2% quarter-over-quarter, slightly higher than the expected 60.8%. Monthly recurring revenue (MRR), reflecting subscription business performance, was $169 million per month, a year-over-year increase of 21.6%, significantly above the expected $159 million, making it the most impressive aspect of the quarterly report. MRR contributed by Plus merchants grew by 29% year-over-year, while non-Plus merchants grew by only 18.6%, indicating that the robust growth in subscriptions was driven by Plus merchants.

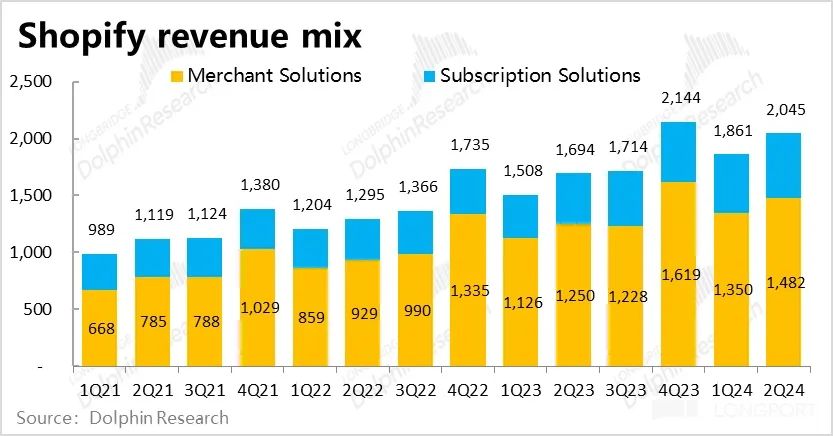

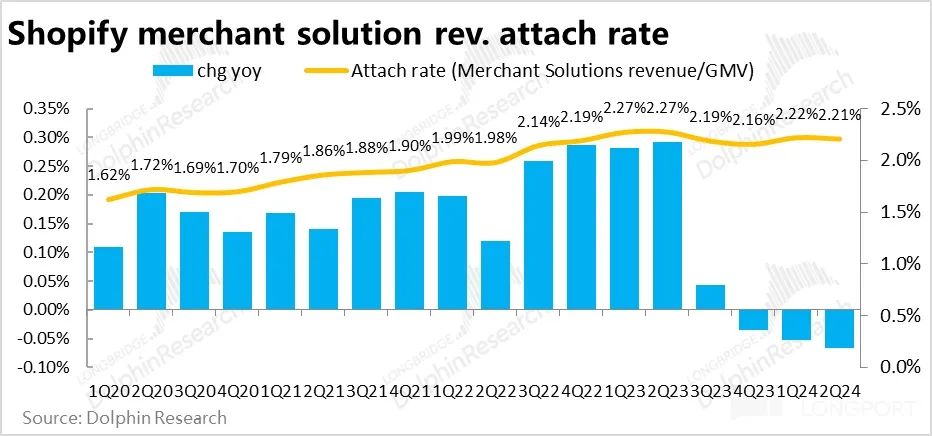

2. Revenue: Merchant services revenue was $1.48 billion, a year-over-year increase of 18.6%, slightly lower than GMV and GPV growth rates and also below market expectations. The monetization rate (as a percentage of GMV) for merchant services revenue decreased by 7bps year-over-year to 2.21%. We believe this decrease is a reasonable consequence of the increased proportion of Plus merchants. Subscription services revenue, in line with the strong MRR growth, increased by 26.8% year-over-year, 5.6% higher than expected.

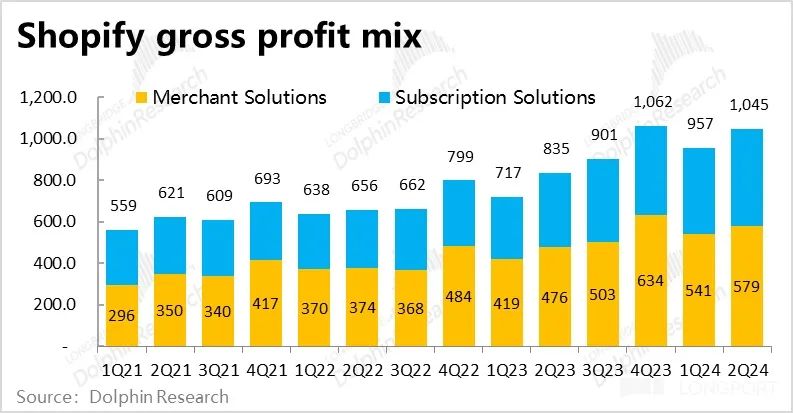

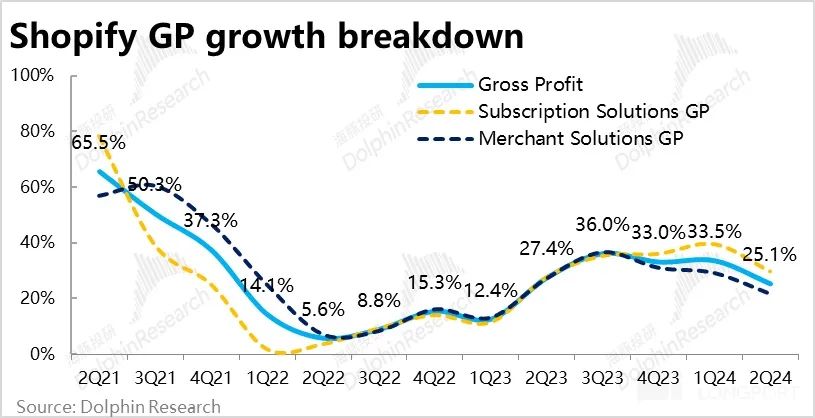

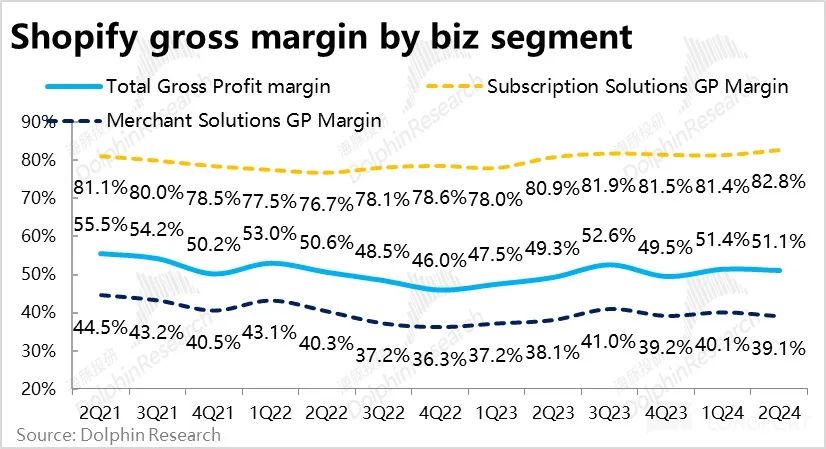

3. Gross Profit: Subscription services gross margin increased by 1.4ppt quarter-over-quarter to 82.8%. With both revenue growth and gross margin improvement, gross profit exceeded expectations by an even larger margin of 6.4%. Merchant services gross margin decreased slightly by 0.3ppt quarter-over-quarter due to the decline in monetization rate, resulting in a gross profit of $579 million, slightly below expectations by 1.4%.

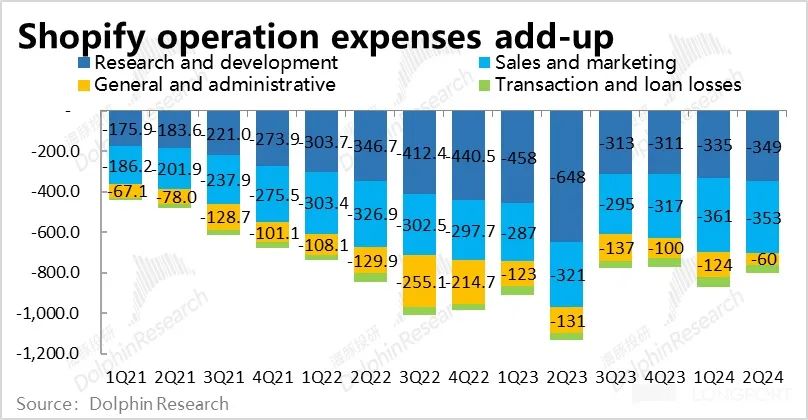

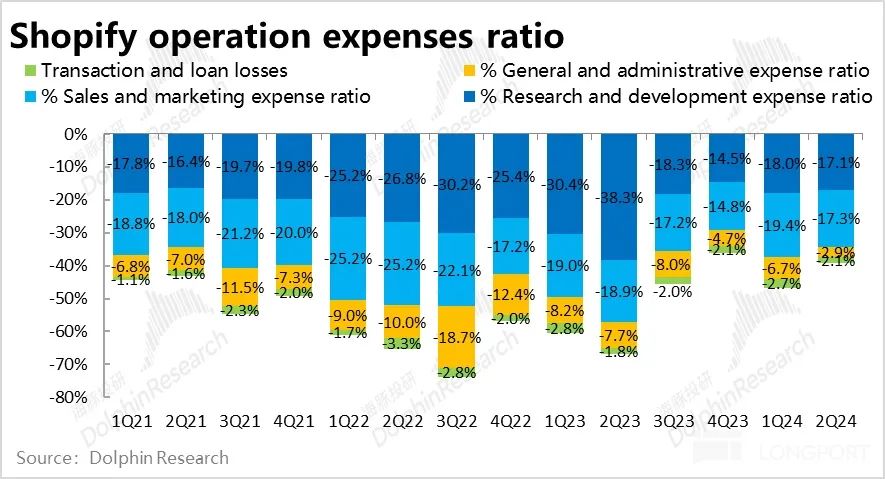

4. Expenses: Shopify's significantly lower-than-expected expenses contributed significantly to profit release. Total operating expenses were approximately $800 million, $100 million (-11.9%) lower than market expectations. Marketing expenses were $30 million less than expected, and administrative expenses were halved year-over-year to only $60 million, $70 million lower than expected.

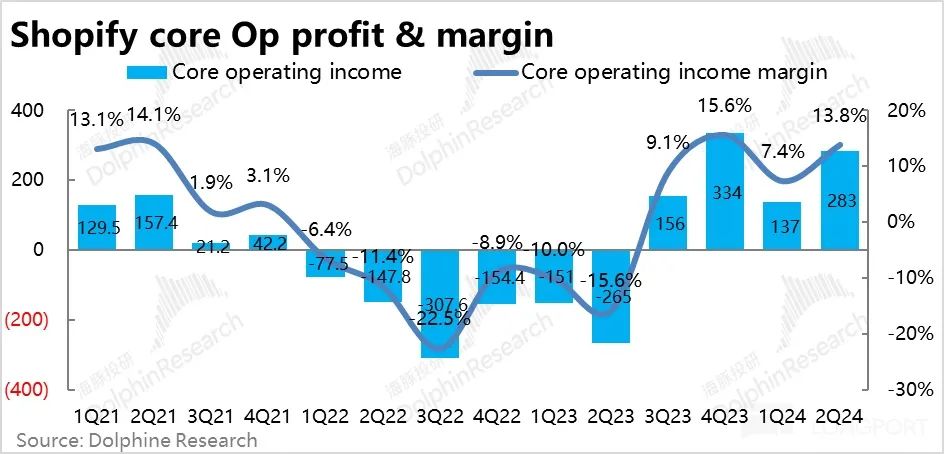

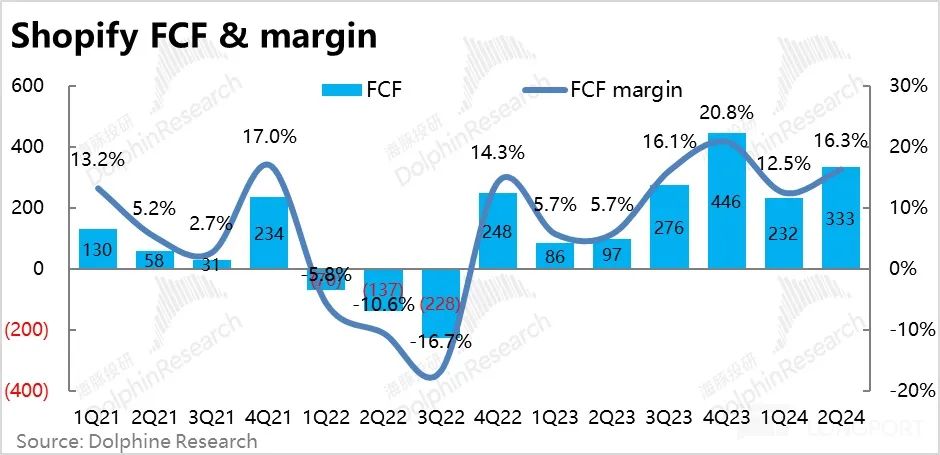

5. Total gross profit exceeded expectations by approximately $20 million, and excellent expense control squeezed out an additional $100 million in profit. This resulted in a near-doubling of the company's core operating profit quarter-over-quarter, increasing by nearly $140 million. Free cash flow profit, which the company values more, was $330 million, an increase of approximately $100 million quarter-over-quarter and $90 million higher than expected.

Dolphin Investment Research Insights:

Based on this quarter's results, both subscription and merchant services business operating metrics exceeded expectations. Although revenue growth was slightly narrower than expected due to the decline in monetization rate, overall revenue and gross profit remained impressive, driven by the stronger subscription business. With exaggerated cost reductions, the incremental profits squeezed out led to a doubling of GAAP operating profits (though also influenced by a low profit base). Nevertheless, the growth, cost control, and profit release undoubtedly constitute an outstanding performance.

Looking ahead to the next quarter, the company expects revenue growth of approximately 20%~25% (20.7% this quarter) while expecting expenses to account for only 41%~42% of revenue, significantly lower than market expectations of 44.4%. In other words, high growth and margin expansion will continue next quarter.

From a valuation perspective, with the company's current high single-digit P/S ratio and double-digit P/E ratio, it is difficult to objectively assess whether it is undervalued or overvalued. Judgments on subsequent stock price movements will largely depend on the trend of marginal changes in performance.

Detailed Interpretation of This Quarter's Financial Report

I. Subscription and Payment Operating Metrics Both Exceeded Expectations

As usual, let's start with the operating metrics that best reflect the true situation. This quarter, Shopify's total GMV was $67.2 billion, a year-over-year increase of 22.2%, with stable growth. Actual GMV exceeded expectations by approximately $1.5 billion (2.2%).

Total payment volume processed through Shopify Payment was $41.1 billion, $1.1 billion (+2.9%) higher than expected and up 29.7% year-over-year. The growth rate of payment volume was higher than that of sales, indicating an increase in the proportion of total GMV processed through Shopify Payment, from 59.5% to 61.2% quarter-over-quarter, slightly higher than the expected 60.8%. As Shopify can generate more revenue through payments, the increase in payment penetration is beneficial to the growth of merchant services revenue.

MRR (Monthly Recurring Revenue), reflecting subscription business performance, was $169 million per month this quarter, a year-over-year increase of 21.6%. (Roughly interpreted as Shopify collecting $169 million in monthly subscriptions from merchants), significantly higher than the expected $159 million. Subscription revenue was the most impressive aspect of this quarter's business. MRR contributed by Plus merchants increased by 29% year-over-year, while MRR growth for non-Plus merchants was only 18.6%, lagging behind overall growth. In other words, the robust growth in subscriptions was driven by Plus merchants.

II. Slightly Lower Monetization Rate Slightly Drags Down Merchant Services Revenue, While Subscription Services Remain Strong

In terms of revenue, merchant services revenue was $1.48 billion this quarter, a year-over-year increase of 18.6%, which did not outperform GMV and GPV growth rates or significantly exceed market expectations. The reason is that the monetization rate (as a percentage of GMV) for merchant services revenue decreased by 7bps year-over-year to 2.21%. Considering the outperformance of Plus merchant MRR, we believe the decrease in the monetization rate for merchant services is a reasonable consequence of the increased proportion of larger merchants with stronger pricing power. Subscription services revenue trends were closely aligned with MRR metrics, with revenue increasing by 26.8% year-over-year, 5.6% higher than expected. Revenue-wise, subscription revenue also performed more robustly.

Thanks largely to strong subscription revenue, Shopify's total revenue for this quarter was $2.045 billion, a year-over-year increase of 20.7%, slightly higher than expected by 1.7%.

III. Merchant Services Gross Margin Slightly Decreases, While Subscription Services Gross Margin Increases

From a gross profit perspective, not only did subscription services revenue growth exceed expectations, but their gross margin also increased by 1.4ppt quarter-over-quarter to 82.8%. Amplified by the increase in gross margin, gross profit exceeded expectations by an even larger margin of 6.4%. In contrast, due to the decline in the monetization rate of merchant services both year-over-year and quarter-over-quarter, merchant services gross margin decreased slightly by 0.3ppt quarter-over-quarter. As a result, merchant services gross profit was $579 million, slightly below expectations by 1.4%.

Combining the two businesses, total gross profit was still 2.1% higher than expected, with approximately $1.05 billion exceeding expectations by approximately $20 million. Year-over-year growth was 25.1%, still outperforming total revenue growth of 20.7%.

IV. Drastic Cut in Administrative Expenses: The Biggest Contributor to Incremental Profits

From an expense perspective, Shopify's significantly lower-than-expected expenses contributed even more significantly to profit release this quarter. Specifically, total operating expenses were approximately $800 million, $100 million (-11.9%) less than market expectations. All four operating expenses were lower than expected, with marketing expenses $30 million less than expected, and administrative expenses halved year-over-year to only $60 million, $70 million less than expected. Even without considering the expected difference, the proportion of the four operating expenses to revenue all decreased quarter-over-quarter. However, the financial report did not explain why administrative expenses plummeted, so we may need to wait for further explanations in the earnings call.

V. Operating Profits Double with Revenue Growth and Cost Control

Due primarily to stronger-than-expected subscription revenue, the company's total gross profit exceeded expectations by approximately $20 million this quarter, and through cost control, an additional $100 million in profits was squeezed out. As a result, the company's core operating profit increased by nearly $140 million quarter-over-quarter, nearly doubling. The company's more closely watched free cash flow profit was $330 million this quarter, an increase of approximately $100 million quarter-over-quarter and $90 million higher than the expected $245 million. Although the extent of exceeding expectations was lower than that of GAAP operating profits, it was undoubtedly still significantly above expectations.

- END -

// Reprint Authorization

This article is originally created by Dolphin Investment Research. Please obtain authorization for reprinting.

-

![]()

Behind the Release of Its First Self-Developed Chip, Is OpenAI's Full-Stack Ambition on Display?

-

![]()

Has Anthropic Targeted Chinese Users? Is a New Era of AI-Driven Racial Discrimination Emerging?

-

![]()

MathWorks: Generative AI Holds Great Potential, Yet a Trusted Toolchain is Essential for Flawless Operation

-

![]()

Small Earphones, Big Business

-

![]()

Volkswagen Slashes 100,000 Jobs, Mercedes-Benz Axes Year-End Bonuses: What’s Ailing German Auto Titans?

-

![]()

Doubao Can No Longer Offer Free Services to 345 Million Users: China's Era of Free AI Is Drawing to a Close

-

![]()

How Can Chinese Small Home Appliances Conquer Southeast Asia Through 'Dimensional Competition'?

-

![]()

Why are top intelligent driving players betting on reinforcement learning?