Young Indifference and High-End Inaccessibility: Is Skyworth Facing a 'Double Bind'?

04/22 2025

04/22 2025

696

696

Amidst the confluence of consumption upgrades and technological advancements, the smart TV market is undergoing a transformative shift unprecedented in recent times. According to AVC monitoring data, the escalation in TV size structure has accelerated since 2024, with 75-inch TVs emerging as the fastest-growing segment across all channels. This underscores a clear trend towards larger screens in the TV market. Concurrently, the rivalry among Mini LED, OLED, and 8K resolution technologies is pushing the boundaries of display quality and interactive experiences, while the profound integration of AI technology is transforming TVs from mere 'hardware products' into 'intelligent home hubs'.

In this metamorphosis, Skyworth TV presents a paradoxical picture. Data reveals that in 2024, Skyworth shipped 6.1 million units, securing a 17.0% market share—a 0.4 percentage point increase from 2023. Despite the overall market downturn, Skyworth has maintained growth, demonstrating resilience. However, this veneer of success masks underlying challenges. Financial reports indicate that in 2024, Skyworth Group's total operating revenue was 66.248 billion yuan, a 5.41% year-on-year decline, with net profit attributable to shareholders falling 46.87% to 568 million yuan.

As the industry transitions from 'scale expansion' to 'value deepening', can this veteran manufacturer, with over three decades of history, sustain its position and even achieve a breakthrough amidst the technological tsunami and market fragmentation? The answer may lie in the finer details.

Sales Surge and Market Frenzy: Skyworth's Fleeting Glory

In recent years, China's smart TV market has witnessed growth fueled by policy incentives and consumption upgrades. Leveraging its deep technical expertise and channel advantages, Skyworth TV has become a focal point in the industry.

AVC data from W1-W52 (January 1st to December 29th) 2024 shows that Skyworth's 100-inch TV sales accounted for 39.4% of total sales across all channels, with sales volume comprising 37.1%, firmly placing it at the top nationally. Notably, the 100Q7D model led the 20,000 yuan price bracket for 100-inch TVs. While these figures are impressive, they conceal underlying concerns.

Firstly, the sustainability of growth in the 100-inch TV segment is uncertain. As a niche within the high-end large-screen sector, the 100-inch TV market's development is constrained by consumer base size and product premium capacity. Despite the acceleration in screen size trends and cost optimization in recent years, there is an inherent ceiling on market size.

AVC data indicates that 75-inch products accounted for 24.1% of sales volume in China's TV market in 2024, up 4.2 percentage points from 2023. Clearly, 100-inch TVs are not the mainstream, and Skyworth's dominance in this niche is insufficient to offset potential market share dilution in mainstream sizes.

Furthermore, as industry players expedite their ultra-large-screen product matrix layouts, competition extends from single-technology rivalry to full-industry chain collaboration capabilities. Leading brands like Hisense and TCL are reshaping the large-screen TV market landscape through technological reserves and channel resource integration, placing dynamic pressure on Skyworth's current market position.

Secondly, Skyworth's technological path is wavering, caught between OLED and Mini LED. As an early leader in the domestic OLED TV market, Skyworth once dominated with a substantial market share. However, the Mini LED technology wave has posed a strategic choice in adjusting its technological route.

In 2023, Skyworth invested heavily in building a Mini LED technology matrix, but its first mass-produced model lagged behind TCL by nearly two product iteration cycles. CMM data for 2023 revealed that TCL led China's Mini LED TV retail sales with a 50.5% market share, while Skyworth's share was 10%. This hesitation during the technological transition reflects Skyworth's adaptation dilemma between reconstructing its core competencies and adapting to dynamic market demands.

AI Strategy Misalignment: The Gap Between Technological Investment and Market Execution

Amidst the global AI wave, Skyworth did not miss the boat. However, despite its 'All in AI' claim, Skyworth's actual results lag significantly behind industry leaders.

Firstly, while Skyworth's AI product matrix showcases a multi-dimensional layout, it lacks flagship products. In 2022, Skyworth established the 'AIoT 5.0' technology framework, launching a comprehensive range of smart home products including smart TVs, refrigerators, air conditioners, etc., forming a product matrix spanning all smart home scenarios. Concurrently, it introduced the 'Xiaowei AI Assistant' smart voice hub, but the strategy's implementation fell short of expectations. Market feedback highlighted significant shortcomings in its product ecosystem, particularly in ecological compatibility, where Skyworth's smart home system supports interconnection with only over 30 brands, in stark contrast to Xiaomi's open ecosystem encompassing thousands of manufacturers.

Secondly, despite Skyworth's consistent R&D investment, breakthroughs in core technologies have been sluggish. Technology is a company's foundation, and Skyworth emphasizes R&D. However, due to its diversified business, R&D resources are dispersed across multiple fields like display technology, AI algorithms, IoT, and new energy, slowing core technology breakthroughs.

Thirdly, Skyworth's commercialization of cutting-edge technologies faces market validation challenges. At CES 2024, Skyworth showcased two flagship Mini LED wallpaper TVs, a new OLED transparent TV, a 165-inch Micro LED TV, projectors, beauty refrigerators, mini washing machines, wall-mounted air conditioners, and more. While these products garnered attention at industry exhibitions, their market penetration remains low, and the premium of technological innovation has not translated into substantial revenue.

Dual Pressure of Emerging Market Breakthroughs and Brand Aging

Skyworth's globalization strategy started early but encountered setbacks in localized operations and brand upgrades in regional markets.

On one hand, Skyworth faces significant challenges in penetrating the European high-end TV market. According to Omdia, Samsung Electronics holds a substantial advantage in the high-end and ultra-large-size TV markets with its Neo QLED, OLED, and lifestyle series. In Europe, Samsung's market share stands at 60.7%. Competing against such strong rivals will be challenging for Skyworth.

Notably, despite attempting to differentiate with OLED technology, Skyworth failed to build a corresponding content ecosystem. In contrast to LG's integration of mainstream European streaming platforms through the WebOS system, Skyworth's Android TV custom system experiences application adaptation delays. This structural contradiction between technological prowess and ecological deficiencies prevents the innovation awards won by its X1 Pro series at the IFA exhibition in Germany from translating into actual sales conversion rates.

On the other hand, Skyworth's brand recognition is weak among Gen Z consumers. According to iiMedia Research, in 2024, Xiaomi, Hisense, and Skyworth ranked top three among smart TV brands purchased by Chinese users, with proportions of 23.58%, 19.50%, and 17.30%, respectively. Skyworth's brand communication heavily emphasizes product parameter analysis and quality endorsements, resulting in low reach on youth-oriented platforms like Bilibili and Xiaohongshu, failing to establish emotional connections with the new generation.

The frenzy of sales growth cannot obscure Skyworth's deep-seated crises in technological iteration, AI implementation, and global operations. Amidst the dual revolutions of intelligence and globalization, this established home appliance giant's transformation has reached critical waters. Without the resolve to reimagine its technological path and rebrand itself, Skyworth risks fading in the new industry reshuffle. After all, the market's applause will always resonate with true innovators.

-

![]()

Rokid's Ambition and Embarrassment: 300,000 Sales Can't Support Its Ecosystem Dream

-

Are Gaming Ventures No Longer in Vogue Among Tech Titans?

-

![]()

Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

-

![]()

Valued at $18 Billion with a Five-Year IPO Plan: Kuaishou’s Kling AI Takes a Bold Leap

-

![]()

NVIDIA Launches 'Computing Power Financing'

-

![]()

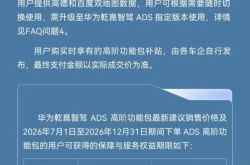

Following Up on the 'Safety Net' for Intelligent Driving: Is Huawei's Strategy Astute or Perilous?

-

![]()

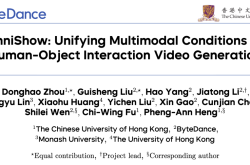

ICML 2026 | One Model to Unify Humans, Objects, Sounds, and Actions: OmniShow Revolutionizes Multimodal Controllable Video Generation as a Systematic Engineering Feat!

-

![]()

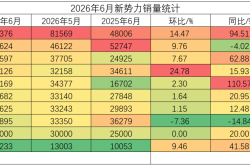

Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma