Following the Inquiry into the Technological Advancement of Over 100 Inherited Patents, Tracing Back and Assessing the Value of Shareholders' Contributions on the Eve of Application

06/13 2024

06/13 2024

754

754

The new regulations issued by the China Securities Regulatory Commission (CSRC) on March 15, 2024 stated that the regulator will strictly examine "pseudo-technology." Additionally, the "Nine National Policies" also proposed improving the evaluation criteria for the technological innovation attributes of the Science and Technology Innovation Board (STAR Market). Based on these guidelines, the Shanghai Stock Exchange has revised its listing review rules and the interim provisions for the STAR Market, requiring that companies applying for listing on the STAR Market should be "hard technology" enterprises with strong growth potential.

On March 30, 2024, after more than a year of attempting to list on the ChiNext, DeYiWei Microelectronics Co., Ltd. (hereinafter referred to as "DeYiWei") terminated its listing process due to its voluntary withdrawal of the application materials. On April 11, 2024, a research report released by Jinzheng Research titled "DeYiWei: Indirectly Investing in Customers and Collaborating the Following Month, the Original President of a Subsidiary Established a Company Contributing Over 90 Million Yuan in Revenue" pointed out that DeYiWei collaborated with a customer the month after indirectly investing in them, and another indirectly invested customer contributed over 50 million yuan in cumulative revenue. The founder of a customer with transactions exceeding 90 million yuan was the former president of a DeYiWei subsidiary.

In this attempt to go public, DeYiWei had a dispersed shareholding structure with no controlling shareholder or actual controller. While its revenue growth was significant, it continued to "lose blood," with over half of its revenue coming from its top five customers. Looking back at the two rounds of inquiries, DeYiWei boasted that its six core technologies reached "internationally leading" levels, and the regulator primarily inquired about DeYiWei's technological innovation capabilities from multiple dimensions.

It is worth noting that the shareholders who established DeYiWei were a partnership enterprise, and two shareholders who subsequently increased their capital investment and became shareholders have become subsidiaries of DeYiWei after undergoing capital reduction or share swaps. The legitimacy of their establishment and acquisition has been questioned. In addition, DeYiWei has also acquired peer companies held by its shareholders, and the business development and technological breakthroughs of DeYiWei before and after the acquisition have attracted regulatory attention.

I. No Controlling Shareholder or Actual Controller, Significant Revenue Growth but "Losing Blood" for Three Consecutive Years

In this listing application, DeYiWei did not have a controlling shareholder or actual controller.

According to the prospectus signed by DeYiWei on November 18, 2022 (hereinafter referred to as the "Prospectus signed on November 18, 2022"), as of the signing date, DeYiWei's shareholding structure was relatively dispersed, with no controlling shareholder or actual controller.

As of the signing date of the prospectus on November 18, 2022, DeYiWei had a total of 64 shareholders. The largest shareholder, Zhicun Micro, held 11.24% of the shares, and both it and Shanding Technology were the company's employee shareholding platforms and were under the same control (Wu Dawei served as the executive partner of both Zhicun Micro and Shanding Technology), holding a combined 11.7% of the shares. The second-largest shareholder, EpoStar, held 7.93% of the company's shares.

Additionally, the executive partners of Huaxin Chuangyuan and Hefei Chenshan were Huaxin Investment or entities where Huaxin Investment served as the executive partner, and they held a combined 5.28% of the company's shares. DeYiWei's shareholding structure was dispersed, and none of the individual shareholders or shareholders under the same control held or could effectively control more than 30% of the voting rights in DeYiWei either individually or collectively. Furthermore, there were no other concerted action arrangements among DeYiWei's major shareholders, and they did not constitute control over DeYiWei.

According to the prospectus signed on November 18, 2022, from 2019 to 2021 and the first half of 2022, DeYiWei's operating revenue was 126 million yuan, 207 million yuan, 745 million yuan, and 471 million yuan, respectively, with year-on-year growth rates of 64.34% and 260.15% in 2020-2021.

From 2019 to 2021 and the first half of 2022, DeYiWei's net profits were -83.8317 million yuan, -292.9174 million yuan, -69.0633 million yuan, and -36.4207 million yuan, respectively, with year-on-year growth rates of -249.41% and 76.42% in 2020-2021.

According to the prospectus signed on November 18, 2022, from 2019 to 2021 and the first half of 2022, DeYiWei's net cash flow from operating activities was -77.7877 million yuan, -164.4843 million yuan, -404.7618 million yuan, and -176.1091 million yuan, respectively.

Founded on November 7, 2017, DeYiWei is a chip design company with storage control technology as its core. Its main business is the research, design, and sales of storage control chips and storage solutions. Its main products and services include three major product lines: solid-state drive (SSD) storage control chips, embedded storage control chips, and expandable storage control chips, as well as storage solutions based on storage control chips such as storage control IP, memory products, and technical services.

According to the prospectus signed on November 18, 2022, from 2019 to 2021 and the first half of 2022, DeYiWei's sales revenue from storage control chips was 55.0882 million yuan, 79.4928 million yuan, 223.8762 million yuan, and 119.9183 million yuan, respectively, accounting for 54.67%, 48.74%, 31.73%, and 26.76% of the main business revenue. The revenue from storage solutions based on storage control chips was 45.6682 million yuan, 83.5883 million yuan, 481.6966 million yuan, and 328.247 million yuan, respectively, accounting for 45.33%, 51.26%, 68.27%, and 73.24% of the main business revenue.

From a sales region perspective, DeYiWei's sales revenue from Hong Kong, China was 56.021 million yuan, 101.7989 million yuan, 562.8701 million yuan, and 327.9824 million yuan, respectively, accounting for 55.6%, 62.42%, 79.77%, and 73.18% of the main business revenue.

According to data cited in the prospectus signed on November 18, 2022, DeYiWei's global market share of SSD storage control chips was 4%.

In terms of customer concentration, during the reporting period, over half of DeYiWei's revenue came from its top five customers.

From 2019 to 2021 and the first half of 2022, the combined sales revenue of DeYiWei to its top five customers accounted for 70.26%, 56.05%, 65.26%, and 70.49% of the current period's operating revenue, respectively.

On April 11, 2024, a research report released by Jinzheng Research titled "DeYiWei: Indirectly Investing in Customers and Collaborating the Following Month, the Original President of a Subsidiary Established a Company Contributing Over 90 Million Yuan in Revenue" mentioned that during the reporting period, DeYiWei had customers that collaborated immediately after establishment, with cumulative transactions exceeding 50 million yuan. Curiously, DeYiWei indirectly held equity in this customer through a participating company, and the month the investment agreement was signed, DeYiWei transferred patents to it.

Moreover, from 2020 to 2022 and the first half of 2023, the cumulative transaction amount between Netac Technology, a major customer, and DeYiWei exceeded 90 million yuan. One of the founders of Netac Technology, Cheng Xiaohua, was an indirect shareholder and president of DeYiWei's subsidiary, Shenzhen Sigotek.

For companies applying for listing on the STAR Market, their innovation capability is the top priority of regulatory inquiries.

II. Boasting Its Core Technologies as "Domestically Leading," Inquiries into the Specific Manifestations of the Technological Advancement of Over 100 Inherited Patents

According to the first-round inquiry response, (1) the major market share and cutting-edge technologies for storage particles and storage control chips are still in the hands of international giants such as Samsung, Micron, and SK Hynix. DeYiWei possesses six core technologies covering various key technical fields of storage control chips, reaching a "domestically leading" technological level. However, it did not provide a specific analysis combining the comparison with comparable companies' technologies, and the comparison scope and selection of competitive products in the application materials were limited, with inconsistent comparison indicators.

(2) During the reporting period, IP licensing revenue was 5.1215 million yuan, 4.7582 million yuan, and 10.8739 million yuan, respectively; technical service revenue was 1.164 million yuan, 1.3441 million yuan, 3.7216 million yuan, and 6.5933 million yuan, respectively, showing a gradual increase in revenue amount.

(3) DeYiWei obtained a total of 107 patents through succession, with transferors including Taiwan Dahsin or EpoStar, Huaxida Technology, South China University of Technology, Guangdong University of Technology, and transfers between DeYiWei subsidiaries. In the past two years, the book value of DeYiWei's intangible assets has increased significantly. During the reporting period, DeYiWei purchased semiconductor IP licensing services from Shenzhen Dahsin for a total of 1.021 million yuan, goods from Taiwan Dahsin for a total of 1.47 million yuan, and technology development services and franchise rights from Phison Electronics for a total of 3.6767 million yuan, based on its R&D and production needs.

(4) DeYiWei's ongoing research projects include three types of storage control chip product line projects and a "low-level technology research and development and technology platform optimization" project. New storage products such as computational storage and distributed storage have gradually increasing performance requirements for storage control chips. According to relevant media reports, storage technologies iterate rapidly in terms of storage density, stacking processes, performance-to-power consumption ratio, etc., placing higher demands on suppliers' cost capabilities.

(5) For its memory product business, DeYiWei sells its self-developed storage control chips and externally purchased storage particles to customers after outsourcing them into memory products.

Therefore, the regulator required DeYiWei to explain: (1) the technological gap and breakthrough difficulties between domestic and foreign storage control chips and memory products, and whether there is a progressive relationship in technical difficulty among DeYiWei's various products.

(2) Combining the number of parameter models, process layers, and comparisons with industry peers that DeYiWei's various storage control chips can adapt to storage particles, as well as comparisons with comparable companies in the industry in terms of memory product performance, power consumption, capacity, speed, reliability, and stability, respectively explain the specific manifestations of the advanced nature of DeYiWei's aforementioned products and core technologies, whether the statement of "domestically leading" is objective, and specify the revenue and gross margin percentages of the compared products, whether they are DeYiWei's main products, and whether the compared competitive products are industry-leading/mainstream products and their launch times.

(3) The necessity and fairness of DeYiWei obtaining a large number of patents through succession, distinguishing between self-developed and externally purchased technologies, explaining the source, formation, and evolution process of DeYiWei's core technologies, the specific content of DeYiWei's externally purchased IP, technology development services, franchise rights, and products, whether there is external technology/IP dependence, and whether it has independent innovation and continuous R&D capabilities.

(4) The basic situation of DeYiWei's ongoing research projects, the R&D achievements that have been formed and are expected to be formed, the specific content of the "low-level technology research and development and technology platform optimization" project and its relationship with DeYiWei's existing core technologies and products; the technological iteration cycle and future development trends of storage control chips and memory products, whether DeYiWei has corresponding technological and personnel reserves in new technological fields, whether its cost control capabilities have an advantage, and whether DeYiWei's technological R&D can adapt to the needs of future technological iterations.

(5) Whether DeYiWei's IP licensing services and technical services possess technological advancement and specific manifestations. Combining the main outsourcing content and business processes of memory, explain DeYiWei's role and function in such businesses, whether it utilizes DeYiWei's core technologies, whether including it in the revenue generated by core technologies is reasonable, and whether it complies with the requirements of the "Registration Management Measures" regarding "DeYiWei should primarily rely on core technologies to carry out production and operation."

From the above inquiries, it can be seen that DeYiWei boasts that its six core technologies have reached an "internationally leading" level. The regulator primarily inquired about DeYiWei's technological sources and technological advancement from perspectives such as market share, technological iteration, technological and personnel reserves, and IP licensing.

According to the second-round inquiry response, (1) DeYiWei's products are mainly consumer-grade storage control chips and memory products, with a small amount of industrial-grade/automotive-grade memory products generating revenue in 2022, accounting for 2.84%. In the most recent year, the gross margin of DeYiWei's storage control chips and memory products was overall about 20% lower than that of peer companies, due to both price and cost factors;

(2) DeYiWei's business primarily revolves around storage control chips and has expanded into memory products based on storage control chips and self-developed firmware. The response did not fully explain the specific manifestations of the technological advancement of storage control chips. DeYiWei's mainstream memory products have lower storage capacity than those of peer companies such as Jiangbolong and Hualan Microelectronics. During the reporting period, it purchased chip design services worth 14.164 million yuan from Beijing Tenafly Electronics Technology Co., Ltd. for IP verification and firmware development;

(3) DeYiWei believes that there is no absolute progressive relationship in technical difficulty among solid-state drives (SATA/PCIe), embedded (eMMC/UFS), and expandable (SD/USB) products, but there are differences in technical difficulty between different protocol interface products of the former two. The technical difficulty of PCIe and UFS is higher than that of SATA and eMMC. DeYiWei's chip products are primarily SATA-based, while its memory products are primarily eMMC-based. The revenue proportion of PCIe 3.0 products is less than 1%, and PCIe 5.0 and UFS products are still in the research and development stage. The earliest launch times of these two protocol versions were 2019 and 2011, respectively, and peer company Lianyun Technology's PCIe 4.0 has already achieved mass production. Although the revenue proportion of expandable products is not high, they have a certain market recognition, with global market shares of 12.38% and 4.65% for SD and USB, respectively;

(4) DeYiWei's SATA chip products have significant market competitive advantages, with a global market share of 23.87%. However, the latest version of SATA 3.0 has been launched for over a decade, and its market share in solid-state drives has declined from 94% in 2015 to 20%, making it the smallest market size category among the various protocol interface products of the three types of storage control chips (0.94 billion units).

Based on the above, the Shanghai Stock Exchange required DeYiWei to explain: (1) the specific application scenarios of DeYiWei's consumer-grade products, whether there are significant differences in revenue proportions compared to peer companies; the protocol interface types, application scenarios, and downstream customers of industrial-grade/automotive-grade memory products, whether they use self-developed storage control chips, and whether they will be mass-produced.

(2) Whether DeYiWei's storage control chip products have comparative advantages in terms of performance, power consumption, reliability, and stability, the reasons for its mainstream memory capacity being lower than that of peer companies, whether the firmware is self-developed, the content of the chip design services purchased from Beijing Tenafly Electronics Technology Co., Ltd. and the specific situation of its use in firmware development, and the reasons and rational

-

![]()

Why Does Changan Insist on HEV Despite Higher Costs Than PHEV?

-

![]()

Harvard Professor Admits an AI Graduate Student: Works Like a Top Student, Fakes Data Like a Poor One

-

![]()

Xiaomi Auto Hits Profitability: Can the New SU7 Redefine the Brand?

-

![]()

New Energy Vehicle Newcomers, Once Struggling, Now Turning Profits

-

Supercharging VS Battery Swapping: Not a Zero-Sum Game

-

![]()

Xiaomi: From Heaven to Hell in a Plunge, What Sustains the Faith?

-

![]()

Mach 100 Chip-Powered, First Integrated with All-New L9, Li Auto Unveils Next-Gen Autonomous Driving Architecture

-

![]()

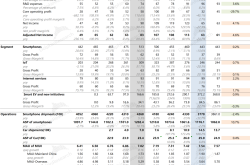

Financial Reports of NIO, XPeng, Li Auto, and Leapmotor Unveiled, All Highlighting Profitability!