Collective Rebound of Tech Stocks: Has the Market Bought It?

07/10 2026

07/10 2026

438

438

The Mid-Game Battle for AI Assets

Author|Qingyun

Editor|Xiaobai

Cover Image|AI Generated

Produced by|Qiangdiao Next

In early July, Chinese tech stocks suddenly rebounded. On July 8, the Hang Seng Tech Index surged 4.97% in a single day, with Alibaba rising over 12%, Xiaomi over 9%, Kuaishou over 8%, and Zhipu briefly surging over 19% intra-day. The market repriced "China's AI assets."

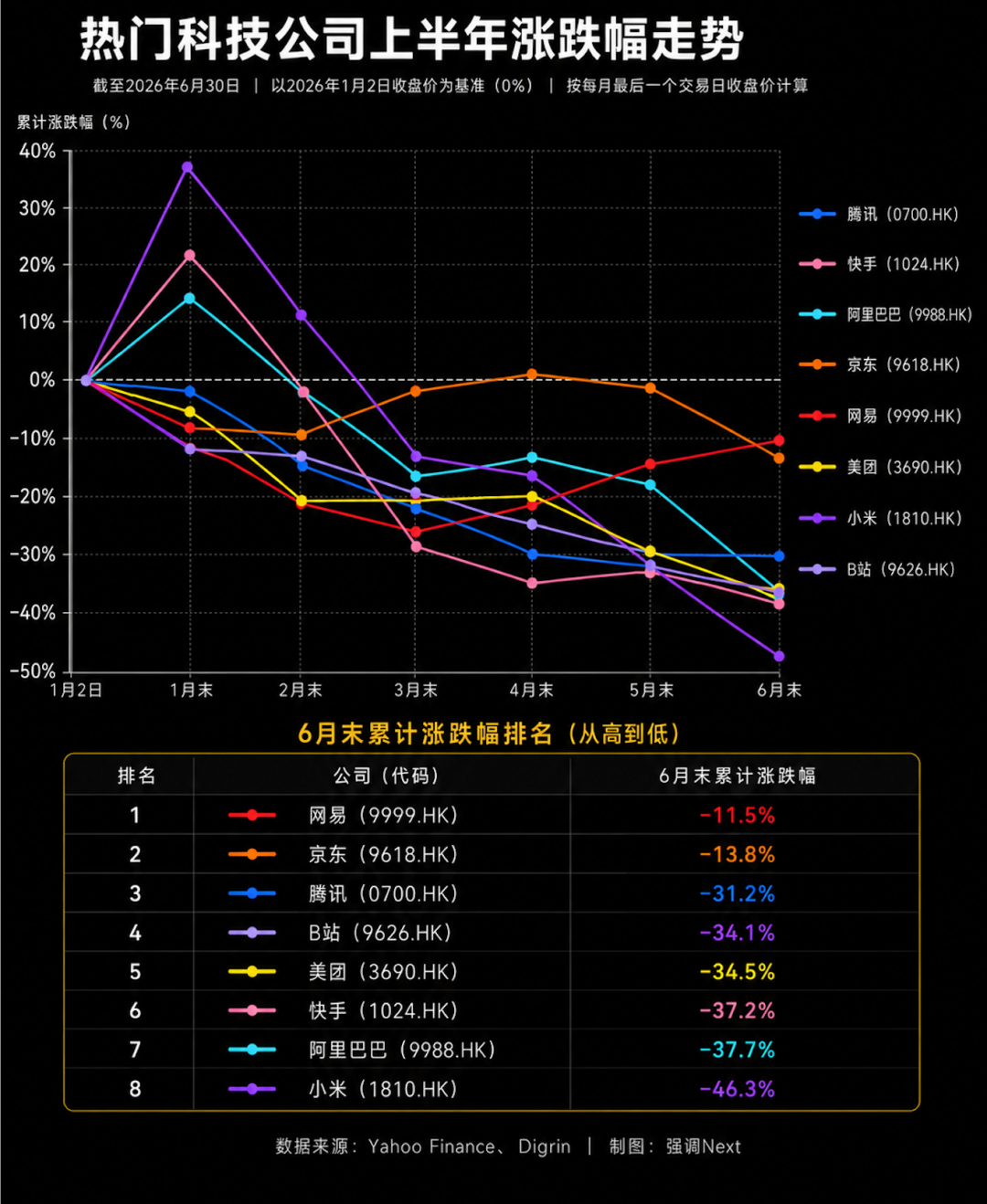

However, looking back at the first half of the year, most mainstream internet and AI-related listed companies were still below their early-year levels by the end of June. The Hang Seng Tech Index had retraced over 30% from its October peak, with the internet sector falling over 40% at one point.

This is not merely a market sentiment issue.

Over the past two years, internet companies have propped up their valuation floors through cost-cutting, efficiency gains, buybacks, and profit repairs. By the first half of 2026, new issues emerged: AI requires funding, local services resumed heavy spending, overseas expansion was no longer just a growth story, and old shareholders began reallocating capital.

The market was no longer satisfied with "companies still making money." More importantly, it questioned where capital would come from and go to in the AI era, and whether it could ultimately translate into new profits. This was a long-overdue reckoning, with issues temporarily suppressed by "cost-cutting" resurfacing over the past six months.

01. Surface: Half Ice, Half Fire

A-shares exemplify a "hard tech bull market." By June 30, the STAR 50 had surged 64.25% in six months, while the ChiNext rose 35.58%, compared to just 3.16% for the Shanghai Composite. AI hardware supply chain companies—such as semiconductor equipment, optical modules, and memory chips—saw their stock prices double or even quintuple.

The reason lies in AI computing power shortages and global capital expenditure upgrades, with orders and profits quickly reflected in financial reports. This is a classic "Davis Double Play," where earnings and valuations expand simultaneously.

Hong Kong-listed tech stocks followed an opposite trajectory. Some analysts attribute this to a global pricing logic mismatch. When global equity markets shifted to pricing "AI hardware profit realization," AI hardware accounted for just ~14.5% of the Hang Seng Tech Index, with the majority still in traditional internet, e-commerce, and new energy vehicles.

During the same period, South Korea's KOSPI surged over 100%, Japan's Nikkei 225 over 39%, and the STAR 50 over 60%, while the Hang Seng Index and Hang Seng Tech Index weakened. Hong Kong-listed internet companies were not unproductive, but global capital prioritized "visible hardware profits" over AI investments still reflected as expenses in Hong Kong, without yet converting into revenue and profits.

The July 8 rebound stemmed partly from valuation repairs and capital inflows, with June's net southbound inflows reaching ~RMB 23.588 billion, a sharp improvement from May's outflows. Another driver was loosening fundamental expectations, as Q2 data showed cloud and instant retail investments beginning to translate into revenue.

Whether this repair evolves from a rebound into a trend hinges on harder validation in August's interim results season, particularly the Hang Seng Tech core constituents' H1 earnings previews and AI capital expenditure guidance—key variables for assessing sector fundamentals.

02. Three Types of Capital Logic and Scoring Standards

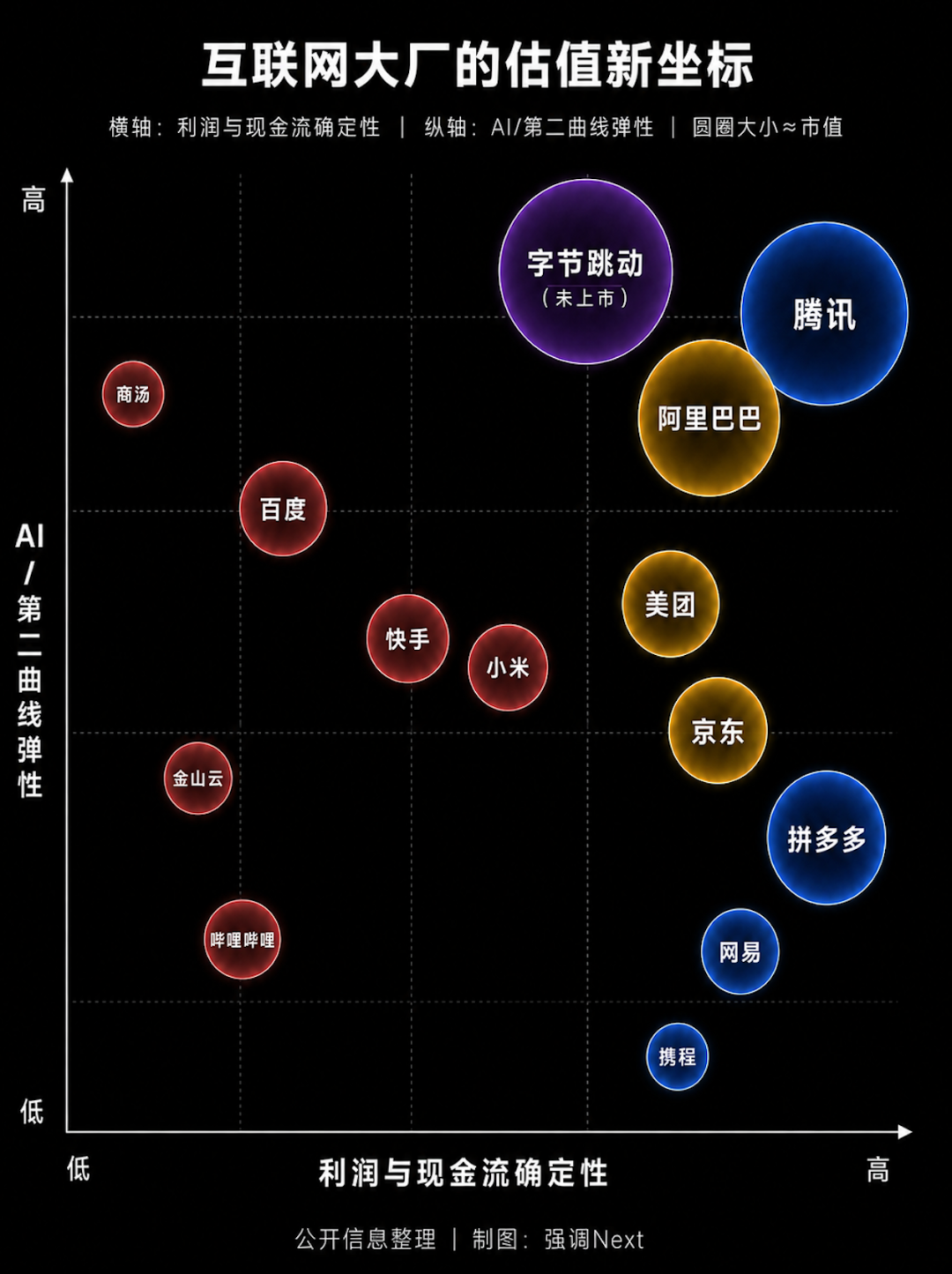

At the company level, what truly determined a firm's "performance" in H1 was not whether it belonged to "internet" or "tech," but which asset category the market placed it in.

Over the past six months, tech assets have been broadly divided into three categories with mutually exclusive valuation logics. Which logic applies to a company is itself a strategic choice.

The first category is "defensive assets," or companies with "free cash flow" profiles. However, Q1 results revealed internal divergences.

Tencent ramped up AI investments in Q1, but core business profitability remained undiluted. Excluding revenue and expenses from new AI products like Hunyuan and Yuanbao, Non-IFRS operating profit grew 17% YoY, outpacing the overall 9%. This suggests the "AI tax" currently manifests as standalone losses in new businesses without eroding Tencent's core cash flow.

NetEase reported Q1 revenue of RMB 30.6 billion (+6.1% YoY) and net profit attributable to shareholders of RMB 10.7 billion, performing steadily.

Pinduoduo, however, was substantially dragged down by the "AI tax" and strategic investments. Q1 net profit attributable to shareholders fell 15% YoY, attributed to its "RMB 100 billion support plan" and supply chain investments. Co-CEO Zhao Jiachen explicitly stated that "supply chain investment will be a core strategic focus for the next decade," with RMB 15 billion already injected in Shanghai and plans to invest RMB 100 billion over three years.

Faced with new investments, Tencent—with the thickest cash flow and rising core business gross margins—largely withstood the profit impact. Pinduoduo, in a strategic pivot phase with sunk costs in supply chain investments, saw profits genuinely suppressed. The "AI tax" is not uniformly imposed; companies with stronger cash cows and smaller pivots face milder impacts.

The second category is "turnaround assets," judged by how quickly and gracefully losses narrow. Alibaba, Meituan, and JD are prime examples. In 2025, Meituan reported a net loss of RMB 23.4 billion (vs. RMB 36.8 billion profit in 2024), JD's new business segment lost RMB 46.6 billion, and Alibaba's instant retail business lost RMB 87 billion, with the three platforms burning RMB 80-100 billion in subsidies annually. In Q1 2026, Meituan's revenue grew 5.6% YoY to RMB 91 billion, but net profit turned from RMB 10.95 billion profit to a RMB 4.97 billion loss, as takeout subsidies directly eroded profits.

Scoring standards for this category underwent two material changes in H1. First, the market no longer rewards "bold spending" but only "spending that can be recouped." Second, regulators codified boundaries into specific clauses. On June 17, China's State Administration for Market Regulation released "Ten Provisions on Subsidy Practices by Food Delivery Platforms (Draft for Comments)."

On June 29, the Beijing Municipal Market Regulation Bureau went further, convening Meituan, Taobao Flash Delivery, JD Delivery, merchants, and industry associations to establish a "Breaking the Cycle, Pursuing Good" consultation mechanism. The three parties agreed to optimize subsidies, reduce fees, and avoid "minute-level speed races."

Turnaround assets' loss-reduction pace is no longer solely company-driven; the space for extensive (undisciplined) subsidies has been systematically compressed. The instant retail battlefield will remain fierce, but the rules have shifted from capital competition to supply chain efficiency and service quality.

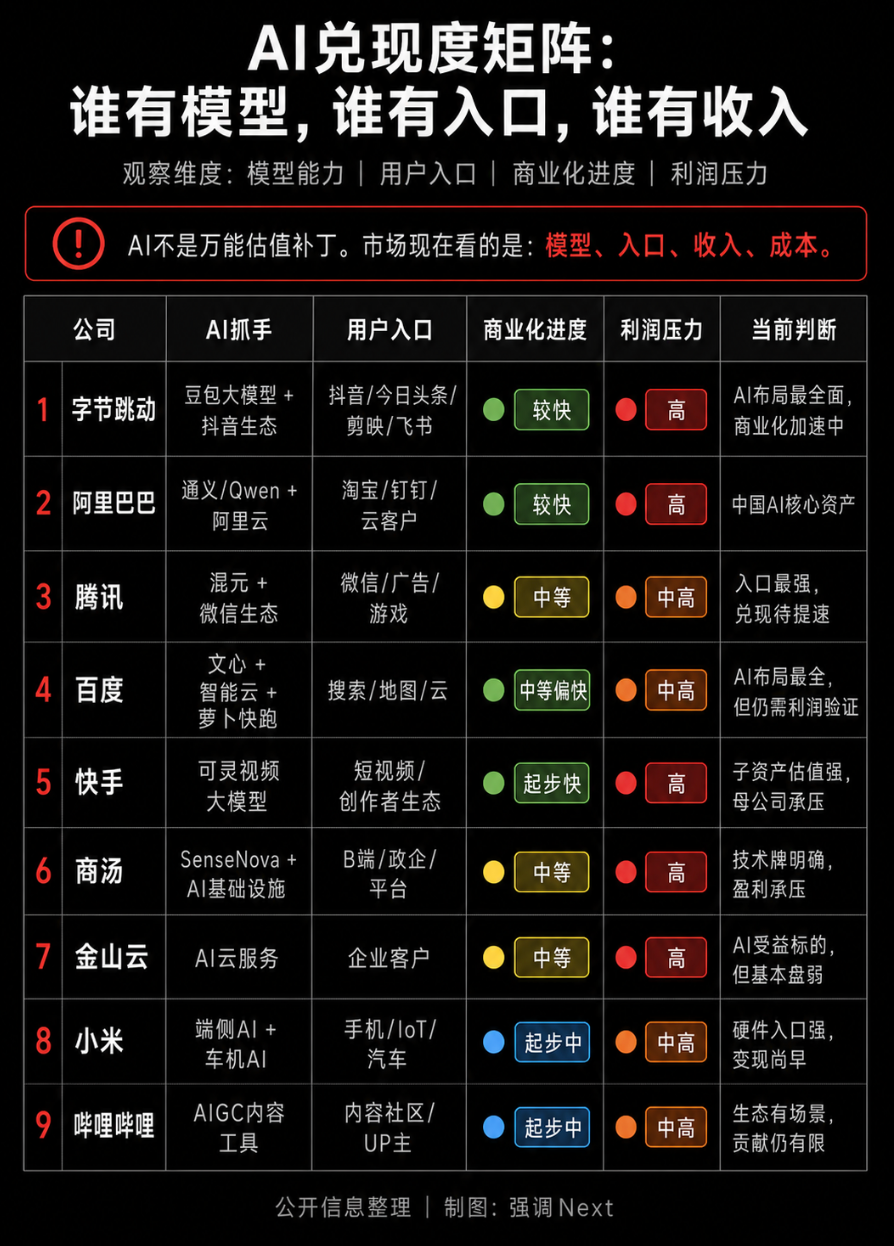

The third category is "imagination assets," corresponding to the "narrative premium" in primary markets. Kling AI, DeepSeek, Zhipu, Moonshot AI, and Kunlunxin operate in this realm, with valuations tied not to current income statements but to future potential in defining entry points, models, or platform rules.

Typically, within the same company, the parent's cash flow business is discounted as a defensive asset, while its AI subsidiaries are priced as imagination assets. Kuaishou's Kling and Baidu's Kunlunxin exemplify this dynamic.

A player that doesn't face scrutiny but dictates exam difficulty is ByteDance. Unlisted and unconstrained by secondary market logics, ByteDance is a hidden variable across all three asset classes.

As an imagination asset, ByteDance leads Chinese tech firms in AI investment aggressiveness, with its 2026 capital expenditure plan raised to ~RMB 200 billion, including ~RMB 85 billion for AI chips—roughly 60% of its 2025 profit. Its Doubao large model boasts 345 million MAUs, surpassing Qianwen and DeepSeek combined, directly prompting Tencent Yuanbao and Alibaba Qianwen to spend heavily on user acquisition.

As a benchmark for defensive assets, ByteDance's 2025 revenue ranked among global internet giants, but due to steep AI infrastructure investments, its 2025 net profit reportedly plunged over 70% YoY (though Bloomberg estimated full-year profit still approached USD 50 billion; ByteDance neither confirmed nor denied either figure, highlighting opacity in its financials).

As a counterpoint to turnaround assets, Douyin E-commerce's 2025 GMV exceeded RMB 4 trillion with >30% YoY growth, quietly reshaping local consumer traffic allocation alongside instant retail and food delivery.

ByteDance's uniqueness lies in its valuation being entirely determined by primary market secondary transactions. An early investor's secondary share transfer quote this year briefly pushed its valuation to USD 550-600 billion—a figure requiring no earnings call validation and immune to immediate repricing from quarterly profit declines.

These three asset classes are not independent scorecards but mutually undermine and support each other. Unexciting cash flows require narratives to sustain valuations, while flawed narratives need cash flows to underpin trust.

All three compete for the same incremental capital. When imagination assets attract new money, defensive assets' old shareholders must reprove holding value—explaining H1 moves like Tencent reducing Kuaishou stakes to increase Kling holdings.

03. Companies Caught in the Middle

Xiaomi and Bilibili exemplify the most awkward samples this half-year, straddling the scoring standards of all three asset classes. Xiaomi's smartphone × AIoT core business faced revenue and profit pressure in Q1, suffering cost impacts as a defensive asset. Meanwhile, its automotive and AI innovation businesses saw revenue growth but still incurred RMB 3.1 billion in operating losses, remaining pure cash burners as imagination assets—unable to stand firmly on either leg.

Bilibili fared differently, with Q1 adjusted net profit up 62% YoY and gross margin improving for 15 consecutive quarters, delivering a solid turnaround performance. However, declining gaming revenue and a weak AI narrative proved it could generate profits but not yet justify revaluation.

Such middle-ground companies are the hardest to price simply and the most worth observing in H2. Their struggles reflect that single labels no longer suffice to describe today's Chinese internet firms.

This is the true implication of internet valuations in H1 2026: there is no longer a unified exam.

The July 8 rebound essentially pre-rehearsed August's interim results exam. Low valuations, capital rotation, and signs of loosening fundamentals encouraged the market to take a stance.

But a stance ≠ an answer. What truly determines H2 rankings is who can first convert expenses into revenue. This "delayed reckoning" will unfold in August.

· Data Sources: Financial data primarily from companies' Q1 2026 and FY 2025 earnings reports, HKEX announcements, regulatory filings, and public market reports. Stock and index data as of July 8, 2026.

· Disclaimer: This article represents the author's personal views only and does not constitute investment advice.

- END -

-

![]()

Li Bin Claims, 'Denying the Pure EV Trend is Like Ostrichism.' What's Li Xiang's Take?

-

Lenovo: Liu Jun Turns Left, Yang Yuanqing Turns Right

-

Lenovo: Liu Jun Goes Left, Yang Yuanqing Goes Right

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech