Lei Jun and Wang Sicong invested in ShanSong's IPO, with giants circling for three years leading to a 6 billion yuan valuation decline

09/30 2024

09/30 2024

592

592

Produced by Radar Finance, written by Xiao Sa, edited by Shen Hai

BingEx Limited (BingEx), which focuses on the one-to-one service model, recently submitted an F-1 filing to the SEC, initiating its IPO process.

According to the prospectus, ShanSong began commercial operations in 2014. Its founder, Xue Peng, is a returned overseas Chinese entrepreneur who focused on "C-end customers who are sensitive to delivery quality and timeliness" from the beginning. By the end of June 2024, ShanSong had approximately 2.7 million registered riders covering 295 cities in China.

In the early stages of ShanSong's development, the company underwent intensive financing rounds, attracting investments from renowned institutions such as Matrix Partners China, CDH Investments, and Shunwei Capital, affiliated with Lei Jun. Wang Sicong's Pusi Capital also participated in two investment rounds in ShanSong in 2017. However, the company's last financing news dates back to March 2021, when its valuation was approximately 13 billion yuan. By 2024, ShanSong's valuation on Hurun Global Unicorn Index had shrunk to just 7.1 billion yuan.

In terms of financial performance, ShanSong recorded net losses of 291 million yuan and 180 million yuan in 2021 and 2022, respectively, before turning a profit in 2023 with a net profit of 110 million yuan. However, last year's profit was primarily driven by increased government subsidies, with operating profits related to business operations amounting to just 11 million yuan for the entire year.

It is worth noting that the industry views ShanSong's "one-to-one dedicated delivery service" as disadvantaged in terms of traffic and user stickiness. As giants in express delivery, e-commerce, and food delivery accelerate market capture, even players like Gaode and Didi have set their sights on this sector, leading to an increasing number of competitors for ShanSong and growing pressure.

Valuation nearly halved from its peak

According to the prospectus, Xue Peng holds a Bachelor's degree in Information and Computer Science from North China University of Science and Technology, a Master's degree in Business Information Systems from Royal Holloway, University of London, an EMBA in Finance from Tsinghua University, and a DBA from Cheung Kong Graduate School of Business.

Prior to founding ShanSong, Xue Peng established Beijing Caichuang Information Technology Co., Ltd. in 2008, which developed the integrated express logistics service platform E-mail Express.

Yu Hongjian, ShanSong's co-founder, previously served as Project Director of E-mail Express, Project Manager at Wensihaihui, and Senior Software Engineer at American Systems Technology Corporation.

In the booming year of 2013 for the sharing economy, Xue Peng embarked on ShanSong's entrepreneurial journey with precise product concepts and operational strategies, officially launching the app in July of the following year.

From its inception, ShanSong demonstrated robust growth momentum, securing millions of yuan in seed funding led by Matrix Partners China in its first year. According to Tianyancha, from 2015 onwards, ShanSong's domestic operating entity, Beijing Tongcheng Bingying Technology Co., Ltd., embarked on rapid financing rounds. In the B-round and B+-round financings that year, investors included Jiuding Investment, Guangyuan Growth Fund, and Tiantu Capital.

In 2015, amidst huge subsidies from companies like Meituan and Ele.me, the food delivery business grew rapidly. However, ShanSong refrained from joining the food delivery competition and adhered to its non-pooling delivery model, serving only one customer per order.

In an early interview, Yu Hongjian stated that ShanSong had achieved a compound annual growth rate of 300% for five consecutive years since its inception, attracting investors who valued this growth.

Subsequently, in 2016 and 2018, the company successfully raised funds in six consecutive financing rounds, with Wang Sicong's Pusi Capital participating in the C-round and C+-round, and Hualian Group and Shunwei Capital, affiliated with Lei Jun, leading the C+-round.

Afterward, ShanSong halted its financing efforts and began preparations for its IPO. In 2020, Du Shangbiao, the company's Vice President, told the media that ShanSong might soon go public.

However, Dada Group beat ShanSong to the punch by successfully listing on NASDAQ as the "first stock in instant delivery." Subsequently, SF Express' same-city delivery business also listed on the Hong Kong Stock Exchange at the end of 2021.

ShanSong's most recent financing round was its D2 round completed in 2021. The prospectus indicates that ShanSong raised 748 million yuan from the D-2 round in March, April, and May 2021.

After this financing round, ShanSong's post-investment valuation reached $2 billion, equivalent to approximately 12.903 billion yuan. However, this marked the company's peak valuation, which began to decline in 2022.

According to Hurun Global Unicorn Index, ShanSong's valuation was approximately 10 billion yuan in 2022 and declined by 31% year-on-year to 6.9 billion yuan in 2023. In 2024, ShanSong's valuation slightly rebounded to 7.1 billion yuan but remained far below the 2021 level.

As the company targets the U.S. stock market, its valuation may undergo a new pricing process. In terms of shareholders, before the IPO, SIG Asia Investments held a 9.7% stake, making it the largest external shareholder. CDH Investments and Shunwei Capital held 8.9% and 7.8% stakes, respectively, with the three parties collectively holding 3.2%, 2.9%, and 2.6% of voting rights.

Additionally, the prospectus reveals that Xue Peng, as the founder, directly holds a 22.7% stake in ShanSong. Furthermore, Xue Peng and his family hold an additional 20.7% stake through Snoweagle-s Limited Trust, making them the largest shareholder.

Last year's profit turnaround primarily due to government subsidies

Instant city delivery, a logistics model emerging alongside O2O, offers delivery within approximately one hour, catering primarily to urgent documents, cakes, flowers, and near-field e-commerce needs.

According to iResearch Consulting, China's on-demand delivery market grew from 164.1 billion yuan in 2019 to 338.5 billion yuan in 2023, with a compound annual growth rate of 19.8%. It is projected to grow at a CAGR of 19.1% to 809.6 billion yuan by 2028, making on-demand delivery one of China's fastest-growing industries.

The prospectus also sheds light on ShanSong's current development status. As of June 30, 2024, the company had approximately 2.7 million registered riders, serving 295 cities across China. According to iResearch Consulting, in 2023, ShanSong held approximately 33.9% of the domestic market share for independent on-demand dedicated express services.

ShanSong's order volume has steadily increased in recent years. From 2021 to June 30, 2024, the platform fulfilled 159 million, 213 million, 271 million, and 138 million orders for individual and business customers, respectively. During the same period, local delivery orders were completed in an average of 35, 31, 29, and 27 minutes, respectively.

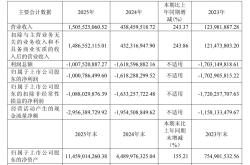

In terms of revenue, ShanSong generated 3.04 billion yuan, 4.003 billion yuan, and 4.529 billion yuan in revenue over the past three years, with year-over-year growth rates of 31.68% and 13.14% in 2022 and 2023, respectively. In the first half of this year, ShanSong's revenue reached 2.285 billion yuan, with year-over-year growth declining to 7.65%.

Moreover, ShanSong's net profits for 2021-2023 and the six months ended June 30, 2024 were -291 million yuan, -180 million yuan, 110 million yuan, and 124 million yuan, respectively.

The company achieved profitability for the first time in 2023, primarily due to increased government subsidies, which boosted other income from 9.2 million yuan in 2022 to 743.2 million yuan. However, operating profits related to business operations amounted to just 11 million yuan.

Achieving profitability for ShanSong has been challenging, directly linked to its high fulfillment costs. The prospectus reveals that during the reporting period, the percentage of compensation and incentives paid to riders as a proportion of revenue was 90.5%, 90.3%, 87.8%, 87.9%, and 85.4%, respectively.

Under ShanSong's "one-to-one" business model, a single rider is responsible for the entire service process, from picking up the item from the sender to delivering it to the recipient. Each rider can only accept one order at a time and cannot take on additional orders until the current one is completed.

This model offers higher delivery efficiency and a superior customer experience but also translates into higher delivery costs. Based on annual revenue and order volume, ShanSong's average revenue per order was approximately 19.1 yuan, 18.8 yuan, 16.7 yuan, and 16.6 yuan for 2021-2023 and the six months ended June 30, 2024, respectively.

Rising fulfillment costs and declining average order values pose challenges to ShanSong's business model. For instance, in the first half of 2024, while ShanSong maintained profitability with a net profit of 124 million yuan on 138 million orders, the average net profit per order was less than 0.9 yuan.

According to industry commentator Zhang Shule, it is difficult to reduce high labor costs in the labor-intensive express logistics sector solely through simple digital management and flattened channels. As a new sector, same-city delivery requires even higher labor intensity and frequency, making it more challenging to address with traditional management approaches.

The optimal solution, he believes, lies in leveraging artificial intelligence, big data, and driverless vehicles to optimize human resources, maximizing efficiency with minimal human intervention. Such devices as driverless vehicles could also enable more scenarios. However, these solutions are still largely speculative at present.

Intense competition amidst industry giants

In the instant delivery industry, two distinct delivery models coexist: the B-end-focused pooling delivery model and the C-end-focused one-to-one urgent delivery model, represented by companies like ShanSong, UU Running Legs, Dada, and SF Express' same-city delivery.

According to iResearch Consulting, the independent on-demand dedicated express market, where ShanSong operates, is projected to grow from 15.6 billion yuan in 2023 to 53.2 billion yuan in 2028, with a CAGR of 27.8%.

Within this niche market, ShanSong is China's largest independent on-demand dedicated express service provider, holding approximately 33.9% of the market share in 2023 based on revenue.

However, the small yet attractive pie that ShanSong commands is being nibbled away by giants. On one hand, ShanSong's existing competitors are increasing their investments. In May this year, JD.com announced the full integration of its JD Express and JD Daojia services, launching "JD Instant Delivery" with further enhanced delivery speed. SF Express' same-city delivery, similarly backed by a major platform, offers not only dedicated express services but also order allocation, merchant advertising, and other customer acquisition channels.

On the other hand, multiple forces have entered the instant delivery sector. Besides established players like couriers, e-commerce giants, and food delivery behemoths like Cainiao and Meituan, newcomers like Didi, Huolala, and Gaode Maps have also set their sights on this market.

For users, the concept of "independent on-demand dedicated express" may be unclear, and they may opt for instant document delivery through services like Fengniao Delivery, Meituan Running Legs, or any accessible same-city delivery option when in need.

These moves by giants underscore the increasingly blurred boundaries of the instant delivery market and the growing trend of cross-border expansion. For ShanSong, it must not only contend with rivals like Dada and SF Express' same-city delivery but also face challenges from cross-border players like JD.com, Meituan, and Cainiao.

Zhao Xiaomin, an express industry expert, believes that after addressing its IPO, ShanSong will face significant changes. Beyond competing within the "one-to-one" dedicated delivery system, ShanSong must also navigate the instant delivery competition landscape dominated by Meituan and Ele.me. As an independent third party, ShanSong must choose between steady development and a more aggressive strategy, adjusting its strategy accordingly.

-

![]()

Chen Hang Initiates 'Integration of DingTalk and Wukong': DingTalk Once Again Takes a Backseat

-

![]()

Five Emerging Golden Entrepreneurial Pathways in the Agent Ecosystem: A Deep Dive into the Report (Part 2)

-

![]()

GEM-TIPS Makes Its Debut at Shenzhen International AI Expo: “Octopus AI Brain” + Intelligent Agent Cluster Pave New Ways for Industrial Intelligence

-

![]()

'China's Pioneer Domestic GPU Stock' Moore Threads Posts Profit in Q1, Yet True Profitability Unverified

-

![]()

Hynix Employees Await 3 Million Won in Bonuses, Samsung Employees Go on Strike: A Dramatic Clash Between Korea's Memory Giants

-

![]()

Twelve Years On, Can Cheng Yixiao Steer Kling to Another Victory?

-

![]()

From Data Scarcity to Open Source Boom: How China's Embodied AI Data Industry Can Break Through

-

Trend丨Indium Phosphide (InP) Prices Soar Amid AI Boom, with Cycles and Disruptions Set to Continue