Miniso wants to save Yonghui, but it may have to acquire Pang Donglai first

10/10 2024

10/10 2024

669

669

Pang Donglai, regarded as the "savior" of supermarket retail, has decided to quit.

Recently, a video circulated online in which Pang Donglai's chairman Yu Donglai stated, "By the end of October at the latest, or as early as the end of September if we hurry, we will withdraw our teams and adjust our business strategy. We will not deploy any more teams." Later, Yu Donglai responded on his social media account that for the enterprises they have already assisted, most of them will be able to adjust and improve on their own during this period. However, he also confirmed that Pang Donglai will no longer send professional teams to assist new enterprises.

Pang Donglai's sudden move has led outsiders to inevitably draw connections with another recent event. On the evening of September 23, Yonghui Supermarket and Miniso announced on the Shanghai Stock Exchange and Hong Kong Stock Exchange, respectively, that Miniso would acquire a 29.4% stake in Yonghui Supermarket for 6.27 billion yuan. Upon completion of the acquisition, Miniso will become Yonghui Supermarket's largest shareholder.

Earlier this year, Yonghui Supermarket sought guidance from Pang Donglai and embarked on a major renovation of its stores. Ye Guofu, the founder of Miniso, traveled to Zhengzhou, Henan Province, to inspect Pang Donglai's model and was impressed by Yonghui Supermarket's renovated stores. The two parties immediately hit it off. While the acquisition seemed like a natural progression, Pang Donglai appeared to be acting as a mere facilitator.

Now that Yu Donglai has decided not to send assistance teams, can Miniso transform Yonghui Supermarket into another "Pang Donglai"?

Renovation cannot change the fate of abandonment

Thanks to Pang Donglai, Yonghui Supermarket has experienced a significant boost this year.

On June 19, Yonghui Supermarket's renovated Zhengzhou Xinwan Plaza store officially opened, attracting long queues outside and bustling crowds inside. Sales on the first day reached 1.88 million yuan, nearly 14 times the average daily sales before the renovation, with nearly 13,000 visitors, 5.3 times the average daily traffic before the renovation. The second renovated store, Zhengzhou Hanhai Haishang, located just 2 kilometers away from Xinwan Plaza, opened on August 7. As of August 22, daily sales had reached 1.08 million yuan, 8.2 times the average daily sales before the renovation, with traffic increasing by nearly 10 times.

The short-term results of Yonghui Supermarket's renovation have far exceeded expectations, but the sudden "change of ownership" has introduced more uncertainties into the renovation process.

Many people feel aggrieved for Pang Donglai, as Yonghui Supermarket used the renovation as an opportunity to boost its share price and sell at a good price in the capital market. Pang Donglai, feeling betrayed by its peer after "working hard to help," decided in anger to withdraw its assistance. However, this is not entirely Yonghui Supermarket's fault. In this transaction, Yonghui Supermarket may not have had much choice, and its shareholders had long since lost patience with it.

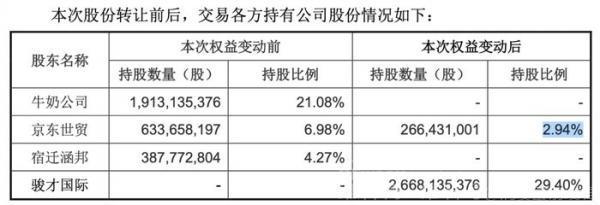

There are three sellers of Yonghui Supermarket's equity: China Dairy Corporation, JD.com World Trade, and Suqian Hanbang. Before the sale, China Dairy Corporation held a 21.08% stake in Yonghui Supermarket, while JD.com World Trade and Suqian Hanbang, as concerted action persons both under JD.com, held 6.98% and 4.27% stakes, respectively, totaling 11.25%.

When Yonghui Supermarket announced its private placement plan in August 2014, China Dairy Corporation entered at a price of 7 yuan per share, subscribing to a 19.99% stake in Yonghui Supermarket for a total investment of 5.692 billion yuan. In 2016, China Dairy Corporation invested another 1.27 billion yuan in Yonghui Supermarket's private placement, bringing its total investment to 6.962 billion yuan. However, based on the current transaction price of 6.27 billion yuan, the share transfer price is 2.35 yuan per share, allowing China Dairy Corporation to recoup only 4.496 billion yuan from its liquidation.

Long-term investment in Yonghui Supermarket has not only failed to generate significant returns for its major shareholders but has also failed to leverage its strategic value in the new retail landscape. As a result, Yonghui Supermarket has become a burden that milk companies and JD.com are eager to shed.

Even the success of the renovated stores does not seem to have changed the minds of these major shareholders about selling Yonghui Supermarket.

On the one hand, under the current economic situation, giants are halting expansion and streamlining their business lines to focus on their core competencies. Companies like Yonghui Supermarket, with poor performance, have naturally become the "castaways" of capital. On the other hand, while the renovation has stimulated the market in the short term, it is not enough to restore the confidence of major shareholders.

For Yonghui Supermarket, it remains to be seen whether customer traffic will continue to remain high. Moreover, as more stores undergo renovation, the herd effect will only diminish.

Consumers do not need a replica of "Pang Donglai"

Relying on Pang Donglai's customer traffic, most of the renovated supermarket stores have experienced a surge in customer visits. However, can the transfer of Pang Donglai's model truly help enterprises like Yonghui Supermarket return to growth?

Theoretically, traditional supermarkets have generally faced operational difficulties in recent years, with little innovation in products, services, marketing, and distribution channels. Pang Donglai has provided a highly successful model for traditional supermarkets by upgrading its products and services, attracting a large number of consumers and earning their loyalty.

However, achieving the same level of unique core advantages in products and services as Pang Donglai, whether for Yonghui Supermarket or others, is difficult.

From the renovated stores, it is evident that Yonghui Supermarket's learning from Pang Donglai is currently limited to imitation.

On the surface, the store's regional renovations, expansion, and product displays are extremely similar to Pang Donglai's. The new products on the shelves, such as large mooncakes, sweet sausages, bucketfuls of oats, beef jerky, DL juice, and DL craft wheat beer, are mostly Pang Donglai's popular items. Additionally, many products come with educational and usage introductions. The abundance of "Pang Donglai" elements gives consumers a strong sense of the Pang Donglai experience, and many customers have also noticed improvements in service.

However, removing some old products and introducing new ones does not constitute a true optimization of the product structure. The fundamental basis for Pang Donglai's product structure adjustment and optimization lies in its private-label products. The research, development, and sales control of these products have led to improved product differentiation and competitive advantages. In contrast, Yonghui Supermarket has struggled to address its shortcomings in private-label product development and innovation.

Earlier, Yonghui Supermarket experimented with a warehouse club model, purportedly learning from Costco and Sam's Club. However, the warehouse clubs still relied on the same suppliers and products, with only a handful of private-label items. Similar issues persist in the renovated stores. One customer commented, "I went to Yonghui Supermarket's Zhongmao store specifically for Pang Donglai's private-label beer, but it was out of stock. The replacement seemed to be Yonghui's own German-style beer, but the packaging didn't interest me at all."

While introducing Pang Donglai's popular private-label products has attracted a large number of customers to Yonghui Supermarket, when these popular items are out of stock, Yonghui's own sourcing or private-label products should ideally serve as substitutes. However, Yonghui's quality control has clearly fallen short of customer expectations.

Beyond products, service is crucial. Service is the "soul" of Pang Donglai, and Yonghui Supermarket has long been criticized for its subpar service. Many customers have expressed dissatisfaction with their shopping experience, citing staff gathered in clusters chatting, ignoring customers, being rude when customers decline recommended products, and refusing to provide extra bags. Yonghui Supermarket has attempted to learn from Pang Donglai in terms of service standards, management methods, and incentive mechanisms, achieving a refreshed look in a short period.

However, these aspects, which can be directly borrowed from Pang Donglai, ultimately depend on the "people" involved. Yonghui Supermarket's offerings to its employees are far from sufficient to consistently motivate them.

This is not because the Pang Donglai model is unreplicable. In fact, the key to its success is well-known: profit-sharing. Yu Donglai is willing to distribute the company's profits to its employees, ensuring that rigorous product selection and service standards are effectively implemented by employees, resulting in high-quality products and exceptional service.

In contrast, Yonghui Supermarket lacks a "Yu Donglai" figure and faces internal strife among its brothers. Moreover, as a nationwide chain supermarket with a vast employee base, it seems impractical for Yonghui Supermarket, whose performance is declining, to be so "generous."

Can young hearts return to traditional supermarkets?

With Yonghui Supermarket's renovation and Miniso's acquisition of a controlling stake, there is speculation that Yonghui could become the next "Pang Donglai." However, aside from Ye Guofu's lack of success in the traditional supermarket sector, Miniso's acquisition of Yonghui Supermarket is a risky "snake swallowing an elephant" move. Furthermore, transforming Yonghui based on the Pang Donglai model rather than Miniso's own model poses significant challenges for Miniso.

Therefore, rather than debating whether Miniso can turn Yonghui into the next Pang Donglai, it is more meaningful to examine whether the integration of Miniso and Yonghui Supermarket can achieve a synergy effect.

Yonghui Supermarket's strength lies in fresh produce, while its weakness is general merchandise. According to Ye Guofu's research, Yonghui Supermarket's annual sales over the past two years have ranged between 80 and 90 billion yuan, with one-quarter of these sales coming from general merchandise. However, most of these sales are generated by third-party brands, with only a single-digit percentage coming from Yonghui's private labels.

Miniso excels in general merchandise, leveraging its extensive supply chain in this category. In the future, Yonghui Supermarket may leverage Miniso's strengths to improve its general merchandise offerings and further optimize its product mix. Of course, this is not the crux of the matter. Miniso's value primarily lies in its ability to develop and promote private labels, echoing Pang Donglai's strategy of building core competencies through private-label products. Yonghui Supermarket's choice of Miniso may well be based on this recognition.

For Yonghui Supermarket, whether it can leverage Miniso to attract new customer segments, develop distinctive private-label products, and engage younger customers will determine whether traditional supermarkets can "rebirth."

However, it is essential to recognize the significant differences in customer demographics between Miniso and Yonghui Supermarket. Can Miniso truly help Yonghui Supermarket win back the hearts of young consumers?

According to public information, Miniso's primary consumer demographic comprises female students and young white-collar workers, with over 60% of its customers under the age of 30. In contrast, Yonghui Supermarket has long been distanced from younger generations. Data from Joychain Insights reveals that Yonghui Supermarket attracts shoppers who prefer browsing and selecting products, with an older age profile compared to online platforms. Morning hours are dominated by middle-aged and elderly customers, and the average transaction value ranges from 55 to 60 yuan, with better-performing stores reaching 60 to 65 yuan, indicating stronger purchasing power than wet markets and group-buying platforms.

These significant differences in customer demographics pose challenges for Miniso in assisting Yonghui Supermarket in developing private-label products. In particular, Miniso's core competency in creating viral IP content is largely ineffective among middle-aged and elderly consumers.

Furthermore, Yonghui Supermarket's imitation of Pang Donglai necessitates not just cost-effective but also high-quality private-label products. However, there are doubts about the quality of Miniso's products. As one consumer put it, "I'm not confident in Miniso's ability to create quality private-label products for Yonghui Supermarket when even Miniso's own products are questionable in terms of quality and heavily reliant on collaborations for revenue."

In 2019, Suning Commerce Group's wholly-owned subsidiary, Suning International, acquired an 80% stake in Carrefour China for 4.8 billion yuan. However, less than two years after the acquisition, Suning Commerce Group was mired in a liquidity crisis due to debt issues, leading Carrefour to sue Suning. Similarly, in 2019, Wumart Stores and Metro Group announced the establishment of a joint venture. However, since this year, multiple Metro stores in Chengdu, Shanghai, Wuhan, and other cities have announced closures for renovation.

Whether Miniso can serve as a savior for Yonghui Supermarket remains uncertain. For this vast undertaking, perhaps only the addition of another Pang Donglai stands a chance of truly reviving it – though this scenario is highly unlikely.

Consumption Frontier, formerly known as Koi Carp Finance, provides professional, unbiased, and neutral business insights. This article is original and prohibits any form of reprinting without retaining the author's information.

-

![]()

Annual Revenue Soars to 24 Billion! Large-Scale AI Models Ignite Edge AI Demand, Quectel Sets Sights on AI-Powered IoT

-

![]()

Left-Hand AIVA, Right-Hand Jiayue! Volcano Engine’s Back-to-Back Moves: Can ByteDance Replicate ‘Hongmeng Zhixing’ Success?

-

![]()

The 'Double-Edged Sword' of Roborock's Operations: Soaring Scale Amid Profit Dilemma Under Heavy Marketing Spend

-

![]()

Agent's 'Anti-Consensus' Strategy in the Second Half: SaaS Companies Carve Out a New Ecological Niche

-

![]()

AI Large Models Compete for the Business of 'Zhang Xuefengs'

-

Chinese Brands Face the 'Twilight of the Gods' and 'Battle of the Gods' at the World Cup

-

![]()

Exclusive | DingTalk's Leadership Change: Next Steps Include Integrating MuleRun

-

![]()

Exclusive | DingTalk's Leadership Change: Next Steps Include Integrating MuleRun