Lucid Motors In-Depth Research Report: An Undervalued Tech-Centric Automaker, Can It Break Through in China's Hyper-Competitive Era?

04/07 2026

04/07 2026

602

602

Faced with China's new energy vehicle market, where monthly sales often reach tens of thousands and competition is fiercely intense, Silicon Valley luxury automaker Lucid—with annual deliveries still hovering around the ten-thousand-unit mark—appears to be confronting a massive existential crisis.

However, a closer examination of the detailed disclosures from its recent 2026 Investor Day reveals an entirely different survival logic.

This article will combine Lucid's actual sales and financial status to deeply dissect its latest products, technological strengths, and business strategy. After reading, you'll understand how a deeply unprofitable 'tech geek' automaker aims to save itself in the global elimination round through extreme modularity and an asset-light model.

That said, this article exceeds ten thousand words—you'll need a bit of patience to finish it.

I. First, the Reality: Where Is Lucid Now?

Before interpreting any grand narratives, we need to confront a sobering reality: Lucid is an electric vehicle startup with annual revenue under $1.5 billion, sustaining persistent losses and relying on 'life support' from Saudi Arabia's sovereign wealth fund.

Sales Performance

Throughout 2025, Lucid delivered approximately 10,200 units (Air + Gravity combined), doubling its 2024 total, with annual production also doubling. In absolute terms, this is less than BYD's daily output. However, one data point stands out: In the $100,000+ all-electric luxury sedan segment, the Lucid Air ranked first for six consecutive quarters. From Q3 to Q4 2025, its sales grew 23% quarter-over-quarter, with market share expanding by 30%.

The ramp-up of Gravity is equally noteworthy—from Q3 to Q4, Gravity deliveries quadrupled. Notably, 80% of Gravity buyers were new to Lucid, and 28% had never owned an SUV before, indicating Gravity is effectively expanding the category's consumer base.

Financial Performance

Lucid's 'sugar daddy' is Saudi Arabia's PIF—this is its biggest distinction from fellow startups. While unlikely to collapse due to short-term funding gaps, it faces constant equity dilution pressure. Currently, Lucid loses $150,000–$200,000 per vehicle sold—a structural issue typical for startups in their ramp-up phase. The problem isn't unsellable products but insufficient fixed-cost amortization and scale not yet reaching critical mass. The entire Investor Day essentially told investors: When will the inflection point arrive, and what's the path to get there?

II. In-Depth Analysis of Existing Products: Air and Gravity

2.1 Lucid Air: Pushing Technical Boundaries in the Luxury Sedan Segment

The Lucid Air is the company's breakthrough model, ranking first for six consecutive quarters in 2025 in the $100,000+ all-electric luxury sedan segment. It even ranked third in its entire class (including internal combustion vehicles), trailing only two classic fuel-powered sedans.

Key Specifications (Grand Touring version):

Range: Over 512 miles (~824 km), a benchmark among global mass-produced electric sedans

Power Output: 819 horsepower, while maintaining best-in-class interior space

Efficiency Path: Systemic optimization of drive units, batteries, and vehicle management software—not just stacking individual subsystems

The Lucid Air Sapphire is the performance flagship, not only recognized in the U.S. but also winning Germany's 2025 Performance Car of the Year award—selected by 32 senior German automotive journalists. This is extremely rare for an American EV startup and serves as strong endorsement of its technical prowess by traditional automotive industrial core markets.

Awards: Since mass production began in 2022, the Lucid Air has made Car and Driver's Top 10 list for three consecutive years. Lucid is the only brand where all its models have made this list—though it doesn't have many models, this record's value is undeniable.

2.2 Lucid Gravity: Redefining the Full-Size Luxury Electric SUV

Gravity is Lucid's first SUV model, positioned to unify sports car-level performance with extreme range in a seven-seat full-size SUV format.

Key Specifications:

Range: 450 miles (~724 km), industry-leading among seven-seat competitors

Charging Speed: 11 minutes to replenish 200 miles of range—practical for fleets and daily users

Power: Over 800 horsepower, with 0-60 mph acceleration reaching sports car levels

NVH Control: Exceptionally quiet, with suspension tuning universally praised by industry reviewers

Market Reception: Motor Trend called it 'the pinnacle of what an electric SUV can achieve'; Esquire named it 2026 Car of the Year, stating 'this car breaks the laws of physics'—an SUV carrying seven people and luggage, with 450 miles per charge, outperforming sports cars in straight-line and cornering performance, while also excelling in parking maneuvers; TechCrunch dubbed it 'an electric SUV without compromises.'

In 2026, Gravity made Car and Driver's Top 10 list alongside the Air, making Lucid the only brand where all mass-produced models have made this list.

Competitive displacement is occurring: Among Tesla Model X owners trading in their vehicles, Lucid Gravity is their top replacement choice, selected at twice the rate of the second choice. This data becomes even more significant after Tesla announced discontinuation of the Model S and X—with about 350,000 of these vehicles currently on U.S. roads, representing a substantial pool of potential converters.

III. Mid-Size Vehicle Platform: Full Technical Breakdown

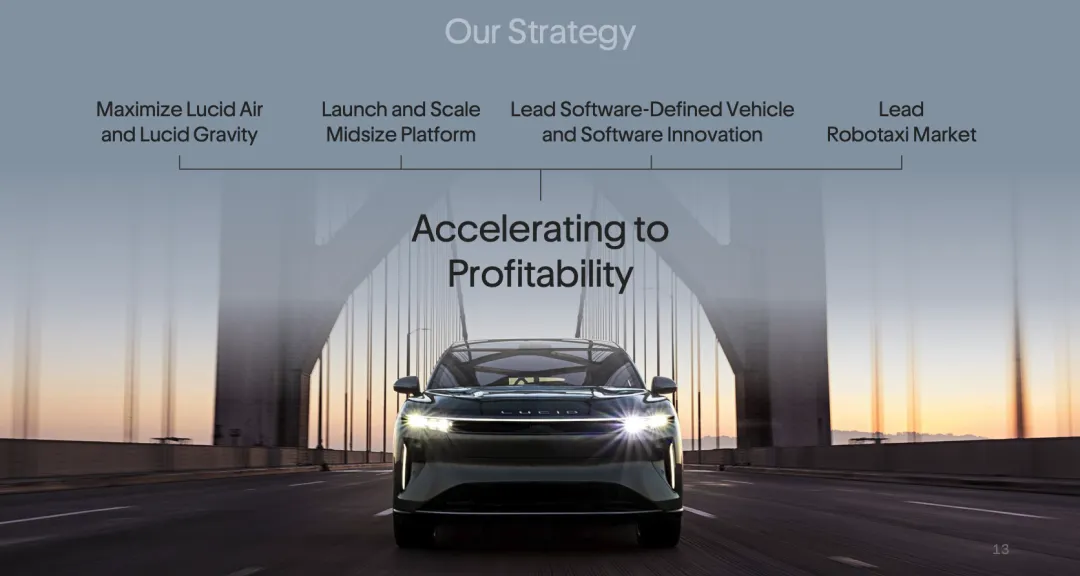

This was the core content of Investor Day and the most critical chapter for understanding Lucid's future trajectory. The mid-size platform (led by Cosmos and Earth) directly determines whether Lucid can break out of the niche luxury market and achieve scalable profitability.

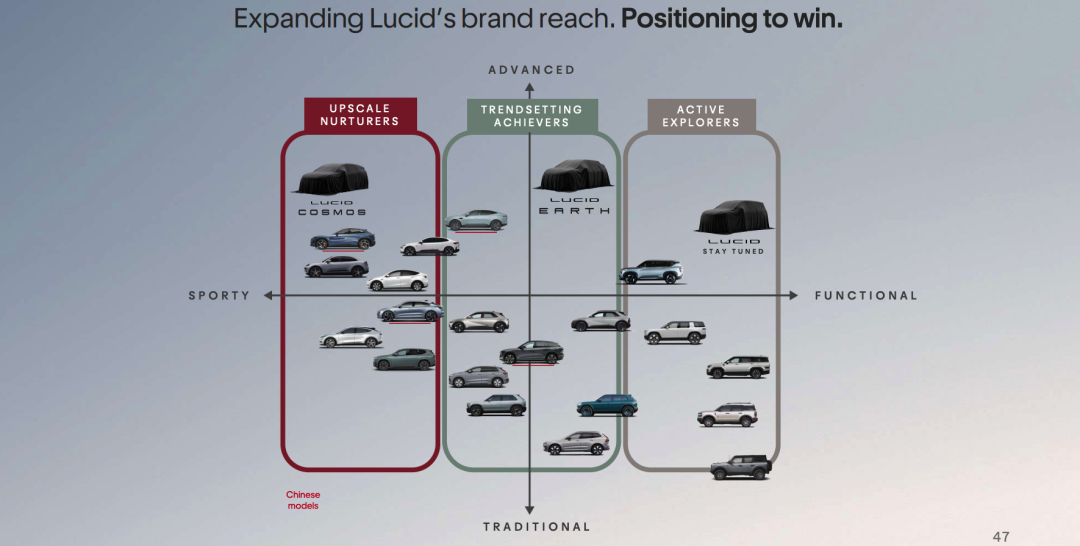

3.1 Product Matrix: Three Models, Three Customer Segments

Lucid's mid-size vehicles aren't just one or two variants but three independent products targeting different segments while sharing a common underlying platform.

Target Customer Research: Existing EV consumers represent only about 10% of the market (premium/tech-oriented), while Lucid's market research identified three previously underserved new groups representing up to 50% of potential EV market share:

"Family Tech Adapters": Focus on family needs, tech experience, and rapid adaptation to new technologies

"Urban Adventurers": Pursue personalized design, balancing urban commuting with weekend exploration

"Active Explorers": Value spatial functionality and advanced technology integration

Model Naming:

First Model: Lucid Cosmos—first to enter mass production, launching at Saudi Arabia's M2 factory in late 2026

Second Model: Lucid Earth—launching about a year after Cosmos

Third Model: Name not yet announced, to be revealed at the next Investor Day

The naming logic is clear: Air → Gravity → Cosmos → Earth, weaving elemental series with physical concepts for strong technological appeal.

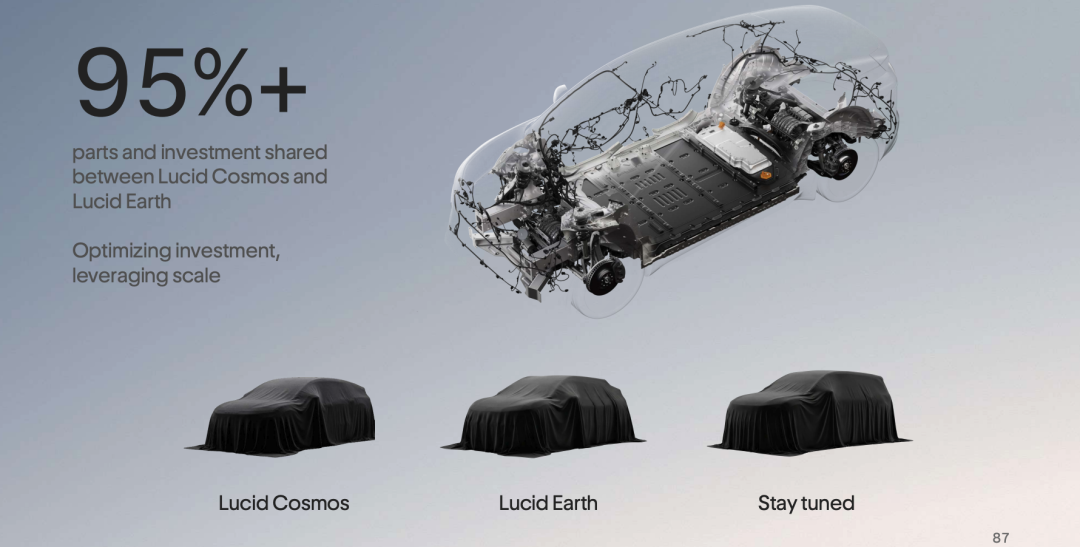

Cosmos and Earth share 95% parts commonality, especially for the largest/most expensive components (batteries, drive units) being fully interchangeable. This means Earth's BOM cost will be in the same favorable range as Cosmos while offering substantially different exterior design and functional positioning to cover distinct customer groups.

3.2 Exterior & Aerodynamics: Pushing Physical Boundaries

Lucid's mid-size vehicle design philosophy: Extremely compact and streamlined externally, with interior space surpassing all competitors in its class. This seemingly contradictory goal is achieved through extreme component miniaturization.

Key Design Parameters:

Drag Coefficient (Cd): Below 0.22—an extremely challenging target requiring precise coordination of entire vehicle airflow management. Few mass-produced vehicles achieve a Cd below 0.22, making this number essential for supporting ultra-long range goals.

Silhouette Language: Compared to Air and Gravity designs, the mid-size models adopt smoother, more dynamic, and emotionally expressive styling. Some critics describe it as 'looking like a future flying car from The Jetsons.'

Cargo Space: 24% more cargo capacity than the class average—a significant advantage in direct comparisons.

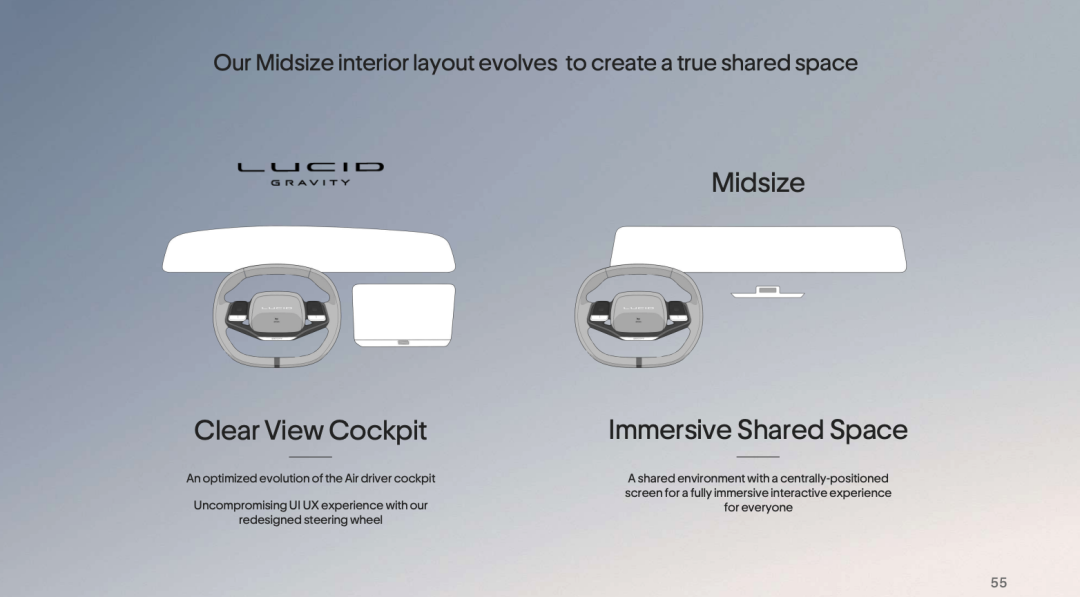

3.3 Cabin Experience: Clear View Cockpit Fully Upgraded

The mid-size models introduce a completely redesigned Clear View Cockpit cabin experience:

Hardware: A single 36-inch high-resolution curved display spans the entire dashboard, positioned directly in the driver's upper line of sight while serving both driver and front passenger. Compared to multi-screen splice solutions on the market, this single integrated display offers fundamental differences in visual continuity and system responsiveness.

Physical Controls Retained: The central area preserves physical knobs/buttons for high-frequency operations like fan speed, temperature, and volume—a conscious counter-trend to excessive touchscreen reliance. In driving scenarios, physical feedback is safer and more intuitive than virtual buttons.

Haptic Steering Wheel: Integrates haptic feedback to provide tangible sensory cues to the driver during ADAS-assisted driving scenarios.

Mechanical Physical Door Handles: Equipped both inside and out—a deliberate differentiation choice amid the current EV trend of hidden/electric handles, balancing emergency reliability with intuitive usability.

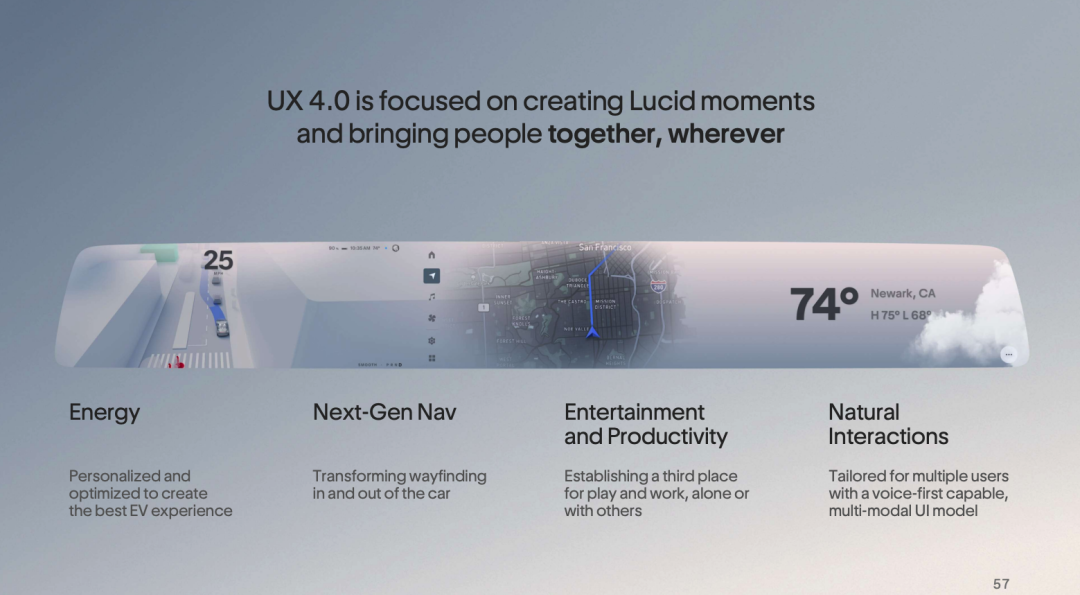

Software—UX 4.0 Four Core Modules:

Energy: Visually presents in real-time how driving style affects range through widget-style displays, helping drivers develop energy efficiency intuition.

Next-Gen Navigation: Offers 3D immersive map experiences with turn-by-turn directions overlaid on ADAS camera feeds, deeply integrating navigation with assisted driving to reduce driver Vision switching burden.

Entertainment & Productivity: Integrates mainstream streaming services and gaming functions for non-driving scenarios like parking or waiting.

Natural Interaction: Centered around Lucid Intelligence AI assistant (detailed next).

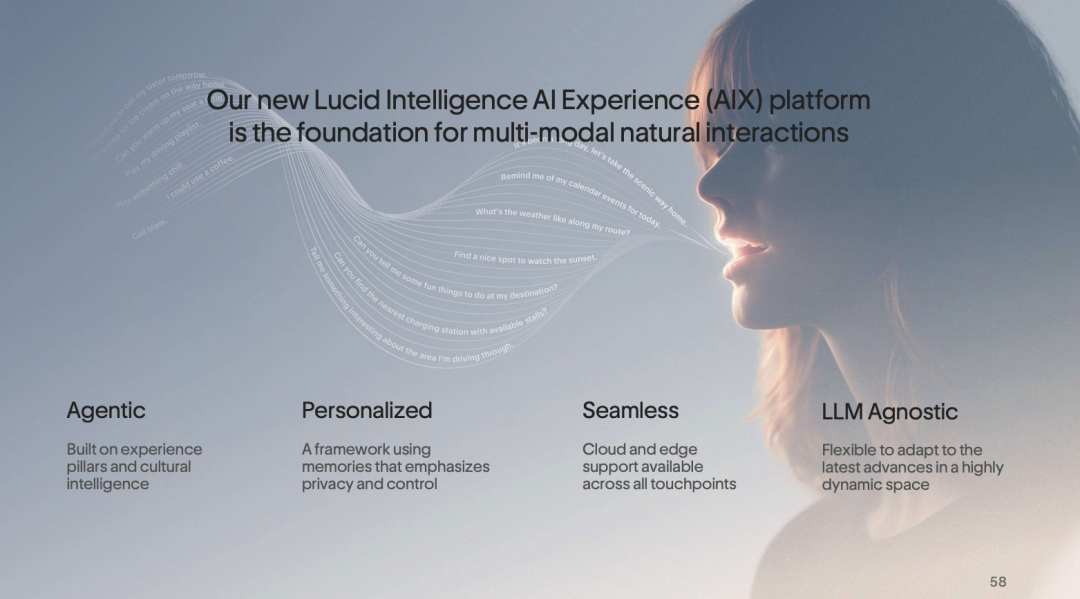

3.4 Lucid Intelligence: Generative AI Assistant

Lucid Intelligence is the core software differentiator for mid-size models, with several noteworthy technical architecture details:

Generative (Agentic) rather than Command-Based: It doesn't just execute single voice commands but understands complex natural language requests, performs multi-step reasoning, and provides personalized recommendations. During the Investor Day demo, the system in one conversation: identified the user's city (New York) → recommended maritime-themed tourist attractions → automatically planned the route → navigated to the parking lot, all without requiring multiple user inputs.

Language Model Agnostic: A crucial architectural decision. Lucid Intelligence's backend can connect to any major large language model (LLM) rather than being tied to a single model provider. This means: When GPT-5, Claude 4, or stronger future models emerge, Lucid can quickly switch underlying engines without reconstructing the entire interaction layer; it also reserves space for different compliant models in various regions (e.g., integrating localized models in certain markets).

Personalized Settings: Users can choose the AI assistant's personality style, ranging from "Easygoing & Relaxed" to "Direct & Efficient," adapting to different driving scenarios and personal preferences.

OTA Continuous Evolution: Throughout 2025, Lucid conducted 13 OTA updates, compared to the industry average of just 2. Upcoming updates include: CarPlay/Android Auto (already rolled out to Gravity), Digital Key (Summer 2026), and Hands-Free Driving in Urban Areas (Late 2026).

IV. Deep Dive into Core Technologies: Engineering Realization of Radical Efficiency

"Radical Efficiency" was the most frequently mentioned term at this Investor Day, but it is not just a slogan—it is a systematic methodology spanning design, manufacturing, and cost dimensions. Below is a detailed breakdown.

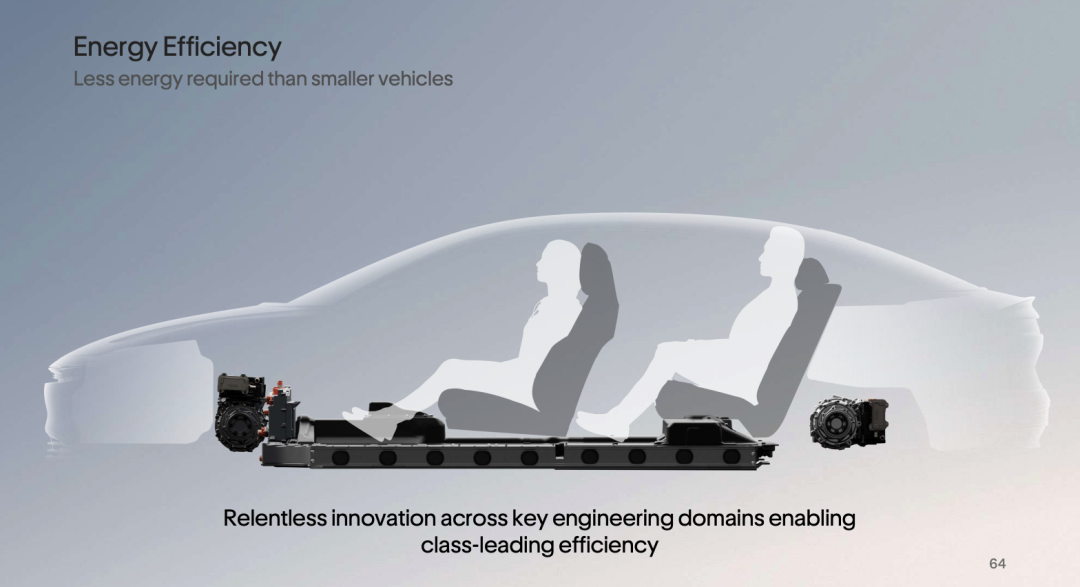

4.1 Energy Efficiency: System-Level Optimization Over Subsystem Stacking

Lucid's efficiency leadership is built on collaborative optimization of the entire powertrain, rather than Maximization (maximizing) individual components. This is the core reason competitors find it difficult to replicate quickly—most companies optimize subsystems independently before integration, whereas Lucid prioritizes efficiency as the primary design goal from the system architecture level.

Current Leading Metrics:

Lucid Air's energy efficiency (miles per kWh) is 15% higher than the best-performing mass-produced competitors, and this advantage has continued to widen over the past five years.

The mid-size Cosmos is expected to achieve over 10% additional efficiency leadership on this basis, benchmarked against the latest globally optimized platforms (including leading brands from the U.S., Germany, and China).

Speaking in concrete numbers: To travel 300 miles, Cosmos requires only 69 kWh; for the same distance, a leading U.S. EV brand requires 73 kWh, while some competitors need 82 or even 86 kWh. For consumers, this means unnecessarily paying approximately $2,000 more for a larger battery without gaining any additional driving value.

In Robotaxi operation scenarios, the mid-size vehicle achieves 4.5 miles per kWh; the dedicated Robotaxi concept car Lunar reaches 5.5-6 miles per kWh.

4.2 Atlas Drive Unit: A Leap from Zeus to Low-Cost, High-Density

The Zeus drive unit (used in Air and Gravity) is currently the highest power-density drive unit in mass-produced vehicles globally—a consensus in the industry. However, Zeus was designed under the premise of "achieving the best at any cost." Atlas, in contrast, is a complete redesign that prioritizes cost while still leading the industry in power density.

Key Improvements in the Atlas Drive Unit:

40% Higher Power Density: Compared to drive units in the same cost segment currently on the market (note: benchmarked against cost-oriented competitors, not performance products built without cost constraints), Atlas achieves a 40% improvement in power density, meaning it delivers equivalent or greater power in a smaller volume and weight.

30% Fewer Parts: Reducing parts not only lowers material costs but also decreases assembly labor, supply chain management complexity, and quality risks.

Fully Universal Front and Rear Axle Drive Units: This is a critical platform decision. Atlas uses the same base design for front and rear axle motors, achieving differentiation through adjusted control parameters. Universalization brings dual benefits: economies of scale (doubled production volume amortizes the same mold and production line costs) and supply chain simplification (single-model procurement enhances bargaining power).

37% Cost Reduction: Compared to Zeus, Atlas's manufacturing cost decreases by 37% due to the above improvements.

Fully In-House Designed and Manufactured: This means Lucid retains complete control over the drive unit's technological path without relying on external suppliers' roadmaps.

Performance (Mid-Size Vehicle): 0-60 mph acceleration: 3.5 seconds

High-Speed Overtaking Performance: Inherits Lucid's sporting DNA

Positive Contribution to Energy Efficiency (efficient motors mean less energy loss converted to heat)

4.3 Battery System: Miniaturized Integration and Factory Streamlining

The mid-size vehicle's battery system most epitomize (concentratedly embodies) the "Radical Efficiency" philosophy, involving simultaneous breakthroughs across product, manufacturing, and cost dimensions.

At the Product Architecture Level—Deep Integration: Previously, Gravity's high-voltage system consisted of multiple independent components scattered throughout the vehicle. The mid-size vehicle consolidates these into a single high-voltage system directly integrated within the battery pack. The direct benefits of this integration approach:

80% Fewer Non-Cell Parts: Non-cell components include all structural parts, electrical connectors, and BMS components outside the battery cells themselves. An 80% reduction means significantly simplified assembly processes.

45% Lower Component Costs Compared to Gravity: Even benchmarked against Gravity, already an engineering marvel, the mid-size vehicle's battery system costs are reduced by an additional 45%.

Leading Charging Performance: 14 minutes to replenish 200 miles of range (~320 km), one of the fastest charging speeds in the U.S. market.

Full Support for V2V (Vehicle-to-Vehicle), V2H (Vehicle-to-Home), and other bidirectional charging/discharging functions, reserving interfaces for future energy management scenarios.

This battery system can be pre-assembled as an independent module offline and then docked with the complete vehicle, significantly boosting final assembly efficiency.

At the Factory Level—Simultaneous Compression of Manufacturing Footprint and Costs:

40% Smaller Battery Factory Footprint with Higher Output

50% Reduction in Labor and Overhead Costs

This means the same capital investment can support greater capacity expansion.

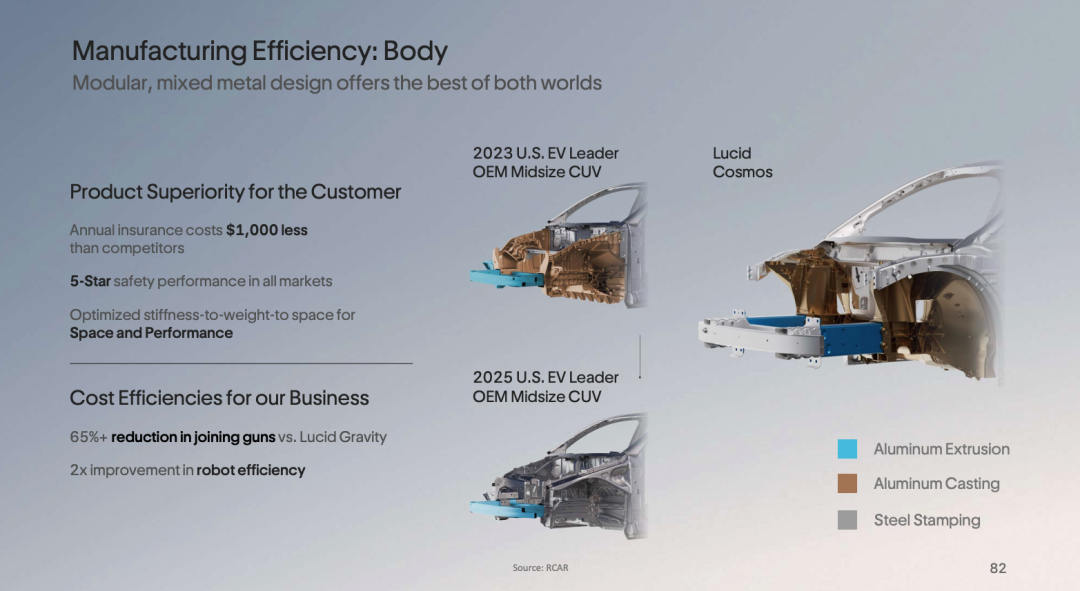

4.4 Body Structure: A Counterintuitive Choice to Abandon One-Piece Casting

Lucid made a surprising industry decision with the mid-size vehicle: not to adopt one-piece casting (Giga Casting) but to insist on a differentiated hybrid approach. Against the backdrop of Tesla heavily promoting Giga Casting and multiple OEMs following suit, this is a strategic choice worthy of in-depth analysis.

What is Lucid's Approach?

Using "Mega Castings" at High-Stress Nodes and Key Connections: These locations bear the greatest loads, and castings provide the strongest rigid support with optimal material distribution—the areas where castings deliver the most value.

Using the Most Suitable Materials (Steel or Aluminum Stampings) in Non-Critical Areas: Adapting to local conditions rather than applying one-size-fits-all casting across the entire vehicle.

Segmented Front Rail Design: The front rail is split into two independent sections—a low-speed repairable rail (absorbing common minor impacts) and a high-speed energy-absorbing rail (absorbing severe collision energy). This allows direct replacement of the repairable rail section after low-speed impacts without touching the casting itself, significantly reducing repair costs.

Why Not Giga Casting? The core pain point of Giga Casting lies in repairability. Once a minor collision deforms the casting, the entire component often requires complete replacement, with repair costs reaching tens of thousands of dollars—and most small repair shops cannot handle it. While this may be acceptable in the luxury car market, it is a clear purchasing barrier for the mid-size vehicle's target demographic (more cost-conscious daily users).

Notably, Lucid pointed out that some companies which once heavily promoted Giga Casting have quietly reverted to full-steel stampings for the front underbody—this indirectly validates Lucid's judgment.

Quantifiable Benefits: $1,000/year lower insurance premiums (~30% reduction): Based on the impact of improved repairability on insurance actuarial data, this represents real user economic benefits, not theoretical estimates.

Still achieves Five-Star Crash Ratings without compromising safety.

65% Fewer Welding Robot Clamping Guns: This directly translates to improved production throughput (JPH, Jobs Per Hour).

2x Higher Robot Operating Efficiency.

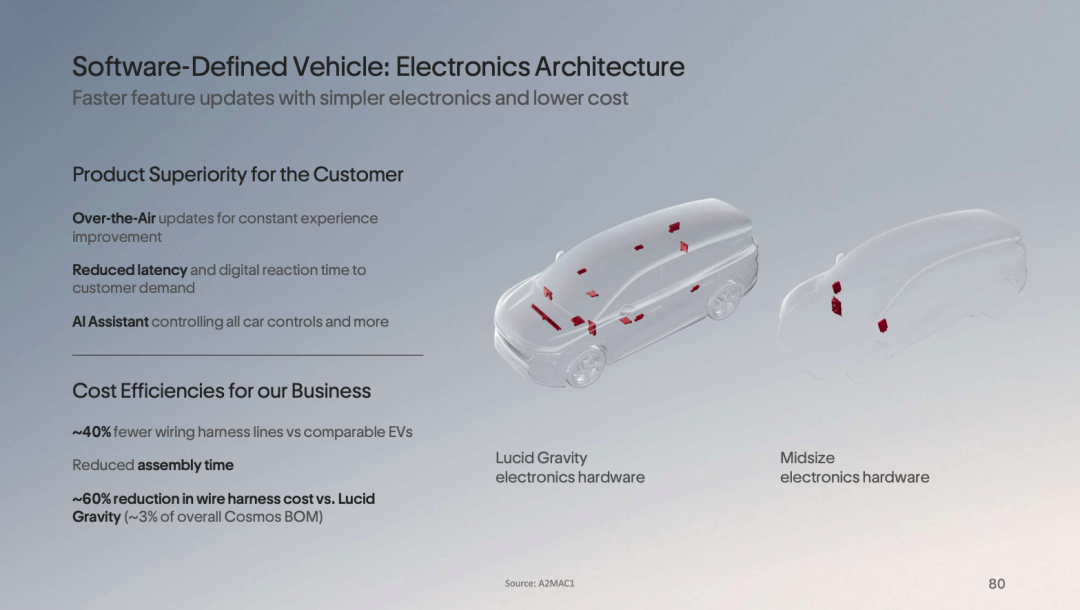

4.5 Software-Defined Vehicle: Architectural Revolution with Three ECUs

"Software-Defined Vehicle" is an industry buzzword, but Lucid gives it substantive content through a highly persuasive engineering decision: consolidating all vehicle body electronics into **three ECUs (Electronic Control Units)**.

Contrast with Traditional Distributed Architecture: Traditional vehicles often have 80-100 or even more scattered ECUs, each managing a functional domain (windows, seats, lights, door locks, etc.), communicating through complex CAN bus networks. The drawbacks of this architecture: Any OTA update for a single function requires coordinating multiple ECUs, leading to high latency, error-prone processes, and complex integration testing.

Benefits of the Three-ECU Integration Solution:

Reduced OTA Update Latency: Fewer communication hops, improved response speed, and updates can be delivered as a holistic package.

Centralized Operation of All Onboard Computing: High-computing-demand functions including AI assistant, navigation, and ADAS support run entirely on the centralized computing platform, avoiding resource fragmentation.

40% Fewer Wire Harnesses: Compared to some EV competitors, wire counts are reduced by 40%, with even greater reductions versus traditional vehicles. Every wire represents cost (materials, weight, assembly labor).

Harness Assembly Time: 4 Minutes: This figure speaks volumes. In traditional auto factories, wire harnesses are among the hardest components to assemble, often requiring specialized workers and significant time. The mid-size vehicle prototype's harness installation took only 4 minutes—the engineering team had originally prepared contingency plans for an entire day.

Virtual Components Replacing Physical Ones: Some functions that previously required independent physical ECUs now run through software virtualization on the centralized computing platform, achieving "reduced hardware without reduced functionality."

V. Autonomous Driving Strategy: Identity Shift from "Selling Cars" to "Selling Platforms"

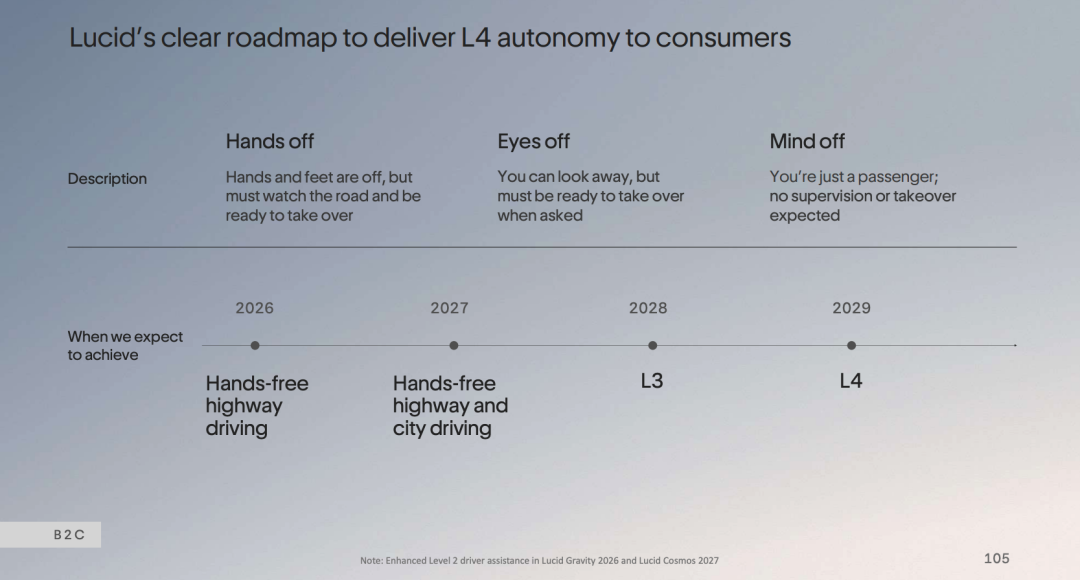

5.1 Consumer Autonomous Driving Roadmap: A Clear Four-Step Path

Lucid has designed a clear iterative path for autonomous driving capabilities for retail customers, with specific implementation timelines for each stage:

Step 1—Hands-Off Driving (Already Achieved):

Lucid Air already features hands-free highway driving (Dream Drive Pro)

Q2 2026: Equivalent functionality introduced to Lucid Gravity

Current Adoption Rates: 40% for Air, 65% for Gravity—far exceeding the industry average of 25%

Step 2—Urban Scenario Expansion (2026-2027):

Late 2026: Gravity achieves hands-free driving in urban areas

2027: Both Gravity and Cosmos support hands-free driving on highways + urban roads

Step 3—L3 Eyes-Off Driving (2028): First introduction of L3-level functionality on Lucid's mid-size vehicle platform

This stage requires a completely new ADAS hardware platform: upgraded high-performance computing unit + additional sensor suite (current Air and Gravity hardware can support up to ~L2++, insufficient for L3/L4-required computing density and sensor redundancy)

L3 means drivers can fully take their attention off the road in specific scenarios

Step 4—L4 Mind-Off Driving (2029): Full L4-level autonomous driving in highway and urban scenarios

"Mind-Off": Drivers need not monitor road conditions and can fully engage in other activities

This represents the ultimate form of consumer autonomous driving and the underlying technology foundation for Robotaxi commercialization

Subscription Pricing Model (From 2027):

L2+ (Hands-Free Driving): $69/month

Subscription fees scale up to $199/month as autonomy levels increase

This constitutes one of Lucid's core sources of recurring software revenue

Upgrade Capability Boundaries for Existing Models: Current Lucid Air and Gravity hardware can push autonomous capabilities to L2++ (hands-free on highways and in cities) via OTA without any hardware modifications. Entering L3/L4 requires a completely new hardware platform—Lucid made this distinction very transparently at Investor Day—meaning existing owners cannot upgrade to L4 via paid subscriptions, but new owners of the mid-size platform (from 2028 onward) can enjoy the full path.

5.2 L4-Ready Architecture: Commercialization-Ready from Factory

This is Lucid's core competitive barrier in the Robotaxi market. "L4-Ready" means vehicles are built with all underlying redundancies required for L4 autonomous operation—no post-factory retrofitting needed:

Steering System Redundancy: Dual steering control loops, single-loop failure does not affect vehicle control

Braking System Redundancy: Independent backup braking system

Low-Voltage Power Redundancy: Multi-path power supply to prevent single-point failures from causing vehicle loss of control

Network Communication Redundancy: Vehicle network architecture supports reliable transmission of safety-critical signals

Pre-Planned Sensor Mounting Locations: Camera, radar, and LiDAR installation positions and harness interfaces are designed in from the start, eliminating the need for destructive body modifications during secondary integration

Computing Power Reservation: Ample computing unit installation space and thermal design reserved for the autonomous driving software stack

What does this mean? For traditional OEMs, transforming an ordinary passenger car into a Robotaxi platform requires dismantling and adding numerous components, as well as recertifying each subsystem. The entire process takes 3-4 years. In contrast, Lucid's vehicles are ready out of the factory. Partners only need to deploy the autonomous driving software stack, complete testing and regulatory certification, a process that takes just 12-18 months—cutting time-to-market by more than half.

5.3 Uber + Nuro + Lucid Tripartite Collaboration: Mechanism and Progress

Collaboration Structure:

Lucid: Provides a factory-ready L4 vehicle platform (Gravity → mid-size vehicle)

Nuro: Supplies the L4 autonomous driving software stack (perception, decision-making, control)

Uber: Offers the operational platform, market entry network, and user distribution capabilities

Key Milestones Achieved:

July 2025 contract signing: Uber commits to deploying 20,000 vehicles over six years and invests $300 million in Lucid

Within seven weeks of contract signing: Lucid delivers the first prototype vehicle to Nuro, enabling Nuro to begin testing and developing the software stack on Lucid's platform—a speed possible only because the vehicle is already factory-ready for L4

Over the next six months (leading up to Investor Day): Fleet size expands to 80 vehicles, all conducting data collection, testing, and development in the San Francisco Bay Area

End of 2026: Plans to initiate commercial operations

Differentiation explained by Uber COO Andrew MacDonald: This is not an ordinary commercial procurement agreement but a true trench-style joint development—teams from the three companies collaborate daily to discuss: how vehicle appearance should evolve with sensor additions, how the in-car experience should be optimized for ride-sharing scenarios (unlike personal use), how vehicle control systems should be designed, and how passenger interfaces should be integrated. Uber also holds an equity stake in Lucid as an additional investor, with all three parties closely connected at the management team and board levels, creating highly aligned interests.

Mid-Size Vehicle Robotaxi Collaboration Expansion: At Investor Day, Uber COO announced that Uber and Lucid are finalizing an agreement to deploy Lucid's mid-size vehicle platform for Robotaxi operations on a scale similar to Gravity. This means more efficient and cost-effective mid-size vehicles will become the mainstay of Uber's Robotaxi fleet, with a scale expected to surpass the Gravity contract.

Operational Economics:

Compared to competing Robotaxis, Lucid's mid-size vehicle platform has 34% lower operating costs per mile

Charging speed and range efficiency alone save approximately $2,000 per vehicle annually in operating costs

Calculated for 20,000 vehicles over six years: Cumulative cost advantage of approximately $240 million—this is the core financial logic behind Uber's choice of Lucid

5.4 Lunar Concept Car: A Forward-Looking Vision for a Dedicated Two-Seat Robotaxi

One of the biggest surprises at Investor Day was Lucid's unveiling of the Lunar, a dedicated two-seat Robotaxi concept car deeply modified based on the mid-size vehicle platform.

Why Two Seats? Robotaxi usage scenarios primarily involve urban solo or duo travel, with space utilization for seven or five seats far lower than a dedicated two-seat solution. Reducing seats allows for significant optimization of passenger space quality within the same external dimensions while reducing vehicle weight to further enhance efficiency.

Key Parameters:

Efficiency: 5.5-6 miles/kWh, a significant improvement over the mid-size passenger version (4.5 miles/kWh)

Operating costs: 40% lower than existing Robotaxis

Body based on the mid-size vehicle platform, sharing numerous components, with development cycles and costs significantly lower than a completely new platform

Robotaxi-Specific Optimizations in Interior Design:

Ultra-wide screen spanning both seating positions: Both passengers can use it jointly, supporting shared entertainment content and transforming the journey into a media experience

Integrated AI assistant: Passengers can query information and control entertainment content via voice interaction (not yet activated on the demonstration day)

Front luggage platform: Short trips allow for direct placement of personal items on the front platform without opening the front trunk, improving entry/exit efficiency

Easy entry/exit: Designed for frequent passenger boarding and alighting, clearly distinct from some existing Robotaxi models that suffer from difficult entry/exit due to unconventional body shapes

Additional Commercialization Opportunities: Lucid believes the ultra-wide in-car screen not only improves passenger experience but also opens possibilities for in-car advertising, content subscriptions, brand partnerships, and other additional commercialization models, supplementing the vehicle's revenue streams.

VI. Product Expansion Strategy: Global Distribution Network Upgrade

Lucid will add 42 new sales and service outlets globally in 2026, with clear regional differences in strategy:

North America (+7, 15% growth): Continues the direct retail model, retaining direct customer relationships across the entire chain from "discovery-purchase-ownership-maintenance-repurchase" while maintaining direct access to software subscription revenue. The 15% growth aligns with the expansion pace of U.S. EV charging infrastructure, representing a deliberate supporting layout.

Middle East (+10): Leveraging the natural advantages of Saudi PIF's backing, the Middle East serves as a strategic anchor in Lucid's global strategy. The Saudi government has committed to purchasing 50,000 (fixed) + 50,000 (optional) vehicles, with this government order becoming crucial for early capacity utilization of the mid-size vehicle.

Europe (+25, 200% network growth): This is the most noteworthy regional expansion. The reason is straightforward: By the end of 2026, EV penetration in North America will reach approximately 8%, while Europe will hit 20%—meaning the European market's EV maturity is 2.5 times that of North America, with lower consumer education costs and higher acceptance of long-range luxury electric vehicles.

Europe adopts an indirect distribution model (partner model): Unlike North America's direct operations, Europe uses local partners for sales and service. Core benefits: Front-end capital expenditures reduced by 85%, with network expansion time accelerated by a full year. This is a pragmatic choice to trade brand control rights for capital efficiency.

Germany is the European focus: Two outlet locations are already confirmed, with an additional 10 outlets signed under letters of intent (LOIs). The endorsement as "Germany's Annual Performance Car" has established a genuine brand foundation for Lucid in the German market, rather than an abrupt entry.

VII. Benchmarking Against China's Auto Industry: Gaps, Opportunities, and Threats

7.1 Head-to-Head BOM Cost Competition

At Investor Day, Lucid unusually disclosed direct comparisons of Cosmos's BOM costs with two types of competitors—a leading U.S. EV brand and a leading Chinese new energy SUV brand (both unnamed):

Compared to the leading U.S. EV brand: On the surface, the latter's costs are slightly lower, but when benchmarked against models with shorter range, standardized comparisons (simulating larger batteries needed for equivalent range) show actual costs are comparable or even higher.

Compared to the Chinese competitor: Lucid Cosmos's BOM costs are already lower than the benchmarked Chinese brand.

If accurate, these figures hold strong strategic significance—but require rational skepticism: Chinese brands' cost advantages stem not only from BOM itself but also software R&D costs (lower Chinese engineer salaries), labor costs, historical government subsidy effects, and supply chain vertical integration (e.g., BYD's in-house battery, motor, and chip production). A true total cost comparison is far more complex.

Lucid emphasizes that these figures are based on actual prices from signed procurement contracts, not forecasts or estimates—an important credibility endorsement.

7.2 China Market: Strategic Absence

The entire Investor Day nearly omitted any mention of the China market. Lucid's geographic expansion path is clearly: North America → Europe → Middle East, with China not in the near-term vision (Chinese: "horizon").

The reasons are multifaceted: The Saudi PIF's controlling stake brings potential geopolitical sensitivities; Chinese domestic brands have formed extremely strong product matrices in the RMB 200,000-500,000 range (Aito M9, Zeekr 001, XPeng X9); Lucid's corresponding price range would be RMB 800,000-1.2 million, highly dependent on brand premium in China, where Lucid has virtually no brand recognition.

However, China's supply chain represents an opportunity for Lucid—if tariff conditions permit, sourcing more competitive battery cells from China could further reduce BOM costs. Investor Day mentioned that "tariff changes represent potential upside," a telling phrase.

7.3 Three Perspectives Chinese Automakers Can Learn From

Spatial Engineering Philosophy: Achieving maximum interior space within compact external dimensions through component miniaturization highly aligns with China's market demand for "spaciousness," but the implementation path involves engineering compression rather than simply enlarging the body.

Software Subscription Monetization: Lucid's 65% ADAS adoption rate and $69-199/month subscription model have successfully established user willingness to pay under a luxury positioning. Chinese brands' intelligent driving subscriptions generally face user reluctance to pay; Lucid's pricing strategy and user education path merit study.

Repairability as a Selling Point: Insurance costs have become a critical variable in Chinese new energy vehicle purchase decisions. The claim of "saving $1,000 annually in insurance premiums" directly addresses pain points, representing an exemplary translation of engineering decisions into consumer value propositions.

VIII. Financial Roadmap: Three Phases to Profitability

Key Milestone: 2028 represents the most critical inflection point, when the Air + Gravity + mid-size vehicle platforms jointly contribute 100,000 units in production volume, while diversified revenue streams (ADAS subscriptions, B2B autonomous driving collaborations) begin making substantive contributions to revenue.

Objectives for the End of the Decade (2029-2030)

Non-North American regions like Europe and the Middle East are expected to contribute approximately $5 billion in additional revenue by the end of the decade, while achieving risk diversification and reducing the impact of single-market cyclical fluctuations.

Multi-Lever Pathways to Profitability

Lucid explicitly states it does not rely on a single lever (pure scaling) to achieve profitability but advances on multiple fronts simultaneously:

Passive fixed cost amortization: Fixed costs for factories, R&D, and management dilute as production volume increases

Structural BOM cost reductions: Procurement scale effects from the mid-size vehicle platform create reverse bargaining power with suppliers for Air and Gravity components ("To win the mid-size vehicle contract, first discount Air/Gravity for us")

Continuous manufacturing efficiency improvements: Lessons learned during the 2025 Gravity production ramp-up are directly applied to mid-size vehicle production organization

High-margin software recurring revenue: ADAS subscriptions, AI features, and OTA paid content, once fleet scale reaches a critical point, have extremely low marginal costs for this revenue stream

B2B autonomous driving collaboration revenue: Vehicle procurement and platform licensing revenue from partnerships with Uber/Nuro and others

IX. Scenario Forecasts and Risk Assessment

Scenario 1: Smooth Execution (~25% probability)

Assumptions: Mid-size vehicle achieves mass production by late 2026, delivers over 10,000 units in 2027; Robotaxi launches commercial operations in the Bay Area by late 2026; European market accounts for over 25% of total deliveries by 2027.

Outcomes: 2028 revenue surpasses $5 billion, gross margin turns positive, stock price surges, attracting strategic investors.

Challenges: Lucid has historically delayed nearly every critical milestone; flawless execution is not in its DNA.

Scenario 2: Partial Delivery (~50% probability)

Assumptions: Mid-size vehicle mass production delayed by 6-12 months; Robotaxi commercialization pushed to 2027; European expansion slowed by geopolitical disruptions.

Outcomes: New financing round in 2027 (diluting existing shareholders by 20-30%), backed by Saudi PIF. 2028 production reaches 50,000-70,000 units, gross margin barely turns positive, still short of FCF break-even. Lucid becomes a "small but beautiful" technology-focused luxury EV brand.

This is the most likely path.

Scenario 3: Systemic Pressure (~25% probability)

Assumptions: Mid-size vehicle mass production encounters severe supply chain or quality issues; global EV demand remains weak amid tariff wars and economic downturns; Nuro faces technical or regulatory hurdles, halting Robotaxi collaboration.

Outcomes: Saudi PIF forced to inject more funds and drive strategic contraction. Lucid may seek merger or acquisition by a large OEM. Most likely buyers: Traditional automakers (Volkswagen, Hyundai) or tech companies seeking rapid access to advanced EV technologies.

X. Researcher's Conclusion

Lucid is a company with extremely high technical sincerity, questionable commercial execution capabilities, and delayed scaling rhythms. The technical details showcased at Investor Day—from the 40% power density improvement in the Atlas drive unit to the 80% reduction in non-cell battery pack components, to the 4-minute wiring harness assembly under the three-ECU architecture—are not PPT numbers but verifiable engineering achievements.

Lucid's story has a rare structure in automotive industry history: It simultaneously operates at the highest levels of both traditional automotive (chassis, performance, craftsmanship) and tech new forces (ADAS, software, AI, autonomous driving). This scarcity is genuine, but whether scarcity can translate into market share depends on whether it can survive long enough to reach mid-size vehicle scaling.

The critical node is the 2027 mass production ramp-up speed of the mid-size vehicle. If Cosmos can achieve over 5,000 monthly units by 2027, Lucid's story truly begins; if delayed again or ramping slowly, the $4.6 billion in cash will run critically low by late 2027, with financing conditions determining everything.

Until then, this remains a costly technological experiment being validated by reality.

This analysis is based on publicly available statements from Lucid Motors' 2026 Investor Day, combined with comprehensive industry data estimates, and does not constitute investment advice. The researcher's views represent personal analytical perspectives only.

References and Images

Lucid 2026 Investor Day PPT presentation and speech.

*Unauthorized reproduction or excerpting is strictly prohibited—access this analysis's reference materials by joining our Knowledge Planet to download extensive public references, including the above materials.

-

![]()

Alibaba and Google March Together in the Agent Era

-

![]()

"National Shrimp Farming": 50 Days of AI Arbitrage Frenzy and Its Sudden End

-

![]()

NetEase’s Timeless Classics Shine in Q1, Reinforcing Global Expansion

-

From 'Construction' to 'Effective Management': Shenzhen's Innovative Approach Tackles the 'Last Mile' Challenge in Telecom Governance

-

![]()

A New Yardstick in the AI Era Measures the Path of Tech Giants

-

![]()

Daily Earnings of $650 Million Fall Short: What’s Next for NVIDIA’s Growth Trajectory?

-

![]()

Industrial Integration: Kepler Chooses a Smarter Path

-

Elon Musk's SpaceX Trillion-Dollar IPO Puzzle