March 2025 New Energy Vehicle Sales: Leaping Motors Leads, Li Auto Defends, Xiaomi Motors Emerges as a Wild Card

04/03 2025

04/03 2025

695

695

The March 2025 sales figures for new energy vehicles are now in, with Leaping Motors claiming the top spot for the first time with 37,095 deliveries, breaking the longstanding "NIO-XPeng-Li Auto" trio's monopoly. Beneath these rankings lies a profound transformation in China's new energy vehicle market, where price wars clash with technology wars, and established giants encounter aggressive newcomers in a fierce battle for survival. This competition transcends mere sales numbers, encompassing a comprehensive contest of business models, technological innovation, and consumer perception.

Leaping Motors Takes the Lead: A Strategic Victory

Leaping Motors' ascent to the top might seem abrupt but is grounded in strategic precision. Its 37,095 monthly sales are a testament to its astute positioning in the 100,000-150,000 yuan price range. The all-new pure electric SUV, Leaping Motors B10, priced at 109,800-139,800 yuan, directly addresses the needs of China's largest car-buying segment. Its strategic partnership with FAW provides robust support from traditional automakers in supply chain and manufacturing. This hybrid model of "new force innovation + traditional automaker resources" is proving effective for second-tier entrants.

Leaping Motors' success also underscores a significant shift in the market: consumer focus is transitioning from "technological experimentation" to "practicality and affordability." With electric vehicle penetration exceeding 30%, mainstream consumers now prioritize cost-effectiveness and practical features over flashy tech. Leaping Motors' product strategy aligns with this trend, offering range, space, and basic intelligent functions without excessive reliance on expensive lidar and computing chips, keeping prices within consumer sensitivity thresholds while maintaining quality.

Li Auto and XPeng: Offense and Defense Strategies

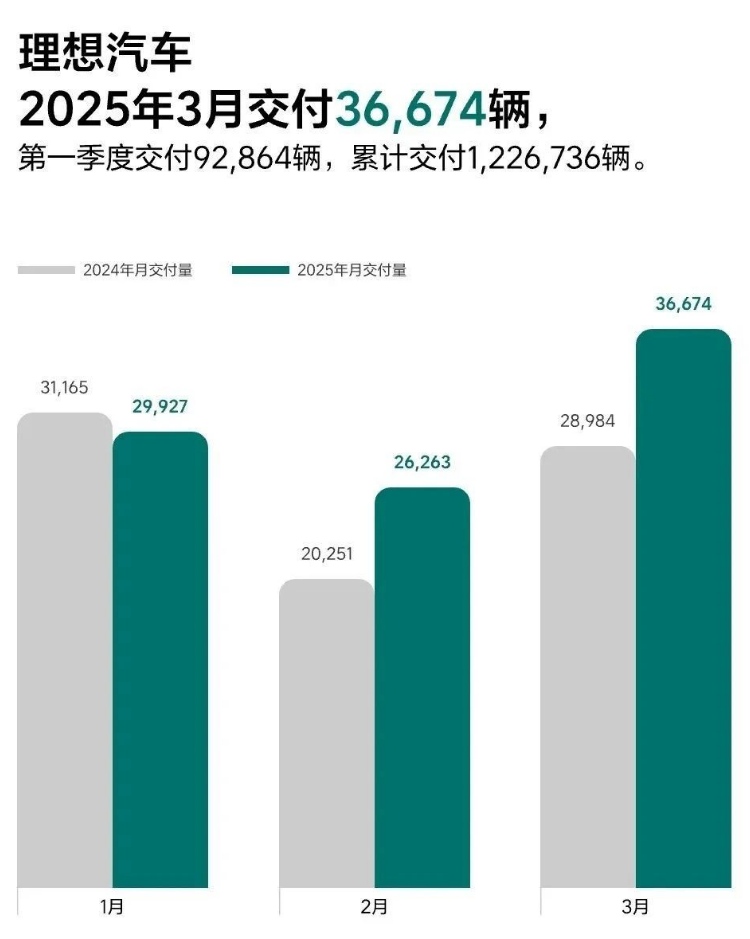

Li Auto delivered 36,674 vehicles, a seemingly stable figure, but with an annual sales target of 700,000 vehicles, it faces significant pressure in the remaining months. A more pressing challenge lies in its sales structure, heavily reliant on extended-range electric vehicles. Its conservative target of 50,000 pure electric vehicles reflects hesitation in a full transition to pure electric. This "two-legged but limping" approach may expose strategic vulnerabilities as the pure electric market accelerates.

XPeng Motors, with 33,205 deliveries and a 268% year-on-year growth, demonstrates another breakthrough strategy: balancing price and technology wars. The 2025 G6's starting price of 176,800 yuan, a direct reduction of 30,000 yuan from the 2024 model, exemplifies the "volume for price" approach. However, XPeng's ingenuity lies in continuously upgrading intelligent driving functions via OTA while lowering prices, preserving its technology brand image. This "hardware parity + software value-added" model is becoming common but demands rigorous cost control and technological iteration.

Xiaomi and NIO: Opposite Ends of the Spectrum

Xiaomi Motors delivered over 29,000 vehicles, showcasing the "miracle of cross-border players." The SU7 Ultra's pricing at 529,900 yuan did not hinder its popularity, validating Xiaomi's premium branding potential. More notably, the upcoming Xiaomi YU7, an SUV targeting the Model Y, could replicate Xiaomi's "cost-effectiveness disruption" in the 250,000 yuan range, potentially reshaping the mid-range market. Xiaomi's threat extends beyond products to its formidable ecosystem synergy, where deep integration with smartphones and smart homes creates unparalleled user stickiness.

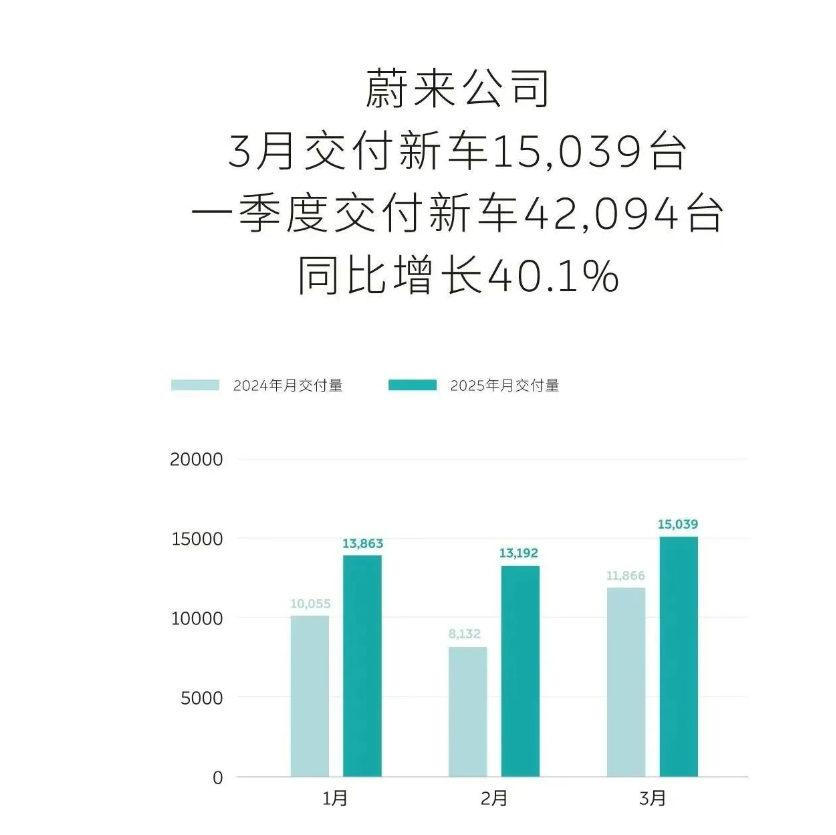

In stark contrast, NIO continues its downturn, with total sales of 15,139 vehicles (10,219 for the NIO brand and 4,820 for the LeDao brand), significantly lagging behind the top tier. NIO's struggles stem from multiple factors: the scalability limits of its battery swapping model, resource dispersion due to its multi-brand strategy, and the vulnerability of its high-end positioning in a cautious market. Whether the upcoming Firefly brand and LeDao L90 can reverse this trend remains uncertain, but NIO's plight proves that early mover advantages do not guarantee sustained leadership in the new force automaking marathon.

Elimination Race Intensifies: Who Will Prevail?

The March sales rankings signal that the new energy vehicle market has entered a brutal elimination phase. The top tier is also witnessing significant differentiation: Leaping Motors and XPeng have achieved rapid growth through different paths, Li Auto faces transformational challenges, NIO urgently needs to reverse its decline, and Xiaomi demonstrates momentum as an emerging force. 2025 will be a pivotal year for new force automakers, with Leaping Motors' ascent marking the beginning of a new stage of diversified competition. The future winners will likely be those who strike the best balance in product positioning, technology routes, business models, and user operations, rather than excelling in a single aspect. As subsidies wane and capital cools, the true test of a company's internal strength has arrived. For consumers, this fierce competition promises better products, more reasonable prices, and improved services. For industry observers, the only certainty is that the plot of the new energy vehicle market will continue to thicken.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving