Insta360 Innovation (688775.SH): When the ‘Vanished Valuation’ Narrative Meets the Share Unlock Cliff

06/05 2026

06/05 2026

464

464

The stock price plummet from RMB 377.77 to RMB 170, with a staggering loss of over RMB 80 billion in market capitalization within eight months, is merely the prelude. On June 11, 2026, a deluge of shares, nearly seven times the current free float, is poised to flood the market—marking the commencement of the true test.

01

Countdown: The 'Quake Lake' Drainage Event on June 11

On June 11, 2025, Insta360 Innovation (688775.SH) made its debut on the STAR Market with an issue price of RMB 47.27. Surprisingly, this panoramic camera company was catapulted by capital to an all-time high of RMB 377.77 within just three months, boasting a market capitalization nearing RMB 150 billion—a valuation surpassing the quarterly revenue of CATL at the time, bestowed upon a consumer electronics company with annual net profits below RMB 1 billion.

Upon listing, Insta360 Innovation had a total share capital of approximately 401 million shares, with only about 32.8 million shares in circulation during the initial period, constituting less than 8.2% of the total shares and a free-float market capitalization of merely around RMB 5.6 billion. The so-called 'trillion-yuan' market capitalization was suspended in mid-air, relying on a few billion yuan worth of shares being shuffled among retail investors, hot money, and quantitative traders.

Now, the ledger for this game has reached the settlement phase.

On June 11, 2026, Insta360 Innovation will face its first major unlocking of restricted shares one year post-listing—an estimated 227 million shares are set to be unlocked, involving pre-IPO shareholders such as EARN ACE LIMITED, QM101 LIMITED, and Thunder Network Technology, along with some strategic placement parties. The unlocked market value is estimated between RMB 38.7 billion and RMB 40.4 billion, accounting for a staggering 56.5% of the total share capital.

With approximately 32.8 million shares currently in circulation, the unlocked shares represent nearly seven times that amount. This is not a mere 'increment' but a seismic shift in the share structure. Even if only 20% of the early shareholders opt to exit at a high—when paper gains remain substantial (issue price of RMB 47.27, with the current price still about 3.5 times higher)—the resulting selling pressure would be sufficient to completely overwhelm the already fragile buying support.

Public data reveals that Insta360 Innovation ranks first in terms of unlocked market value among A-shares in June and tops the list of the top five unlockings in terms of market value that month, at around RMB 40 billion. As of June 3, Insta360's share price has been hovering around RMB 170, down 28% since the beginning of the year and 18.44% over the past 60 days. The market is voting with its feet—no one wants to be caught under the dam before the flood of unlockings arrives.

02

'Revenue Growth Without Profit Increase': Not a Temporary Pain but a Business Model Warning

The last breath of optimism for the bulls hinges on the fact that 'revenue is still growing rapidly.' Insta360 Innovation's full-year revenue in 2025 was RMB 9.741 billion, up 74.76% year-on-year, and its Q1 2026 revenue was RMB 2.481 billion, up a staggering 83.11% year-on-year—at first glance, it resembles an unstoppable growth machine.

However, a closer look at the income statement paints a starkly different picture: Insta360 is sacrificing profit margins to fuel revenue growth.

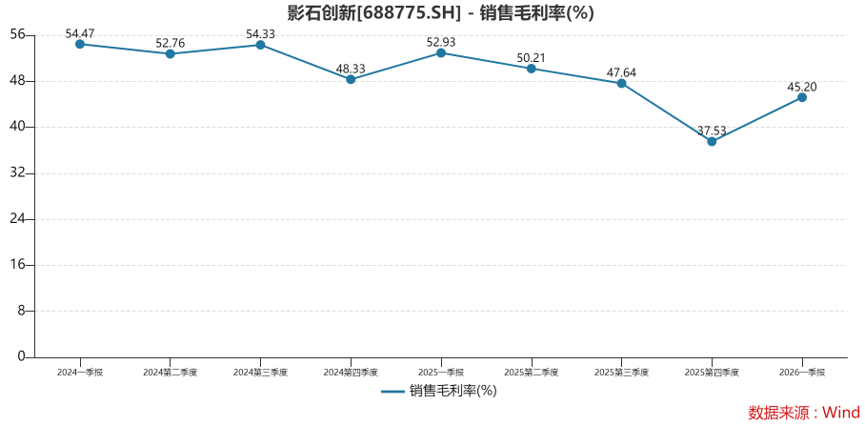

Examining the quarterly trajectory of the gross profit margin more closely—the overall gross profit margin remained as high as 52.93% in Q1 2025 but averaged 45.74% for the full year, dropping to 37.53% in Q4 for the single quarter. A decline of over 15 percentage points in the gross profit margin within a year indicates that, for a consumer hardware company, pricing power is eroding.

Management's external explanation is 'cost pressure from rising raw material prices such as storage chips,' but the market remains unconvinced—because everyone knows that rising raw material prices are merely a superficial symptom; the real issue is a price war that the company has been forced into.

In July 2025, DJI launched its panoramic camera Osmo360, priced at RMB 2,999, directly undercutting Insta360's similar product. Within just three months of entering the market, it captured about 49% of the Chinese e-commerce market and about 43% of the global market. The 'panoramic camera moat' that Insta360 had built over a decade was breached by a single product.

When your 'high-end differentiation' is directly erased by a competitor's lower-priced equivalent product, the decline in gross profit margin is not cyclical—it is a structural shift in pricing power.

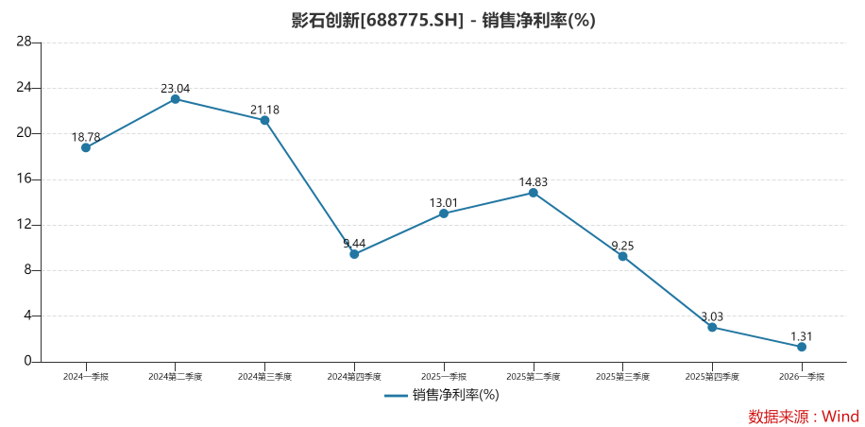

Moreover, the collapse of the net profit margin from over 20% to just 1.3% in Q1 2026 indicates that the problem extends beyond the gross profit side.

In 2025, R&D expenses soared to RMB 1.53 billion, up 96.95% year-on-year, nearly equivalent to the total R&D investment over the past three years; the sales expense ratio climbed to 17.23%; the combined R&D and sales expense ratio surged to a historic peak of 36.8%. The company refers to this as 'strategic losses' and 'paying tuition for new categories.' However, the issue remains—a moat built by burning cash is ultimately not a moat but a cash flow meat grinder.

03

The Illusion of the 'Second Curve': Drones, Action Cameras, and DJI's Suffocating Encirclement

The core pillar of Insta360 Innovation's bullish narrative is that panoramic cameras are merely the starting point, with the company aiming to become a platform-based imaging technology company—launching drones (Yingling/Antigravity A1), action cameras, gimbal cameras (Luna), smart accessories, and even self-developed chips.

Goldman Sachs provided an extremely optimistic forecast in its coverage report: a compound annual revenue growth rate of 64% from 2026 to 2028, with action cameras accounting for 55% of revenue, 360 cameras and drones each about 20% by 2028, and a compound annual net profit growth rate of 81%. This forecast treats the 'best-case scenario' as the 'baseline scenario.'

But reality is striking back one by one:

① Drones—were crushed right out of the gate. Insta360's Antigravity A1 (Yingling A1) was launched in December 2025, with about 30,000 units shipped in its first month, but at a low unit price, negative gross margins, and high marketing expenses, it continued to incur losses. More fatally, DJI holds over 70% of the global consumer drone market share, with extremely high technical patent barriers.

In March 2026, DJI sued Insta360 for infringing on six drone patents, and Insta360 countersued for 28—the litigation cloud itself would severely slow down product iteration cycles and raise overseas compliance costs. The focus of this lawsuit centers on the definition of trade secrets and employment-related inventions. According to public information, DJI alleged in its lawsuit that Insta360 poached its core R&D personnel and took away employment-related invention results in specific technical fields for use in product development.

It is reported that the State Administration for Market Regulation recently issued the 'Provisions on the Protection of Trade Secrets,' which will take effect on June 1, 2026. The 'Provisions' clarify that interim results or failed experimental data and technical solutions formed in production and business activities are also protected if they meet certain conditions, and they list eight types of reasonable confidentiality measures, including signing confidentiality agreements, personnel management, and departure management, fully responding to the actual needs of trade secret protection in the digital age. If the invention results are subsequently determined by the court to be employment-related inventions, the patent ownership will revert to DJI. This means that Insta360 Innovation would have no right to implement the technical solution without permission. If DJI refuses to license it, Insta360 may face the risk of related product removals, production halts, and compensation.

② Action cameras—are the hunting grounds of GoPro and DJI. GoPro has been deeply cultivated in this field for over a decade, with strong brand recognition and content ecosystem barriers; DJI's Osmo Action series, leveraging its drone user base and channel advantages, captured 66% of the global action camera market share in Q3 2025, surpassing GoPro to take the top spot. Insta360 only launched its relevant product line in January 2026, and the presumption of 'going from zero to industry leader' before the financial report's cash flow turns positive seems more like rhetoric to sustain valuation.

③ Gimbal camera Luna—faced a dimensionality reduction attack right from birth. In April 2026, DJI's Osmo Pocket 4 was reduced by RMB 500 to RMB 2,999, precisely suppressing Luna's pricing space. Insta360's profit pool for this single category simply cannot withstand DJI's platform-based strategy of 'cross-subsidizing camera categories with profits from drones and stabilizers.'

Simply put, the global market size for panoramic cameras is only about RMB 6-8 billion, and Insta360 accounts for about 66% of that—meaning the ceiling of its core business is already visible. And every 'second curve' used to 'break through the ceiling' is fighting on DJI's home turf, each requiring losses to gain market share.

This is not a 'temporary pain during a growth transition.' It is the head of a small-track player crashing into the iron wall of a large-track giant's dimensionality reduction clearance.

04

Unlocking Brings the Game to the Liquidation Round

Putting the entire chain together, Insta360's script is uncomfortably clear:

1. During the initial listing period, only 8% of the shares were in circulation, allowing a small amount of capital to push the price from 47 to 377, appearing as 'consensus' but essentially a liquidity illusion caused by artificially constricted supply;

2. A dense barrage of bullish narratives: 'King of Panoramic,' 'China's Second DJI,' 'Platform-Based Imaging Technology,' pricing the best-case scenario into the stock price (peak price-to-earnings ratio exceeding 90 times, far above the consumer electronics industry average);

3. Retail investors chased high and entered the market, with most who bought at the peak on the first day still in floating losses eight months later;

4. Cracks in the fundamentals emerged, with revenue growth without profit increase, a collapse in gross profit margins, direct competition from DJI, and the cloud of patent litigation;

5. The stock price dropped from 377 to 170, with over RMB 80 billion in market capitalization evaporating, but the real supply shock—the release of 7 times the current free float on June 11—still hangs overhead, with the countdown underway.

As of June 3, Insta360's stock price is about RMB 170, with a total market capitalization of about RMB 70 billion, and the trailing price-to-earnings ratio still around 82 times—for a consumer electronics company with a net profit margin collapsed to 1.3%, facing the loss of pricing power in its main business and the largest-ever unlocking shock on the horizon, 'valuation digestion' is probably not something that can be resolved with one or two quarters of bottoming out but may require a more thorough reset of the valuation anchor.

05

Conclusion

The unlocking of nearly 227 million shares on June 11 will subject the premium created by 'artificial scarcity' to the arithmetic of real supply and demand. Early investors hold low-cost shares at RMB 47.27 per share, and even at the current price around RMB 170, the paper return is still over 3.5 times. With a net profit margin of only 1.3%, a declining gross profit margin, and a price war ahead, would you sell?

The answer is probably already written on the tape.

In a market without shorts, the last baton in the hot potato game is always picked up by retail investors. The only difference this time is—even the drumbeat is barely audible.

- END -

-

On the Eve of Its IPO, Avatr Finds Itself Embroiled in a 'Farce of Controversy and Belittlement'

-

![]()

Yutong Optics' Japanese Subsidiary Unveiled in Tokyo, Shifting Strategic Focus to Technology-Driven Growth

-

![]()

Half-Year Revenue Outstrips Last Year’s Total! Zhongrun Optics Forecasts 80.2% H1 Revenue Growth

-

![]()

Why Does AI Competition Start with Computing Power?

-

![]()

Apple AI Finally Makes Its Debut in China, Yet iPhone's 'AI Autonomy' Faces Uncertainty

-

![]()

Apple AI and QianWen Make Up Lessons: Alibaba Has Its Own 'Doubao Phone'

-

![]()

QianWen Joins Apple, Signal for Large Models to ‘Fade into the Background’

-

![]()

The ‘Anchor’ Strategy of Google Hidden Behind the Bleeding Financial Report