Disassembly of the Unmanned Delivery Vehicle Industry Chain

04/24 2025

04/24 2025

1035

1035

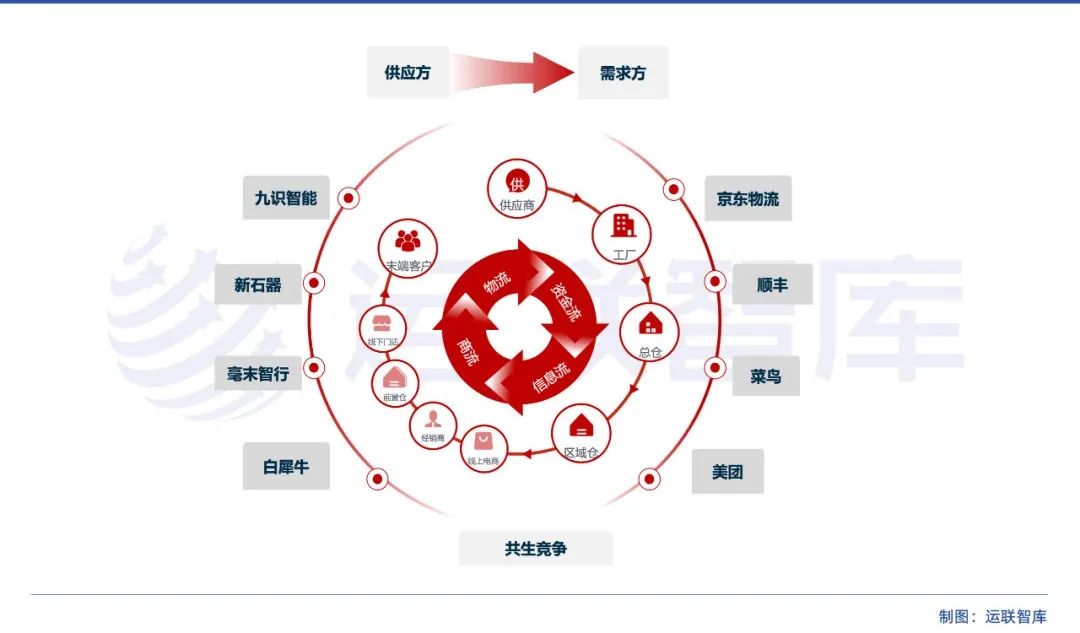

The industry chain of unmanned delivery vehicles constitutes a multi-layered, multi-dimensional collaborative network, centered around technological advancements, cost management, scenario adaptability, and policy directives. Below, we dissect this chain by categorizing it into upstream, midstream, and downstream segments, while also examining the logical interdependencies within each segment.

Upstream: Core Technologies and Components

The upstream segment serves as the technological bedrock of the industry chain, influencing the performance and cost of unmanned delivery vehicles. Technological advancements here propel performance enhancements and cost reductions. For instance, LiDAR is transitioning from mechanical to solid-state, and the surge in AI chip computing power has doubled algorithm efficiency and shortened R&D cycles. Key areas include:

1. Perception Layer: Sensors and Navigation

(1) Sensors: This includes LiDAR (critical for positioning and obstacle avoidance), cameras (for visual recognition), and millimeter-wave radar (for all-weather perception), which collectively form an environmental perception network.

The LiDAR market has witnessed rapid growth in recent years, with YOLI Industry Research Institute predicting a global market size of approximately RMB 43.18 billion by 2026. Leading LiDAR suppliers include Hesai and Robosense.

Many unmanned delivery vehicles are equipped with 4-8 industrial cameras surrounding them to provide a 360° field of view, utilizing deep learning algorithms to extract RGB images in real-time for pedestrian, vehicle, and traffic sign detection, as well as adaptive recognition under varying lighting conditions.

Ultrasonic sensors, primarily placed at the front/rear and sides of the vehicle, have a ranging distance of 0.2-6 meters and a resolution of about 0.1 meters. They excel at detecting low-speed, close-range obstacles and assisting in parking, characterized by anti-interference capabilities and low cost.

(2) High-Precision Positioning and Mapping

Relying on BeiDou/GPS and SLAM (Simultaneous Localization and Mapping) technology, there is a growing demand for lightweight high-precision maps to minimize deployment costs. Well-known map service providers include Gaode and Baidu, while inertial navigation system suppliers, known for their low profile, primarily provide centimeter-level positioning capabilities for unmanned vehicles.

2. Computing Platforms and Chips

(1) Automotive-Grade Computing Platforms: Suppliers such as NVIDIA Drive, Mobileye EyeQ, Cambricon, and Horizon Robotics support real-time computation of perception and decision-making algorithms.

(2) AI Chips: Responsible for data processing and decision-making, GPUs currently dominate, but NPUs and ASICs are gradually gaining traction due to their high energy efficiency. According to ZhiKe Research, the AI chip market size is projected to reach RMB 153 billion by 2025, more effectively supporting the operation of complex algorithms in the future.

(3) Communication and V2X Modules: The V2X communication module industry encompasses vehicle-mounted cellular communication (2G/3G/4G/5G) modules, CV2X dedicated modules, and supporting hardware, software, and services. Key manufacturers include Quectel, Fibocom, SIMCom, Qualcomm, and Autotalks, offering products that support various protocols like LTE/5G, LTEM, NBIoT, and CV2X.

Operators such as China Mobile, China Unicom, and China Telecom are responsible for providing dedicated V2X networks and IoT data packages to ensure stable connectivity. Additionally, remote OTA upgrades, edge computing, and cloud platforms form a comprehensive ecosystem to support vehicle status monitoring, dispatching, and data analysis.

3. Chassis, Batteries, and Actuators

(1) X-by-Wire Chassis and Power System: The X-by-Wire chassis is the core of vehicle motion control, with redundant design enhancing safety. Battery technology (e.g., lithium iron phosphate) must balance range and cost, with automotive-grade standards becoming the norm.

(2) Power Batteries and Motors: CATL and BYD dominate the power battery market, while domestic electric drive leaders also supply motors and electronic controls.

4. Autonomous Driving Algorithms and Software

Autonomous driving technology leverages deep learning and large autonomous driving models (like DriveGPT) to enhance adaptability to complex scenarios. The data closed loop (collection-training-iteration) poses a technical hurdle, and the amortization of R&D expenses impacts the overall vehicle cost.

Midstream: Solutions and Equipment Manufacturing

The midstream segment focuses on the integration and mass production of unmanned delivery vehicles, with core challenges revolving around scale and scenario adaptability. Midstream enterprises must balance performance and cost, and the choice of technology routes (e.g., the number of LiDARs and reliance on high-precision maps) directly influences the pace of commercialization.

1. Vehicle Design and Manufacturing

Modular design allows for customizable cargo boxes, sensors, and endurance to cater to various scenarios like express delivery, supermarkets, and parks. Cost reduction strategies include supply chain integration (e.g., reusing passenger car supply chains) and minimizing the number of LiDARs.

Traditional automakers such as Dongfeng, Great Wall, and SAIC-GM-Wuling have modified their commercial vehicle platforms to accommodate unmanned delivery solutions. Startups like Zhenji Intelligence, Pudu Robotics, Neolith, and White Rhino specialize in the design and mass production of small delivery vehicles.

2. System Integration and Operation and Maintenance

Cloud Scheduling and OTA Upgrades: Facilitate vehicle status monitoring, path optimization, and remote maintenance to reduce operational costs.

Safety Redundancy Mechanisms: Incorporate multi-sensor fusion, emergency braking systems, and collision warnings to ensure the reliability of unmanned operations.

Parameters of Neolith, JD.com, Meituan, and Baidu Apollo Unmanned Delivery Vehicles Source: Neolith Official Website, Kuajikeji, Meituan Official Website, Apollo Official Website

Downstream: Application Scenarios and Demand Drivers

Downstream demand shapes the path to commercialization, with scenario adaptability and policy dividends as the core logic. Scenario complexity dictates technological requirements (e.g., seamless indoor-outdoor switching for community delivery), while policy dividends (e.g., road rights opening) and costs affect the speed of commercialization.

1. Main Application Scenarios

Unmanned delivery vehicles are emerging as a crucial solution for the "last mile" logistics problem. They can replace the short-distance transportation segment from outlets to stations in traditional express delivery and e-commerce, freeing up human resources for genuine endpoint deliveries. Many have already spotted these vehicles in residential areas and around office buildings. In scenarios like supermarket restocking and food delivery, due to high delivery frequency and small single loads, unmanned vehicles can efficiently cover a 3-kilometer living circle, significantly boosting delivery efficiency. Standardized environments such as enclosed parks and ports, with fixed routes and manageable operations, have become priority policy support areas, providing ideal commercial landing spaces for unmanned vehicles.

2. Policy and Standard Drivers

The standard system related to unmanned delivery vehicles is gradually being refined, providing institutional support for the industry's healthy development. Internationally, IEC has released the "IEC63281-3-2" standard, offering a unified method for testing components and complete vehicles of unmanned delivery vehicles. Domestically, institutions like the Beijing Municipal Science and Technology Commission have spearheaded standard formulation, with cities like Beijing, Shanghai, and Shenzhen successively issuing management details and testing road plans for unmanned delivery vehicles to facilitate their legal operation on open roads. Additionally, the formulation of industry standards such as "Technical Specifications for X-by-Wire Chassis of Unmanned Delivery Vehicles" and "Technical Requirements for Autonomous Driving Systems" is beneficial for the industry in building a systematic standardization system and accelerating technology deployment and large-scale applications.

3. Market Demand Growth

With the annual growth rate of express delivery business volume exceeding 20%, the monthly salary of couriers in first-tier cities has reached around RMB 7,000, and labor costs continue to escalate, pushing the transformation of terminal logistics towards automation. According to ZhiYan Consulting, China's unmanned delivery market will expand to RMB 17 billion by 2025.

Industry Chain Collaboration and Future Trends

The development of unmanned delivery vehicles faces multiple challenges and breakthroughs at the technical, industrial, and social levels.

At the technical level, recognizing dynamic obstacles under complex road conditions and adapting to extreme weather conditions still need improvement, while biomimetic designs like stair-climbing robots are gradually expanding application boundaries.

At the industrial level, with the mass production of core components such as LiDAR, the overall vehicle cost has significantly declined, and a 5S service system has been established by integrating transportation capacity, vehicles, and system tools, propelling the industry towards a closed-loop ecosystem.

At the social level, unmanned vehicles can replace some transportation links in the short term but also create new positions such as dispatchers and operation and maintenance personnel. In the long term, they may reshape the human resource structure of the logistics industry, driving the transition from manual labor to high value-added services.

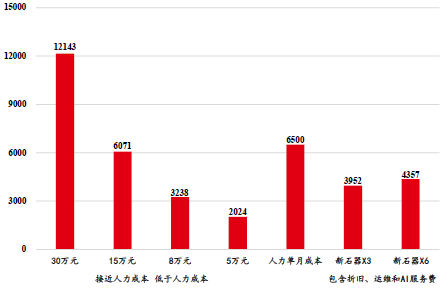

Progress in Landing Depends on Single-Vehicle Costs

In the current unmanned delivery market, express delivery terminals wield significant influence, and each company has distinct expectations for the application of unmanned vehicles. This makes most unmanned delivery companies prefer to "sell cars" or provide autonomous driving software service fees rather than operate logistics themselves.

Thus, the cost of a single vehicle becomes pivotal: if the price is too high or product quality is hard to guarantee, it will be challenging for customers to achieve operational profitability. Currently, due to advancements in autonomous driving technology, the unit cost of unmanned delivery vehicles has approached the economic threshold of manual driving.

The impact of autonomous driving technology on the cost structure is primarily reflected in two aspects. Firstly, as vehicle intelligence increases, urban distribution efficiency also rises, boosting revenue. Secondly, with robust performance support, the entire vehicle can achieve higher stability and reduced human intervention, thereby lowering back-end operation, maintenance, and monitoring expenses.

Whether it's a delivery vehicle used on open urban roads or unmanned transport tools in enclosed scenarios like ports and mining areas, the core competitiveness lies in the vehicle's ability to operate continuously, stably, and intensely without human intervention, coupled with excellent hardware durability and cost-effectiveness.

Total Lifecycle Software and Hardware Cost Estimation of Unmanned Delivery Vehicles (in ten thousand yuan) Source: Euromonitor International, Neolith Official Website, Jiushi Intelligence Official Website

At the pricing level, the business model for unmanned delivery vehicles is not yet standardized, typically involving one-time buyouts or monthly/annual rentals. Many companies attempt to enter the market with low vehicle prices and achieve profitability through subsequent autonomous driving system service fees, lowering the initial investment threshold for customers.

Technological advancements must prioritize safety. L4-level autonomous driving systems need to withstand multiple complex scenarios on open roads to ensure stability during long-term, high-frequency operations. Currently, the industry has amassed considerable experience in autonomous driving safety, with active collision accidents being extremely rare.

From an application perspective, the current unmanned delivery market is still in its nascent growth stage. In city logistics alone, there are over ten million light commercial trucks with low market penetration. Early entrants primarily include technology companies and express delivery industry franchisees, but in recent years, express delivery giants have also begun incorporating unmanned vehicles into their business processes.

However, this transformation is not merely a straightforward replacement but rather entails a multifaceted deep integration process that includes scenario-specific process reengineering, technological adaptation, and system integration. This places heightened demands on the collaborative efforts across the entire industry chain. Currently, a substantial number of enterprises have garnered a solid reputation among users, with many customers already initiating repeat purchases.

Source: Euromonitor International, Neolith Official Website

Comprehensive Monthly Cost of Unmanned Delivery Vehicles

Conclusion

The evolution of the unmanned delivery vehicle industry chain adheres to the core progression of "technological cost reduction - scenario adaptability - policy enablement - demand surge," expediting its shift from pilot projects to large-scale commercial deployment.

Currently, autonomous driving technology is continuously advancing, and both international and domestic standard systems are gradually being established, providing a unified framework for industry access and testing.

Within the industry chain, the four key segments of hardware components, algorithm platforms, vehicle integration, and operational services are increasingly synergistic. Externally, these segments are jointly propelled by standards and policy directives, cloud platform empowerment, and capital market advancements.

As costs continue to decline and application scenarios expand, driverless delivery vehicles are anticipated to emerge as a crucial infrastructure component of the smart logistics system within the next 3-5 years, supporting the intelligent transformation of urban and park-level terminal distribution networks.

-

The Moment to Evaluate Montage Technology Has Arrived

-

![]()

StepOn Has Solved the Monetization Challenge of Large Models with Just a Smartphone

-

![]()

Is a Camera the New AI Safety Guardian? Hikvision Introduces Active Vision Operation Monitoring Gun-Ball Camera at WAIC 2026

-

The Second Half of AI: Cost-Effectiveness Takes Center Stage

-

![]()

Location, Concentration, and Trajectory Tracking: Hikvision’s TDLAS Gas Cloud Imaging Telemetry System Debuts at WAIC 2026

-

The 'AI Study Tour' Under the Original Equipment Manufacturer Model is Set to Create a New Wave of Internet-Famous Science and Innovation Cities

-

![]()

Now, There's a 'Basis' to Curb 'Price Wars': Future Reports of Automakers Setting Low Prices Will Be Probed Under New Rules

-

![]()

WAIC 2026: Farewell to Parameter Races, Full-Chain AI Commercialization