Shen Wei Still Opts to 'Stand Aside'

07/03 2026

07/03 2026

513

513

A few days back, Huawei rolled out a comprehensive update for Xiaoyi Claw. I placed my phone on the table, glanced at the system notification, and was suddenly reminded of something from three months prior.

In March, an open-source project dubbed 'lobster,' named OpenClaw, took GitHub by storm for two weeks. However, by April, the hype had died down—uninstallations surged, group activity dwindled, popularity plummeted, and the frenzy didn't even last a full month.

What about smartphone manufacturers? Huawei, the speediest, waited over three months before finally rolling out 'Xiaoyi Claw' to all users on June 25th. The slower ones followed suit: Vivo's X Fold 6 just launched its 'Atomic Workbench,' where Atomic Notes can assist you in continuing your writing, refining your text, and creating mind maps. It seemed lively, but that was already summer, long after the 'lobster' craze had cooled. Honor was even later, announcing that the next-gen Agentic OS architecture would only be released in July.

Everyone seemed to be rushing to submit their work this summer, as if it were an unavoidable summer assignment.

When you lay out these timelines on paper, it becomes evident: Vivo isn't the slowest on this schedule, but it's certainly the most 'consistent'—so consistent that every step lags half a beat behind, to the point where 'speed' isn't even in its vocabulary.

This is Shen Wei's deliberate choice. He refers to it as 'choosing what not to do.'

But this time, the cost of 'standing aside' might be higher than anticipated.

'Daring to Be Last' Doesn't Cut It Anymore

Let's begin with a series of contradictory choices.

At the start of 2026, Duan Yongping posted on Snowball: 'In the new year, I need to seriously learn how to use AI.' This investor, who retired early and rarely discusses trends, rarely made such a statement about AI. Six months earlier, he had made a bold prediction: 'Of those developing large models, probably no more than 10% will survive in ten years. I'd bet on Gemini because Google, with its immense power, has finally woken up.'

Predictions are one thing, but actions speak louder. By the end of the first quarter this year, Duan Yongping's total U.S. stock holdings exceeded $20 billion, and his portfolio adjustments were even more aggressive than his NVIDIA acquisitions a year ago—he nearly overhauled his entire portfolio.

NVIDIA was his biggest AI play. In Q4 last year, he increased his position by over 11 times in a single quarter, and in the first quarter this year, he doubled it again, bringing his holdings to 13.84 million shares worth $2.4 billion, making it the third-largest holding in his portfolio. But this was just a fragment of his AI strategy—he also initiated a 3.4 million-share position in Tesla, doubled his stake in Google, and simultaneously invested in a slew of AI supply chain companies like Palantir, CrowdStrike, and Snowflake. His Apple position was reduced from 50% to 37%, Alibaba was completely liquidated, and TSMC was significantly trimmed.

This was no longer just 'buying a chip company' but a shift from an 'Apple-centric' strategy to an 'Apple plus AI ecosystem matrix.' Duan Yongping reconfigured his $20 billion in assets for the AI era—he didn't just buy shovels; he bought mines, roads, and miners as well.

Shen Wei took a different path.

His Vivo didn't pour its biggest resources into chasing large models. Instead, he traded his most valuable assets—user data access, channels, and brand—for someone else's 'brain.' The smart assistant in his phones connects to ByteDance's Doubao, and the overseas version uses Google's Gemini. At the Boao Forum in March this year, he officially announced the establishment of Vivo Robot Lab, offering million-dollar salaries to recruit talent, with technical planning roles priced at over $1.2 million annually, formally entering the home robot market.

Both mentor and apprentice saw the same thing: At the model layer, only giants will survive. But their solutions were polar opposites—Duan Yongping's approach was to buy these winners and become their shareholder; Shen Wei's approach was to connect with these winners and become their customer.

Duan Yongping sits behind the scenes as the financier, while Shen Wei has no choice but to play at the table.

This isn't just Shen Wei's choice. It's the same dilemma faced by the entire smartphone industry in the face of AI. But Shen Wei went the furthest—while others were still hesitating about whether to develop their own 'brain,' he had already written 'standing aside' into the company's annual keywords.

To understand Shen Wei's move, you must first grasp the mindset he shares with Duan Yongping.

Duan Yongping has long advocated, and OV has followed for three decades: 'All masters dare to be last; they just do it better than others.' The idea is not to be a pioneer. Blazing a trail for a new category requires tremendous effort to cultivate the market and educate consumers, a slow and costly process. It's better to wait until others have clarified demand, then enter and perfect the product. Slow down, stay steady, and strive to lead from behind.

Vivo has mastered this playbook. After Apple validated touchscreen smartphones as a necessity, Vivo entered the market and became a domestic leader through imaging and audio quality. It believes that time favors those who excel.

Shen Wei himself is a devout follower of this mindset. He rarely gives interviews, appearing in public no more than two or three times a year, but each time he says the same thing—focus on fundamentals, and results will follow naturally. At last year's annual meeting, he wrote 'choosing what not to do' into the annual strategy, saying, 'Choosing what not to do is resolve and wisdom; it determines the bottom line of a company's existence.' He also said, 'Bet less, but bet heavy.'

At the same event, he rarely admitted anxiety, saying the smartphone market 'is expected to shrink further.' But he quickly added, 'Don't compete for short-term speed; compete for long-term depth.' These words from Shen Wei were both a pep talk for himself and an answer to everyone asking, 'Why aren't you rushing?' At the annual meeting, he even laid out the rhythm more bluntly: After smartphones, MR will take three to four years, and robots will take five-plus years. Let others fight the current battles; Vivo will first perfect agents like imaging and photo albums that don't require real-time responsiveness. He doesn't want to be the first to cross the finish line but the last one still running.

His words were measured. But for the usually reserved Shen Wei, this was his most candid public statement yet.

But AI doesn't respect this sense of timing.

Going back to that three-month time difference—this isn't just Vivo dragging its feet; it's an industry-wide issue. A smartphone's operating system only gets one major update per year; the on-device model inside is frozen into the system on day one, with only minor tweaks possible afterward. The really complex tasks must be offloaded to the cloud (according to InfoQ's breakdown of edge-cloud collaboration mechanisms). Meanwhile, cloud-based large models are upgrading almost monthly. Capabilities running on GPT-5 in March may be two generations behind by June.

Google is relatively flexible but has taken a dual-track approach—one for its own Gemini and one for everyone else. Gemini gets system-level access to core apps like Phone, Messages, and WhatsApp without rooting, allowing it to read texts, make calls, and reply to WeChat for you. But third-party AI agents? They're still stuck outside the sandbox. A lobster trying to read the screen or operate apps faces no reduced barriers. In March this year, China's National Internet Emergency Response Center specifically issued risk warnings about OpenClaw's prompt injection and malicious plugin attacks, followed by the Ministry of Industry and Information Technology's notice. Several universities even required students to uninstall it. Technically slow, platforms are also getting involved—compliance and competition act as two gates.

Duan Yongping's 'daring to be last' philosophy relied on a premise: Pioneers are slow and expensive, so latecomers are steadier. That premise has collapsed in AI. Pioneers finish the race in two weeks; latecomers can't catch up.

Shen Wei isn't unaware. He just hasn't found another way to survive yet.

Nine Factories, One Brain

Shen Wei didn't chase recklessly. He took 'standing aside' to the extreme.

Vivo's self-developed Blue Heart large model isn't bad—Blue Heart Little V can write poems, polish text, and create summaries—but Shen Wei clearly doesn't aim to make it the 'smartest.' His biggest bet is on the three-to-five-year horizon—the Robot Lab, gambling that smartphones will collect data, MR headsets will train spatial awareness, and serve as the eyes and brains for future home robots. As for the connected 'brain' needed in phones right now, he conceded it cleanly: Domestically, it's Doubao; overseas, it's Gemini.

On the same question, his peers gave opposite answers.

OPPO's Chen Mingyong, also a disciple of Duan Yongping, is far more impatient. Over two years ago, he sent an internal memo to all staff, declaring 'the first shot of AI smartphones,' saying AI phones represent the third stage after feature phones and smartphones. He immediately established an AI center, allocating resources to AI without limit, going all-in on AI (according to IT Home and QbitAI reports). But to this day, ColorOS still relies on edge-cloud collaboration for model-driven features, and the global version directly embeds Google Gemini. One shouted to take the lead, the other quietly 'stood aside'—yet they ended up in the same place: Neither truly grasped that 'brain.' Shen Wei skipped the hype and saved hundreds of millions in R&D costs.

Xiaomi seems the most determined. It's the only phone maker trying to control the system, chips, and large model in one hand—self-developed HyperOS, self-developed Surge O1 chip, and in March this year, it unveiled a trillion-parameter self-developed model, MiMo-V2. Lei Jun vowed to spend over $16 billion on AI R&D this year. The direction is right, and the catch-up timeline is tight. But while its self-developed model wasn't mature, its Super Xiaoyi first connected to DeepSeek and Doubao. The full-stack dream is intact, but it still lacks a usable self-developed brain. Shen Wei didn't make chips or spend $16 billion, but his ByteDance-powered Atomic Workbench already delivered on the X Fold 6.

Honor was even more eager to make a statement. Last year, it announced the 'Alpha Strategy,' pledging $10 billion over five years to transform into an AI terminal ecosystem company; in June, it 'defined for the first time' AgenticOS, with product line president Fang Fei calling it 'equivalent to redoing hardware with AI.' It sounded grand, but the system's full architecture would only be released this month, with capabilities rolling out gradually in subsequent versions. Yet in the past year of dense press conferences, Honor's domestic market share dropped from first in Q1 last year to sixth (according to Counterpoint data). The louder the announcements, the thinner the hand. Shen Wei didn't hold many press conferences, keeping his words to the low-key Boao announcement.

Even Apple had to concede. Its new version Siri, hyped for two years, delayed and settled for a $250 million lawsuit, finally debuted at WWDC in June—powered by Google's Gemini. The company that epitomizes vertical integration in software and hardware rented someone else's brain for AI. The China version was even more awkward, relying on Alibaba's Tongyi Qianwen as a fallback, stuck in regulatory limbo and accidentally launched for three hours in late March before being withdrawn. Shen Wei had already made the same choice—domestically Doubao, overseas Gemini—but he didn't make it news.

Putting this together reveals a stark fact: By mid-last year, nine of the world's top ten smartphone manufacturers had deep ties with ByteDance's Volcano Engine, with Doubao's large model covering over 400 million devices. ByteDance made it clear: It doesn't make phones but collaborates with manufacturers at the 'operating system level.' Later, even WeChat joined in—on June 4th, it announced plans to connect its smart agent with Huawei, Xiaomi, OPPO, and Vivo. More key entry points in phone systems now belong to others.

Nine phone makers, sharing one brain. Shen Wei's 'standing aside' placed him within that brain's reach too.

Only Huawei was the exception. With its own HarmonyOS, its own Pangu large model, and its own Kirin chips, it's the only one that didn't outsource its 'brain' and the only one that fully rolled out the 'lobster' to users. Keeping the system, model, and chips in one hand is the only escape route on this path. Xiaomi, OV, Honor, and even China's Apple don't have this luxury.

Where Did the Money Go?

If we zoom out further, we'll see this isn't just a strategic choice but a profit allocation issue.

Smartphone makers' profits have been squeezed from both ends in recent years. First, upstream costs. Storage prices went crazy—according to Counterpoint, storage prices jumped 40-50% in Q4 last year and another 40-50% in Q1 this year; memory now accounts for over 20% of the material cost of a mid-range Android phone, up from around 10%. Xiaomi, OPPO, and Vivo all cut their full-year device orders, and Vivo raised prices by $14-$100 across the board in March, but higher prices only discouraged upgrades. Smartphones, this pile of metal, are getting more expensive.

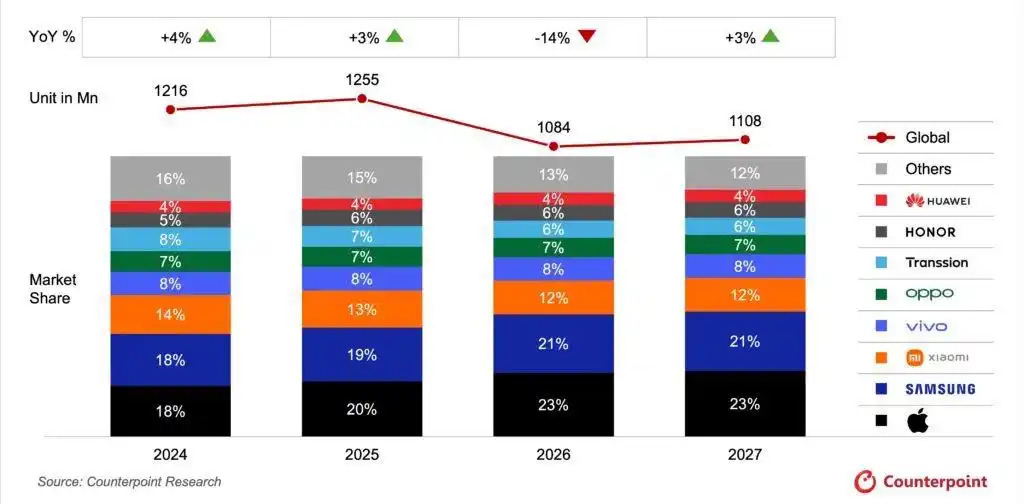

Now look at what they can charge. Counterpoint's Q1 2026 data: Apple took 42% of global smartphone revenue, raising its average selling price by 11% year-over-year. Half the industry's money goes to one company, leaving all Android makers to split the other half. As the saying goes, in this year's smartphone wars, Huawei won volume, Apple held profits, and Xiaomi/OV were squeezed on both ends.

More than two decades ago, a similar scenario unfolded in the personal computer (PC) market. At that time, Microsoft and Intel, armed with Windows operating systems and CPUs, respectively, captured over 90% of the industry's profits. In contrast, machine builders like Lenovo, Dell, and HP were left to share less than 10% of the profits, struggling to stay afloat.

However, it's crucial to clarify: AI is not rendering hardware unprofitable. On the contrary, this year has witnessed significant institutional investments pouring into computing hardware. NVIDIA's supply chain has seen a surge in real orders and profits, while cash-strapped software companies have experienced a halving of their valuations (as reported by TMTPost and other sources). What is truly unprofitable is the highly commoditized metal components in consumer electronics, which have missed out on the computing hardware boom. Moreover, the most valuable layer of intelligence—the software—has had its pricing power eroded by AI models. Duan Yongping recognized this trend more clearly than anyone else. Hence, he didn't merely acquire a chip company; he invested in the entire infrastructure for the AI era, including shovels (basic tools), mines (data sources), and transport lines (distribution networks), completely bypassing traditional phone manufacturers.

So, where does the money ultimately flow?

For many, the first name that comes to mind may not be Google. On one hand, Google integrates its Gemini AI into the Android ecosystem. On the other, it has secured a deal with Apple, with the new Siri being powered by Gemini, reportedly costing Apple billions of dollars annually. The iOS and Android camps, once engaged in a fierce battle for supremacy, now have their most intelligent components driven by the same company's model. According to Sensor Tower data, over the past year, ChatGPT's share in the generative AI market has declined from around 70%, while Gemini's share has skyrocketed from single digits to 27.7%. Alphabet's stock price has more than doubled. Despite not manufacturing a single phone, Google stands at the forefront of this paradigm shift.

In China, it's ByteDance that's capturing this value. The "intelligence" behind nine phone manufacturers ultimately relies on its Doubao AI platform. ByteDance has even partnered with ZTE to launch a Doubao-powered phone, directly integrating large AI models into the system and bypassing the mainstream ecosystems of Huawei, Xiaomi, OPPO, and Vivo.

Among phone manufacturers, only Huawei has managed to secure its own share of the AI pie. Shen Wei, the head of Vivo, has not; his company is still paying for access to others' AI capabilities.

Standing further apart is a disruptor: OpenAI. Its AI device, developed in collaboration with Jony Ive, is slated for release in the second half of this year. There are also rumors of a potential partnership with Qualcomm and MediaTek to manufacture its own phones by 2028, targeting an annual production of 300-400 million units. Even Altman, OpenAI's CEO, admits that this is a new category, not intended to replace smartphones—the moment to truly overturn the phone market has not yet arrived.

In Conclusion

Returning to the phone manufacturers rushing to release new products this summer.

What they've unveiled looks impressive—Huawei's Xiaoyi Claw, Vivo's Atomic Workbench, and Honor's Agentic OS set for release in July. However, beneath the surface, most phone manufacturers truly hold only hardware arrangements in their hands. If this trend continues, their systems will inevitably be replaced. Even in terms of app activity within phones, these fragmented work demands will be supplanted by co-work products like Work Buddy and Marvis, ultimately quietly stripping phone manufacturers of all software pricing power.

Thirty years ago, Duan Yongping imparted to Shen Wei the mantra "Dare to be last, quietly cultivate causes"—a highly effective mindset for the smartphone era. Slowing down was acceptable; time would favor those who excelled. Back then, Vivo could afford to wait—waiting for Apple to validate touchscreens as a necessity, waiting for market education to complete, and then entering to reap the rewards. In Shen Wei's minimally lit office, these words probably still adorn the wall.

The sentiment of "needing to seriously learn how to use AI" feels less like a passing thought and more like a final confirmation before placing a significant order.

The master has acquired the entire map. The disciple is still selectively opting out.

But to be fair.

Shen Wei's heavy bet on robots and spatial awareness might be a gamble that the next gateway lies not in phone-based models but in bodies capable of navigating the physical world. Phone cameras as eyes, MR headsets for spatial computing, and on-device chips running perception algorithms—when pieced together, these fragments point not to a cloud-based brain but to a physical form that can move around your home, serve tea, and care for the elderly. If that's truly the endgame, his current "quiet cultivation" might be planted in a farther, yet more correct, field.

However, the robotics lab was only established in March of this year. Talent is still being recruited, technical routes are still being explored, and products are still just shadows on the horizon.

Meanwhile, the battle has already reached the mountainside. Doubao covers 400 million devices, WeChat's intelligent agents are integrating with phone manufacturers, and Gemini's global share has risen to 27.7%. Whether Shen Wei's shield of "opting out" can withstand the artillery of the smartphone era—let alone the tidal waves of the AI era—remains to be seen.

The track remains the same, but after the starting gun fires, no one is waiting.

Phone manufacturers can no longer view only each other as competitors; in the AI era, their rivals are everyone.

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan

-

A Single-Day 40% Plunge! AI-Themed New Listings: The Cruelest 'Slashes' for Retail Investors in Hong Kong Stocks