China’s AI Industry: A Unified Pivot Towards Monetization?

07/03 2026

07/03 2026

502

502

Image generated by Doubao AI

The Game’s Rules Are Being Rewritten

Written by / Li Xuanqi

Edited by / Li Ji

Layout by / Annalee

As summer 2026 unfolds, China’s AI industry is experiencing a significant transformation.

Recently, Doubao officially launched Doubao Pro, powered by its latest Doubao 2.1 large model, featuring a three-tier pricing strategy.

In mid-June, DeepSeek, previously committed to “no financing, no IPO, no commercialization,” completed its first external funding round, raising over 50 billion yuan, with a post-money valuation exceeding 50 billion USD. At the same time, Doubao, boasting 345 million monthly active users, quietly introduced three tiers of paid subscriptions on the App Store, with the highest annual fee reaching 5,088 yuan. Prior to this, Yuezhiyan (Kimi) had secured five funding rounds within six months, raising a cumulative total of nearly 6 billion USD, with its valuation skyrocketing from 4.3 billion USD to 30 billion USD.

In just a few months, the “Hundred-Model Battle” era—where companies vied on parameters, free quotas, and launch speed—has concluded. Capital no longer solely funds technological narratives, and users no longer unconditionally accept free AI services. A clear industry consensus has emerged: China’s large models are transitioning from a phase of cost-ignoring, cash-burning expansion to a commercial transformation cycle.

On one hand, financing is essential to sustain computing costs; on the other, paid monetization is crucial to validate business models. This collective pivot “towards money” is both an inevitable choice for industry survival and fraught with transformation challenges.

DeepSeek’s 50 Billion Yuan: A Capital Feast Masking Control Disputes

The recent focus of attention is undoubtedly DeepSeek's funding round.

50 billion yuan, approximately 7.4 billion USD, marks the largest single funding round in China’s large model industry. The investor lineup is impressive: founder Liang Wenfeng personally contributed 20 billion yuan, making him the largest single contributor; Tencent invested 10 billion yuan; the CATL ecosystem invested about 5 billion yuan; NetEase, JD.com, Monolith Capital, and IDG Capital each invested about 3 billion yuan; and the National Artificial Intelligence Industry Investment Fund contributed about 980 million yuan. However, another version suggests that Tencent, CATL, and other enterprises and capital participants invested about 1.4 billion USD each.

Image source: Qichacha

But the transaction structure is even more intriguing than the amount.

According to 36Kr, except for the National AI Fund, other external investors' funds were not directly injected into DeepSeek's main entity but into a limited partnership managed by Liang Wenfeng. External investors received economic rights and priority participation in future funding rounds but no voting rights. All external investments are subject to a five-year lock-up period during which they cannot be transferred.

Additionally, on April 27, 2026, DeepSeek completed industrial and commercial changes, increasing its registered capital from 10 million yuan to 15 million yuan, with the additional capital fully subscribed by Liang Wenfeng personally. This raised his direct shareholding from 1% to 34%, and with indirect shareholdings, his total control reached about 84%.

Recall that when DeepSeek first emerged, an investor paid a 5 million yuan meeting fee and visited Hangzhou three times, staking out DeepSeek's building without ever meeting Liang Wenfeng. Another investor from a state-owned fund met eight FA (financial advisors) claiming to have allocation rights, to no avail.

Why would a “money-no-object” founder suddenly open up to financing?

The answer lies in the intensifying industry competition. In 2026, the large model track has shifted to a capital consumption war. According to Zero2IPO Research, total investment in China’s AI sector exceeded 110 billion yuan in the first quarter of 2026, up 185.4% year-on-year. Zhipu and MiniMax have already gone public, and Yuezhiyan has raised nearly 6 billion USD in six months. As competitors' funding levels continue to swell, DeepSeek can no longer sustain head-to-head competition solely through internal financing.

According to CCTV Business statistics, nearly 600 financing events occurred in China’s AI sector in the first quarter of 2026, but funds are rapidly concentrating in a few leading large model companies. Financing difficulties for small and medium-sized model companies have surged, and the Matthew effect continues to strengthen.

Partial financing history of Kimi. Image source: Qichacha

The financing pace of Yuezhiyan (Kimi), one of China’s AI “Four Little Dragons,” perhaps more vividly reflects the capital frenzy. In December 2025, Kimi completed a 500 million USD Series C funding round, with Alibaba and Tencent participating, reaching a post-money valuation of 4.3 billion USD. In February and May 2026, it raised funds again, with its valuation jumping to 20 billion USD. Recently, according to Bloomberg, Kimi is initiating another funding round.

Thus, the market widely interprets DeepSeek's opening to financing not as a cash flow shortage but as a move to leverage industrial capital resources to address commercialization shortcomings, rely on funding advantages to solidify technical barriers in code and long-text reasoning, and layout revenue streams from enterprise APIs and industry-customized solutions.

In fact, changes in the investor structures of DeepSeek and Kimi also hint at shifting winds: early-stage investments were dominated by USD-based VCs and financial investments from internet giants, while now telecom central enterprises, national-level industrial funds, and real economy manufacturing capital are entering in batches. The investment logic has shifted from “betting on technological breakthroughs” to “industrial chain synergy and implementation.”

In short, the rules of the game are being rewritten.

AI’s Pricing Experiments: The Devil Is in the Details

An industry analysis article on Huxiu.com once pointed out that the valuation logic for large models in the primary market has been completely rewritten in 2026: two years ago, institutions primarily referenced parameters, rankings, and user growth rates for valuation; now, the top three metrics scrutinized in due diligence are monthly operating income, amortization of computing costs, and paid user conversion rates. Projects unable to provide a clear commercialization path basically struggle to secure new funding rounds.

This means financing is no longer an expansion gimmick but a “buffer” for leading companies to support their commercial transition period. The premise for capital to provide funds is that companies must present feasible monetization schemes.

A landmark industry turning point was ByteDance's Doubao updating its service agreement on the App Store, officially disclosing a tiered paid subscription scheme and declaring the era of free, national-level AI to have ended. The news instantly propelled the topic “Doubao to Officially Charge” to the top of hot search trends, with over 300 million views.

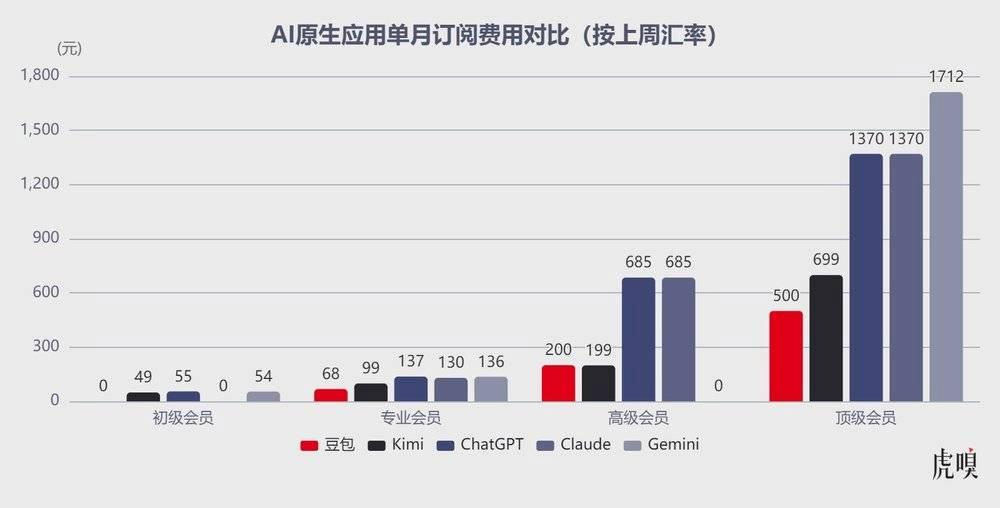

Specifically, Doubao Standard costs 68 yuan/month (approximately 10 USD); the Enhanced version costs 200 yuan for continuous monthly subscription or 2,048 yuan annually; and the Pro version costs 500 yuan for continuous monthly subscription or 5,088 yuan annually. Paid benefits focus on high-computing-power productivity scenarios, including AI batch PPT generation, in-depth data analysis, long document batch processing, high-definition graphic and video generation, enterprise-level API access, priority computing power scheduling during peak hours, and extra-large context quotas—value-added services precisely targeting office workers, content creators, and small and micro-enterprise clients.

On June 24, 2026, Doubao officially released Doubao Pro, based on its latest Doubao 2.1 series large model, adopting a three-tier pricing scheme: the Standard package costs 68 yuan for continuous monthly subscription; the Enhanced package costs 200 yuan for continuous monthly subscription; and the Advanced package costs 500 yuan for continuous monthly subscription.

Why is Doubao charging?

Let's crunch the numbers. By March 2026, Doubao's large model daily Token usage had surpassed 120 trillion, up from about 120 billion at its initial release in May 2024—a 1,000-fold increase in two years. Reports also indicate that ByteDance is discussing spending 70 billion USD in 2026 on data center construction and other AI infrastructure.

Clearly, ByteDance's launch of a paid version is not a hasty attempt to harvest users but a premeditated move to complete user segmentation operations: retaining massive general users to solidify the base while having heavy-duty paid users cover marginal computing costs, exploring a sustainable business model of “free foundation + value-added monetization” to address the industry's common problem of “increasing users leading to greater losses.”

This is also an industry consensus.

Before Doubao officially announced its paid model, Kimi had already completed its commercialization layout. On September 25, 2025, Kimi officially launched two tiers of paid subscriptions at 49 yuan/month and 99 yuan/month, targeting professional scenarios such as contract review, academic paper dissection, financial report in-depth analysis, and large-volume long material sorting. According to an internal letter from Kimi's founder, from September to November 2025, after the membership launch, its paid user monthly growth rate once exceeded 170%, with overseas API call revenue simultaneously quadrupling, forming a dual revenue structure of C-end membership subscriptions + B-end API calls.

However, public complaint information on the Heimao Complaints Platform shows that many paid users have reported issues such as model lag during peak hours, errors in ultra-long document parsing, and cumbersome post-sale refund processes.

DeepSeek, meanwhile, took a different approach. In May 2026, DeepSeek announced a permanent price reduction for its V4-Pro interface to 25% of the original price, with cache hit call prices reduced to one-tenth of the original, relying on extreme cost advantages to target orders from small and medium-sized developers and software service providers, attempting to achieve revenue balance through scaled calls.

Image source: Huxiu

In short, as QuestMobile data shows, the commercialization paths of current domestic leading AI platforms are still being explored, generally maintaining a strategy of “free basic applications + tiered charging for upgraded versions.” Overall, domestic AI paid services are still in their early cultivation stage, with users not yet forming stable payment habits. Product value alignment, pricing rationality, and experience stability will determine the pace of each company's commercialization.

But one thing is certain: from DeepSeek's first funding round, Kimi's continuous capital injections, to Doubao's decisive trial of a paid system, a series of landmark events mark a critical turning point in China’s AI industry. “Shifting towards money” is not a utilitarian regression for China’s AI but a necessary path to maturity.

Technology requires money to nurture, and commerce needs time to validate. What China’s AI is experiencing is the inevitable journey from the laboratory to the market, from idealism to reality. This path is destined to be uneven—users will vote with their feet, capital will vote with valuations, and the market will vote with time.

In short, China’s AI is shifting “towards money.” But whether it can truly earn money is another question.

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan