Can Lumi United Tech, With 1.47 Billion Yuan in Annual Revenue and 300 Million Yuan in Losses, Successfully List on the Hong Kong Stock Exchange by Relying Only on Xiaomi?

04/10 2026

04/10 2026

528

528

Caigou Business Review © Original content by our editorial team

Author | Fei Ma

In the spring of 2026, the smart home sector witnessed renewed turbulence. Shenzhen-based IoT unicorn Lumi United Tech (hereinafter referred to as "Lumi") officially submitted its prospectus to the Hong Kong Stock Exchange, with Huatai International as the sole sponsor. As a former star enterprise in Xiaomi's ecosystem, Lumi stepped into the spotlight of the capital markets, boasting the title of "the world's largest provider of China's spatial intelligence infrastructure."

However, the data disclosed in the prospectus has sparked widespread discussion in the market: Lumi's revenue has hovered around 1.5 billion yuan for three consecutive years, with cumulative net losses exceeding 700 million yuan over the same period. Amid increasingly fierce competition in the whole-house smart home sector, is Lumi—a company highly dependent on Xiaomi's ecosystem—a "hidden giant" with deep technological barriers, or merely a "contract manufacturer" stuck in a growth bottleneck?

Lumi Founder You Yanyun

Lumi Founder You Yanyun

The Truth Behind Stagnant Revenue and "Strategic Losses"

Upon reviewing Lumi's prospectus, the most striking impression is of its "stagnant" business scale and "shocking" reported profits. However, delving deeper into the data reveals profound qualitative changes in its financial structure.

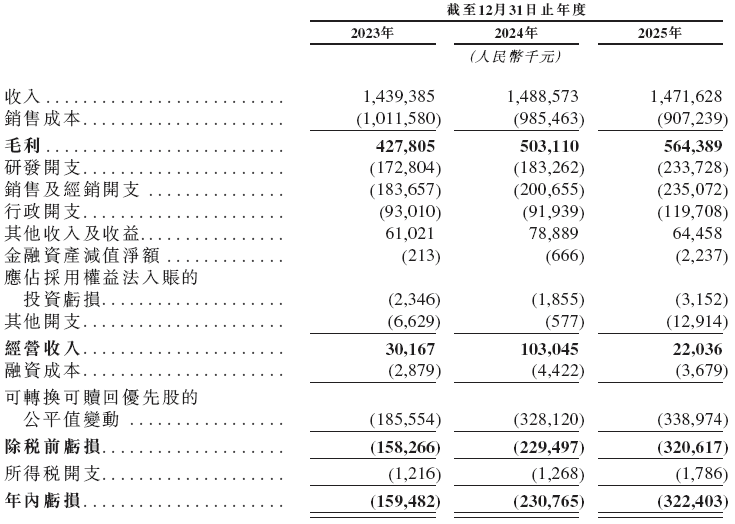

Data shows that in 2023, 2024, and 2025, Lumi's operating revenues were 1.439 billion, 1.489 billion, and 1.472 billion yuan, respectively. Against the backdrop of double-digit growth in the smart home industry as a whole (with China's smart home market scale exceeding 1.2 trillion yuan in 2025), Lumi's revenue growth has clearly failed to keep pace with the broader market.

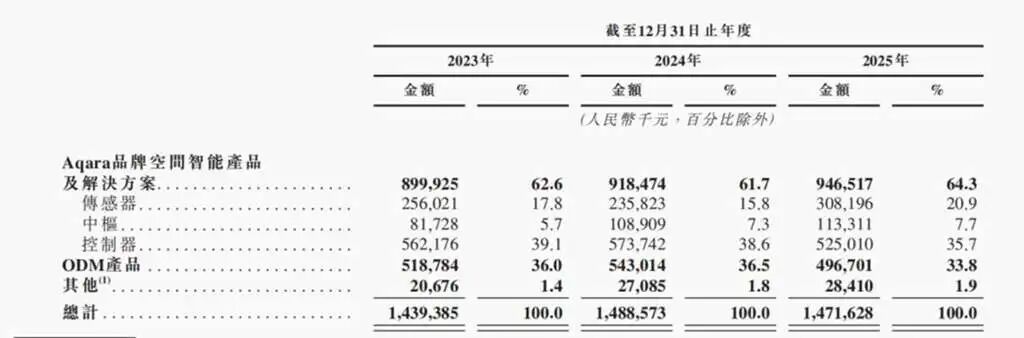

Yet, beneath the surface of stagnant revenue, its profit quality has been steadily improving. From 2023 to 2025, Lumi's overall gross margins were 29.7%, 33.8%, and 38.4%, respectively, cumulatively increasing by nearly 9 percentage points over three years. This significant improvement is primarily attributable to the optimization of its business structure: the revenue share of its high-margin proprietary brand Aqara rose from 62.6% to 64.3%, while the proportion of relatively low-margin ODM contract manufacturing gradually declined.

Trends in Lumi's Revenue, Net Profit, and R&D Expenditure (2023-2025)

Trends in Lumi's Revenue, Net Profit, and R&D Expenditure (2023-2025)

The most glaring data point in the prospectus is the expanding net losses year after year: 159 million yuan in 2023, 231 million yuan in 2024, and a staggering 322 million yuan in 2025. With cumulative losses exceeding 700 million yuan over three years, does this imply that Lumi's business model is unsustainable?

The answer is no. A deep dive into the income statement reveals that the current losses are primarily due to changes in the fair value of convertible redeemable preferred shares. This is a common occurrence in IPOs of new economy companies listed in Hong Kong—the higher the company's valuation, the larger this reported loss becomes. If non-operating factors such as share-based compensation expenses, fair value losses on preferred shares, and listing expenses are excluded, Lumi has already demonstrated self-sustaining profitability. Its adjusted net profits were 45 million, 113 million, and 57 million yuan in 2023, 2024, and 2025, respectively.

Detailed Core Financial Data for Lumi (2023-2025): Note the "Fair Value Change of Convertible Redeemable Preferred Shares" item

Detailed Core Financial Data for Lumi (2023-2025): Note the "Fair Value Change of Convertible Redeemable Preferred Shares" item

As a hard-tech enterprise recognized as a key "specialized, refined, distinctive, and innovative" little giant, Lumi spares no expense on R&D investment. From 2023 to 2025, its R&D expenditures were 173 million, 183 million, and 234 million yuan, respectively, with the proportion of total revenue climbing from 12.0% to 15.9%. This high-intensity R&D investment has enabled it to build a complete product lineup spanning 50 categories and 1,700+ SKUs, along with a technological moat of over 1,000 patents.

Is Xiaomi's Ecosystem Sweet Honey or Deadly Poison?

Since joining Xiaomi's ecosystem in 2014, Lumi has formed a deep-seated interest alignment with Xiaomi. This partnership provided Lumi with substantial traffic and order dividends in its early stages, but as it approaches its IPO, it has become a Sword of Damocles hanging overhead.

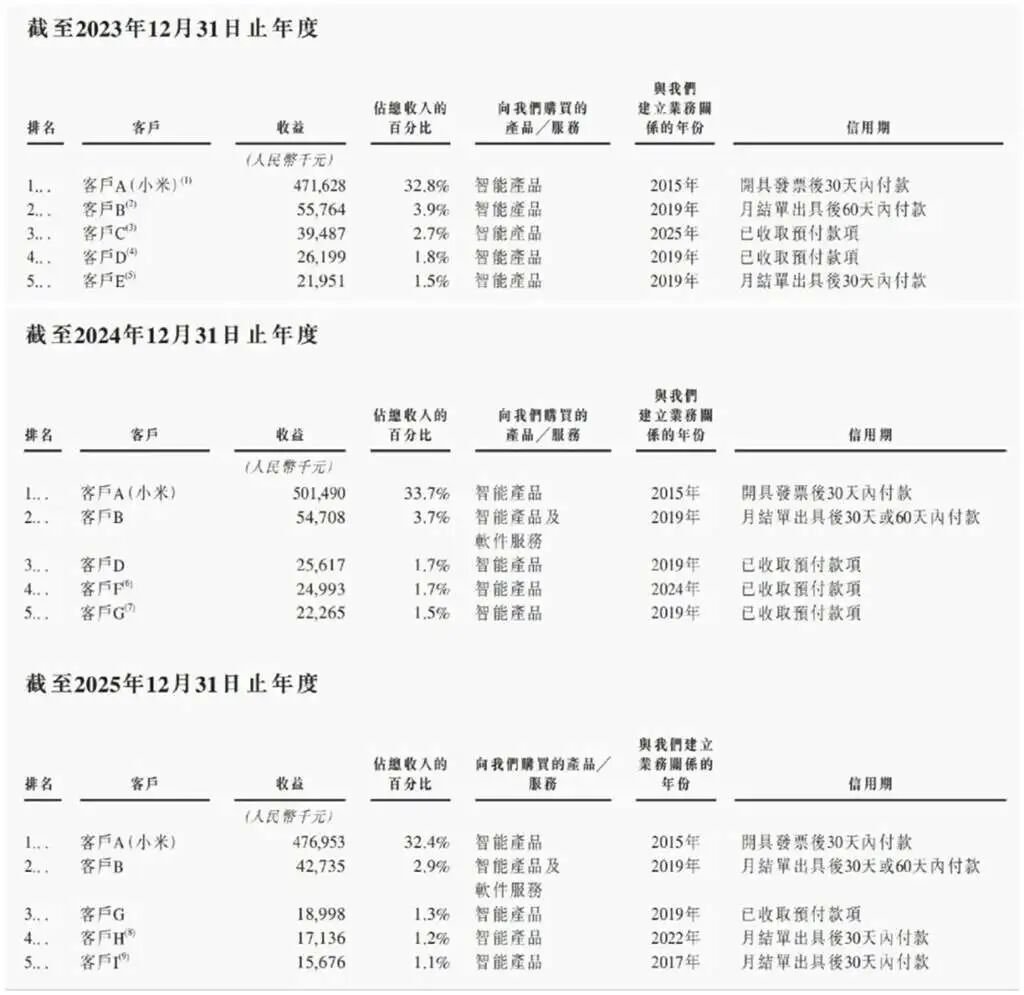

Xiaomi is Lumi's absolute single largest customer. From 2023 to 2025, Lumi's revenue from Xiaomi was 472 million, 501 million, and 477 million yuan, respectively, accounting for a stable 32.8%, 33.7%, and 32.4% of total annual revenue. This means nearly one-third of Lumi's lifeline is in Xiaomi's hands.

Breakdown of Lumi's Top Five Customers: Xiaomi (Customer A) Contributes Over 32% of Revenue for Three Consecutive Years

Breakdown of Lumi's Top Five Customers: Xiaomi (Customer A) Contributes Over 32% of Revenue for Three Consecutive Years

Not only is Xiaomi Lumi's core customer, but it is also a key supplier. Lumi needs to purchase integrated circuits, modules, and adapters from Xiaomi, with procurement amounts rising from 2.8% to 4.9% of total revenue from 2023 to 2025. Additionally, in terms of equity structure, Xiaomi Group holds a 7.92% stake; at the management level, Lumi President Lin Zhen, Non-Executive Director Jiang Wen, and several other executives have deep Xiaomi backgrounds.

Excessive customer concentration is a key focus in IPO reviews. To shed the label of "Xiaomi's contract manufacturer," Lumi began laying the groundwork for its proprietary brand Aqara as early as 2016, adopting an extremely clever differentiation strategy—deep integration with Apple's ecosystem.

Integration with Apple's smart home ecosystem forms Lumi's core barrier in overseas and high-end markets. By the end of 2025, over 340 Lumi models had been integrated into Apple Home, making it the world's first door lock manufacturer to support Apple Home Key and UWB hands-free unlocking. This strategy of "independence while maintaining compatibility" (supporting both Xiaomi and Apple Home) has not only enabled Lumi to successfully penetrate developed markets like North America and Europe but also allowed its overseas revenue to gradually surpass its domestic market, effectively hedging against single-customer risks.

Steady Increase in Proprietary Brand Aqara's Revenue Share, Gradual Decline in ODM Business Share

Steady Increase in Proprietary Brand Aqara's Revenue Share, Gradual Decline in ODM Business Share

Dealer Attrition and Giant Encirclement

Despite its strong product and ecosystem performance, Lumi faces severe challenges in channel operations and market competition.

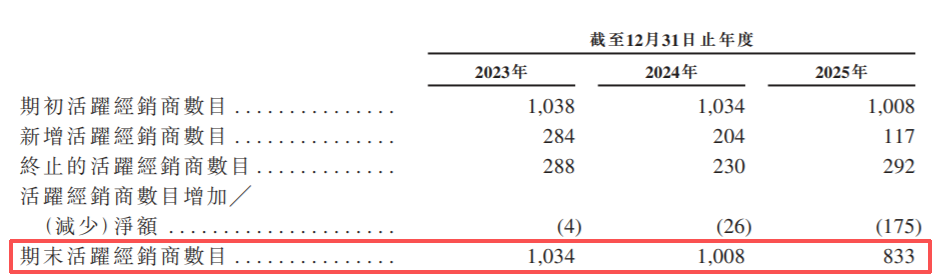

Whole-house smart homes are characterized by their "experience-heavy, delivery-heavy" nature. Lumi's offline service provider system was once its proud moat (pioneering the smart home 4S service system). However, data disclosed in the prospectus reveals troubling signals: Lumi's number of active dealers plummeted from 1,038 at the beginning of 2023 to 833 by the end of 2025. In 2025 alone, the net decrease in active dealers reached 175.

Lumi's Number of Active Dealers Shows a Year-over-Year Decline

Lumi's Number of Active Dealers Shows a Year-over-Year Decline

Lumi attributes this to "increased direct sales and the elimination of some dealers." However, it cannot be denied that limited operational control over dealers, inventory pileup risks, and the high operating costs of offline stores are eroding the stability of its channel network. In 2025, revenue from dealers accounted for 57.0% of Aqara brand revenue, making channel turbulence a direct threat to its core business.

In 2024, China's whole-house smart home industry market size was approximately 222.4 billion yuan, with projections to exceed 440 billion yuan by 2030. Facing this massive market, competition has evolved into a multi-factional battle:

Tech Giants: Huawei's HarmonyOS Smart Home leverages system and communication advantages to target the high-end market, while Xiaomi Mi Home covers the mass market with its ecosystem and cost-effectiveness.

Traditional Home Appliance Enterprises: Haier Smart Home and Midea Group rely on their deep home appliance foundations and vast offline channels to rapidly deploy full-scene solutions.

Vertical Innovators: Companies like Lumi Aqara and ORVIBO deeply cultivate bottom-layer sensors and niche technological fields.

Within this competitive landscape, while Lumi holds a 20% market share in sensors, it still has significant shortcomings compared to giants like Huawei and Midea in terms of brand recognition, capital scale, and full-category home appliance synergy.

Will the Capital Markets Buy In?

What macroenvironment does Lumi face as it prepares to list on the Hong Kong Stock Exchange in 2026?

First, favorable funding and policy conditions exist. Since 2025, the Hong Kong IPO market has staged a strong recovery, particularly with the implementation of Chapter 18C rules for technology innovation enterprises, significantly lowering the listing threshold for hard-tech companies. Simultaneously, Southbound and overseas capital are continuously increasing their allocations to Hong Kong's IT sector. The recent successful listings and strong performance of To B robotics companies like Geek+ demonstrate international capital's recognition of high-quality Chinese tech assets.

Second, Lumi's "spatial intelligence" narrative is unique. Positioning itself as a "spatial intelligence infrastructure provider," Lumi emphasizes its self-developed ORAP semantic framework, edge computing capabilities, and deep support for the Matter protocol. This full-stack capability—spanning bottom-layer hardware to system-level and experiential layers—distinguishes it from ordinary smart single-product manufacturers and aligns with the current AI large model-driven transformation of the smart home industry.

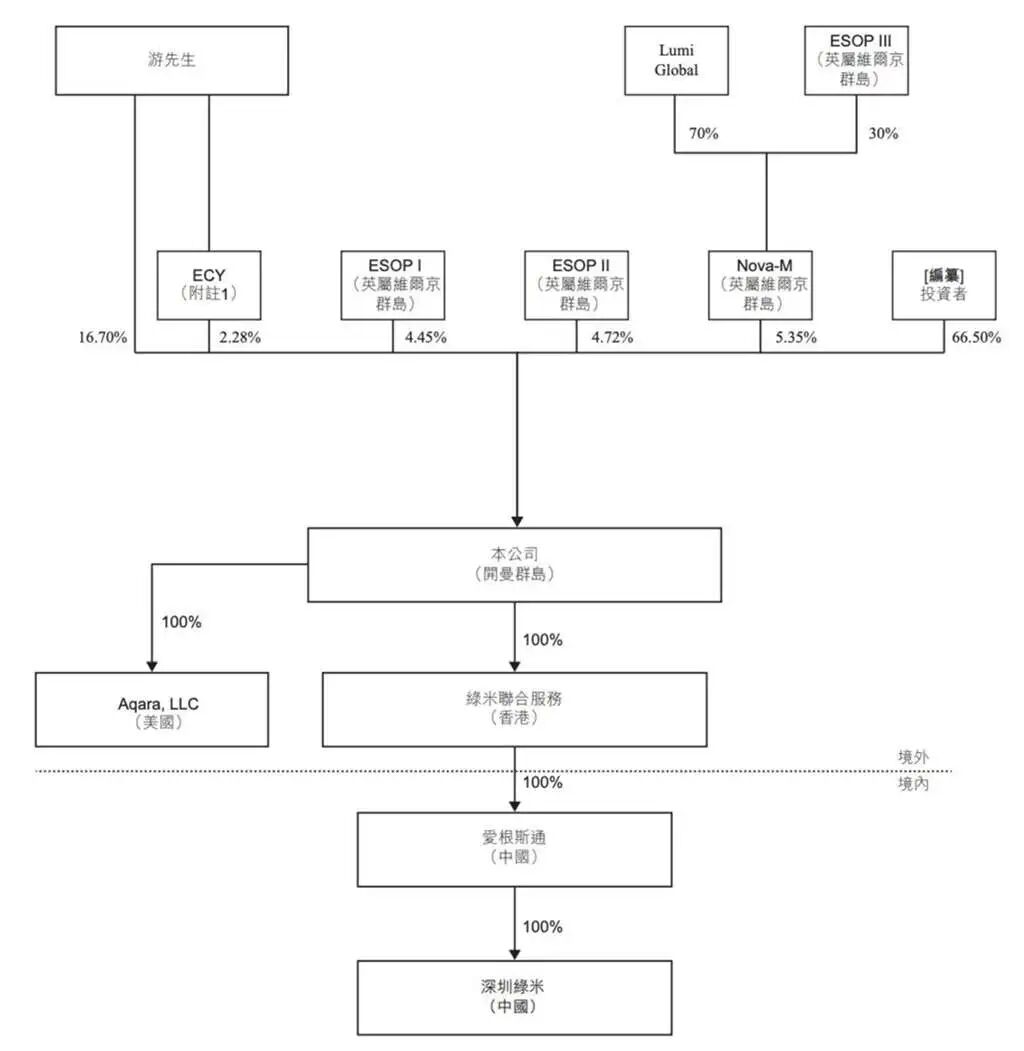

Lumi's Pre-IPO Equity Structure: Industrial Capitals Like Xiaomi, Midea, and China Telecom Gather

Lumi's Pre-IPO Equity Structure: Industrial Capitals Like Xiaomi, Midea, and China Telecom Gather

In this IPO, Lumi plans to allocate the largest proportion of proceeds to R&D investment, followed by expanding sales channels and enhancing brand awareness. This indicates that management clearly recognizes that technological barriers and global channels are the keys to escaping internal competition and achieving valuation leaps.

Conclusion

Lumi United Tech's prospectus reveals the typical growing pains and transformation of a Xiaomi ecosystem enterprise as it matures. Behind the annual revenue of 1.47 billion yuan and reported losses of 300 million yuan lies its strategic choice to actively optimize its business structure and increase R&D investment.

Relying solely on Xiaomi might allow Lumi to thrive comfortably, but it can never support a hundred-billion-yuan independent listing platform. Lumi's true ace lies in its differentiated ability to penetrate the Apple ecosystem and its technological accumulation in bottom-layer sensors and spatial intelligence algorithms.

Listing on the Hong Kong Stock Exchange is just the first step. After going public, Lumi must prove two things to the capital markets: first, whether it can find new growth engines through overseas markets and B-side businesses (smart buildings, hotels, etc.) after three years of stagnant revenue; second, whether it can stabilize and expand its offline service provider network amid pressure from giants like Huawei and Midea. Only by overcoming these two hurdles can Lumi truly transform from a "contract manufacturer behind Xiaomi" into a global leader in spatial intelligence.

Disclaimer: This article is based on publicly available information or data provided by interviewees. However, Caigou Business Review and the author do not guarantee the completeness or accuracy of the information or affiliated details mentioned or displayed in this article and do not represent the stance of any institution. In case of infringement, please contact us for deletion. Under no circumstances shall the information or opinions expressed in this article constitute investment advice to any individual.

▼

-END-

-

![]()

Breaking News | Core Chip Team Member Unexpectedly Changes Jobs! OpenAI Transforms into Anthropic's Talent Hub, with Over 15 Ex-OpenAI Core Members Now Holding Key Roles at Anthropic

-

![]()

When European Factories Face Idle Capacity, Chinese Brands Offer a ‘Traditional Chinese Remedy’

-

![]()

SEER Robotics Passes IPO Hearing: How Valuable Is the 'First Robot Brain Stock?'

-

![]()

5 Years, 170 Billion Yuan Wealth Vanishes: Where Did Wei Jianjun Go Wrong?

-

![]()

What Exactly Has Changed with the AI That Automatically Opens a Browser to Search Xiaohongshu?

-

![]()

Over 3,000 Heat-Related Deaths Daily, Yet India Imposes Ban on Chinese Air Conditioner Imports: Unraveling the Underlying Motives

-

![]()

Second-Hand Car Prices Plummet: Are Gasoline Vehicles on the Verge of Collapse?

-

![]()

800V vs. 48V: Which Reigns Supreme? Online Clash Between Executives Intensifies Debate Over Li Auto and NIO's Suspension Systems | MIRROR Pro