"Post-Huawei Era": Seres Advances into the Self-Validation Phase

04/10 2026

04/10 2026

555

555

Seres reported its 2025 financial results, achieving RMB 165.05 billion in revenue and RMB 5.96 billion in net profit attributable to shareholders. With revenue reaching an all-time high and profits continuing to rise, the financial data appears impressive at first glance.

However, the capital market has remained largely unimpressed.

At the same time, Seres' market capitalization hovered around RMB 150 billion, nearly halving from its peak last year. The contrast between a growing financial report and a shrinking market cap underscores market skepticism about Seres' future prospects: In the "post-Huawei" era, what strategic path will Seres pursue?

The answer cannot be reduced to a simple binary choice between dependence on Huawei or independence. After new energy vehicle adoption reached a certain threshold, discussions around technological breakthroughs and restructured industry分工 (division of labor) have resurfaced. For most automakers, the past two years have been defined by "transformation." The core challenge lies in identifying a sustainable development model for the next phase.

To truly understand Seres, we must look beyond vehicle sales volumes and profit figures. The critical questions are: How were these vehicles sold? How was profit distributed? More importantly, what kind of "identity" is Seres constructing atop its existing collaborative framework?

I. A "Fragmented" Financial Report and Market Confusion

According to the financial report, Seres sold a total of 517,000 vehicles in 2025, with 426,000 deliveries under the AITO brand. In the fiercely competitive premium new energy vehicle market (vehicles priced above RMB 250,000), this performance solidified Seres' position as the second-largest player in extended-range electric vehicles, trailing only Tesla.

More notably, amid industry-wide "price wars," Seres maintained its pricing strategy. The average transaction price for AITO vehicles increased from RMB 377,000 to RMB 391,000. This indicates that its product strength—particularly Huawei's intelligent driving technology—has created differentiated consumer appeal, supporting premium brand pricing.

The issue lies in profit distribution.

Seres achieved a gross margin of 28%, significantly outperforming all listed new energy vehicle companies. This demonstrates the effectiveness of its product positioning and cost control. However, this high gross margin translated into a net profit margin attributable to shareholders of only around 3.6%. In the fourth quarter, this figure dropped to 1.2%.

Where did the profits go?

Judging by the expenses disclosed in the financial report, sales, administrative, and R&D expenses collectively consumed over 24% of revenue. Among these, the sales expense ratio reached 15%, far exceeding competitors in the same price range. For example, Li Auto's combined per-vehicle sales and administrative expenses amount to approximately RMB 26,300, while Seres' are close to RMB 60,000.

This difference of around RMB 30,000 per vehicle is key to understanding Seres' business model. It is not "wasted" but partially flows to Huawei (though not exclusively) to compensate for Huawei's contributions in technology licensing, brand empowerment, and channel sales.

A clear picture emerges: Seres builds high-quality vehicles and sells them at premium prices, achieving substantial gross margins. However, to acquire the "capabilities" to build and sell these vehicles, it must allocate a significant portion of its profits as compensation.

This financial structure directly leads to a second market confusion: the failure to achieve traditional economies of scale.

In conventional manufacturing, the golden rule is that as production volume rises, fixed costs per vehicle decrease, boosting profitability. However, Seres' financial report does not reflect this trend. Its per-vehicle costs did not decline significantly with the delivery of 426,000 units.

When viewed through the lens of its business model, the reason becomes clear: The portion of costs paid to Huawei for various services is not fixed (like factory or equipment depreciation) but a variable cost tied to sales volume. The more vehicles sold, the higher these expenses rise. For Seres, the leverage from economies of scale is relatively limited.

High growth and high gross margins, yet constrained net profits and a breakdown of traditional economies of scale—these results precisely outline Seres' unique position in the current industrial division of labor. It is not a traditional automaker but has not yet fully transitioned into a pure technology company.

II. Decoding the "Huawei-Seres" Model: Balancing Efficiency and Autonomy

How should we view Seres' previous operating model? The market often resorts to simplistic labeling, but this approach is overly reductive and even misleading.

A more accurate description is that during a specific historical and technological window, the market naturally forms deep value alliances. Huawei provides the most scarce and expensive "soft power" in the intelligent vehicle era: full-stack intelligent solutions, brand influence, and a vast retail channel network. Seres contributes "hard power" such as mature vehicle design, manufacturing, supply chain management, and quality control.

Their combination is commercially efficient. Huawei avoids heavy asset investments in vehicle manufacturing, rapidly commercializing its technology. Seres bypasses the lengthy self-development and brand-building phases, directly entering the high-end intelligent electric vehicle market through a "blitzkrieg" approach.

This represents a trade-off: exchanging market autonomy for development efficiency.

The results are undeniably successful. Without Huawei, Seres might still be struggling through the transformation pains of traditional automakers, unable to achieve its current market position and revenue scale so quickly. Huawei's technology and brand are the fundamental reasons Seres can command high prices and achieve high gross margins.

However, the flip side of this model is the solidification of profit structure and partial surrender of development autonomy.

From the outset, the value contributions and benefit-sharing framework between the two parties were largely locked in. Seres earns manufacturing profits, while Huawei gains technology premiums and market realization. As sales volume expands, the overall pie grows, but the proportion of the pie divided remains fundamentally unchanged. This explains why Seres maintains high gross margins but struggles to boost net profit margins.

More importantly, this model partially "outsources" Seres' long-term capability building. Core elements such as intelligent driving R&D, brand positioning, and direct user engagement channels—the cornerstones of future automotive industry competitiveness—are not fully controlled by Seres.

As Huawei's "Harmony Intelligent Mobility" alliance expands to include more "brands," how Seres maintains its uniqueness and priority becomes a practical challenge.

Thus, Seres does not face a simple question of a good or bad model. Instead, it confronts the challenge of evolving from a "phase-specific successful model" to a "sustainable growth model."

III. The Path of Self-Validation and the Possibility of Valuation Reconstruction

Understanding the starting point and constraints clarifies the internal logic behind all of Seres' recent actions. Since 2025, Seres' initiatives have aimed to maintain the alliance's existing strengths while strategically filling capability gaps, converting some external dependencies into internal strengths. In other words, internalizing its market insights into new operational philosophies.

In 2025, Seres' R&D investment surged to RMB 12.51 billion, up 77.4% year-on-year, with R&D personnel increasing by over 2,800.

The direction of this massive investment is noteworthy. Seres is clearly not competing head-on with Huawei but is conducting deeper integration and more scenario-specific optimizations atop Huawei's technological foundation. It is also establishing its own technological reserves and voice in potential "hard tech" areas such as three-electric systems, vehicle architectures, and materials engineering—as well as niche segments not fully covered by Huawei's ecosystem (e.g., specific-scenario robots). This is akin to "renting a brain" while striving to build its own muscles.

Second, Seres recently established a venture capital platform with RMB 500 million in registered capital using its own funds. For industrial capital, investment goals extend beyond financial returns. It serves as an efficient radar and outpost. Through investments, Seres can closely track innovations in AI, robotics, semiconductors, new energy, and other frontier fields, forming synergies with portfolio companies and even incubating seeds for future business transformations—much like how Shunwei Capital's investments empower Xiaomi's ecosystem.

Finally, before Huawei fully deploys its global automotive business, Seres has already elevated overseas expansion to a strategic priority. Premium markets in Europe and the Middle East offer a rare "testing ground" for Seres to validate its product definition, brand operations, and channel-building capabilities relatively independent of Huawei's domestic channel support. The experience and organizational capabilities accumulated through this process are invaluable.

All these actions aim for a single goal: increasing Seres' node weight and irreplaceability within the industrial value network. This is the path of self-validation, and future valuation will be its price.

If Seres successfully completes this round of capability internalization, its high-quality manufacturing system, efficient supply chain management, and quality control capabilities can be replicated across other technological routes, helping Seres become a technology application and integrated innovator in specific fields.

If it establishes competitive autonomous solutions in areas like robotics, AI-vehicle fusion scenarios, or "secondary core" technologies such as three-electric systems—and feeds these back into its main automotive business to form a unique "dual-wheel drive"—it will justify a portion of "technology premium" valuation.

Currently, Seres remains in an intermediate state. The market sees its solid foundation as a manufacturing enterprise (preventing valuation collapse) but has not yet seen a sufficiently clear "second growth curve" capable of propelling it into a technology company. However, when the moment of self-validation arrives, combined with the current booming trends across its targeted fields, the inflection point is unlikely to be far off.

-

![]()

Domestic Pioneer: Changjin Photonics, First Listed Company Focused on Special Optical Fibers, Soars Over 15-Fold on STAR Market Debut

-

![]()

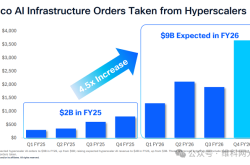

Single-Quarter Orders Break $1 Billion Barrier! Cisco’s Acacia Surfs the AI Boom

-

![]()

Consistently Propelling Technological Progress: Qualcomm’s Xu Hao Elucidates How 6G Trial Frequencies Can Optimize the Balance Between Coverage and Bandwidth

-

![]()

Liushenyu Mine Disaster Drives Industrial Innovation: Pioneering a New Era of Intelligent Mine Safety with Integrated Air-Ground Systems

-

![]()

Ant Group CEO Han Xinyi's Latest Speech: The Emergence of 'Trust Logic' in the AI Era

-

![]()

Demystifying the Rankings: Do High Scores in Robotics Competitions Equate to Real-world Implementation Strength?

-

![]()

Europe's Q1 Smartphone Market Shipments Revealed: Samsung Holds Firm at First Place, Honor Surges Over 60%

-

![]()

Mixed Fortunes: The Ongoing Transformation of the Automotive Industry's Value Landscape