Chinese Home Appliances Should Not Indulge in the False Victory of 'Defeating Foreign Brands'

05/01 2026

05/01 2026

549

549

Advantages Should Not Remain at the 'Manufacturing End'

While we should acknowledge the achievements of Chinese home appliance companies in the global market, we must also not overlook the gap between them and global electronics giants.

Over the past six months, Chinese home appliance companies have undertaken two major integrations. One is that Sony outsourced its home entertainment business, including TVs, projectors, and audio systems, to TCL through a joint venture. The other is that Panasonic handed over the production and sales of TVs in European and North American markets to Skyworth.

This has led to a temporary sense of nostalgia, giving the illusion that two giants have been defeated by Chinese companies and exited the TV market. But it's not just TVs; Chinese home appliance companies have swept the global market in various categories, including refrigerators, air conditioners, and other black and white goods.

As we revel in the sentiment that Chinese home appliances have defeated international giants, we must not overlook the fact that these Japanese and Korean home appliance giants have not 'died or been sold.' On the contrary, companies like Sony, Panasonic, and even earlier ones like Samsung and General Electric are still thriving and continue to lead in high-end technologies such as imaging components and storage.

▌1. Generational Gap

Several Japanese and Korean home appliance giants from the past era are still thriving today.

General Electric in the United States, and Samsung, Sony, and Panasonic in Japan and South Korea, are all reaching new heights in terms of market capitalization and revenue.

Let's take a few examples.

Samsung's revenue in 2025 was KRW 333.6 trillion, equivalent to RMB 1.54 trillion, with a profit of RMB 201.66 billion. This is comparable in scale to Tencent, which had a revenue of RMB 751.8 billion and a net profit of RMB 259.6 billion in 2025. Of course, Tencent's higher profit is due to the higher gross margin of its virtual business.

You might think Samsung's success is due to its strong mobile phone sales, but let's look at Samsung's revenue breakdown:

The DX division - Device Experience division, which includes digital TVs, refrigerators (and other home appliances), smartphones, and network system businesses, had a revenue of approximately RMB 869.35 billion and a profit of RMB 59.444 billion.

The DS division, which mainly includes memory, wafer foundry, and system large-scale integrated circuit businesses, had a revenue of RMB 601.8 billion and a profit of RMB 114.969 billion, with a higher profit margin.

Many might say Samsung's success is mainly due to mobile phone sales, which is not comparable to home appliance companies. But let's look at Samsung's development history. In 1969, Samsung began producing black-and-white TVs, washing machines, and refrigerators. In 1979, Samsung Electronics Industry started mass-producing microwaves. In 1980, Samsung Electronics Industry began producing air conditioners.

Also in 1980, Samsung entered high-end manufacturing by establishing a semiconductor company and renamed it Samsung Electronics in 1984.

That was 40 years ago.

Sony and Panasonic, as two Japanese home appliance giants, have also transformed their businesses.

In fiscal year 2024, Sony's sales revenue was JPY 12,957.1 billion, equivalent to RMB 554 billion, with an operating profit of JPY 1,407.2 billion, equivalent to RMB 60.2 billion. The revenue mainly came from games, music, film and television, entertainment services, and image sensors. TV products were mainly in the entertainment, technology, and services division, with a revenue of RMB 103.2 billion and a profit of RMB 8.177 billion, indicating an extremely low profit margin.

But a decade ago, Sony's revenue structure was completely different. In 2015, the revenue from home entertainment and audio business was RMB 49.6 billion, making it the second-largest business.

Panasonic's revenue in fiscal year 2025 was RMB 362.3 billion, with a profit of RMB 18.3 billion. Among them, the revenue from living appliances was RMB 153.5 billion, with a profit of RMB 5.48 billion. The revenue from automotive systems was RMB 34.5 billion, with a profit of RMB 1.29 billion. The revenue from internet products and services was RMB 57.1 billion, with a profit of RMB 3.3 billion. The revenue from industrial solutions was RMB 46.4 billion, with a profit of RMB 1.85 billion. The revenue from energy, such as batteries and energy storage, was RMB 37.4 billion, with a profit of RMB 5.15 billion.

It can be seen that Panasonic's core business has not yet escaped the realm of home appliances, with an overall gross margin of only 5%.

Sony entered the gaming industry in 1994, while Panasonic shifted towards the B2B sector in 2010.

Looking back at domestic home appliance companies, Midea is doing the best, with a revenue of RMB 456.5 billion and a profit of RMB 43.9 billion in 2025.

Haier Smart Home had a revenue of RMB 302.3 billion and a profit of RMB 19.59 billion. Hisense Home Appliances had a revenue of RMB 87.9 billion and a net profit of RMB 3.19 billion in 2025. Hisense Visual Technology had a revenue of RMB 57.68 billion and a profit of RMB 2.45 billion in 2025. TCL had a revenue of RMB 184.1 billion and a profit of RMB 4.52 billion in 2025. Gree had a revenue of RMB 171.1 billion and a net profit of RMB 29 billion in 2025.

In addition, Midea's market capitalization is RMB 618.5 billion, Haier Smart Home's is RMB 202.9 billion, Hisense Home Appliances' is RMB 32.6 billion, Hisense Visual Technology's is RMB 32.7 billion, Gree's is RMB 222.7 billion, and TCL's is RMB 89.8 billion.

Now let's look at Samsung, Sony, and Panasonic, with market capitalizations of RMB 6,860 billion, RMB 803.3 billion, and RMB 320.8 billion, respectively.

Oh, and speaking of home appliance giants, we must not overlook General Electric. In 2016, GE sold its home appliance business to Haier for USD 5.4 billion. However, the three companies spun off from GE now have market capitalizations of RMB 184.5 billion, RMB 1.95 trillion, and RMB 2.01 trillion, respectively.

To summarize briefly, the earlier a company abandons the home appliance business and enters high-end manufacturing, the higher its current revenue and market capitalization will be.

As Fang Hongbo of Midea said in 2025, the home appliance industry will not give birth to great high-tech companies.

▌2. Advantages Should Not Remain at the 'Manufacturing End'

Of course, we must still acknowledge the achievements of Chinese home appliances in recent years.

In recent years, whether in the black or white goods sector, Chinese home appliances have captured a leading global market share. Haier leads globally in refrigerator and washing machine businesses. Hisense and TCL are competing for the second position in the global TV business. Midea's overseas revenue is close to RMB 200 billion.

Many have also noticed that in overseas mainstream markets, refrigerators and washing machines are all Chinese brands. This is different from the 'Made in China' label a decade ago; Chinese home appliances have moved from OEM to the brand level.

Moreover, some well-known Japanese and Korean electronics brands have indeed been defeated and acquired by Chinese home appliances, such as Toshiba being acquired by Hisense. Haier has acquired countless home appliance brands, including General Electric, Sanyo, and Fisher & Paykel.

But the advantage of Chinese home appliances still lies in manufacturing.

For example, Haier has 173 global manufacturing centers, but 144 are in China. Furthermore, according to its official website, the manufacturing plants in Italy and Turkey do not produce large items like refrigerators and TVs.

From a broader perspective, according to data released by the General Administration of Customs of China, the cumulative export volume of Chinese home appliances in 2024 reached a staggering 4.48 billion units. Additionally, China's domestic home appliance production currently accounts for 56% of the global total.

The core manufacturing chain is still within China.

Moreover, a portion of the overseas business of Chinese home appliance companies is actually OEM. For example, Midea's financial report mentions that 45% of its overseas revenue comes from OEM.

Chinese home appliance companies still have a gap to bridge in the two high-premium areas of technology and branding.

The current stage of Chinese home appliance companies is relatively close to Panasonic's development model.

Half of Panasonic's revenue comes from home appliances, and the other half comes from energy, internet products and services, and industrial solutions.

Since 2020, Midea has explicitly shifted towards To B services. Currently, the revenue from building technologies, industrial technologies, and other divisions, including logistics and robotics, accounts for 30% of its total revenue.

Haier Group, in addition to Smart Home, also has businesses in health and robotics.

All companies are seeking a second growth curve, or even a second life. From the development paths of Panasonic, Sony, and Samsung, this process basically starts from the advantages in manufacturing, gradually shifts from the C-end to the B-end, and then to underlying components.

Midea and Haier are following exactly this development path.

In addition, TCL and Hisense are expanding in the display business. TCL has grown its OLED panel business through CSOT, while Hisense has acquired Unilumin Group and developed Hisense chips to attempt high-end RGB-Mini LED.

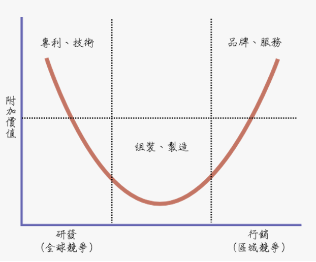

▌3. Behind 'Aluminum Replacing Copper,' Still Standing at the Bottom of the Smiling Curve

The recent hot topic in the home appliance industry is 'aluminum replacing copper,' which involves multiple parties and various influencing factors.

However, the core reason why the 'aluminum replacing copper' incident occurred is that Chinese home appliance companies are still standing in the middle part of the industry's smiling curve, unable to access the high profits at both ends.

It can be seen that the most profitable parts of an industry are either based on core R&D of basic technologies, creating barriers through patents and technology, or generating high premiums through branding and services. We must ask ourselves, have Chinese home appliances truly broken free from the assembly and manufacturing link in the global market?

When new brands like Xiaomi enter the air conditioner and TV industries with low prices, and when leading air conditioner companies are still preoccupied with the cost of basic raw materials, how can they possibly reach the high-premium ends?

Of course, some leading companies have already realized this issue.

Fang Hongbo of Midea last year declared that the home appliance industry cannot give birth to great high-tech companies. Subsequently, Wang Jianguo, Vice President of Midea, revealed that the company plans to invest at least RMB 50 billion in R&D funds over the next three years to layout AI large models, new energy, robotics, embodied intelligence, and other cutting-edge fields.

Looking at the historical transformations of companies like Samsung, Sony, and General Electric, there is always a critical period when they can enter specific fields relatively early, such as Samsung's semiconductor industry, Sony's gaming industry, or General Electric's opportunities in the aviation sector.

These fields overlap with their original businesses, allowing for a natural transition, and they have advantages in technology and market reserves during the early stages of the industry.

From this perspective, over the past and next decade, there have been or will be multiple opportunities for these home appliance companies.

For example, new energy vehicles. Home appliance companies are naturally skilled at making 'refrigerators, TVs, and large sofas.' All they need to do is move these appliances from the living room into the car. Skyworth is one of the home appliance companies that has entered the new energy vehicle sector.

Midea acquired Yunnan Bus Factory, Yunnan Aerospace Shenzhou Automobile, and Hunan Sanxiang Bus in 2003 but later sold them. In 2020, Midea acquired Hiconics Drive, this time focusing on businesses such as new energy vehicle powertrains and motor controllers.

Of course, there was also a home appliance brand that once announced its intention to build cars, which is Dyson. However, Dyson later abandoned the plan, and since it is not a domestic brand, we will not discuss it further.

Another opportunity for home appliance companies could be robotics. The manufacturing processes and service targets of home appliance companies involve a large number of robotics scenarios. At the same time, servo motors, reducers, and controllers are all areas where home appliance companies excel.

Another possibility is home energy. For example, Tesla's Powerwall is a similar product. Home appliances are significant consumers of home energy, so combining energy with home appliances could also be an advantage for home appliance companies.

There could also be opportunities in chips, liquid cooling, and other related products. Some companies are already exploring these areas, while others have tried and given up.

In short, focusing on technological innovation is more promising than getting caught up in the 'aluminum replacing copper' trend.

- End --

-

![]()

From Philosophical Concept to Technological Concept, and Then to Economic Concept: The Past and Present of Token

-

![]()

When DeepSeekV4 and Meituan LongCat Simultaneously ‘Surpass One Trillion Parameters,’ What Signals Are Being Sent?

-

![]()

Chinese Home Appliances Should Not Indulge in the False Victory of 'Defeating Foreign Brands'

-

![]()

2026 Beijing International Auto Show: Navigating the Future of Smart Driving

-

![]()

The Fan Economy: A Lucrative Field, Yet AI Artists Struggle to Gain Fans

-

![]()

Now, Luxshare Precision no longer wants to limit itself to contract manufacturing for Apple.

-

![]()

Global CPU Giant Launches Potent Surprise Offensive, Introducing New AI Logic Core

-

![]()

China's Optical Fiber Boom