16 consecutive trading limits, Huawei brings another speculative stock soaring

09/20 2024

09/20 2024

789

789

Speculative stocks emerge in a weak market, and this year is no exception.

Wanfeng Auto Wheel in the first quarter and Zhengdan Chemical in the second quarter both became the top-performing stocks of the year.

Since August, it's Shenzhen Huaqiang's turn, with 16 consecutive trading limits in 17 days, just one step away from becoming the best-performing stock of the year.

[Speculative Stock Reappears]

The outbreak of speculative stocks is inseparable from hot topics. Wanfeng Auto Wheel capitalized on the boom in the low-altitude economy, Zhengdan Chemical benefited from the surge in TMA prices, and this time, Shenzhen Huaqiang rode on Huawei Hisilicon's coattails.

At the end of July this year, some media reported that Huawei Hisilicon would hold its first Connectivity Conference on September 9, during which it would launch multiple Hisilicon chips covering various application scenarios such as audio-video, HarmonyOS, and Xingshan.

As Huawei's chip company, Hisilicon fell into a trough due to US sanctions a few years ago. Its announcement of the Connectivity Conference naturally attracted significant attention.

Previously released operating results showed that Huawei Hisilicon's business fully resumed in 2023.

In the fourth quarter of 2023, Hisilicon shipped 6.8 million chips, a year-on-year increase of 5,121%, with revenue soaring 24,471% for the quarter. In the first quarter of this year, Huawei Hisilicon sold over 8 million chips, returning to the top five globally.

Relying on its fully independently developed advanced chips like Kirin, Kunpeng, and Ascend, Hisilicon not only regained its position at the center of the global chip industry but also drove a comprehensive recovery in Huawei's performance.

In 2023, Huawei's revenue reached 704.2 billion yuan, up 9.63% year-on-year, marking the largest annual increase since 2019, with a net profit of 87 billion yuan, up 144.5% year-on-year. In the first half of this year, Huawei's revenue growth continued to accelerate, with revenue reaching 417.5 billion yuan, up 34.3% year-on-year, and net profit of approximately 55.11 billion yuan, up 18.2% year-on-year.

There are also market rumors that Hisilicon may eventually become independent from Huawei, similar to Huawei's Intelligent Automotive Solutions BU, becoming a global supplier like Qualcomm and NVIDIA. This suggests that Hisilicon's chip research and development and mass production capabilities may see unexpected progress.

As Huawei Hisilicon gains momentum, the market naturally seeks out concept stocks to speculate on, and Shenzhen Huaqiang, located in the same city as Hisilicon, has become the "chosen one."

Shenzhen Huaqiang is one of Huawei Hisilicon's largest agents, representing products such as smart TV chips, display driver chips, and AI chips, making it a genuine Hisilicon concept stock.

Meanwhile, the company promptly responded to the hot topic, stating that as Hisilicon continues to launch new products, it will intensify R&D and promotion efforts for Hisilicon product application solutions to facilitate market expansion.

This statement further piqued market interest.

Shenzhen Huaqiang's unique shareholding structure also makes it conducive to becoming a speculative stock.

According to data, Shenzhen Huaqiang's total share capital exceeds 1 billion shares, but 740 million shares are held by the controlling shareholder and its concerted parties, leaving only around 300 million shares in actual circulation, with a market value of less than 3 billion yuan before the rally began. ▲Source: iFinD

▲Source: iFinD

In terms of short-term momentum, Shenzhen Huaqiang is indeed unparalleled among Hisilicon concept stocks, but its long-term fundamentals paint a different picture.[Quality Assessment]

Shenzhen Huaqiang's primary business revolves around electronic components, with three major segments: authorized distribution of electronic components, the industrial internet for electronic components, and physical trading markets for electronic components and electronic terminal products.

Electronic component distribution is the company's most critical revenue source, and representing Huawei Hisilicon's chips falls under this segment. In 2023, Shenzhen Huaqiang's electronic component distribution revenue reached 18.018 billion yuan, accounting for 87.49% of total revenue, making it the leader in China's electronic component distribution sector.

As a heavily speculated Hisilicon concept stock, Shenzhen Huaqiang has not disclosed its business data related to Huawei Hisilicon. However, changes in past performance to some extent reveal the impact of Hisilicon on the company.

Shenzhen Huaqiang became a Hisilicon distributor in 2017 through the acquisition of Qinuo Technology. Although the company's overall revenue has doubled over the past six years, its net profit has changed little, suggesting that being a Hisilicon distributor has not significantly increased Shenzhen Huaqiang's earnings.

Starting from the first quarter of 2023, Shenzhen Huaqiang's net profit has declined for six consecutive quarters, with the last four quarters even experiencing revenue growth without corresponding profit growth. In the second quarter of this year, Shenzhen Huaqiang generated revenue of 5.921 billion yuan, up 22.97% year-on-year, with a net profit attributable to shareholders of 119 million yuan, down 15.79% year-on-year.

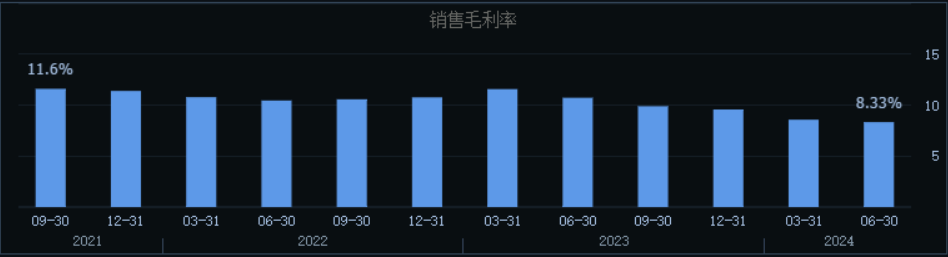

Perhaps due to Hisilicon's dominant position eroding the company's bargaining power, Shenzhen Huaqiang's gross margin for electronic component distribution fell sharply from 11.59% to 6.61%, dragging down the company's profitability. ▲Source: iFinD

▲Source: iFinD

Expanding into new Hisilicon businesses in the future will require significant capital, but the support Shenzhen Huaqiang can receive from its backers is limited.

The company's controlling shareholder, Huaqiang Group, had interest-bearing debt of up to 36.6 billion yuan in 2023, including short-term debt of 23.7 billion yuan, while its monetary funds were only 6.2 billion yuan, leaving a short-term debt funding gap of up to 17.4 billion yuan. To raise funds, the listed company even faces the risk of being drained by its major shareholders.

Therefore, despite the surge in share price, Shenzhen Huaqiang has not forgotten to remind investors of the uncertainties surrounding the progress of Hisilicon's new product launches and the impact on the company's performance, which remains to be observed. The company's recent sharp short-term share price increase, which significantly deviates from market trends, poses a risk of overheated market sentiment.[Lessons from the Past]

Huawei's influence in the capital market speaks for itself, with over 800 A-share concept stocks associated with the company. Shenzhen Huaqiang is not the first listed company to see its share price soar by piggybacking on Huawei.

In June 2021, around the launch of Huawei's HarmonyOS, a stock called Runhe Software became a speculative darling, with its share price surging nearly sevenfold in just over two months.

In response to a subsequent inquiry from the Shenzhen Stock Exchange, Runhe Software replied that it was one of the initiating members of OpenHarmony and a co-builder of the HarmonyOS ecosystem, seemingly justifying the surge in its share price.

However, reality was not as optimistic as expected. In 2021, HarmonyOS contributed negligible revenue to Runhe, and in 2022, Runhe's net profit even declined by 40%. The script of a turnaround fueled by HarmonyOS did not materialize, and the share price plummeted by nearly 60% from its peak.[Future Outlook]

On August 29, 2023, the day Huawei launched the Mate60 series, another speculative stock, Jierong Technology, began to soar. In less than a month, Jierong Technology racked up 16 consecutive trading limits on the back of being a Mate60 supplier, with its share price surging more than fivefold.

The market's focus on Jierong at the time was partly due to its low market capitalization and partly because Huawei had once been Jierong's largest customer, contributing nearly 50% of its revenue.

In reality, however, Huawei became Jierong's largest customer nine years ago, and its revenue contribution has since dwindled to below 10%. In 2021, 2022, and the first half of 2023, Huawei accounted for 0.46%, 3.48%, and 3.70% of Jierong's revenue, respectively.

Speculative market maneuvers often come and go quickly. After just one month of gains, Jierong's share price began to decline continuously and is now down more than 60% from its peak.

Similarly, Shenzhen Huaqiang's sudden surge on the back of Hisilicon hype lacks a solid long-term foundation.

Historical experience in the global industrial economy shows that the long-term beneficiaries of a hardware giant's growth and expansion are undoubtedly upstream component suppliers, not downstream product agents. This trend has been consistent from the early Apple supply chain to more recent examples like Tesla and NVIDIA.

For superbrands, agents are unlikely to dominate, and they may eventually be replaced by the brand's own distribution channels.

From this perspective, as Huawei Hisilicon grows, the true beneficiaries in the A-share market are upstream suppliers rather than downstream agents. Shenzhen Huaqiang's future performance is unlikely to mirror the rapid growth seen in leading suppliers like Luxshare Precision or NVIDIA supply chain leaders like InnoLight Network Systems.[Risks and Challenges]

Apart from the risk of share price adjustments due to easily disprovable performance claims, the risk of selling by controlling shareholders cannot be ignored.

Public data shows that of the 740 million shares held by Shenzhen Huaqiang's controlling shareholder, 330 million shares are pledged as collateral for exchangeable bonds. Currently, these bonds are in the conversion period, and the surging share price of Shenzhen Huaqiang is significantly higher than the conversion price. If these shares enter the secondary market through conversion for sale, they will undoubtedly have a significant impact on the share price.

On September 9, the rumored Huawei Hisilicon Connectivity Conference failed to make any splash online, and Shenzhen Huaqiang's share price opened high but closed low, falling by the daily limit for two consecutive days.

Such speculative sentiment comes and goes quickly. After the event-driven positive factors are realized, Shenzhen Huaqiang's future share price will likely revert to being driven by its performance.

Disclaimer

The content related to listed companies in this article is based on the author's personal analysis and judgment of information publicly disclosed by the companies in accordance with legal requirements (including but not limited to interim announcements, periodic reports, and official interaction platforms). The information or opinions contained herein do not constitute any investment or other business advice. Market Value Observation shall not be held responsible for any actions taken as a result of adopting this article.

–END–

-

![]()

Over 50% of Revenue Hinges on Yutong Optics! This Optical Equipment Manufacturer is Charging Towards an IPO

-

![]()

YOCO Optics Finalizes Industrial and Commercial Registration Update Post 160 Million Yuan Investment in Jiangfeng Biology, Securing 20% Stake to Emerge as Second-Largest Shareholder!

-

![]()

Google Market Value Plummets by $1.5 Trillion Overnight Following the Loss of Two Key Figures

-

![]()

Put an End to the EV 'Weight Gain Race'! Can Your Car Still Be Driven Under the New National Standards?

-

![]()

In 2026, 'AI Upstarts' Collectively Bet on World Models

-

![]()

【OFweek Weike Cup】Phoenix Optics Officially Participates in the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Ford Ditches Mach-E: Will Its Billion-Dollar Electrification Drive Have to Start All Over Again?

-

![]()

【OFweek Weike Cup】Shuangli Hepu Officially Participates in the 2026 High-Growth Enterprise Award in the Optical Industry