European Auto Market | Italy June 2025: Market Decline Amid Chinese Brand Growth

07/07 2025

07/07 2025

854

854

In June 2025, the Italian new car market experienced a sharp 17.4% year-on-year decline, indicating an overall contraction. Private consumption weakened significantly, traditional fuel vehicles continued to lose ground, and plug-in hybrids grew robustly.

Amidst the market downturn, Chinese automakers demonstrated robust growth, with BYD, MG, Omoda+Jaecoo, and JETOUR swiftly expanding their market share, signaling a new dawn for Chinese manufacturing in the Italian market.

01 Italian Market Overview and Competitive Dynamics

In June, new car registrations in Italy totaled 132,191 units, a 17.4% decrease from the previous year, marking another significant decline since the start of 2025. This brought the first-half sales figure to 854,690 units, a 3.6% year-on-year drop and more than 220,000 units below the pre-pandemic levels of 2019.

Consumer behavior diverged, with private car purchases plummeting 29.5% year-on-year, and their market share declining from 59.5% in 2024 to 50.9%, reflecting waning consumer confidence. This decline was partially offset by the leasing market, with short-term leasing surging 36.6% and long-term leasing increasing by 4%. Together, they accounted for nearly 30% of the market, indicating that corporations and leasing companies have become the primary sales drivers.

From a powertrain perspective, pure internal combustion engine vehicles continued to decline:

◎ Gasoline models accounted for 23.6% of June sales, down 26.5% year-on-year.

◎ Diesel models fell to 10%, a steep 35.8% decrease.

◎ LPG models accounted for 9.6%, down 21.5%.

◎ Hybrid models remained the market mainstream with a 43.6% share, but mild and full hybrids declined by 8.1% and 4.7% respectively.

◎ Plug-in hybrids were a bright spot, with sales surging nearly 70% year-on-year to a 7.2% market share.

◎ Battery electric vehicles (BEVs), once highly anticipated, saw a significant 40.7% decline, with only 7,953 units sold and a 6% market share.

This may be attributed to adjustments in incentive policies and their implementation pace, though their cumulative share for the first half of the year remained higher than the same period last year.

In terms of brand competition:

◎ Fiat retained its sales lead despite a 34.8% year-on-year decline in June, with its market share dropping to 8.3%. Its main model, the Panda, sold 7,488 units in a single month, accounting for 68% of Fiat's sales.

◎ Volkswagen and Toyota remained stable in the top three, with sales of 9,619 units and 10,064 units, respectively.

◎ Dacia ranked fourth despite a 32.6% year-on-year decline, thanks to the success of the Duster and Sandero, becoming the only brand with two models in the top three in June.

◎ Renault, BMW, Audi, and Peugeot experienced fluctuating rankings, indicating intense competition.

◎ Tesla saw a steep 66% decline, selling only 1,697 units and falling out of the mainstream.

From the model rankings:

◎ The Fiat Panda retained its top spot, but its market share fell from 10% at the beginning of the year to 5.7% in June.

◎ The Dacia Duster returned to third place with a 19.5% increase, becoming the brand's sales leader.

◎ Models like the Renault Clio and Jeep Avenger experienced double-digit declines.

◎ Notable performers included the Ford Puma with a 26.2% year-on-year increase, the BMW X1 with a 28.1% increase, and the Peugeot 208 with a 12.1% increase.

◎ The Chinese brand MG ZS ranked ninth with 2,522 units sold, a slight 5% year-on-year decrease, but remaining in the top ten, demonstrating its strong product appeal.

02 Rapid Ascent of Chinese Brands: Sales and Model Analysis

Despite the Italian market's downturn, Chinese brands have shown remarkable growth.

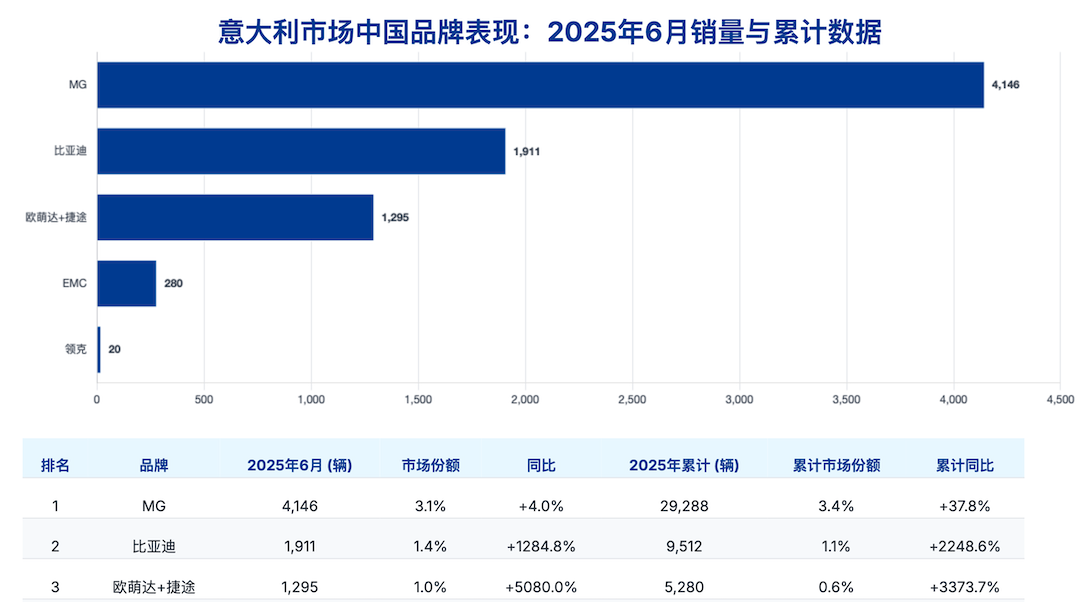

◎ BYD sold 1,911 units in June, a staggering 1284.8% year-on-year increase. Cumulative sales for the first half of 2025 reached 9,512 units, a remarkable 2248.6% increase, positioning BYD in the top 25 sales rankings in Italy for the first time.

◎ MG brand (MG Motor) performed steadily, selling 4,146 units in June, a 4% year-on-year increase. Cumulative sales for the year surpassed 29,000 units, ranking 13th among mainstream brands. Notably, the MG ZS consistently ranks in the top ten model sales, serving as a benchmark for Chinese brands.

◎ The newcomer Omoda+Jaecoo emerged as a significant player, selling 1,295 units in June, a whopping 5080% year-on-year increase. Since the start of the year, it has sold 5,280 units, with a year-on-year growth rate of 3373.7%.

As Chery's new venture in overseas markets, this combination's product design aligns well with European market aesthetics and needs, demonstrating strong market acceptance.

Chinese brand models are predominantly small and compact SUVs, catering to Italian consumers' preferences for urban commuting and fuel economy.

◎ The MG ZS is a prime example, supported by its high cost-effectiveness, straightforward configuration, and reliable after-sales systems.

◎ BYD's product mix is not yet clearly defined, but its surge in sales suggests that models like the Yuan PLUS and Dolphin are significant contributors.

Despite Tesla's decline, the surge in plug-in hybrid sales has created policy space for Chinese brands. BYD and Chery are gradually introducing plug-in hybrid technology into the mainstream European market. With continued improvement in incentive policies, their growth potential should not be underestimated.

Summary

The Italian auto market underwent significant adjustments in mid-2025, with traditional brands and technology systems facing challenges, and the structure of new energy vehicles evolving. Chinese brands have not only achieved rapid market share growth but have also matured in terms of product strength, technology adaptation, and localized deployment. BYD and MG enjoy stable sales support, while Omoda+Jaecoo and JETOUR have opened new avenues, indicating that Chinese automakers have transitioned from testing the waters to systematic operations in the European market.

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’