From China's Richest Man to Institutional Target Price Cuts: Xiaomi's Year of Turmoil

03/05 2026

03/05 2026

691

691

Source: Shenlan Finance

Are Institutions Collectively Bearish on Xiaomi?

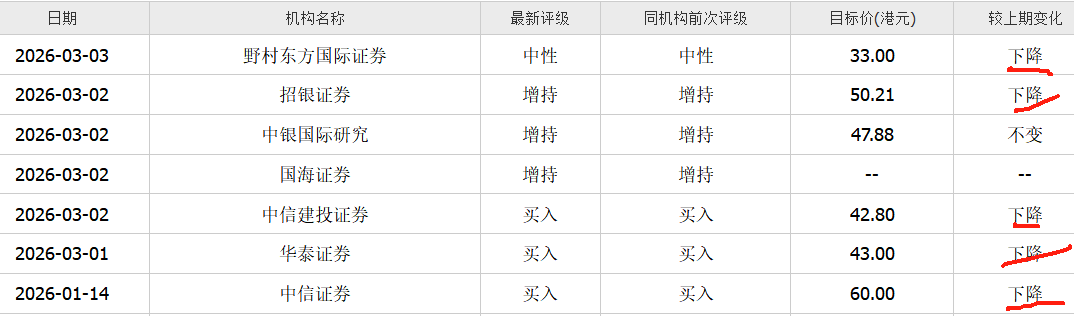

Since March, leading global and domestic financial institutions—including Nomura Orient International, CMB International, CSC Financial, and Huatai Securities—have all issued reports downgrading their target prices for Xiaomi Group, with reductions reaching as high as 46%!

Institutions are primarily concerned that Xiaomi's smartphone business will face mounting pressure from surging upstream memory costs by 2026, with both shipment volumes and profit margins under threat. Meanwhile, Xiaomi Auto and AIoT businesses are also expected to face significant challenges.

On the secondary market, Xiaomi Group's stock performance has been sluggish, with a maximum retracement of nearly 50% over the past year. On March 2-3, the stock plunged for two consecutive days, with cumulative losses exceeding 9.7%. Despite launching a HK$10 billion share buyback to stabilize its market value, Xiaomi has been unable to reverse the downward trend, leaving investors who participated in the high-priced rights issue facing paper losses of nearly 40%.

A year ago, Lei Jun briefly claimed the top spot on China's richest list amid soaring Xiaomi stock prices; a year later, the stock has undergone a dramatic reversal. This sharp contrast highlights a shift in market sentiment from last year's optimism to current caution—even pessimism.

The former trillion-dollar giant now faces multiple challenges.

1

Multiple Institutions Downgrade Target Prices

Since March, major financial institutions—including Nomura Orient International Securities, CMB International Securities, BOC International Research, Haihong Securities, CSC Financial Securities, Huatai Securities, JPMorgan Chase, and Jefferies—have all released updated reports, with the vast majority lowering their target prices for Xiaomi Group.

On March 4, Jefferies cut Xiaomi Group's target price from HK$43.36 to HK$30.45 (a 30% reduction), citing expectations that Xiaomi's Q4 2025 results may fall short across all three major business segments.

On March 3, JPMorgan Chase noted in a report that despite Xiaomi Group's recent underperformance relative to the broader market, gross margin pressures will continue to weigh on profitability in the coming quarters, putting downward pressure on the stock price. JPMorgan lowered Xiaomi Group's EPS forecasts for 2026-2027 by 16%, reduced the target price to HK$35, and maintained a "Neutral" rating.

Also on March 3, Nomura slashed Xiaomi Group's target price from HK$61 to HK$33 (a 46% reduction) while maintaining a "Neutral" rating. The bank warned that if overall cost pressures for Xiaomi smartphones persist throughout the year, shipment volumes could decline by about 20% year-on-year. Additionally, the bank expressed concerns about Xiaomi's electric vehicle business due to potentially weaker-than-expected demand and profitability.

According to Tonghuashun data, since March, institutions including Nomura Orient International, CMB International, CSC Financial, and Huatai have all recently lowered their target prices for Xiaomi Group.

Possibly impacted by the recent wave of target price reductions from major international institutions, Xiaomi Group's stock fell sharply for two consecutive days on March 2 and 3, with cumulative losses exceeding 9.7%. However, recent declines have been significant across Hang Seng Tech Index component stocks, not just Xiaomi.

Key institutional concerns include:

First, soaring upstream memory prices have triggered cost control pressures. Since last year, DRAM and NAND flash memory prices have surged by 80%-100%. According to South Korean media, to secure memory supply for the iPhone 17 series, Apple has accepted a doubling of Samsung's LPDDR5X chip prices. With this precedent, manufacturers like Xiaomi may find it unavoidable to accept price hikes.

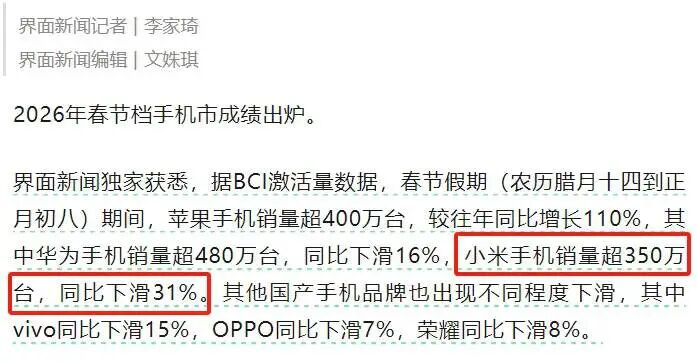

Second, the high-end smartphone market has been impacted by price wars from Apple, Huawei, and others, making it difficult for Xiaomi to fully pass on cost pressures to consumers. According to "Jiemian News," based on BCI activation data, Xiaomi's smartphone sales exceeded 3.5 million units during the Spring Festival period, down 31% year-on-year.

Additionally, according to preliminary data from IDC Consulting's latest "Global Quarterly Mobile Phone Tracker" report, in Q4 2025, Xiaomi shipped 10 million units, down 18% year-on-year—the largest decline among the top 6 vendors. Therefore, JPMorgan Chase expects Xiaomi's smartphone gross margin may fall to a historical low of 8%-9% in Q4 2025.

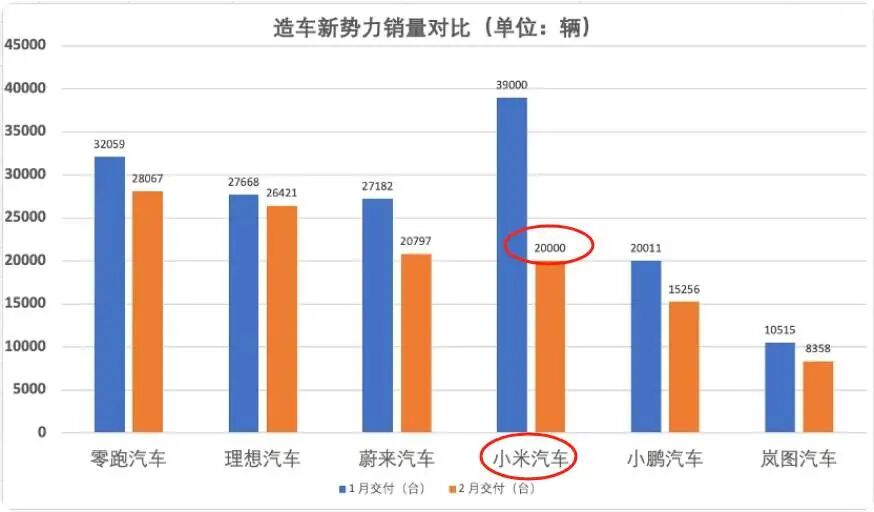

Third, emerging business growth falling short of expectations has heightened market concerns. Institutions believe that after rapid growth in 2025, Xiaomi's auto business showed signs of fatigue in early 2026. Data shows that Xiaomi Auto delivered 20,000 units in February, down 51% month-on-month from 39,000 units in January. However, February was significantly affected by the Spring Festival holiday and should be viewed more objectively.

It should be noted that an institution lowering a company's target stock price does not necessarily indicate "bearishness" but is primarily a necessary revision based on new information. If institutions fail to adjust, it could lead to market distortions, and investors should view this objectively.

2

HK$10 Billion Buyback Fails to Stem Decline

Notably, on March 27, 2025, Xiaomi Group successfully completed a share placement raising approximately HK$42.5 billion, with each share subscribed at HK$53.25. This placement adopted a "top-up" model, where major shareholder Lei Jun first sold existing shares, and the company then issued new shares to the major shareholder at the same price to raise funds.

After the placement and subscription were completed, Lei Jun's shareholding ratio became 23.4%. Placees hold 800 million shares, accounting for 3.1% of ownership; other shareholders' ownership became 73.6%. However, the specific names of the placees and their respective subscription amounts were not disclosed.

In hindsight, Xiaomi secured significant funds while its stock price was at a high.

However, facing stock price pressures, Xiaomi had to initiate a new round of market value maintenance. Shenlan Finance noted that according to data from the Hong Kong Stock Exchange, from September 29, 2025, to March 4, 2026 (104 trading days), Xiaomi Group's stock price plummeted by 41%, but the company conducted share buybacks on 61 trading days during this period, with cumulative repurchases totaling HK$10.19 billion.

Meanwhile, on November 24, 2025, Lei Jun announced that through his wholly-owned Team Guide Limited, he had purchased 2.6 million Class B ordinary shares from the open market at an average price of HK$38.58 per share, spending over HK$100 million. This move was positively interpreted by the market.

(Stock Price)

However, as the company was buying back shares and Lei Jun was increasing his stake, Xiaomi co-founder and Vice Chairman Lin Bin suddenly announced plans to reduce his holdings. According to the announcement, Lin Bin plans to sell shares starting in December 2026 over four years, selling no more than US$500 million worth every 12 months, with cumulative cash-outs not exceeding US$2 billion. The bad news is that Lei Jun's close ally Lin Bin will be reducing his stake this year; the good news is that it won't start until December. However, the market's interpretation leaned "negative," even perceiving it as a "betrayal."

Combined with these factors, Xiaomi's HK$10 billion buyback is merely a drop in the bucket compared to its trillion-dollar market value at that time.

Calculating from last June's peak stock price of HK$61.45 per share and the March 4 closing price of HK$32 per share, Xiaomi Group's stock price has seen a maximum retracement of 48% over the past year, "nearly halving." Based on the placement price of HK$53.25, investors' paper losses have approached 40%.

Now, with international investment banks one after another lowering their target prices, investors may face another difficult period.

3

Xiaomi Faces a Critical Year Ahead

Xiaomi's first major challenge this year is ensuring the successful launch of its next-generation Xiaomi SU7.

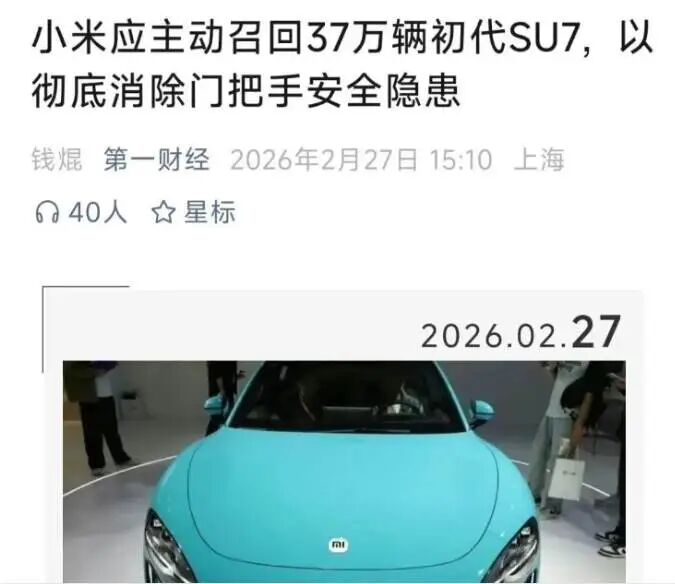

However, controversies surrounding the first-generation SU7 have not ended. Just recently, in October 2025, a review result was released for the collision and fire incident involving a Xiaomi SU7 on Chengdu's Tianfu Avenue—after the collision, the doors could not be opened from the outside due to low-voltage system power loss, resulting in fatalities.

This incident reignited public discussions, with many still calling for a recall of the first-generation SU7. Faced with 370,000 existing first-generation Xiaomi SU7 units, Xiaomi is caught in a dilemma.

To make way for the new model, in early February, Lei Jun directly announced the discontinuation of the first-generation SU7, focusing all efforts on launching the updated SU7 in April.

To promote the updated SU7, on the evening of February 27, Lei Jun's first livestream after the Lunar New Year holiday detailed the safety advantages of the updated model, including: upgraded high-strength steel and aluminum alloy body materials, standard 9 airbags across all models, and upgraded bulletproof coating on the battery bottom. For the controversial door handles, the new model is equipped with multiple power redundancies and ensures mechanical unlocking in case of a collision.

(Image Source: Official Website)

However, there was no direct response during the livestream to calls for a full recall of the first-generation SU7.

Affected by the discontinuation of the first-generation SU7, Xiaomi Auto delivered over 59,000 units in January and February 2026. This performance still represents a nearly 50% year-on-year increase compared to the over 40,000 units delivered in January and February 2025.

In horizontal comparison, Xiaomi Auto's combined deliveries in January and February 2026 are approaching those of Leapmotor, the leader among new EV makers, and surpassing those of the "NIO, XPeng, Li Auto" trio (NIO, XPeng, and Li Auto). From this perspective, Xiaomi Auto's fundamental position remains quite solid.

This year, Xiaomi Auto aims to deliver 550,000 units, up about 34% from 410,000 units in 2025. To achieve this, Xiaomi Auto plans to launch six new models this year, including the SU7 facelift, YU7 Ultra, and the internally codenamed "Kunlun" (YU9) large extended-range SUV, which are worth anticipating.

In smartphones, despite significant pressures this year, Xiaomi continues to drive growth through innovation. Xiaomi Group President Lu Weibing recently publicly stated that the current round of smartphone memory price hikes may persist until the end of 2027. This year, Xiaomi will focus on increasing the proportion of high-end products in overseas sales. More notably, Xiaomi will eventually integrate chips, OS, and self-developed AI large models into a single device, which will be the key to building its future core competitiveness.

4

Conclusion

Despite major institutions expressing concerns for Xiaomi this year, the company's competitive advantages—built through hundreds of billions in annual R&D investment and a massive fan base—remain strong. Its closed-loop capability of "smartphone-auto-home" ecosystem is rare globally. Once Xiaomi achieves breakthroughs in core areas like self-developed chips and AI large models, its market value could quickly return to its peak.

Do you continue to be bullish on Xiaomi?

Shenlan Finance New Media Cluster originated from the Shenlan Finance Journalist Community 15 years ago and is a well-known domestic financial new media outlet. Its accounts focus on China's most valuable companies, cutting-edge industry developments, and emerging regional economies, providing valuable content for investors, corporate executives, and the middle class. Welcome to follow.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?