"Farewell" to Price Wars: Auto Companies Compete with "Financial Cards" of 7-Year Ultra-Long Loans

03/05 2026

03/05 2026

622

622

At the beginning of 2026, the domestic auto market is undergoing a brand-new competitive transformation. The once-dominant direct price wars are gradually fading away, and low-interest auto financing schemes spanning seven years or more, centered around "low down payments, low monthly payments, and long cycles," have become the common choice of over 20 auto companies. From new energy powerhouses like Tesla, Xiaomi, and Li Auto to traditional domestic brands such as BYD and Great Wall Motors, and even joint ventures like Dongfeng Nissan and GAC Honda, all have joined the fray. Some brands have even extended loan terms to eight years and reduced down payments to zero, further lowering the threshold for car purchases.

This trend of ultra-long-term low-interest loans represents not only a marketing adjustment by auto companies in response to the current market environment but also a signal that the auto market is shifting from price competition to financial competition. For budget-constrained consumers with rigid demand ( rigid demand translates to " rigid demand " in Chinese, meaning " rigidity demand" or "essential demand" in English, but for better readability, we use "essential demand"), these low-threshold purchasing methods indeed offer tangible convenience. However, the differences in schemes, cost composition, and property rights rules behind this model also require consumers to conduct a comprehensive assessment based on their own circumstances. Against the backdrop of regulatory authorities continuously standardizing automotive financial service behaviors, ensuring compliance and transparency in auto companies' financial promotions and enabling consumers to understand the core logic of different schemes have become core issues worthy of attention in this wave of car-buying enthusiasm.

▍Diversified Strategies Among Auto Companies, Low-Interest Schemes with Varying Focuses

The industry trend of seven-year low-interest auto financing was initiated by Tesla in January 2026, followed by rapid industry-wide adoption. By late February, over 20 automotive brands had launched related schemes, with significant differences in design based on each company's brand positioning and market strategy. Variations in down payment ratios, annualized interest rates, loan models, and additional conditions require consumers to carefully discern the differences amidst a plethora of promotional information.

Within the new energy vehicle sector, scheme designs exhibit notable divergence. Some brands emphasize transparency and low fees, while others focus on lowering entry barriers to attract consumers.

Tesla's seven-year low-interest scheme adopts a bank mortgage loan model, with a minimum down payment of 15% and an annualized interest rate as low as 0.5%, translating to an approximate annualized percentage rate (APR) of 0.98%. The most notable feature is that vehicle ownership is transferred to the consumer upon delivery, enhancing scheme transparency. NIO, on the other hand, offers an even lower annualized interest rate of 0.49% and explicitly commits to no financial service fees. Consumers can also prepay without incurring penalties, further reducing additional costs associated with car purchases.

In contrast, new energy brands like Xiaomi, XPeng, and Li Auto prioritize lowering entry barriers, with minimum down payments also starting at 15% and annualized interest rates ranging from 1% to 2.5%. However, these schemes generally impose additional conditions such as credit qualification reviews and model restrictions.

Traditional domestic brands have followed suit with flexible scheme designs tailored to different consumer groups. BYD leverages its in-house financial leasing company to operate its seven-year low-interest scheme, aligning its vehicle ownership rules with those of leading new energy brands like Tesla, ensuring clarity in ownership from the outset and minimizing potential disputes. ZEEKR, meanwhile, has introduced a more aggressive scheme in the industry, combining "seven-year zero down payment + interest-free for the first three years" to virtually eliminate upfront financial pressure. However, this scheme comes with more stringent additional conditions, including detailed credit qualification requirements and regulations on vehicle usage and maintenance. Consumers must meet all conditions to enjoy the corresponding financial benefits.

Joint venture brands have chosen ultra-long loan terms as their selling point. Dongfeng Nissan was the first to extend loan terms from seven to eight years, supporting zero down payments and emphasizing "low daily payments." Dongfeng Nissan offers 96-installment financing across its entire lineup, with daily payments as low as 27 yuan, intuitively conveying reduced repayment pressure to consumers. However, these schemes come with relatively high annualized interest rates, reaching up to 4.88%. Behind the seemingly consumer-friendly low daily payments lies increased total interest costs due to the extended loan term.

This limited-time promotional approach indeed helps auto companies quickly boost orders and alleviate current high inventory pressures. However, it may also lead some consumers to make purchasing decisions without fully understanding the information. Nevertheless, it is worth noting that Cheshi Ruijian conducted actual calculations using two popular models on the market, revealing significant differences.

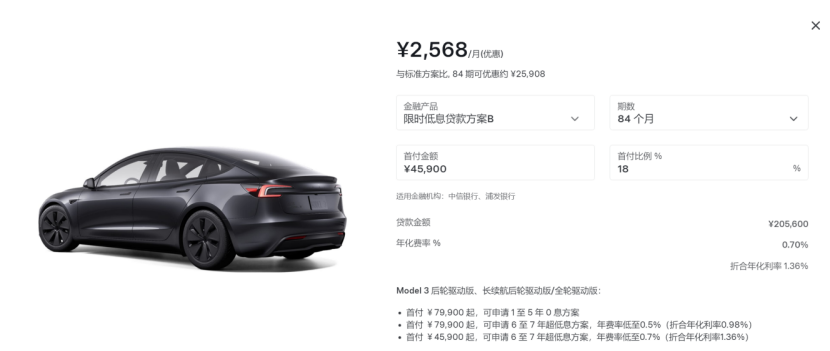

Taking the Tesla Model 3 Rear-Wheel Drive version as an example, with an official guide price of 259,500 yuan, under Tesla's seven-year low-interest scheme with an 18% down payment, the loan amount is 205,600 yuan, and the annualized interest rate is 0.7%. Using an equal principal and interest repayment method, the monthly payment over 84 installments (seven years) is approximately 2,568 yuan, with total interest expenses of around 10,032 yuan.

In contrast, the Dongfeng Nissan Teana HarmonyOS Cockpit Comfort Edition has an official guide price of 129,900 yuan. Under its eight-year zero down payment low-interest scheme, the loan amount is 129,900 yuan, and the annualized interest rate is 4.88%. With equal principal and interest repayment over 96 installments, the monthly payment is approximately 1,650 yuan, with total interest expenses of around 27,386 yuan. The calculation results clearly show that the ultra-long terms and zero down payments offered by joint venture brands result in significantly higher total interest costs compared to new energy brands, leading to substantial differences in consumers' actual car purchase expenses.

▍Core Logic Behind Seven-Year Low-Interest Schemes: Models and Costs

The core differences in seven-year low-interest auto financing schemes are not only reflected in down payments and interest rates but also hidden in the loan models and actual cost compositions, which are often overlooked by ordinary consumers. Currently, ultra-long-term loan schemes on the market mainly fall into two categories: bank mortgage loans and financial leasing. Over 90% of auto companies have chosen the financial leasing model, with only a few brands like Tesla opting for bank mortgage loans. The two models differ fundamentally in terms of ownership, usage rights, and subsequent disposal, directly impacting consumers' car purchasing experience and asset rights.

The rules for bank mortgage loan models are relatively simple. After paying the down payment, consumers apply for a loan from a bank to purchase the vehicle, which is registered under the consumer's name. The vehicle is merely pledged to the bank as collateral for repayment, and ownership is transferred to the individual upon delivery. In this model, consumers have full usage rights to the vehicle and only need to make timely monthly payments during the repayment period. After repaying the loan, they can complete the release of the pledge. Even if repayment delays occur, the bank must go through legal procedures to dispose of the vehicle, ensuring clear legal protection for consumers' rights.

In contrast, the financial leasing model is commonly understood as "lease-to-own." During the lease term, the ownership of the vehicle belongs to the leasing company, and consumers only have usage rights. Although monthly payments are still required, users are essentially signing a long-term lease contract rather than a loan contract. Over the seven-year repayment period, consumers are merely renting the vehicle and are not the owners. In this model, consumers' vehicle usage is subject to certain restrictions, with some schemes requiring maintenance at designated stores. Moreover, vehicles under financial leasing models have a depreciation rate in the second-hand market that is 5%-10% lower than those under conventional loan models. If consumers wish to upgrade their vehicles later, the disposal proceeds will be affected.

Besides the differences in loan models, the actual costs of seven-year low-interest schemes are not limited to surface-level interest expenses. Additional fees and prepayment rules in some schemes can alter the actual car purchase costs. Although some brands have explicitly eliminated financial service fees, under the financial leasing model, many auto companies require consumers to purchase insurance through their dealerships, with insurance types and premium standards determined by the dealerships, leaving consumers without the autonomy to choose more cost-effective insurance plans. Additionally, some schemes impose prepayment penalties, which become hidden car purchase costs.

Furthermore, taking new energy vehicles as an example, given the current iteration speed of intelligent electric vehicles, seven years are sufficient for technological generational shifts. Once technologies like solid-state batteries and advanced autonomous driving are widely implemented, the residual value of existing models may plummet. After three to four years, the market value of the vehicle may fall below the outstanding loan balance, creating an awkward situation for those wishing to upgrade their vehicles.

The reason auto companies are flocking to launch seven-year low-interest auto financing schemes is essentially an inevitable choice to cope with the current market environment. Previously, regulatory authorities halted the disorderly price wars in the automotive industry, as direct price reductions not only triggered dissatisfaction among existing car owners but also led to a decline in vehicle residual values while imposing significant operational pressures on dealerships. The ultra-long-term low-interest approach has become an effective means for auto companies to boost orders in a compliant manner. Some experts suggest that the interest subsidy costs incurred by auto companies are likely to be passed on to consumers through hidden fees, reduced configurations, or compromised service quality, which is why some schemes may appear to offer low interest rates but result in high actual total expenses.

However, this new model of financial competition is not outside regulatory scrutiny. In December 2025, the State Administration for Market Regulation issued the "Compliance Guidelines for Pricing Behavior in the Automotive Industry (Draft for Comment)," emphasizing the need to standardize pricing behavior in automotive sales, financial services, and other sectors. The guidelines clarify rules for clear pricing, requiring auto companies to transparently disclose all information related to car purchase costs, including loan interest rates, repayment methods, and additional conditions, and prohibiting intentional concealment or ambiguous expressions.

Cui Dongshu, Secretary-General of the China Passenger Car Association, also previously stated that the shift from "price competition" to "financial competition" in the auto market is an inevitable trend in industry development. However, this competition must be based on compliance and transparency. If auto companies engage in unclear communication, conceal additional conditions, or transfer costs, they will cross the compliance red line and face penalties from relevant authorities. Currently, some regulatory measures have been implemented to urge auto companies to standardize their financial promotion practices, enabling consumers to have a clearer understanding of the true nature of different schemes.

Layout 丨 Yang Shuo Image Sources: Qianku.com, Tesla, Xiaomi Auto, BYD

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?