Zhipu: Generating 700 Million in Revenue, Incurring 3.2 Billion in Losses? With Grand Aspirations, Focusing on Losses is 'Missing the Forest for the Trees'

04/01 2026

04/01 2026

535

535

A sixfold revenue surge in a single quarter—Zhipu, the darling of capital and a star in the model stock arena during this period, has unveiled its financial results. While its stock price has soared, the performance in the latter half of 2025 appears more subdued. But does it truly matter?

Let's dive straight into the heart of the matter:

I. Revenue Perspective: API Business Hits 250 Million in Annualized Recurring Revenue (ARR) by March—Everything Else Pales in Comparison!

Among China's independent model providers, Zhipu stands out as a purely 'domestic large model' player, with its talent pool backed by universities and a client base primarily consisting of government and state-owned enterprises (B2B).

Local deployments are resource-intensive, and the market has long harbored concerns about the sustainability of project renewals. Prior to the Agent boom, the market was reluctant to assign Zhipu a significant valuation premium.

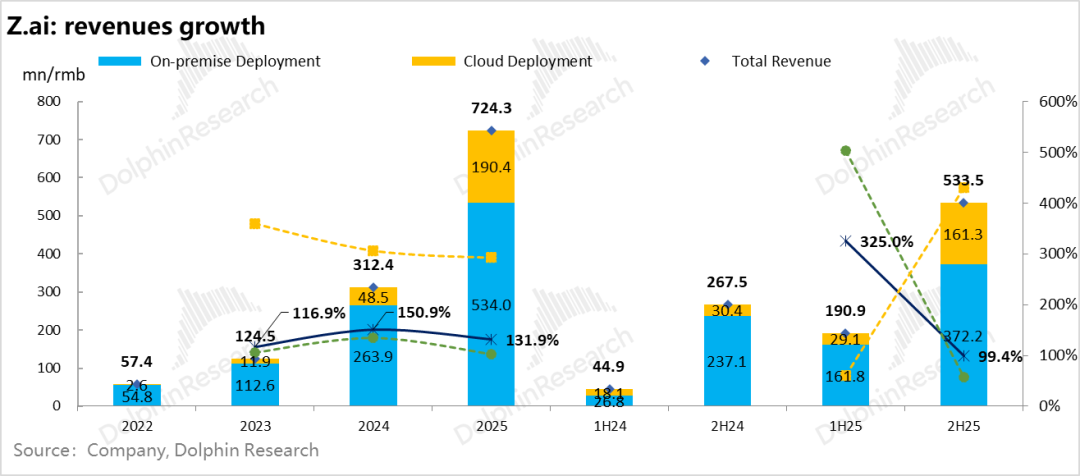

1) Revenue Growth Slows, but Open Platform Business Picks Up: Total revenue in 2025 reached 720 million, marking a nearly 132% year-over-year increase—still robust but slower than the previous year's 160% growth.

With first-half results already disclosed, the focus shifts to the latter half: Revenue hit 530 million, up just 99% year-over-year, indicating a more pronounced slowdown trend.

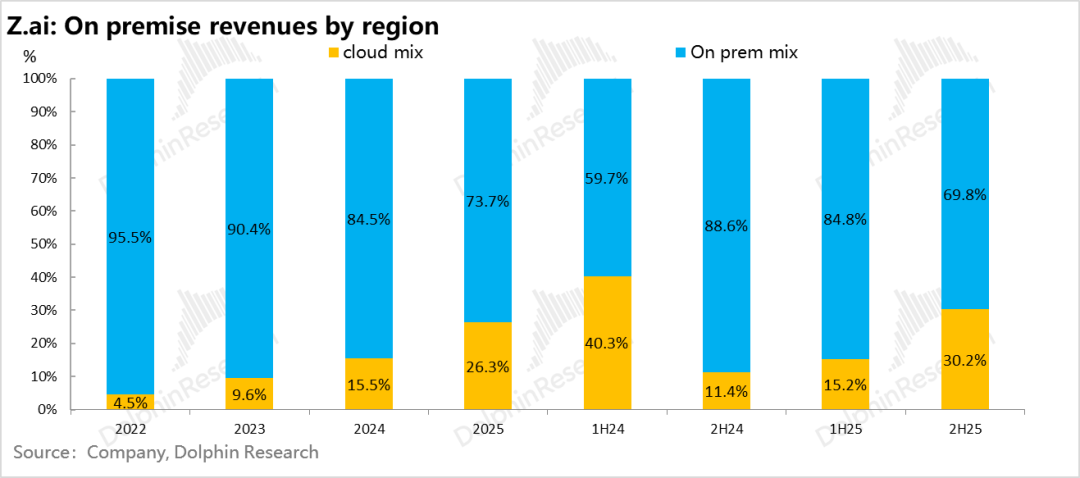

The primary reason for the slowdown confirms previous market apprehensions—the local deployment business, accounting for over 80% of revenue, saw growth decelerate to 57% in the latter half of 2025, reaching only 370 million, with its share slipping to 70%.

In stark contrast, cloud-based deployments such as API interfaces and open platforms, which the market truly favors, surged 430% year-over-year in the latter half, reaching 160 million. The full-year API-related business hit 190 million, nearly on par with MiniMax's 180 million. Moreover, in terms of growth trajectory, Zhipu's nearly 300% annual growth outpaces MiniMax's 200%, showcasing greater explosiveness.

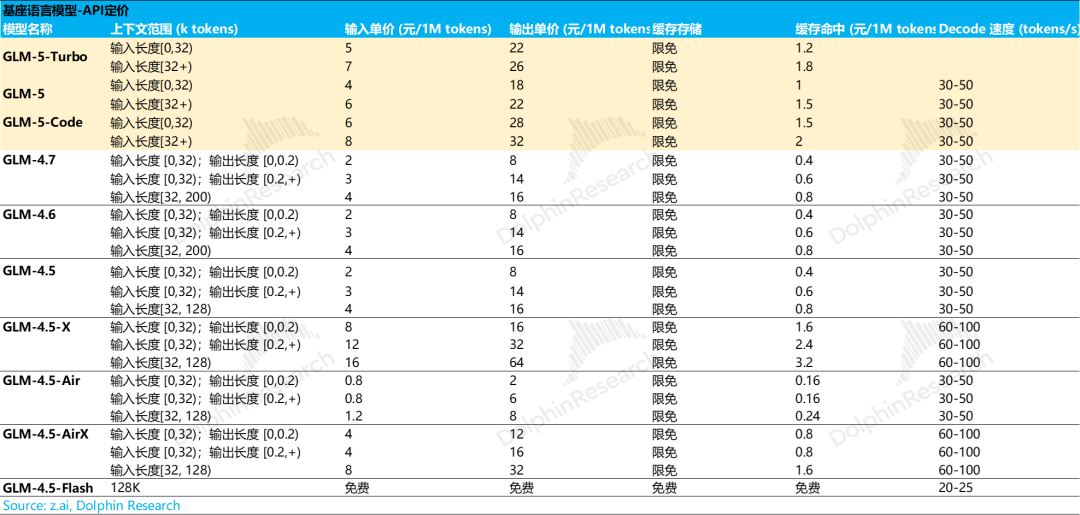

This is precisely why the market is willing to assign Zhipu a higher valuation: While the API and open platform businesses for models have faced intense competition and aggressive pricing, leading to poor gross margin performance, the standardized, light-delivery revenue model becomes highly scalable once it gains momentum. Especially after the company raised API prices by 83% in a single quarter in February, gross margin becomes less of a critical factor.

Revenue growth serves as the core indicator of Token consumption and model popularity: With GLM 5 not yet released in the latter half, the open platform's rapid growth indeed suggests Zhipu's model has 'real substance.'

Since the Spring Festival this year, Zhipu has rapidly iterated its model three times:

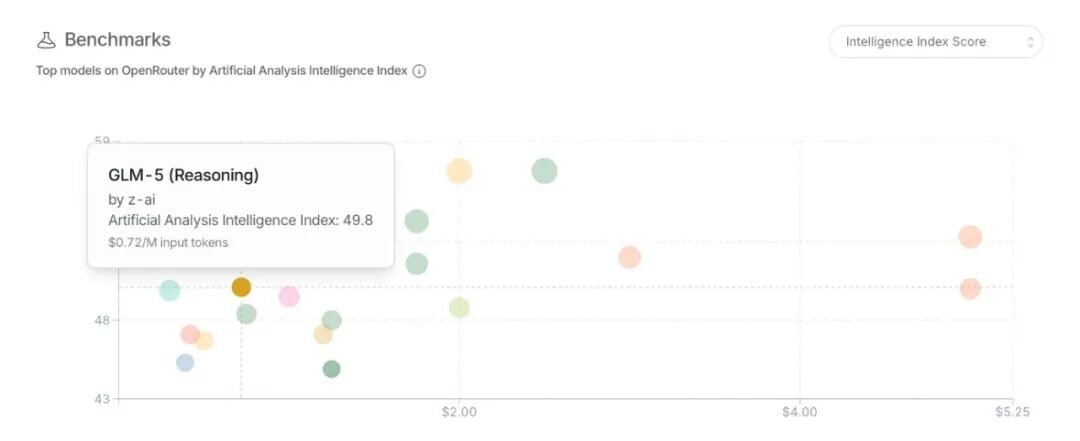

a) On February 11, GLM-5 was released, ranking first in open-source intelligence on the Artificial Intelligence index at launch;

b) On March 15-16, just a month later, it launched the specialized GLM-5-Turbo model for the viral Lobster Agent, focusing on tool invocation, multi-step task execution, complex instruction decomposition, and multi-agent collaboration workflows.

c) On March 27, GLM-5.1, targeting programming, was released as a post-training optimized version of GLM-5 for all Coding Plan users.

Alongside the GLM-5 release, Zhipu announced price hikes for its large model—raising subscription and API prices across the board. API prices rose again after Turbo's launch, with an 83% increase within a single quarter.

On the application front, with Openclaw gaining popularity in China but facing official data security concerns, Zhipu seized the opportunity to launch a domestic alternative—AutoClaw—featuring easy installation, one-click deployment, and monthly packages of 39 yuan for 35 million tokens or 99 yuan for 100 million tokens.

The Agent boom and rising AI penetration in IT have driven the company's stock price up 3.5 times since February, with the core driver being a shift in pricing logic and business model:

Backed by its 'top-tier model,' the company has transitioned from project-based local deployments to cloud-based API interfaces, and even after price hikes, it still reports insufficient computing capacity, reflecting strong demand.

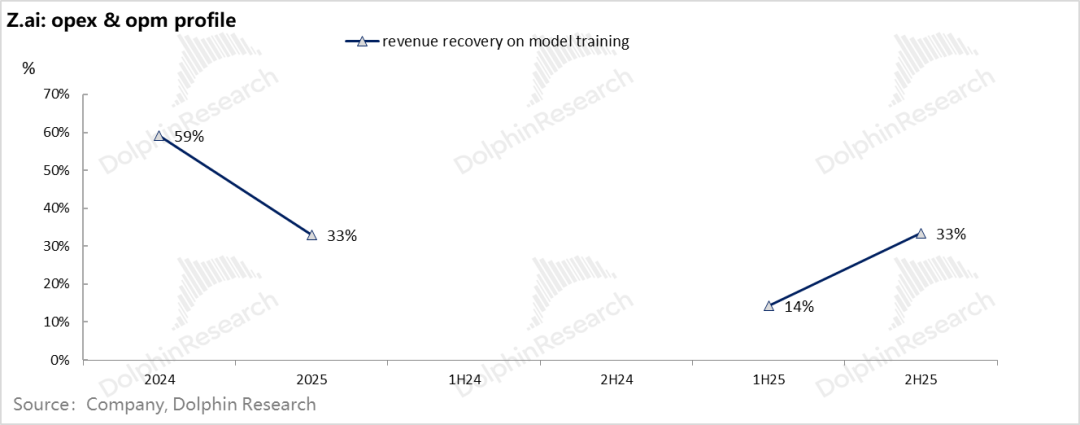

2) Can Current Revenue Cover Last Generation's Model Training Costs?

With foundation models updated annually, a model trained over a year has only a one-year service life. Thus, model economics can be partially assessed by comparing its direct and indirect revenue against the previous year's training investment.

For Zhipu, model training and R&D personnel expenses primarily fall under R&D spending (about 70%). Using R&D expenditure directly, we assess revenue's ability to cover model investments.

Zhipu's 2024 R&D expenditure was 2.2 billion, with 2025 revenue at 720 million, recovering only 33% of 2024 R&D expenditure. For 2026, revenue needs to double to around 1.4 billion to see the recovery rate improve to 45%, roughly in line with MiniMax.

According to the company's earnings call, its cloud API business reached 250 million in March ARR (annualized monthly revenue), better than expected.

This is crucial—considering 2025 actually spent 3.2 billion RMB, annualized revenue already covers 55% of 2025 R&D input even without full demand release, indicating the model is on a steady commercial path.

For comparison, among Chinese peers disclosing ARR, Kling, focused on high-priced video models, hit 300 million in January ARR but gave full-year guidance at January's annualized level due to competition. MiniMax reported 150 million in February ARR (likely including some non-API recurring revenue). Currently, Zhipu holds an edge in both ARR growth trajectory and absolute value, especially as its accelerating ARR comes with pricing power and undersupplied Token capacity, with demand not fully released.

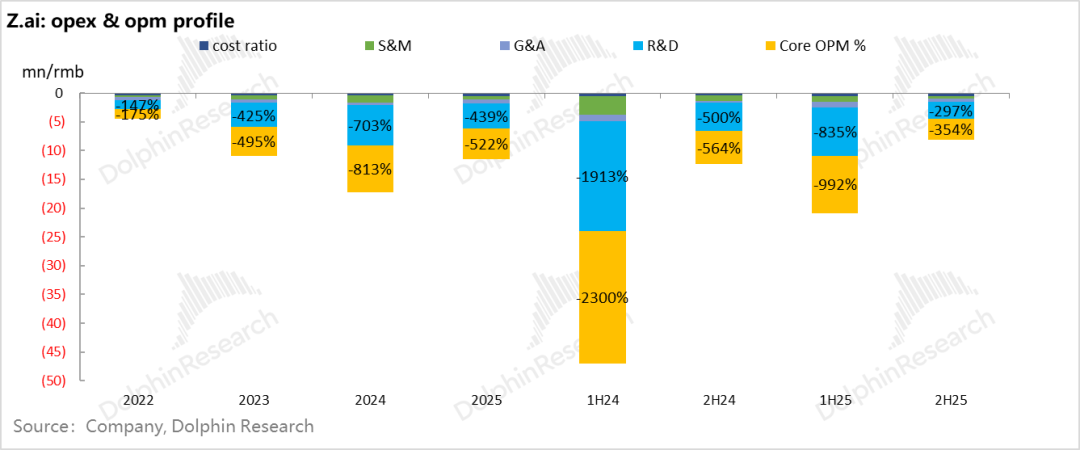

II. Is Gross Margin Still in a 'Pain Phase'?

Unlike MiniMax, which balances B2B and B2C monetization, Zhipu focuses almost exclusively on B2B, with local deployments primarily serving government and state-owned enterprise clients.

After DeepSeek, charging for large models themselves became difficult, shifting focus to local adaptation and tuning during deployments—a process heavy on labor (headcount rose from 883 in 1H25 to nearly 1,100). By the latter half, resource and labor investment drawbacks became more evident.

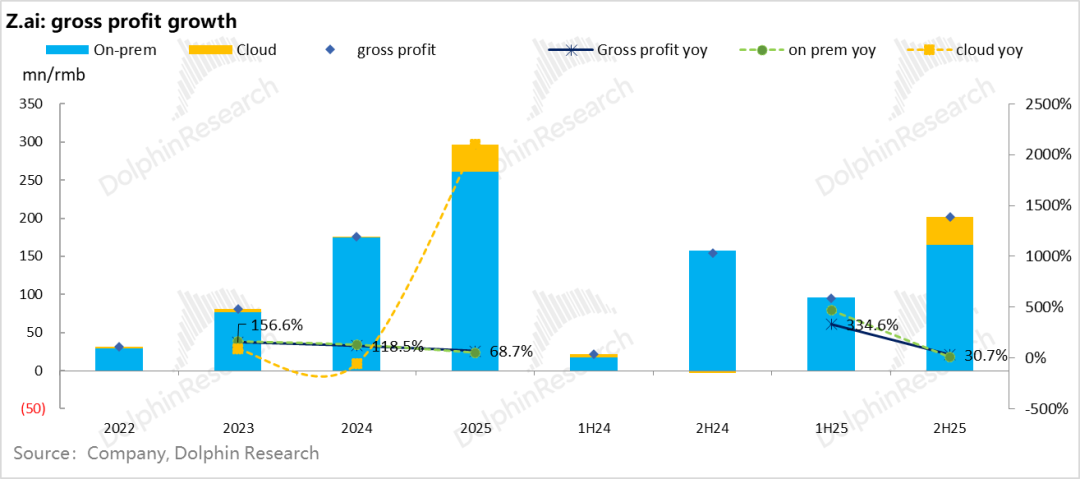

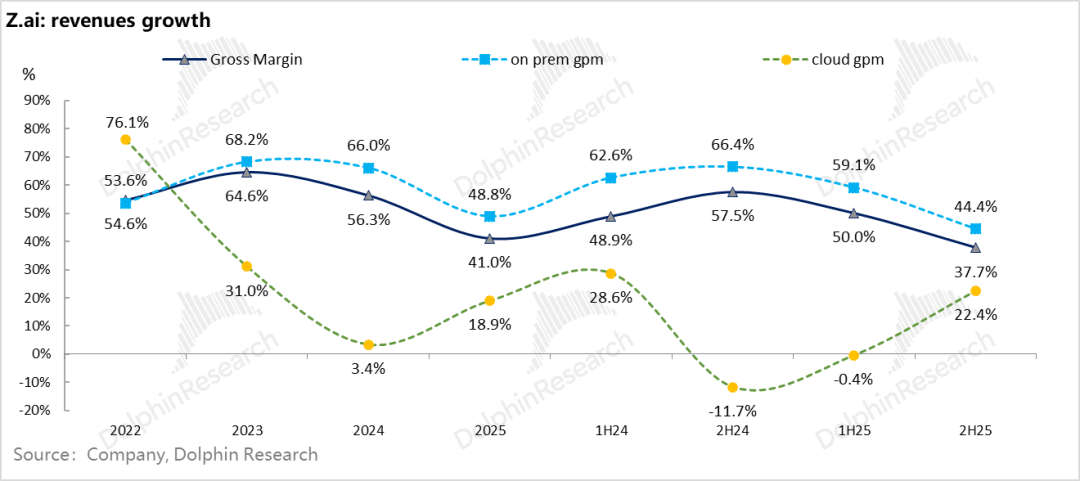

Second-half gross profit was just 200 million, up only 30% year-over-year; local deployment gross profit grew just 5% despite 57% revenue growth.

As explained earlier, local deployments require heavy resource investment, with revenue growth not strongly accompanied by scale effects. Gross margin for local deployments fell from nearly 60% to 44%, steadily declining as revenue expanded.

Conversely, while the model's API business started with extremely low margins due to fierce competition, it benefits from strong scale effects. Second-half revenue growth of 430% lifted margins from near-zero to 22%.

However, with high-margin local deployments slowing + margin decline, and low-margin API business surging + margin improvement, the company's second-half gross margin hit a record low of 38%, well below market expectations.

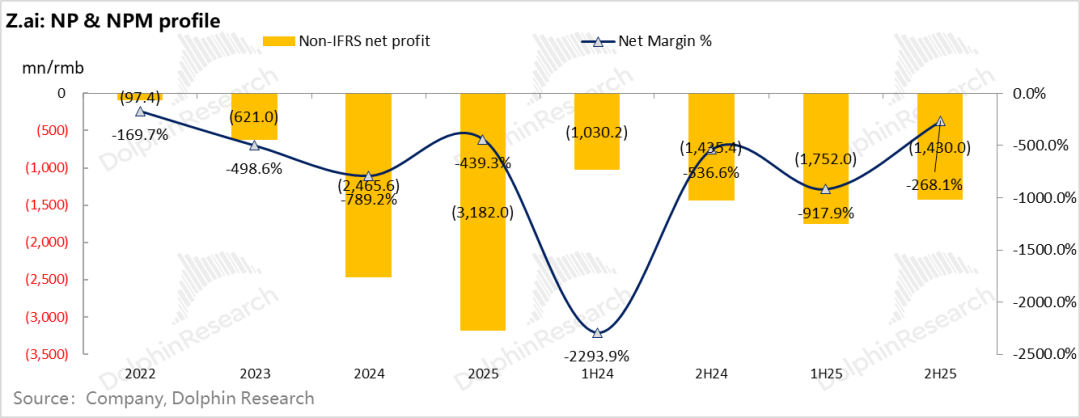

III. Generating 700 Million in Revenue, Incurring 3.2 Billion in Losses! Does Loss Matter When Dreams Are Big?

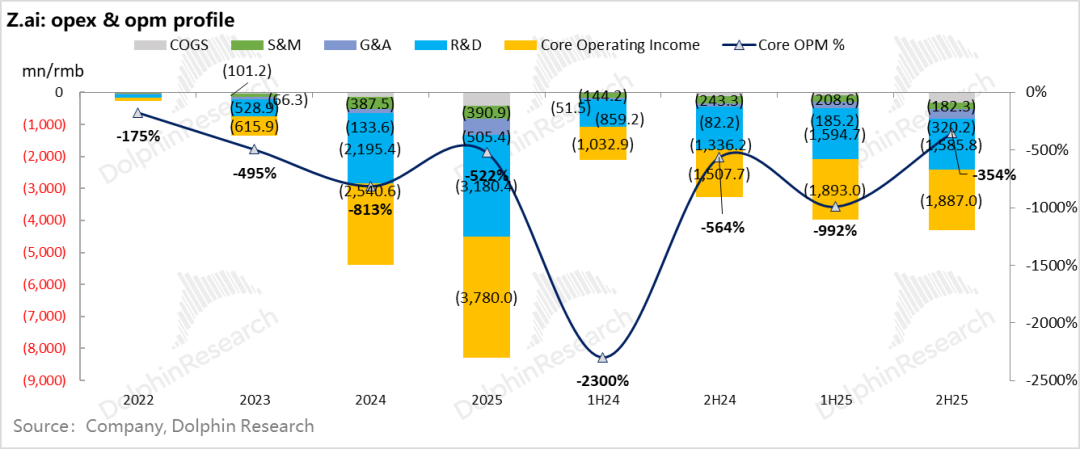

The 38% gross margin seems manageable because it doesn't yet account for the largest investment in large model startups—training expenses, included in R&D expenditure.

Typically, R&D expenditure is 3-5 times revenue, so rapid model iteration via training makes profitability nearly impossible (click here for reasons).

Second-half R&D expenditure (primarily training) hit nearly 1.6 billion RMB, while revenue was just 530 million—three times higher.

With such massive R&D expenditure, other expense changes pale in comparison:

General and administrative expenses were 320 million, up 290% year-over-year—relatively fast. But like MiniMax, Zhipu's sales expenses fell 25% year-over-year to just 180 million in the latter half (model acquisition relies on the model's capabilities, not marketing).

Ultimately, second-half 2025 operating loss after gross profit minus three expenses was 1.9 billion, a 354% loss rate; excluding stock-based compensation, it was 1.5 billion RMB, slightly narrower than the first half's 1.7 billion-plus.

Full-year adjusted net loss was 3.2 billion RMB, a 439% loss rate (losses exceeding revenue fourfold), though rapidly narrowing.

The second-half loss narrowed more sharply: Adjusted net loss was 1.4 billion RMB, a 268% loss rate relative to 500 million in revenue.

Dolphin Research Overall View: AI is Hot, but Zhipu is Hotter?

Among the two listed domestic AI model leaders, Zhipu—initially rated slightly weaker than MiniMax—has delivered a stronger performance in just one quarter.

The core difference, in our view, is Zhipu's higher intelligence index, meaning in the B2B productivity space, intelligence 'scarcity' is a core asset and the key to Token pricing power.

Capital values models based on intellectual scarcity and, on that basis, Token sales volume and revenue.

As a listed company, Zhipu doesn't need to worry about financing, especially with API prices surging and Token demand still undersupplied.

The post-holiday stock rally reflects the market's revaluation of Zhipu, shifting from a discount for local deployment AI providers to a valuation model comparable to overseas B2B peers like Claude.

After a sixfold stock price surge in a quarter, the key question is current ARR and its growth trajectory. The company clearly understands capital market demands—the earnings call opened by highlighting that API-only business hit 250 million in March ARR, with computing capacity undersupplied and easily sold out.

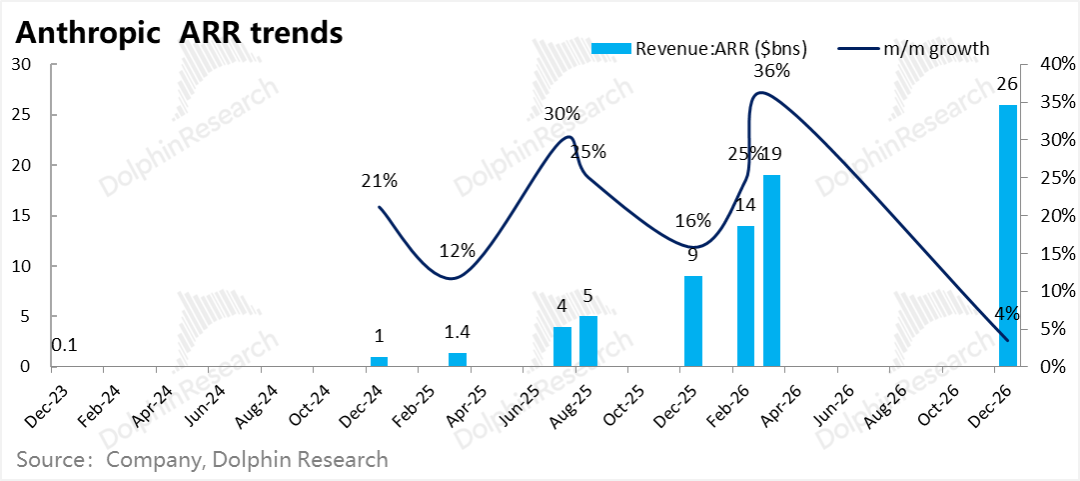

Such guidance invites comparisons with overseas peers' growth and valuation curves: Anthropic, after passing a critical intelligence threshold, grew revenue from 100 million to 1 billion USD in one year, then from 1 billion to 10 billion USD in another.

So the question arises: If Zhipu follows a similar revenue trajectory, reaching 1 billion USD in a year, does valuation still have room to grow?

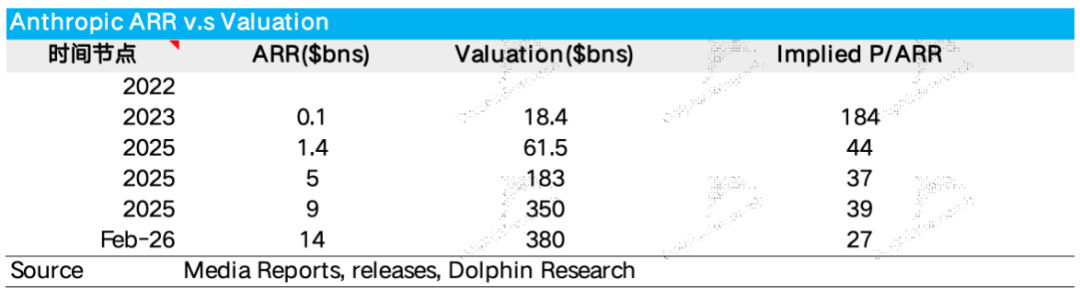

For reference, when Anthropic had an annualized revenue of $1.4 billion, its valuation in the primary market financing was $61.5 billion.

From the current perspective, with a market capitalization of $40 billion and aiming to reach $60 billion, the ARR growth rate, which directly quantifies the intelligence level and popularity of the model, remains of utmost importance.

At least for now, Zhipu seems to be pushing forward with even greater momentum than MiniMax.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. For reprinting, please add and obtain authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the views expressed in this report shall not, under any jurisdiction, be considered or construed as an offer to sell or a solicitation to buy securities, nor shall they

This report is compiled by Dolphin Research, which retains exclusive copyright ownership. Without the prior written approval of Dolphin Research, no institution or individual is permitted to (i) produce, copy, reproduce, duplicate, forward, or generate any form of copies or reproductions in any way, and/or (ii) redistribute or transfer the report, either directly or indirectly, to any unauthorized parties. Dolphin Research reserves all rights pertaining to this matter.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?