Zhipu's 'Aolong': A Hot Topic in the AI Arena

04/08 2026

04/08 2026

497

497

Zhipu Faces Midway Challenges

Author | Jingxing

Editor | Gu Nian

The stock market journey of Zhipu has been a rollercoaster ride, marked by dramatic surges and dips, only to soar once more.

From April 2 to 8, Zhipu's stock witnessed a remarkable 31.94% increase in the first three trading days following the release of its financial report. However, this was swiftly followed by a 14.86% decline, before surging again on April 8, with gains nearing 20% at one point. The revaluation driven by the Token economy has sparked intense debate among market optimists and pessimists.

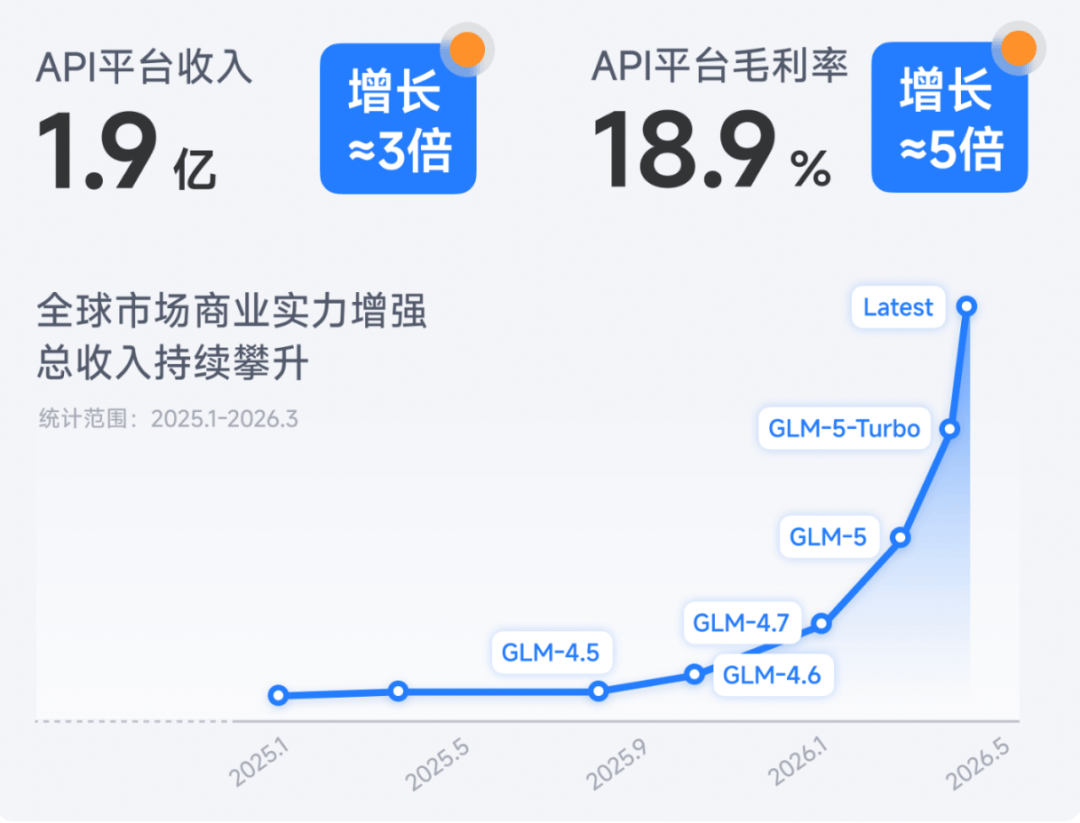

The financial report itself painted a mixed picture. On March 31, Zhipu unveiled its 2025 financial results, revealing a total revenue of 724 million yuan for the year, a significant 131.9% year-on-year increase, marking the third consecutive year of revenue doubling.

The standout performer was the revenue from the cloud-based MaaS platform. In 2024, Zhipu's MaaS platform revenue accounted for a mere 15.5% of total revenue, but this figure jumped to 26.3% in 2025, with business volume reaching 190 million yuan, a staggering 292.6% year-on-year increase. The platform's annual recurring revenue skyrocketed 60-fold over the past 12 months to 1.7 billion yuan. Amidst a price war in China's large model industry, Zhipu boldly raised API prices by a cumulative 83% in the first quarter of 2026. Surprisingly, platform Token usage not only remained resilient but actually surged 400%, defying market trends.

However, in stark contrast to the revenue surge, Zhipu's losses continued to widen. The financial report disclosed a net loss of 4.718 billion yuan for 2025, with an adjusted net loss of 3.182 billion yuan, a 29.1% year-on-year increase. Full-year R&D expenses soared to 3.18 billion yuan, a 44.9% year-on-year rise, exceeding revenue by more than fourfold.

This scenario paints the fundamental picture of the world's first publicly traded large model company: soaring revenue juxtaposed with massive losses. While gross margins for on-premises deployment business declined, cloud deployment business witnessed volume and price increases, with gross margins rising from 3.3% to 18.9%, hinting at a second growth curve. In response, Zhipu CEO Zhang Peng proposed a new brand narrative formula: AGI-era commercial value = upper bound of intelligence × Token consumption scale.

Zhipu's AGI growth narrative hinges on the explosion of high Token consumption scenarios since last year. From developers flocking to programming scenarios to Agent products unleashing Token consumption potential, Zhipu has capitalized on the rising tide of the large model market. In essence, Zhipu's revaluation represents a triumph on the demand side.

Divergent Strategies in the AI 'Lobster' Market

In terms of business ecosystem, Zhipu positions itself as a cost-effective alternative to Anthropic. Zhang Peng once publicly stated, "Our models are excellent enough to be world-class. We have a significant advantage in pricing and cost. We joke that if Anthropic sells for $200, we'll sell for 200 RMB."

This strategy aligns with their business model. The GLM series models are designed to compete with Anthropic's Claude models, aiming to expand their user base with lower Token prices, drive API usage growth, and feed back into model iteration and Token cost increases. The financial report reveals that Zhipu has become one of China's top vendors in paid Token consumption, leading the market's shift from paying for low prices to paying for results.

However, Zhipu and Anthropic (the developer of Claude, which Zhipu targets) are taking divergent paths in their approach to 'lobster' (a metaphor for high-consumption AI scenarios).

On April 4, Anthropic announced that Claude's subscription quotas would no longer support third-party tools like OpenClaw. Some users noted that OpenClaw is a Token black hole, with subscription-based Tokens unable to keep pace: "Just reading a file at the start of a task consumes several rounds of calls. The current MCP (external communication protocol for Claude models) is still single-turn, meaning only one tool can be called at a time, waiting for feedback before calling the next. A single task can consume hundreds of thousands to millions of Tokens."

According to platform plans, Claude's subscription models include Pro, Max (with 5x and 20x versions), and Team (with standard and premium tiers), priced at $20/month, $100/month, $200/month, $25/person/month, and $125/person/month, respectively. Essentially, the more you pay, the higher your usage quota, stronger model permissions, and more advanced features you get, better suited for developers who frequently call models and consume Tokens.

Facing the age of intelligent agents, Anthropic is streamlining its offerings, while Zhipu is adding features.

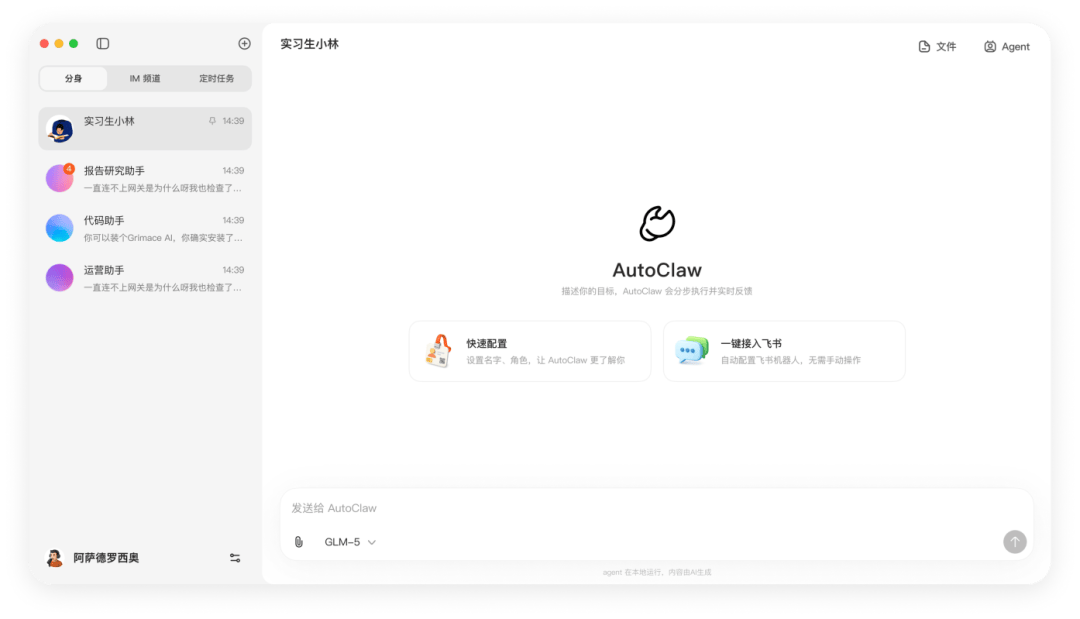

On March 10, Zhipu released AutoClaw, enabling users to install with one click and significantly lowering the barrier to 'lobster' usage. Six days later, Zhipu unveiled GLM-5-Turbo, a base model deeply optimized for lobster scenarios, while raising API prices by 20% and introducing lobster subscription packages priced at 39 RMB/month for 35 million Tokens and 99 RMB/month for 100 million Tokens.

Meanwhile, Anthropic is promoting its own lobster alternative tools, using official versions to attract users' complex task needs and avoid unlimited drains on subscription users' computing power.

Behind these moves lie vastly different commercial objectives. While the pioneer chases an independent lobster ecosystem, the latecomer still grapples with filling its stomach.

Public data shows Anthropic's latest annualized revenue has reached $14 billion. In contrast, Zhipu, with revenue surging to $700 million, is not even in the same league.

In other words, facing Anthropic's robust enterprise-grade API ecosystem, Zhipu's API platform is still in its early ecosystem-building stages. Its user perception remains that of a cheap alternative to overseas models, lacking a leading edge. One Zhipu user's comment sums it up well: "(Cost-effectiveness) depends on the comparison. You get what you pay for. Don't expect too much."

Token Calls: No Room for Weak Hands

If "the upper bound of intelligence determines pricing power" is Zhipu's core narrative, then this year's lobster craze in the AI circle provides tangible support for Zhipu's story: replicating Anthropic's commercial path, serving enterprises while eyeing consumers.

For a long time, Zhipu's revenue structure has relied on "two legs": one is on-premises deployment, emphasizing a strong presence in the government and enterprise market, indirectly reaching development teams covered by enterprise clients. With high average selling prices and gross margins, this has supported Zhipu's early revenue base. The other leg is MaaS cloud deployment, serving enterprises and individual developers through API calls and subscription services, billed by Token consumption or monthly packages, offering stronger scalability. Zhipu enhances developer stickiness by releasing AI code editors and codebase analysis tools, binding them to Zhipu's development ecosystem.

In the past, Zhipu focused on on-premises revenue, emphasizing a strong presence in the government and enterprise market and indirectly reaching development teams covered by enterprise clients. Its consumer-facing (To C) business has long been marginalized, evident in its "reserved" marketing efforts targeting consumers.

During the 2026 Spring Festival, Baidu, Alibaba, ByteDance, and Tencent engaged in a red envelope war, with AI-powered red envelope collection becoming a common user behavior during the New Year period. Meanwhile, Zhipu remained silent in its promotion, with C-side activities largely stalled. The next time ordinary users paid attention to Zhipu was on March 10, when it officially released AutoClaw in an article titled "Today, We Put Lobsters on Every Computer." By March 16, Zhipu rapidly updated GLM-5-Turbo, the world's first base model deeply optimized for lobster scenarios, seeking the next growth point in Token consumption through targeted optimizations for lobster needs.

This is why capital markets have overvalued Zhipu. During the earnings call, when asked whether API growth is sustainable, Zhang Peng confidently replied that the industry has been searching for a simple, cost-effective, and powerful business model to drive growth for years. Today, AI capabilities have evolved from being usable and fun to truly solving increasingly complex and important problems, enabling API calls and Token consumption to translate into real economic value. OpenClaw will drive exponential growth in future API and Token consumption, forming a definite and long-term trend.

However, in the lobster wave, Zhipu is not the biggest winner in the domestic market.

OpenRouter's OpenClaw model data shows that while Zhipu's GLM-5 once topped the popularity charts, models like Kimi, MiniMax, Step (Jieyue Xingchen), MiMo (Xiaomi), and Qwen (Alibaba) dominated OpenClaw's call volume charts for most of the time.

The OpenClaw model rankings show a relay-style rotation at the top. Kimi K2.5 quickly topped the charts due to its cost-effectiveness, being set as OpenClaw's official free main model. MiniMax and Step staged strong comebacks by leveraging their multimodal capabilities and base model optimizations.

The reason is that in Token-intensive scenarios like OpenClaw, daily automated calls from a larger user base are the main consumption drivers. GLM, known for complex production tasks and higher call costs, faces scalability challenges in this Token war.

Data shows that Zhipu's cloud deployment gross margins surged in 2025, with two price hikes upon the release of GLM-5 and GLM-5-Turbo winning market acceptance. However, in terms of revenue structure, Zhipu's on-premises deployment revenue reached 534 million yuan in 2025, accounting for 73.7% of total revenue, remaining its absolute revenue mainstay.

Although Zhipu has specifically optimized the GLM-5-Turbo model for lobster usage scenarios, emphasizing superior execution efficiency in long-chain tasks, it has not overtaken the C-side market due to global users' brand perception inertia. Instead, after its release, it quickly gained adoption from internet giants like ByteDance, Alibaba, and Tencent, becoming a supporting role in their intelligent transformation.

Large Models: A Marathon Without a Finish Line

Judging by its 2025 financial performance, Zhipu seems to have staged a perfect comeback. However, the costs it paid behind the scenes are substantial.

In 2025, Zhipu's sales costs surged over 200% year-on-year to 427 million yuan. The financial report attributed this to increased computing service fees from business expansion. Additionally, R&D expenses rose 44.9% year-on-year to 3.18 billion yuan, due to higher staff costs and increased computing service fees paid to third-party providers.

Compared to internet giants with heavy asset-based, self-owned computing power layouts, Zhipu, a technology-focused company, prefers an asset-light technology supplier model. Its computing power relied heavily on third-party leasing in 2025, with computing costs passed on to downstream clients. This means Zhipu must pay high computing procurement fees to support explosive growth in Token calls, without owning infrastructure.

For Zhipu, this approach has its pros and cons. Compared to BAT's pursuit of self-controlled infrastructure moats, Zhipu emphasizes building barriers at the technology and application layers, allowing it to focus limited funds on maintaining core competitiveness. The downside is that the company must maintain extremely strong competitiveness at the model layer to offset the impact of rising computing costs. From a gross margin perspective, Zhipu's overall gross margin declined from 56.3% in 2024 to 41% in 2025, likely related to computing procurement squeezing profits.

Meanwhile, the large model industry is precisely a marathon with no finish line in sight. From DeepSeek to Seedance, from Manus to OpenClaw, no one knows when the next window of opportunity (windfall) will arrive.

At the AGI-Next Frontier Summit earlier this year, Tang Jie, Zhipu's founder and chief scientist, made the following remarks:

"Large models are now more about speed and time. Maybe if our code is correct, we'll go further in this regard. But if we fail, we might lose six months—just like that."

The launch of any new product could reshape the industry's perception of AI's capability boundaries. In this race, failing to keep up with one generation's capabilities could erase previously accumulated advantages in a short time.

An industry insider close to large models told 'Shixiang' that product iterations in the large model space happen extremely fast. Even if a company achieves leadership with one generation of models, it's hard to fundamentally turn the tide. The ability to endure in a protracted war and avoid falling behind is more crucial in this industry:

"For model companies, standing out is incredibly difficult. Outsiders may not notice, but application companies have a chance to achieve positive ROI or high gross margins. They can build barriers following tech company routes. Even leading application companies that release their own models can gain more overseas attention than flagship models from top model vendors."

This outlines the survival dilemma of model factories. Without delving into underlying computing power, laying out application ecosystems, and building competitive barriers across the entire chain, it is difficult to claim control over market pricing power. Zhipu has fortunately seized the wave of lobster-driven intelligent agents, but how long this dividend will last and where the next challenger will emerge can only be answered by the future.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?