Bilibili: Is Tencent Cutting Back Its Stake? Are AI Costs Eating into Profits? Can Games Save the Day?

05/20 2026

05/20 2026

517

517

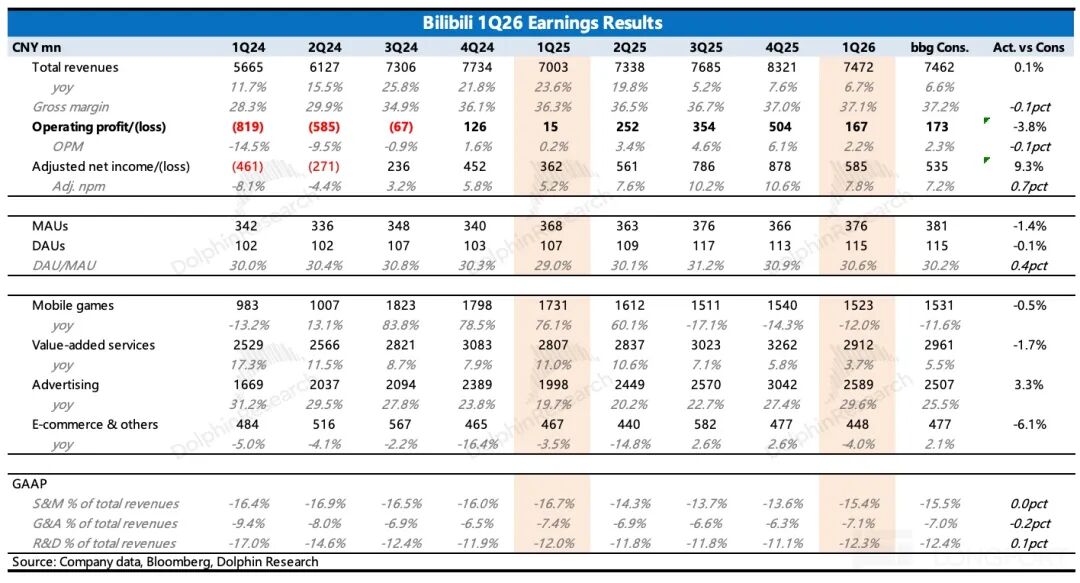

On May 19th, Beijing time, following the close of the Hong Kong stock market, Bilibili (BILI.US) unveiled its Q1 2026 financial results, which continued to showcase a performance where 'advertising takes the lead,' generally meeting market expectations.

Let's delve deeper:

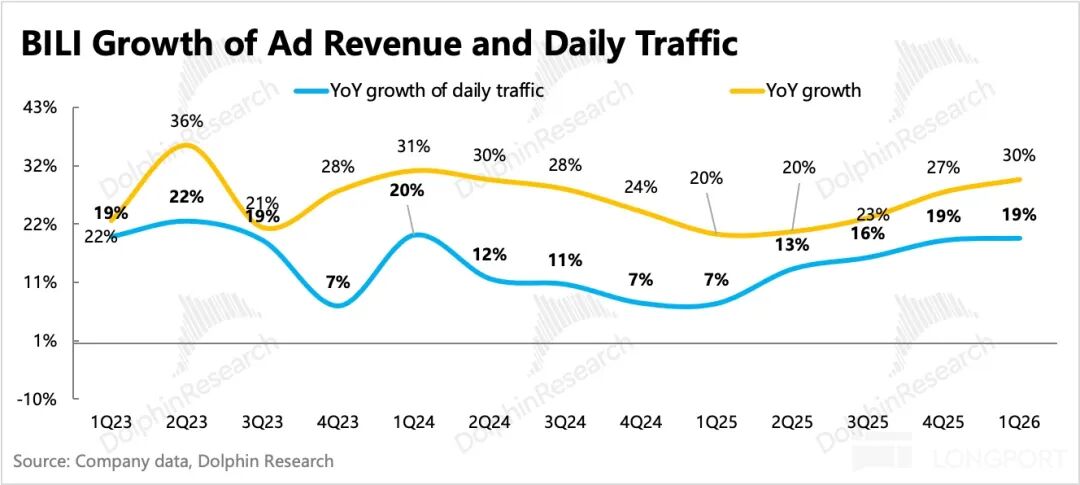

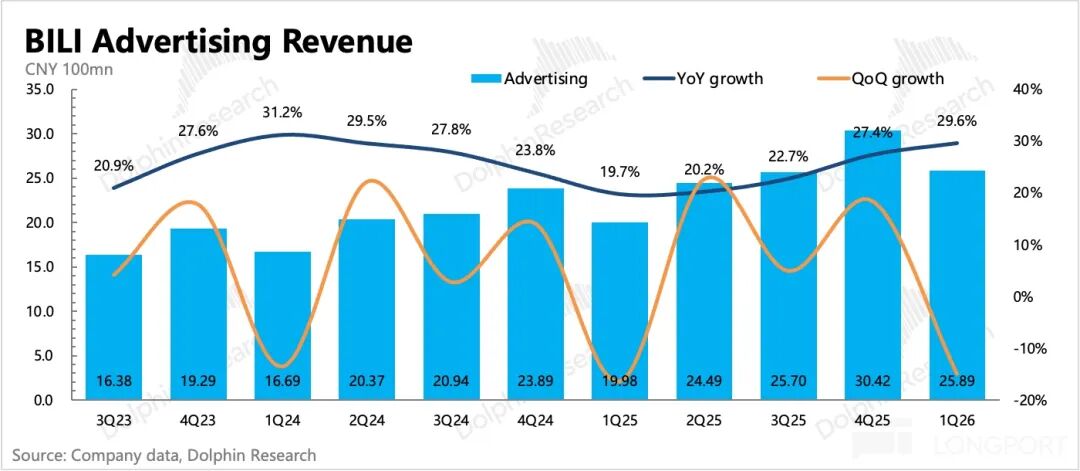

1. Advertising is booming: Q1 advertising revenue surged by 30%, slightly surpassing forecasts, particularly impressive amid a challenging industry landscape. Bilibili has clearly capitalized on the high growth and fierce competition in sectors such as AI and gaming.

This growth spurt is anticipated to persist for some time, fueled by sustained sector expansion and competition, coupled with Bilibili's ongoing enhancement of its advertising inventory.

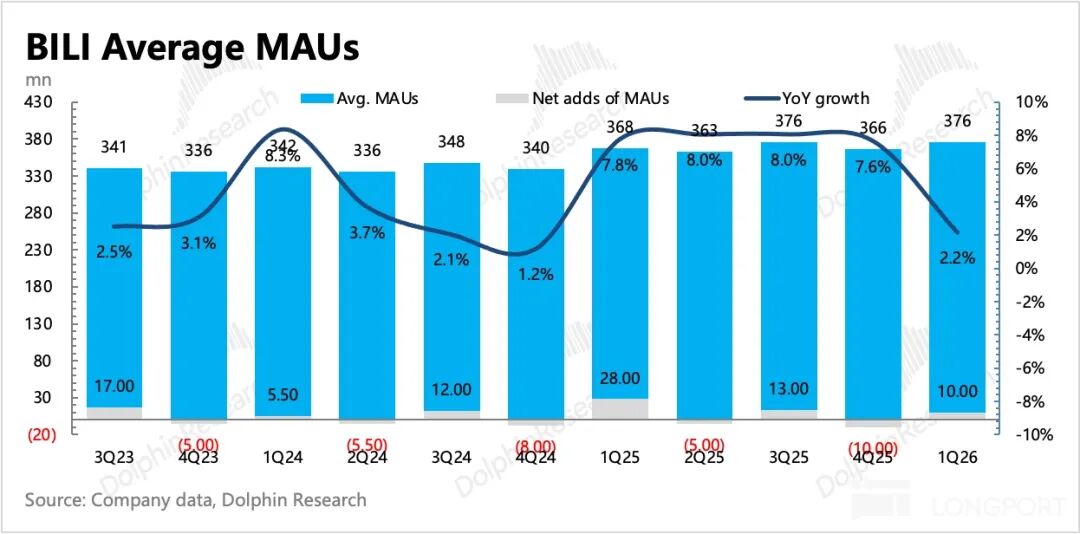

2. User growth has plateaued, but engagement is on the rise: Q1 monthly active users (MAUs) increased by 10 million sequentially, reaching 376 million, matching Q3 levels from the previous year but failing to hit a new peak during the typically strong Q1 season, which is a minor setback. This could be influenced by the timing of the Spring Festival and winter vacation, with further insights expected from the earnings call.

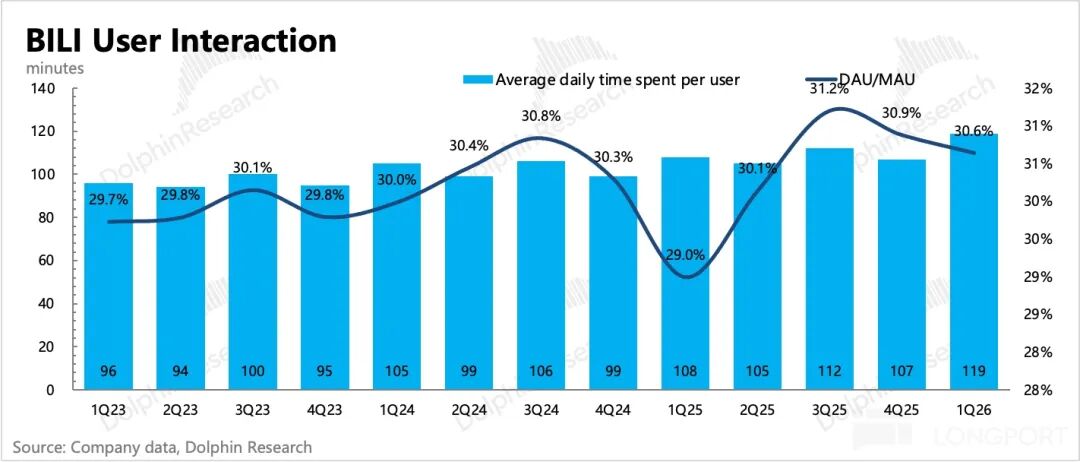

User engagement metrics (DAU/MAU, average daily usage) continued to improve marginally year-over-year, with DAU/MAU reaching 30.6% and average daily usage hitting a record high of 119 minutes.

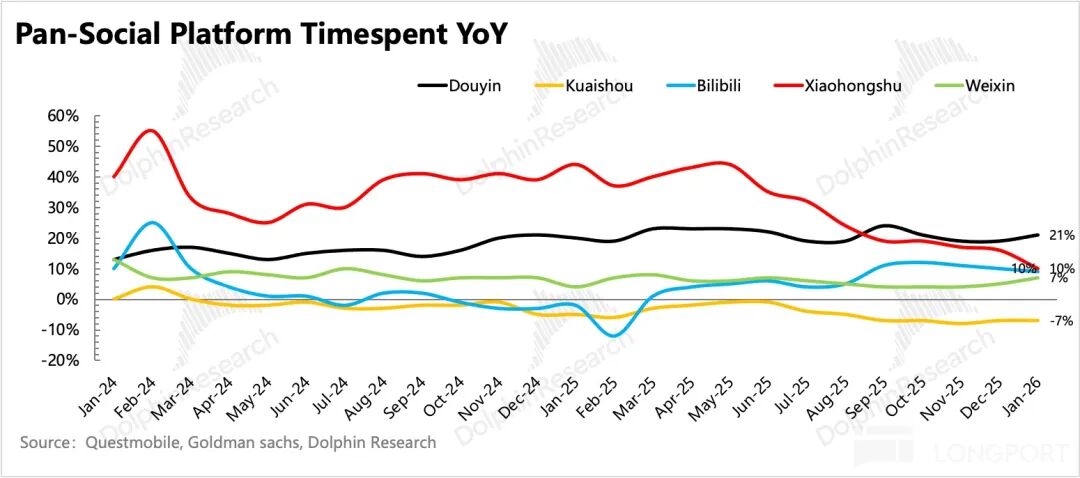

Combining data from QuestMobile, total user time spent grew slightly in January compared to Q4 last year, but given the low base in Q1 last year, the overall growth trajectory remains steady. When compared to social platforms and long-form video counterparts, except for the unstoppable rise of Douyin and a slight rebound in WeChat's growth, Bilibili is holding its own. Xiaohongshu has seen a marked slowdown, while Kuaishou continues to experience a slight decline.

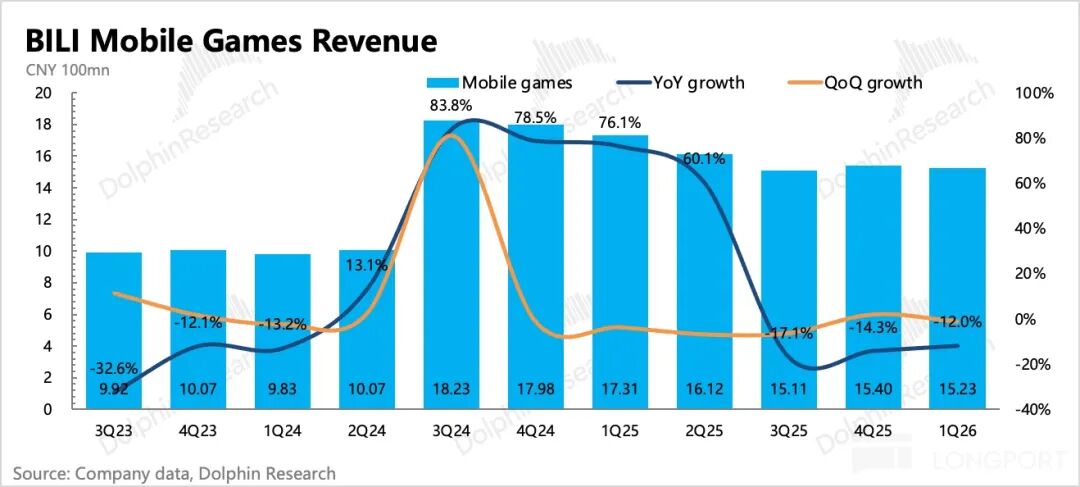

3. A new gaming cycle is on the horizon: Q1 was still impacted by a high comparison base, with a 12% year-over-year decline. The quarter primarily saw the release of 'San Mou' in Hong Kong, Macau, and Taiwan, in a relatively small market with steady performance. With the planned launch of 'Three Kingdoms: Heroes' at the end of Q2 and two additional games in the second half of the year, a new gaming cycle is gradually emerging.

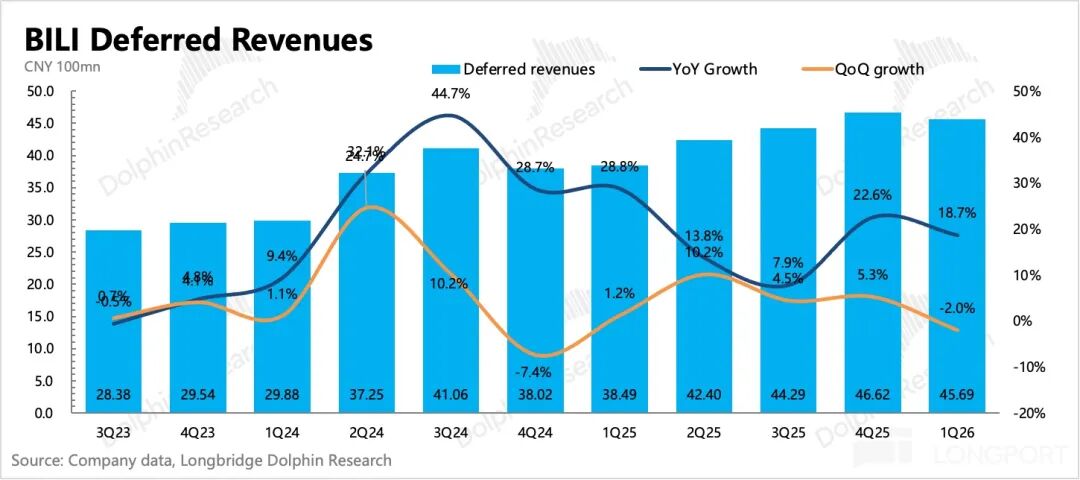

Deferred revenue at the end of Q1 increased by 19% year-over-year but decreased slightly sequentially, possibly due to the strong sales contribution of 'Escape from Yakov' in the previous quarter.

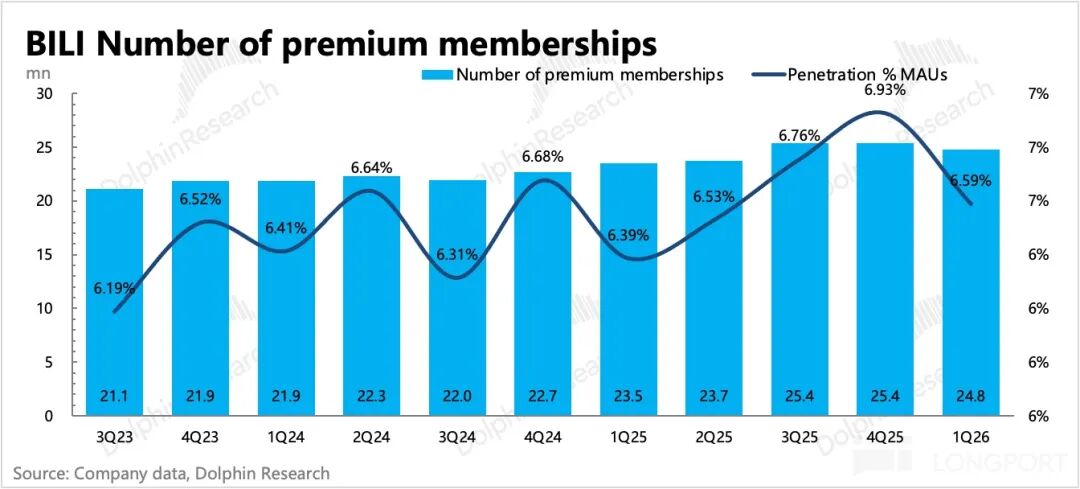

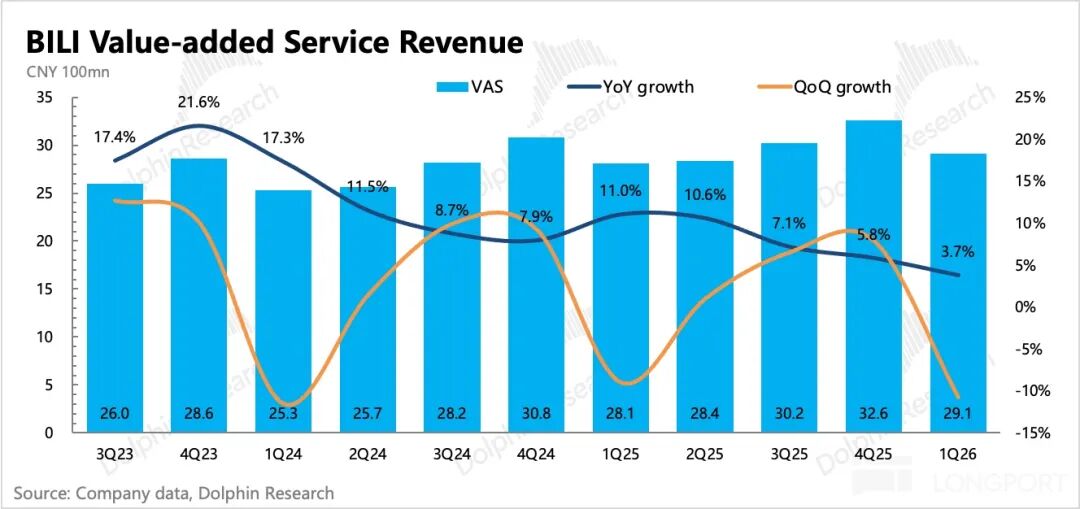

4. Live streaming remains under pressure, and long-form video is losing steam: Q1 value-added services growth slowed further to 3.7%, with both live streaming and premium memberships weakening, and the membership base decreasing by nearly 500,000.

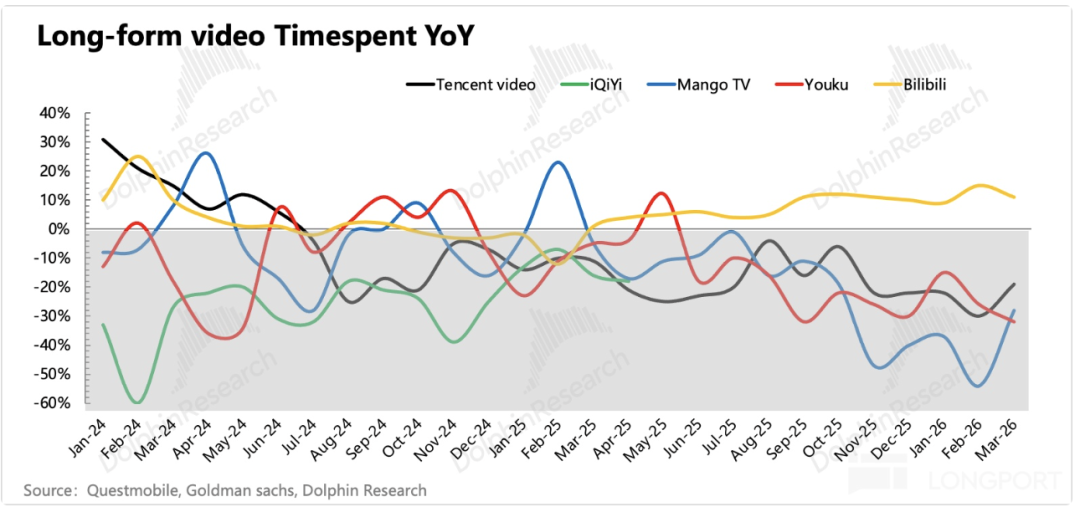

Combining data from QuestMobile, total viewing time for iQIYI, Youku, and Tencent Video continued to decline in Q1. Long-form dramas are not only being affected by AI-generated comics, live-action short dramas, and short videos, but movies during the Spring Festival also underperformed, with Q1 box office revenue down 51% year-over-year, following the 'Ne Zha' high in the previous year.

However, Bilibili's premium membership content selection logic differs from that of iQIYI, Youku, and Tencent Video. Bilibili's content is continuously supplied by uploaders, and its copyrighted content mainly consists of global classics. Its ability to swiftly gauge user preferences through comments and bullet screens allows for the acquisition of relatively low-cost classic films. In contrast, iQIYI, Youku, and Tencent Video rely heavily on new copyrighted dramas to drive user engagement, and without fresh content, users tend to drift away.

5. Increased AI investments are becoming evident: Operating profit reached RMB 170 million, with a profit margin of 2.2%. Although Q1 typically sees lower profit margins due to the e-commerce off-season affecting advertising revenue, the marketing peak season, and employee year-end bonuses, the sequential decline this quarter was more pronounced than in previous years. The key difference is the increased AI investments mentioned last quarter, reflected in R&D expenses shifting from three consecutive years of contraction (reducing game R&D) to a 9% year-over-year increase this quarter.

Ultimately, adjusted net profit reached RMB 590 million, with a profit margin of 7.8%, a sequential decline of nearly 3 percentage points. Last quarter, management provided guidance, expecting the increased AI investments this year, even with offsets from control over other expenses, to still impact profits by RMB 500 million to RMB 1 billion.

6. Share repurchases have concluded, with attention turning to new plans: In Q1, the company repurchased 2.5 million shares, spending US$60 million at an average price of US$24. As of the end of Q1, the repurchase plan approved in 2024 (US$200 million over 2 years) has been completed.

Currently, the company has net cash of RMB 19.3 billion (approximately US$2.8 billion) on hand, enabling it to continue with repurchases. Attention will be focused on management's plans for shareholder returns in the earnings call.

Especially after being rattled by Tencent's plan to sell high-valued investment assets to support its own repurchases a few days ago, which led to a significant stock price decline, it's worth noting that Tencent currently holds about 10% of Bilibili's equity.

7. Overview of Performance Indicators

Dolphin Research's Perspective

Q1 earnings revealed that advertising remains the standout performer, but before the new gaming cycle truly arrives, the erosion of profits by AI investments has already commenced. Last quarter, the company guided that this year's investments were expected to impact profits by RMB 500 million to RMB 1 billion. Based on trends this quarter, Dolphin Research estimates the impact to be around RMB 50 million to RMB 100 million, largely in line with the guided script.

Although management also stated last quarter that they would invest while monitoring the situation and maintain investment discipline, the market still reacted negatively. This is understandable, as Bilibili's market cap was close to US$11 billion at the time, with a PE of nearly 25 times based on original profit expectations (adjusted profit after adding back SBC), significantly higher than its Chinese peers.

This is because the market was largely basing its projections on management's previous long-term profit margin guidance of 15% to 20%, extrapolating profit growth trajectories for the next three years. The newly added AI investments naturally disrupted these expectations, as they are clearly not short-term one-time investments.

Moreover, the impact of AI investments on performance is not as immediately visible as cloud revenue or large language model subscription revenue. Therefore, the market is bound to question the return on investment behind these expenditures, and the short-term erosion of profits will inevitably delay the achievement of target profit margins, necessitating the incorporation of these risk discounts.

However, considering the current perspective on the erosion of profits by AI investments, we believe there may be shifts from last quarter's judgment. If there are further short-term adjustments, it could present an opportunity for attention:

(1) The approaching new gaming cycle: Revenue growth is the most effective way to alleviate market concerns about increased investments eroding profits. Currently, Bilibili is heavily reliant on games for revenue growth.

The upcoming release of 'Three Kingdoms: Heroes' in mid-year, 'Shining Lumi' in Q3, and the potential release of 'Romance of the Three Kingdoms: The Righteous Path' at the end of the year bring us closer to this new gaming cycle.

While these three games may not match the blockbuster potential of 'San Mou,' the lower base in the second half of the year, combined with incremental growth, will alleviate the pressure of AI investments on Bilibili's profitability.

(2) Partial digestion of high valuations: Last week, Tencent released its earnings report, and during the earnings call, management addressed how to ensure shareholder returns amid significant increases in Capex, mentioning adjusting the investment portfolio to support repurchases. This involves liquidating some investment assets to obtain funds for repurchases.

Regarding which investment assets might be sold, management mentioned comparing asset valuations with their own (excluding the value of investment equity, with a main business PE of 10x). If an asset's valuation is significantly higher than their own, they would make adjustments.

As a result, Bilibili, which has historically had a relatively high valuation among Chinese assets, became a concern, with a total decline of 15% over Thursday and Friday. Tencent's stake in Bilibili decreased from 13.5% to 10.5% between 2020 and 2022, with no significant reductions since 2023.

Dolphin Research believes that the likelihood of Bilibili being a target for Tencent's asset liquidation is low:

On one hand, Bilibili's market cap has mainly hovered between US$8 billion and US$10 billion over the past year, with a short-term neutral valuation just over US$10 billion, and the possibility of reaching US$15 billion only under optimistic sentiment (refer to the valuation ranges provided under different expectations in last quarter's earnings review). Selling Tencent's entire 10% stake would yield less than HK$10 billion in funds, which, at the current repurchase pace of HK$500 million per day, would not even last a month.

On the other hand, as an important channel for pan-entertainment and now labeled as a primary AI investment channel, it would not be strategically suitable for Tencent to make such large-scale reductions.

Therefore, we believe that, at least in the short to medium term, the aforementioned concerns are somewhat overblown. Although the current valuation is still not low from a horizontal perspective, it is currently a period of pressure for games. With the new gaming cycle kicking off in the second half of the year and performance growth recovering, the valuation is expected to be further digested.

The following is a detailed analysis:

1. User Growth Slows, Engagement Increases

In Q1, Bilibili's MAUs increased by 10 million sequentially, but failed to set a new high during the peak season. However, engagement metrics continued to improve, with DAU/MAU reaching 30.6% and user time hitting a record high of 119 minutes, an increase of 11 minutes year-over-year. According to QuestMobile data, Bilibili's time spent growth in Q1 was also at the mid-to-upper level among social platforms.

2. Advertising Remains the Standout Performer

In Q1, Bilibili's advertising revenue reached RMB 2.6 billion, a 30% year-over-year increase, accelerating growth and slightly exceeding expectations. The growth was mainly driven by an increase in total user time spent within the ecosystem (+19% year-over-year, slightly accelerating from 18.6% in Q4) and an increase in ad load.

Currently, Bilibili's ad load is still at 7%-8%, with room for improvement compared to peers. In early April, the company introduced a new ad slot called 'Pause Ad' on the playback page, which automatically plays when users manually pause a video, although this feature can be turned off by users and uploaders.

3. The New Gaming Cycle is Approaching

Game revenue continued to face pressure from a high comparison base and a pipeline vacuum in Q1, with a 12% year-over-year decline, in line with expectations. Q1 mainly saw the release of 'San Mou' in Hong Kong, Macau, and Taiwan, in a relatively small market with steady performance. The sequential decline in deferred revenue in Q1 may be attributed to weakness in value-added services and the overall平淡 (plain) performance of games.

Regarding the future pipeline: In addition to those mentioned last quarter, 'Three Kingdoms: Heroes,' expected to launch in mid-year, and 'Shining Lumi,' expected for a global release in Q4, a new co-published game, 'Romance of the Three Kingdoms: The Righteous Path,' is expected to launch in Q4.

'Romance of the Three Kingdoms: The Righteous Path' was officially unveiled on March 18th and opened for pre-registrations across all platforms, with the 'Peach Garden Closed Beta' starting on March 28th. It is a 3D sandbox strategy SLG game. As a new game licensed from the 'Romance of the Three Kingdoms' series IP, which once pioneered the SLG genre, it is worth watching and anticipating.

In addition to basic strategy gameplay, this game emphasizes immersive role-playing and character development, making it more of a single-player experience. Moreover, 'Romance of the Three Kingdoms: The Righteous Path' follows a strategy of reducing grind and pay-to-win elements, simplifying interactive design and focusing on core strategic gameplay.

Currently, some institutions expect the game to generate RMB 1.7 billion in revenue in its first 12 months, approximately 40% of 'San Mou's' revenue. Dolphin Research believes this may be slightly aggressive, while also considering the potential internal cannibalization of 'San Mou' and other games with similar themes.

However, from a trend perspective, with the approaching new gaming product cycle, Bilibili's gaming turning point is also near.

4. Significant Pressure on Value-Added Services

VAS revenue, primarily from live streaming and premium memberships, grew by 3.7% year-over-year in Q1, with growth continuing to slow. The premium membership base decreased by 500,000 sequentially to 24.77 million in Q1. Given the industry-wide pressures on long-form video, Bilibili is not immune.

Apart from premium memberships, the sluggish performance in the fan economy and live streaming sectors can largely be attributed to challenges within the live streaming industry itself.

V. AI Investments Start to Yield Impact

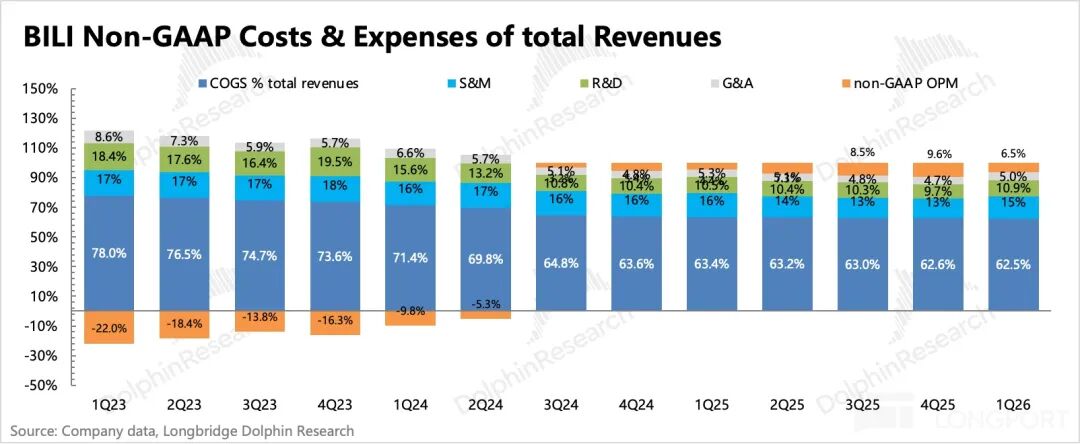

Despite Bilibili's profits continuing to surge year-on-year in the first quarter, the ramifications of AI investments have begun to emerge.

From the vantage point of operating profit derived from core business operations (= gross profit - operating expenses), the figure reached 170 million for the period, boasting a profit margin of 2.2%. The adjusted net profit stood at 590 million (primarily adjusted by incorporating SBC expenses, which constituted 4% of total revenue), with a profit margin of 8%.

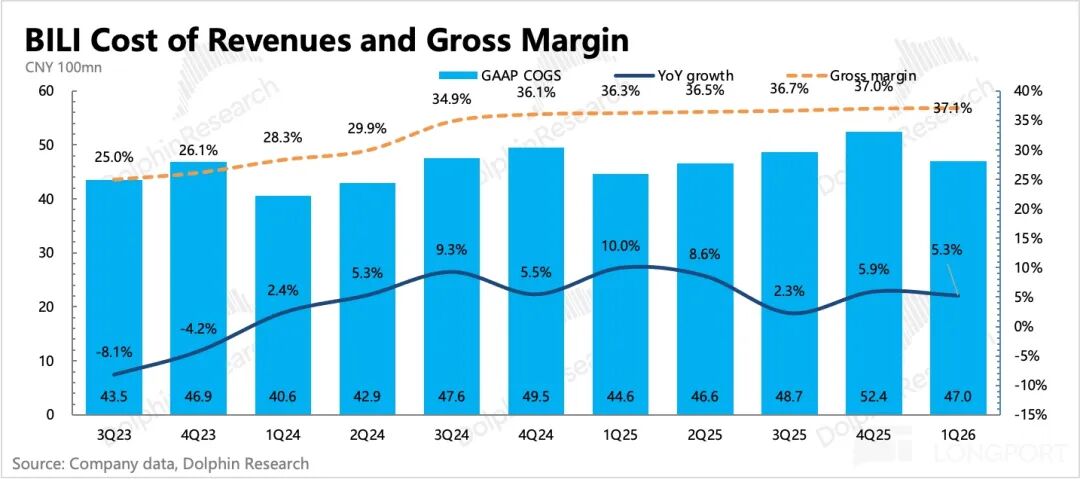

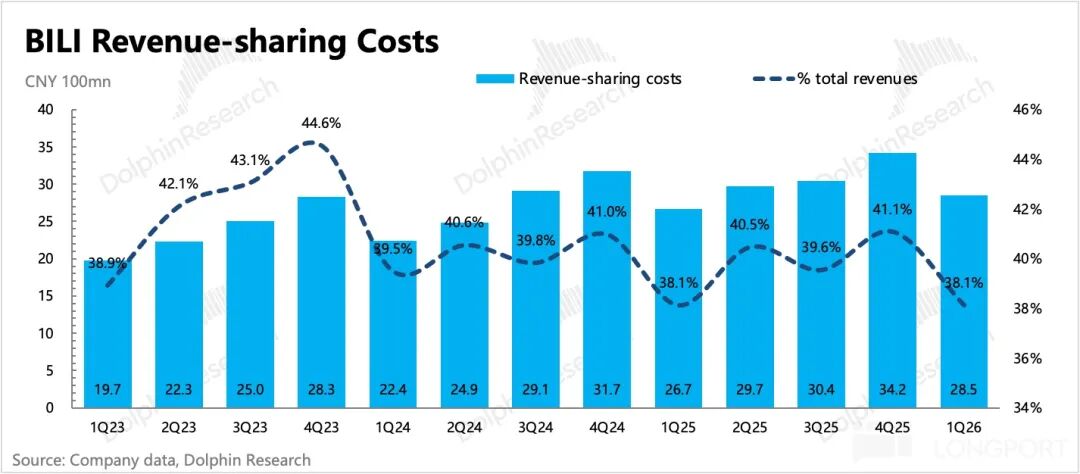

1. Gross Profit Margin Edges Up Gradually

The gradual uptick in the gross profit margin is predominantly fueled by the sustained robust growth in advertising, a sector known for its high gross profit margins.

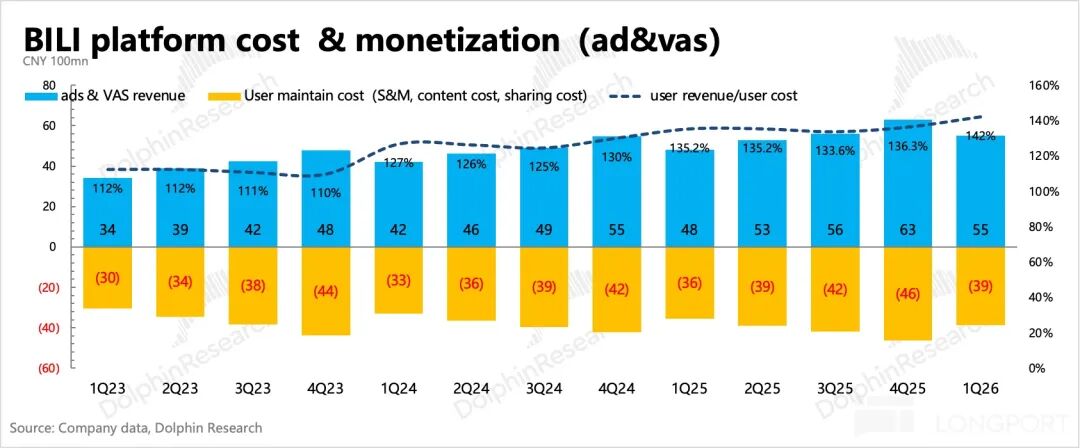

In terms of the specific cost structure, revenue-sharing costs constitute the largest share (38% of revenue), primarily linked to gaming, live streaming, and Huohuo Advertising. In the first quarter, revenue-sharing costs continued their upward trajectory, reaching 2.85 billion, marking a 7% year-on-year increase.

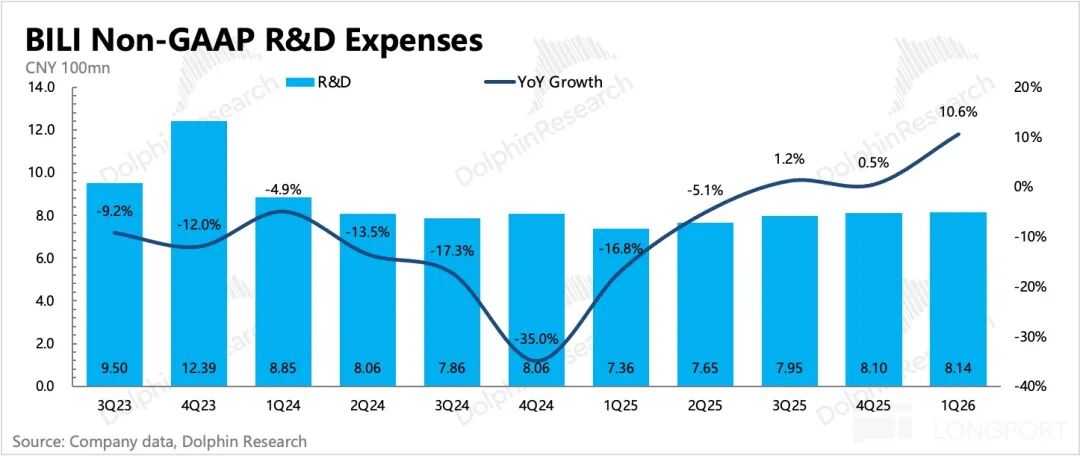

2. R&D Expenditure Rises for the First Time in Three Years

Among operating expenses, sales expenses remained relatively stable, while administrative expenses witnessed a slight uptick. Consequently, the primary growth was observed in R&D expenses, which experienced a notable 9% increase for the first time since 2023, underscoring the impact of AI investments.

Although profits have experienced a slight dip, from the perspective of the 'traffic monetization/cost relationship' that Dolphin Research has consistently monitored, the platform's monetization efficiency continues to enhance, reflecting more on the stability of the platform ecosystem and its inherent monetization capabilities.

Of course, the worthiness of AI investments also hinges on management's ability to continually demonstrate accelerated growth and monetization efficiency.

- END -

// Reprint Authorization

This article is an original piece from Dolphin Research. Reprinting is strictly prohibited without prior authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general informational and data reference purposes, designed for the perusal of users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, preferences, risk tolerance, financial situation, or unique needs of any individual recipient. Investors are advised to consult with independent professional advisors before making investment decisions based on this report. Any person utilizing or referring to the content or information mentioned in this report does so at their own risk. Dolphin Research shall not be held liable for any direct or indirect liabilities or losses that may arise from the use of the data contained herein. The information and data presented in this report are sourced from publicly available materials and are for reference only. Dolphin Research endeavors to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information or opinions expressed in this report shall not, under any circumstances, be construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, solicitations, or advice regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for distribution to, or use by, any person in any jurisdiction where such distribution, publication, provision, or use would contravene applicable laws or regulations or would subject Dolphin Research and/or its affiliates or associated companies to any registration or licensing requirements in that jurisdiction.

This report solely reflects the personal views, insights, and analytical methods of the relevant authors and does not represent the official stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is exclusively owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) reproduce, copy, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

AI Titans Are All in the Red: Time for Intelligent Driving Car Buyers to Reassess?

-

![]()

In the Next Decade of Joint Ventures, Honda Should Move Away from 'Stubbornness'

-

![]()

Operating Profit Plummets by 57%! What Caused Tesla’s Profitability to Decline in Q2?

-

![]()

Starting at 12,999 Yuan! Samsung’s Pioneering Wide Foldable Phone Unveiled: Sleek, Lightweight, and Ushering in a New Era for Android Foldables

-

![]()

Seven Bankruptcies Fail to Topple It! Aston Martin Raises £550 Million to Keep Afloat

-

![]()

Weichai's 'Triple Leap': From Diesel Engine Manufacturer to a 400 Billion Yuan Powerhouse

-

![]()

Tesla’s Financial Acumen Outshines Even Huawei’s

-

![]()

ChinaJoy 2026 Preview Roundup: AI Smartphones, AI PCs, and Robots Take Center Stage, Far Beyond Gaming!