NVIDIA: Rivals Pressure, AI 'Bottlenecks' Shift, Can the 'Cosmic' Stock Avoid a 'Slight Setback'?

05/22 2026

05/22 2026

663

663

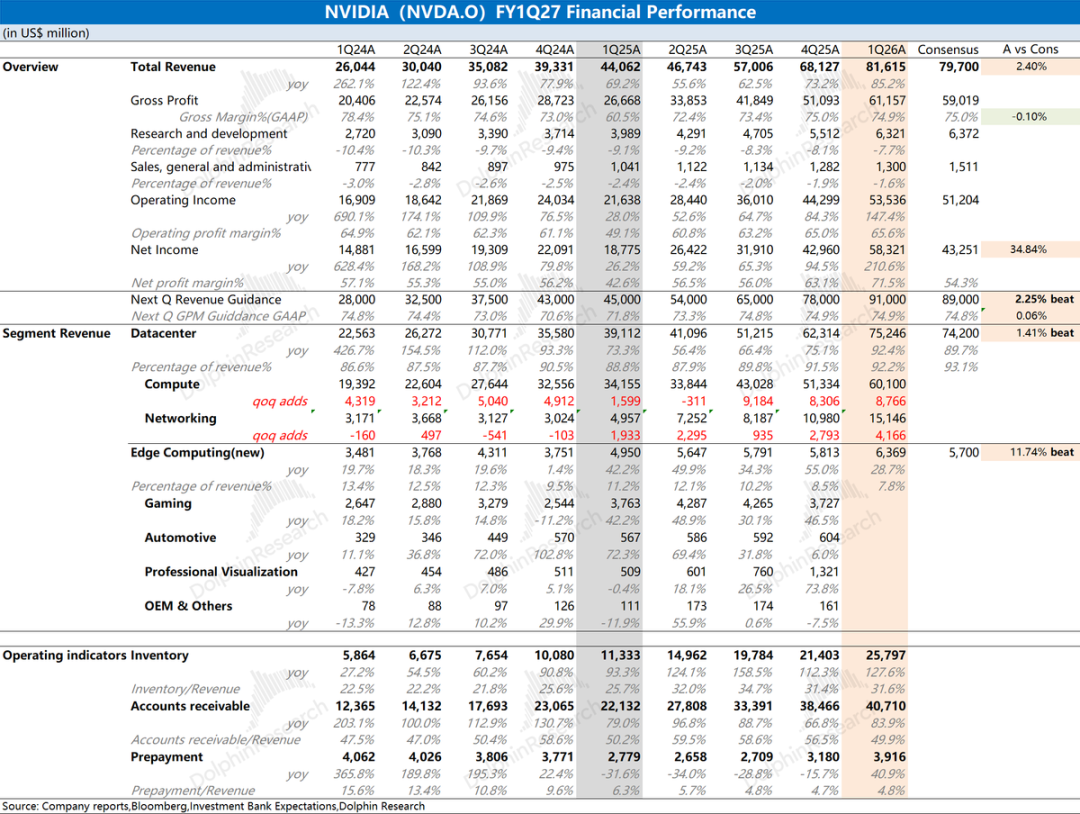

NVIDIA (NVDA.O) released its first-quarter earnings report for FY2027 (as of April 2026) after the U.S. market closed in the early morning of May 21, 2026, Beijing time. Key details are as follows:

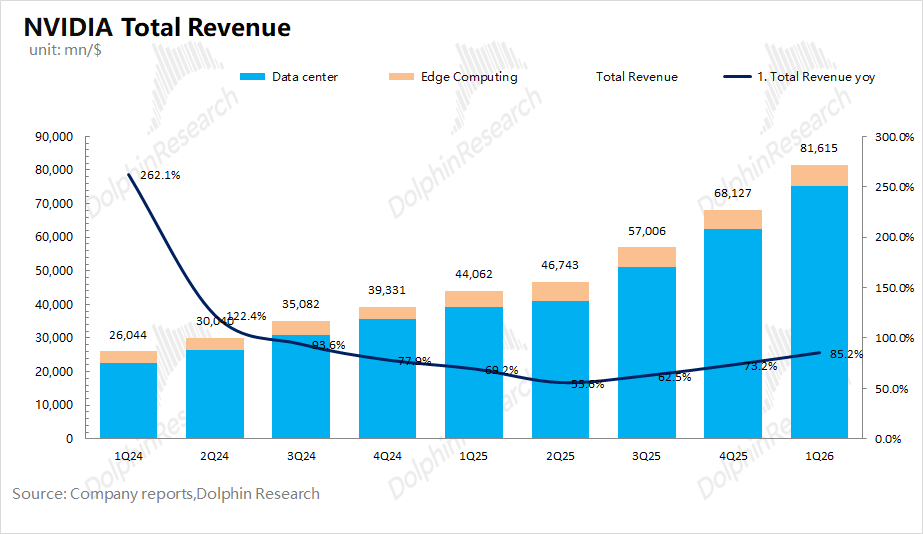

1. Core Operating Metrics: Total revenue reached $81.6 billion, exceeding upgraded buyer expectations ($78-80 billion), with a quarter-over-quarter increase of $13.5 billion, almost entirely driven by growth in Blackwell mass production within the data center business.

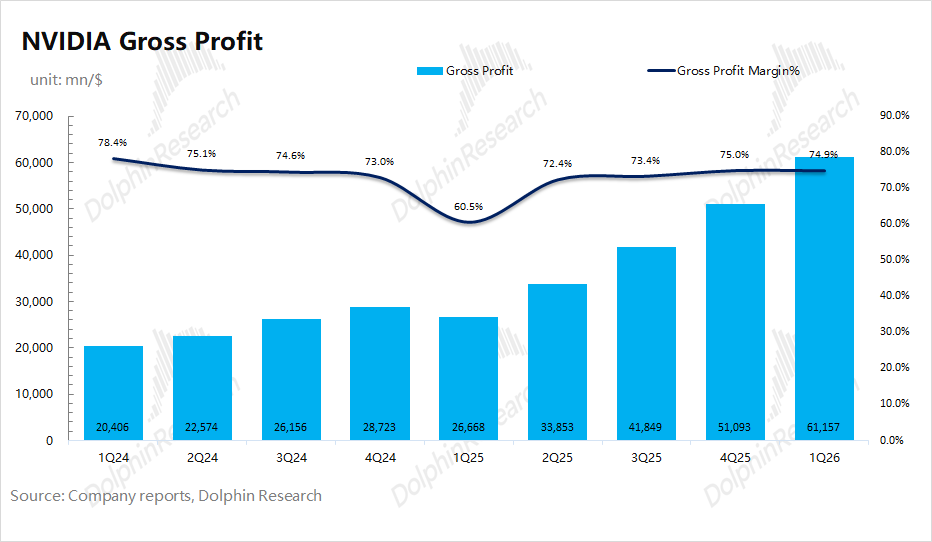

Gross margin for the quarter was 74.9%, down 0.1 percentage point sequentially, largely in line with market expectations (75%). With B300 mass production ramping up, the company's gross margin has rebounded to around 75%.

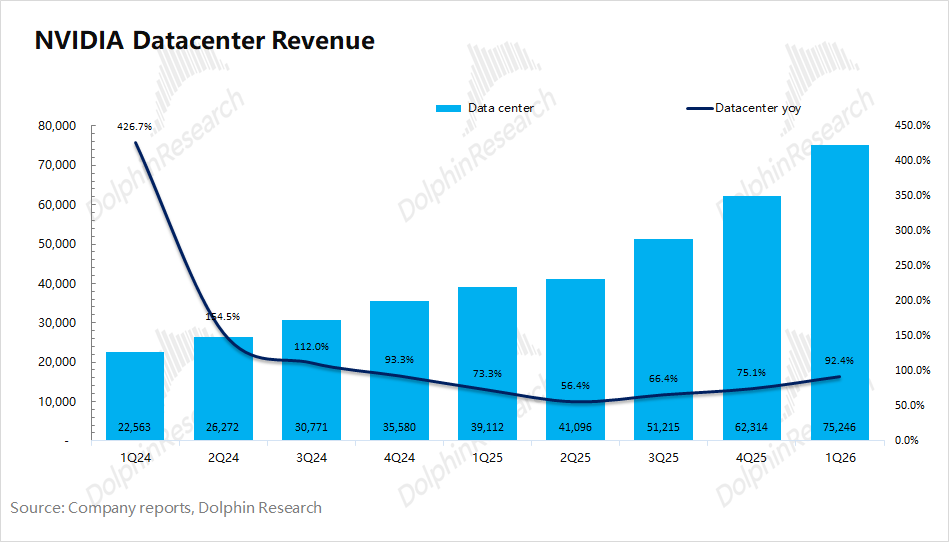

2. Data Center: Revenue reached $75.2 billion this quarter, with a sequential increase of $12.9 billion, primarily due to increased deliveries of B300 series chips. The Blackwell architecture has become the dominant product across all customer categories.

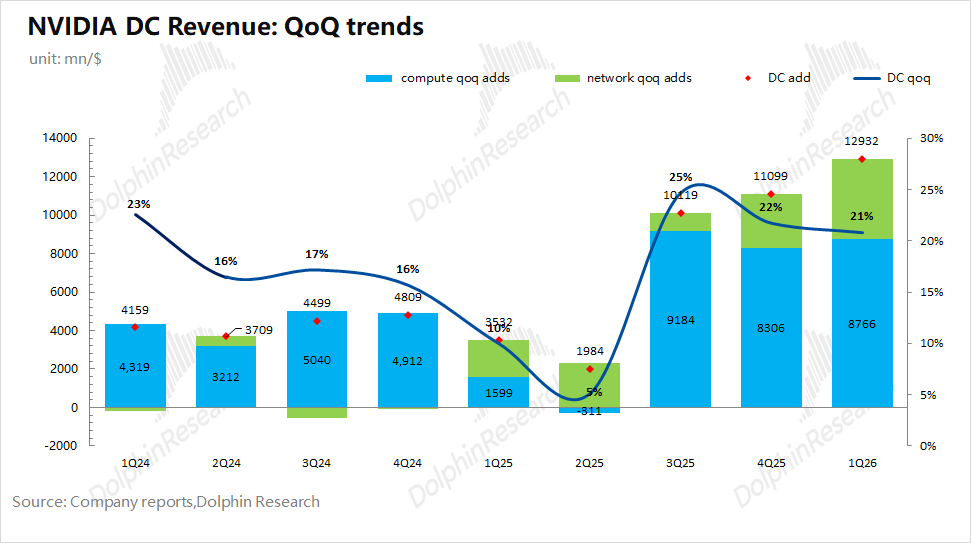

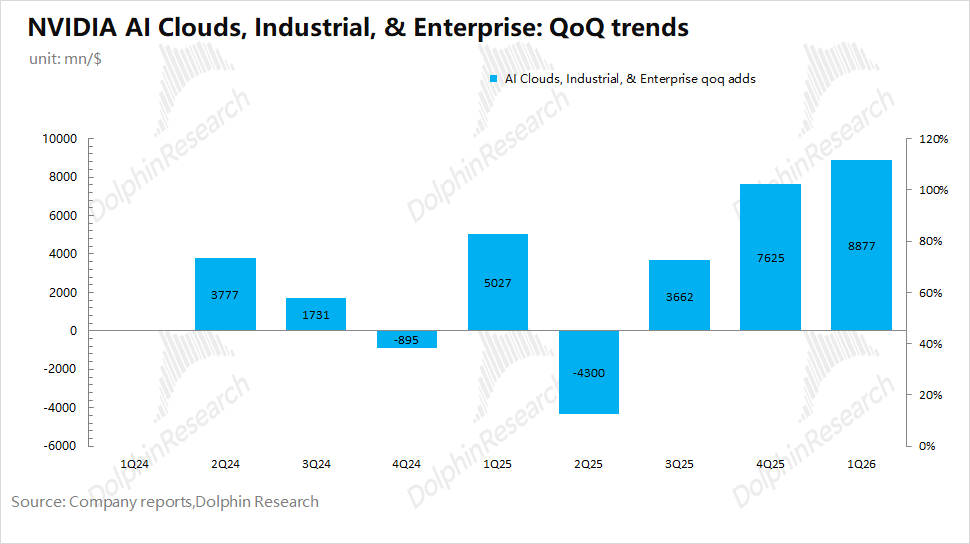

The company adjusted its disclosure approach this quarter, shifting from the previous breakdown of 'Computing and Networking' to 'Hyperscale and Other Cloud Customers.' Specifically, revenue from hyperscale customers reached $37.9 billion, up $4 billion sequentially, while revenue from other cloud customers hit $37.4 billion, a sequential increase of $8.9 billion, representing the largest growth contributor.

Given that major cloud providers are developing their own chips, Dolphin Research believes the company's decision to break down data center revenue by customer type aims to highlight its sustained growth capabilities in other cloud segments (industrial and government/enterprise clouds).

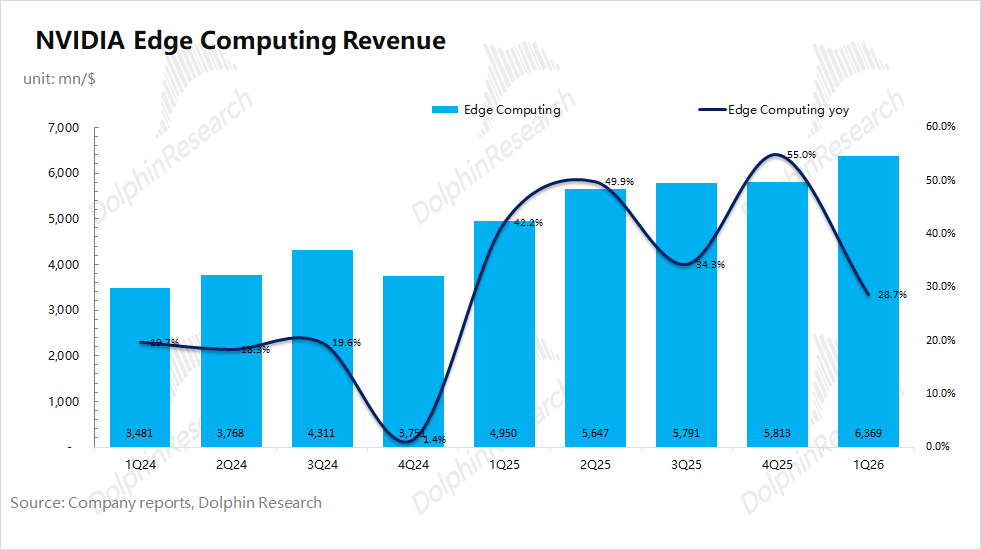

3. Edge Computing: This quarter, the company consolidated all non-data center businesses into edge computing, including personal computers, gaming consoles, workstations, AI-RAN base stations, robots, and automotive sectors, discontinuing separate performance disclosures.

Edge computing revenue reached $6.4 billion, up 29% year-over-year. The gaming business, the largest segment within edge computing, was the primary driver of growth this quarter.

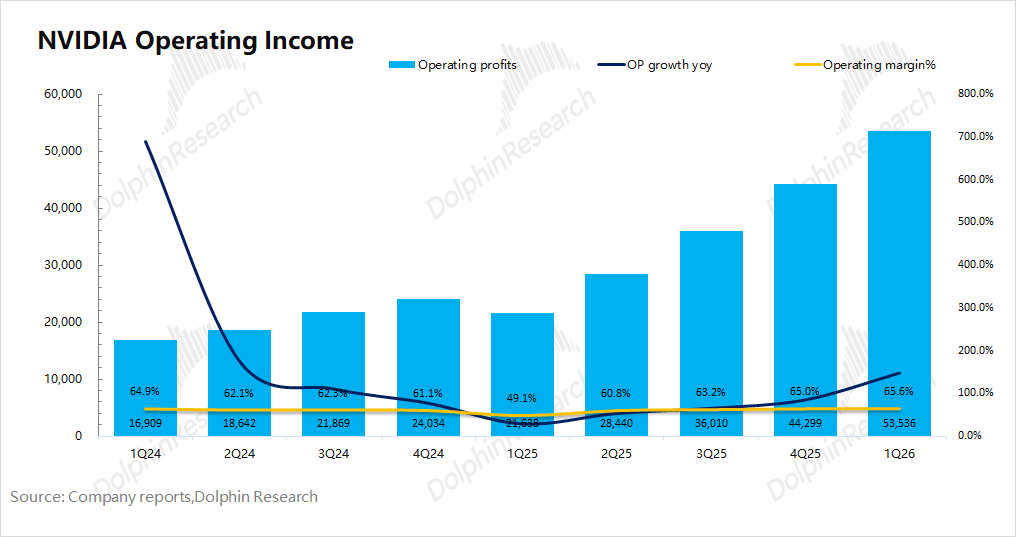

4. Profitability: Core operating profit reached $53.5 billion, up 147% year-over-year, benefiting from rapid revenue growth and a rebound in gross margin to around 75% (last year's 'collapse' was due to the H20 ban). Core operating profit margin reached 65% this quarter.

5. Next-Quarter Guidance: The company expects revenue of $91 billion for the second quarter of FY2027 (2Q26), up $9.4 billion sequentially, excluding China's data center computing revenue from guidance, surpassing upgraded buyer expectations ($89 billion). Gross margin (GAAP) is expected at 74.9%, flat sequentially, largely in line with market expectations (74.8%).

Dolphin Research's Overall View: The Computing Power Leader is Being 'Hunted' by 'Cost-Effectiveness'

Huang Renxun once again raised the company's AI business outlook at the GTC conference, projecting cumulative data center revenue to reach $1 trillion from 2025-2027 (up from $500 billion at last year's GTC). The market remains unconcerned about NVIDIA's performance in FY2027-2028. Thus, slight earnings beats in the short term are unlikely to significantly boost the stock price.

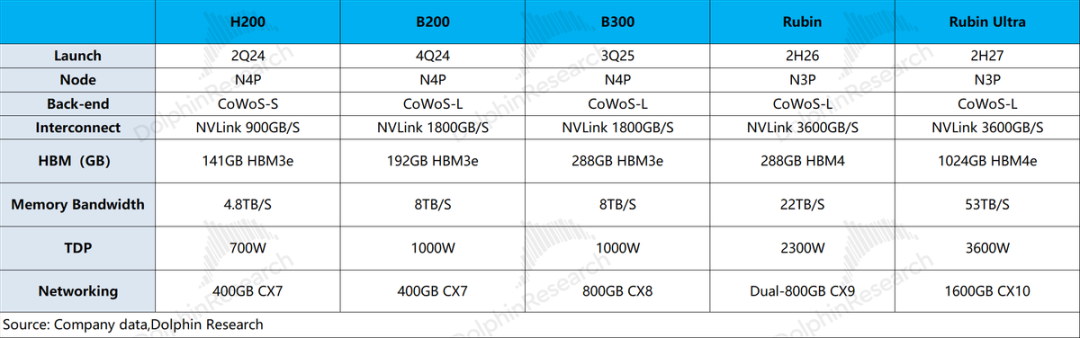

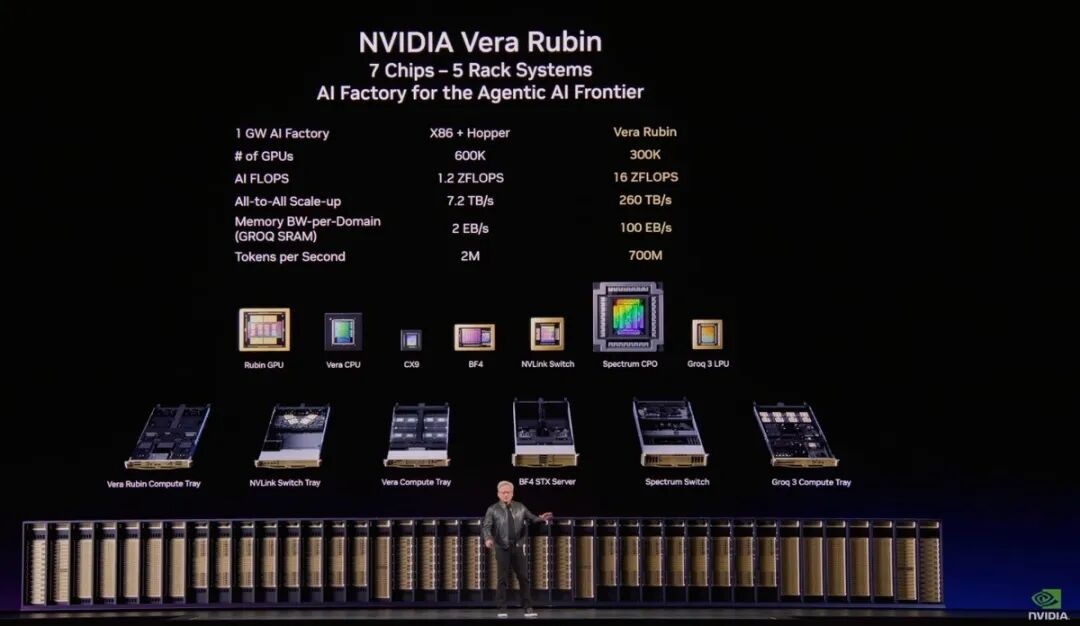

However, major players continue to increase capital expenditures, NVIDIA's AI chip market share keeps rising, and the company has introduced more Agentic workflow-compatible computing solutions in the Vera Rubin architecture:

a. Developed an in-house inference context memory platform (ICMS) to alleviate 'memory wall' issues;

b. Introduced Groq 3 LPU to accelerate decoding;

c. Utilized its in-house Vera CPU for task scheduling to enhance efficiency.

However, NVIDIA's monopoly premium is gradually weakening. When models are split into training and inference phases, NVIDIA maintains clear advantages in training. Post-training, inference requires repeated identical computations, prioritizing token throughput, latency, and cost—areas where major players' in-house chips aim to compete.

Especially as inference shifts from Chatbox to Agentic workflows—a current Harness engineering trend—pure computing bottlenecks diminish, while memory, CPUs, and cost-effectiveness become more pressing constraints.

In other words, NVIDIA's products and system-level solutions remain industry-leading by a wide margin. However, as AI technology advances to a stage where 'memory, CPUs, connectivity, and cost-effectiveness' become more critical and bottlenecked, and cloud providers have 'backup' options for inference computing, NVIDIA's unique training-era barriers and pricing power are weakening.

Of course, with industry beta tailwinds and Blackwell volume growth, NVIDIA is undeniably in a strong earnings-release phase. The stock price will naturally rise with Blackwell shipments and the launch of the more inference-market-compatible Vera Rubin in the second half of the year.

If Vera Rubin shipments exceed expectations, NVIDIA may still have room to grow. However, replicating the double-digit valuation (valuation) and earnings growth of the past two years will be challenging; 2026 may rely solely on EPS growth to support the stock price. A more detailed valuation analysis has been published in the Changqiao App's 'Insights-Deep Dive' section under the same article title.

Here's a detailed analysis:

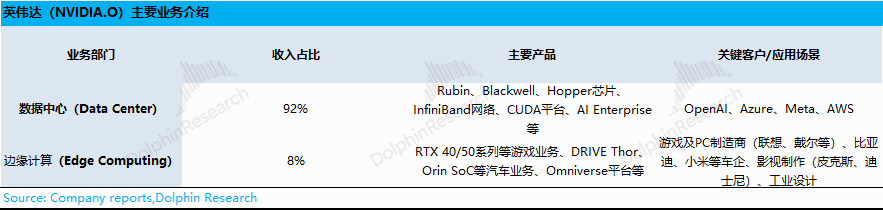

I. NVIDIA's Business Overview

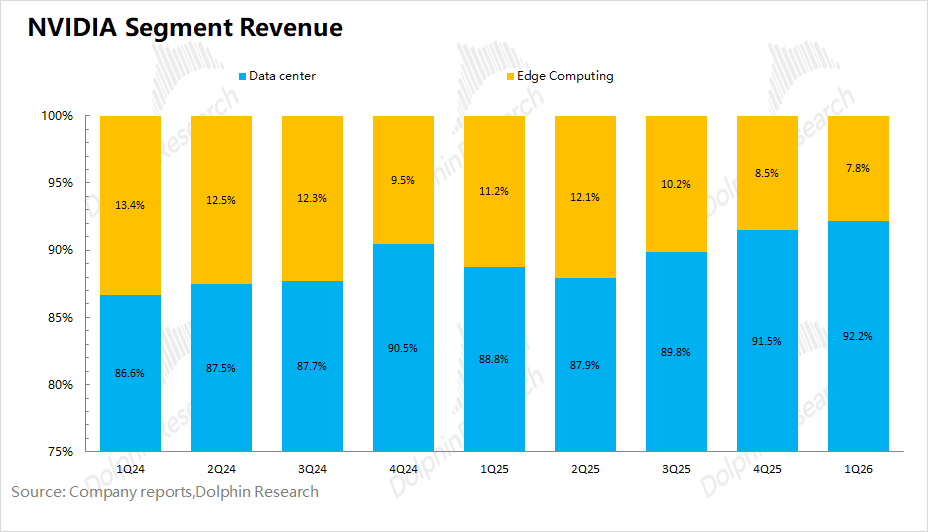

With sustained growth in NVIDIA's data center segment, it now accounts for over 90% of total revenue. This quarter, the company restructured its reporting by consolidating gaming, automotive, and other businesses into a new 'Edge Computing' segment, discontinuing separate disclosures.

Key business segments:

1) Data Center: The primary focus, featuring products like Blackwell computing chips and InfiniBand networking. Core customers include cloud giants Amazon, Microsoft, and Google.

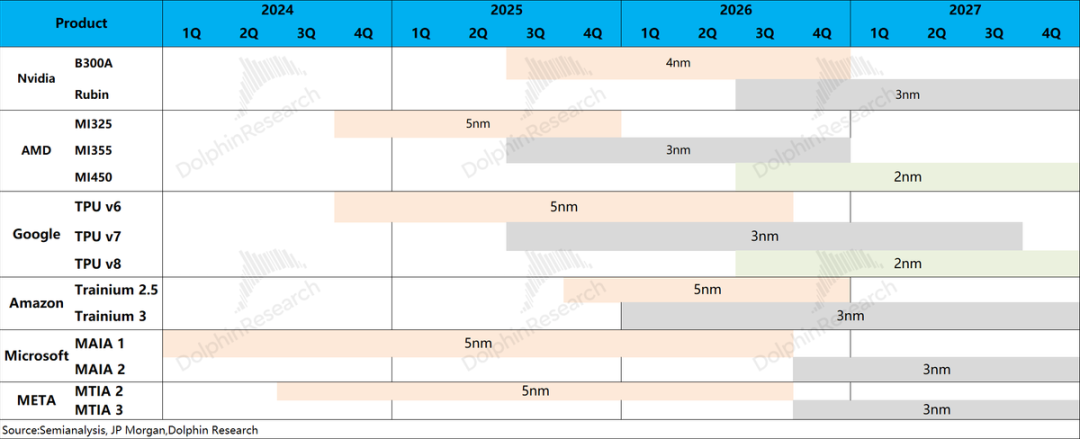

Currently, the data center business is in the Blackwell product cycle, with B300/GB300 as the main offerings. The product cycle will shift to the Rubin series following mass production in the second half of the year.

2) Edge Computing: Encompasses personal computers, gaming consoles, workstations, AI-RAN base stations, robots, and automotive sectors, with no separate disclosures for sub-segments.

The gaming business is the largest within edge computing, with current main products being the RTX40 and RTX50 series, targeting gamers and PC manufacturers.

II. Core Earnings Metrics: Slightly Exceeding Market Expectations

2.1 Revenue: In Q1 2027 (1Q26), NVIDIA reported revenue of $81.6 billion, up 85% YoY, surpassing upgraded buyer expectations ($78-80 billion). The $13.5 billion sequential increase was almost entirely driven by data center growth and Blackwell series volume ramp-up.

For next quarter, the company guides $91 billion in revenue, up $9.4 billion sequentially, exceeding upgraded buyer expectations ($89 billion). Growth will primarily come from B300/GB300, with Rubin new product (new products) entering mass production in Q3 2026.

2.2 Gross Margin (GAAP): In Q1 2027 (1Q26), NVIDIA achieved a gross margin of 74.9% (GAAP), largely in line with market expectations (75%). Last year's 'collapse' was due to the H20 ban.

For next quarter, the company expects a gross margin of 74.9% (GAAP), flat sequentially, meeting market expectations (74.8%). With Blackwell volume ramping up, margins have rebounded to around 75%.

Management previously mentioned a FY2027 target gross margin of 75%, providing some market confidence. However, concerns persist about margin erosion post-FY2027.

III. Core Business Progress: Cloud Customers Outside Major Players Drive Growth

Fueled by AI Capex, NVIDIA's data center business (Compute+Networking) now accounts for over 90% of revenue. Other businesses, collectively under 10%, were consolidated into edge computing this quarter and are no longer separately disclosed.

3.1 Data Center: In Q1 2027 (1Q26), data center revenue reached $75.2 billion, up 92% YoY. Growth was primarily driven by Blackwell series volume increases, fueled by accelerated computing and AI demand.

Breakdown: ① Computing revenue reached ~$60 billion, up $8.7 billion sequentially, with B300 shipments contributing the most; ② Networking revenue hit ~$15.1 billion, up $4.2 billion sequentially.

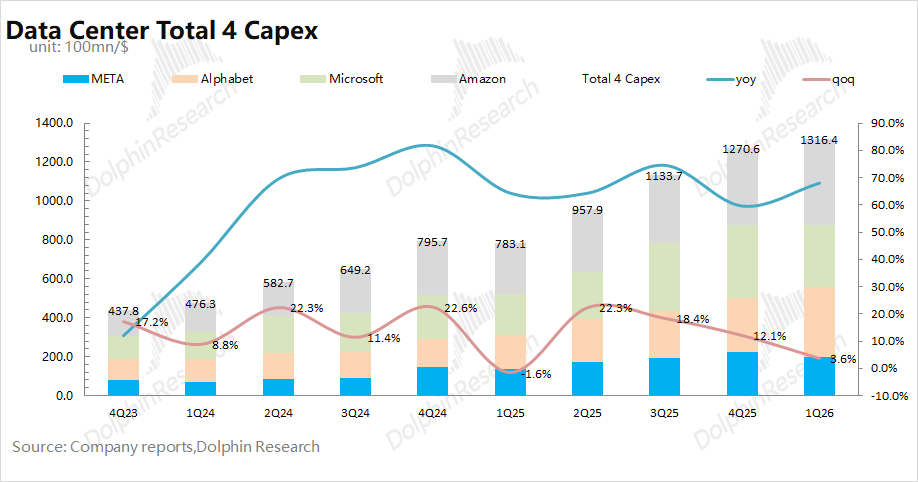

Cloud providers remain NVIDIA's largest AI chip buyers, with their CapEx forming the foundation of data center growth. Based on management commentary from four major players (Google, Meta, Microsoft, Amazon), Dolphin Research expects their combined 2026 CapEx to exceed $700 billion, up nearly 80% YoY, securing NVIDIA's FY2027 growth.

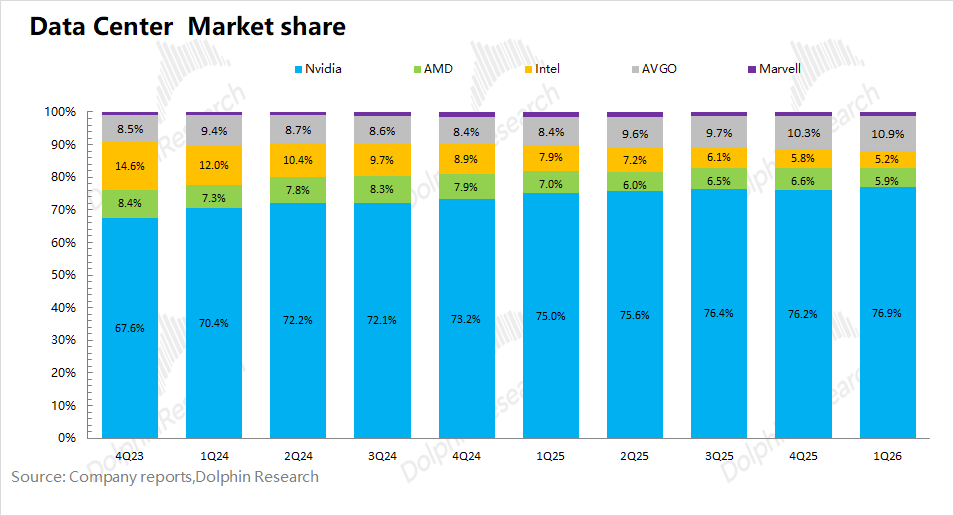

Beyond CapEx, the market is more concerned about competition from in-house ASICs. Key AI chip players include NVIDIA, 'Google+Broadcom,' and AMD, collectively holding over 90% market share. While NVIDIA GPUs dominate training, inference requires lower performance in some cases, making Google TPU and other in-house solutions more 'cost-effective.'

NVIDIA's high-margin chips absorb significant industry profits, impacting downstream economics. As inference gains importance, dependency on NVIDIA weakens, motivating major players to develop in-house chips or seek ASIC alternatives.

Amid this, NVIDIA adjusted its disclosure to highlight growth in industrial and government/enterprise clouds.

By customer type: Hyperscale revenue reached $37.9 billion, up $4 billion sequentially; other cloud revenue hit $37.4 billion, up $8.9 billion sequentially, representing the largest growth contributor.

Over the past two quarters, despite in-house chip development, NVIDIA has seen accelerated growth in government/enterprise and industrial clouds outside major players, showcasing its sustained growth potential.

The company's current gross profit margin has returned to around 75%. If its subsequent market competitiveness (market share) declines, it will, to a certain extent, bring about a "potentially adverse impact" on the company's gross profit margin. Previously, the company's management explicitly set a target gross profit margin of 75% for the fiscal year 2027, maintaining it at a high level. However, current mainstream institutions still anticipate a decline in the company's gross profit margin for the fiscal year 2028 and beyond.

3.2 Edge Computing Business: In the first quarter of the fiscal year 2027 (i.e., 1Q26), NVIDIA's edge computing business achieved revenue of $6.4 billion, a year-on-year increase of 29%, primarily driven by shipments of products such as the RTX 50 series in the company's gaming business.

With the proportion of data center business increasing to over 90%, the importance of other businesses is relatively low. Starting this quarter, the company has simply grouped them together under the broad category of "Edge Computing" and no longer discloses them separately.

Within the edge computing business, the gaming business is the largest segment, accounting for approximately 60-70%. Although the current PC and gaming markets are relatively sluggish, NVIDIA still maintains a significant leading advantage in the gaming graphics card market compared to AMD's gaming business, which generated quarterly revenue of $720 million.

IV. Key Financial Indicators: Steady Increase in Profit Margins Driven by High Growth

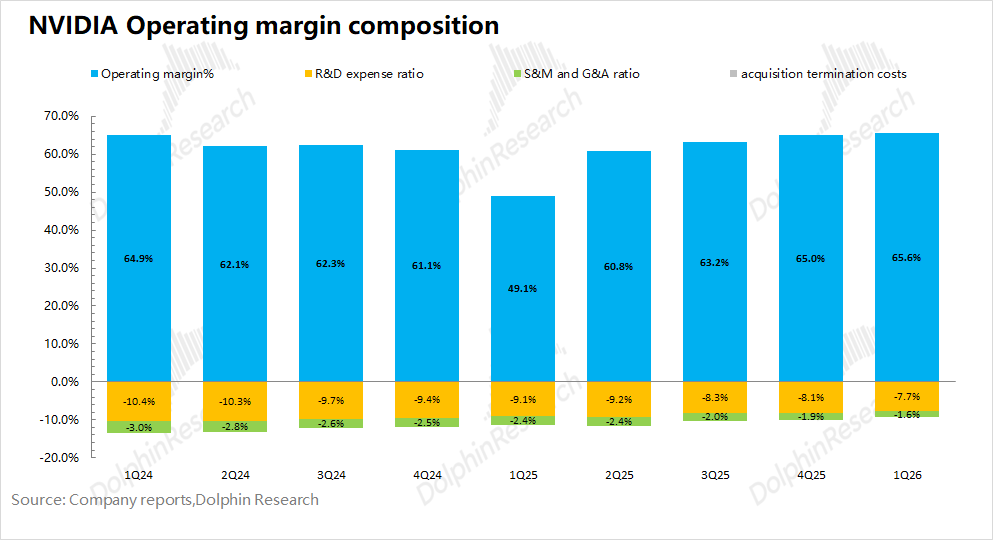

4.1 Core Operating Profit Margin

In the first quarter of the fiscal year 2027 (i.e., 1Q26), NVIDIA's core operating profit margin was 65.6%, showing a steady increase, primarily influenced by a decrease in operating expense ratios.

Analyzing the composition of the core operating profit margin, the specific changes are as follows:

"Core Operating Profit Margin = Gross Profit Margin - R&D Expense Ratio - Sales, Administrative, and Other Expense Ratio"

1) Gross Profit Margin: This quarter, it was 74.9%, a slight sequential decrease of 0.1 percentage points, maintaining around 75%.

2) R&D Expense Ratio: This quarter, it was 7.7%. Although the company's R&D investment increased by $800 million sequentially, the R&D expense ratio continued to decline due to rapid revenue growth.

3) Sales, Administrative, and Other Expense Ratio: During the Blackwell product cycle, the company's current sales and administrative expenses remained relatively stable, with this quarter's proportion in revenue decreasing to 1.6%.

The company expects the operating expense guidance for the next quarter to continue rising to $8.5 billion. Considering the revenue guidance, the operating expense ratio for the next quarter is expected to remain around 9.3%.

4.2 Core Operating Profit

In the first quarter of the fiscal year 2027 (i.e., 1Q26), NVIDIA's net profit was $58.3 billion, a year-on-year increase of 71%.

Since net profit is also affected by non-operating items, Dolphin Research pays relatively more attention to the company's core operating profit (gross profit - R&D expenses - sales, administrative, and other expenses). The company's core operating profit this quarter was $53.5 billion, a year-on-year increase of 147%. The core operating profit margin increased to 65.6%, primarily driven by revenue growth and a rebound in the gross profit margin (due to the H20 ban in the same period last year).

The company's current performance growth is primarily driven by the Blackwell product cycle. Combining the company's previously provided outlook for the data center business, with the mass production of the new Rubin product starting in the third quarter, the company is expected to maintain high growth in the fiscal years 2027-2028.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reprinting is only allowed with authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report must bear their own risks. Dolphin Research shall not be held responsible for any direct or indirect liabilities or losses that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available sources and are intended for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the relevant information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be considered or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for or proposed for distribution to jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials conflicts with applicable laws or regulations, or to citizens or residents of jurisdictions where Dolphin Research and/or its subsidiaries or affiliated companies are required to comply with any registration or licensing requirements in such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle