Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

06/08 2026

06/08 2026

432

432

Source | YuanMeiHui

Before Hong Kong investors could fully catch their breath from the recent market excitement, Beijing Zhipu Huazhang Technology Co., Ltd. (hereinafter referred to as "Zhipu") made a surprising announcement: the company plans to sprint for listing on the STAR Market of the Shanghai Stock Exchange, following a surge in its market value to HK$600 billion.

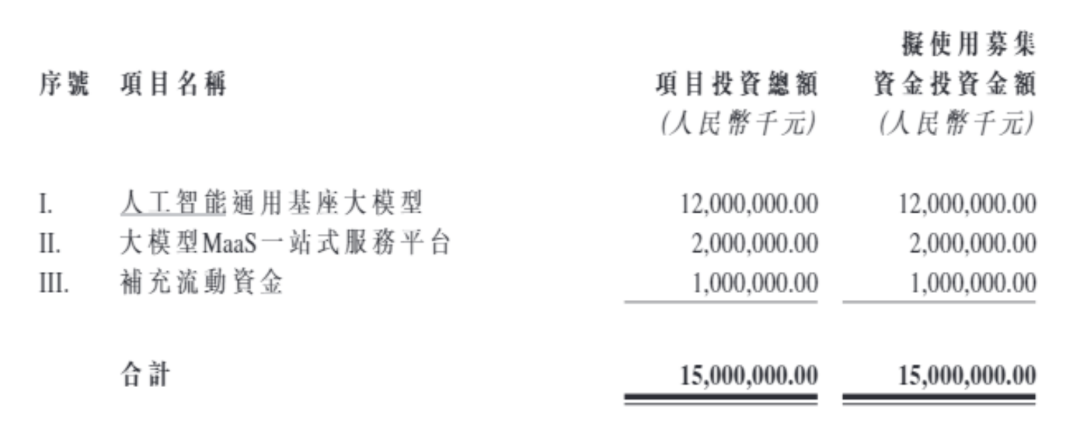

According to the announcement, Zhipu intends to issue no fewer than 9.0988 million and no more than 38.769 million new A-shares, aiming to raise RMB 15 billion. The funds will be allocated to general-purpose AI foundation models, a one-stop MaaS platform for large models, and supplementary working capital.

Image Source: Zhipu's Hong Kong Stock Exchange Announcement

The news caught the market off guard. After all, just six months earlier, Zhipu had been vigorously promoting its globalization narrative, with its market value soaring from hundreds of billions to briefly surpassing HK$600 billion. By all appearances, it should have capitalized on this momentum to solidify its position as the "First Large Model Stock" in Hong Kong. Yet, it chose to "return to A-shares" at this juncture.

More intriguingly, almost simultaneously, MiniMax also announced its plan to return to A-shares. The back-to-back pivots of these two AI stars have sparked curiosity: What signals are these new industry leaders picking up on?

01. OpenClaw's Turning Point and Zhipu's Pricing Confidence

Rewind to early 2026, when capital markets were skeptical about the growth potential of large models. The traditional low-Token-consumption Chatbot model struggled to sustain high valuations, trapping the industry in a "high-profile but unprofitable" dilemma.

The turning point came with the explosive popularity of the open-source project OpenClaw. It shifted models from passive Q&A to high-Token-consuming active Agent task execution, where model value was no longer measured by flashy responses but by task execution capabilities. Zhipu emerged as the most aggressive player in this wave.

On March 10, Zhipu launched AutoClaw, leveraging the OpenClaw ecosystem to become one of China's first service providers to achieve large-scale deployment of localized AI Agents. Observers noted that Zhipu was crafting a "hardcore" commercialization strategy on OpenClaw's ecosystem—borrowing open-source momentum while packaging it with localization and security features to directly tap into the enterprise market.

Just six days later, GLM-5-Turbo was released, with API prices raised by 20% alongside low-cost Token packages. Initially, the market reacted with skepticism: "Where does this pricing confidence come from?"

But stellar operating data soon validated Zhipu's confidence.

Zhipu CEO Zhang Peng disclosed at the 2025 earnings briefing that the company's API call pricing in Q1 2026 increased by 83% year-on-year. Despite the hike, overall call volume surged by 400%, with sustained undersupply in market demand. Coupled with product structure and service model upgrades, Zhipu's gross margin for cloud deployment services soared from a mere 3.3% in 2024 to 18.9% in 2025, marking a qualitative leap in profitability.

This rare industry phenomenon—simultaneous volume and price growth, with demand remaining resilient despite price hikes—was highlighted in a J.P. Morgan research report. The firm explicitly stated that Zhipu had established scarce market pricing power in high-value enterprise service scenarios. CICC subsequently raised Zhipu's target price, thoroughly refactoring the capital market's valuation logic for Zhipu.

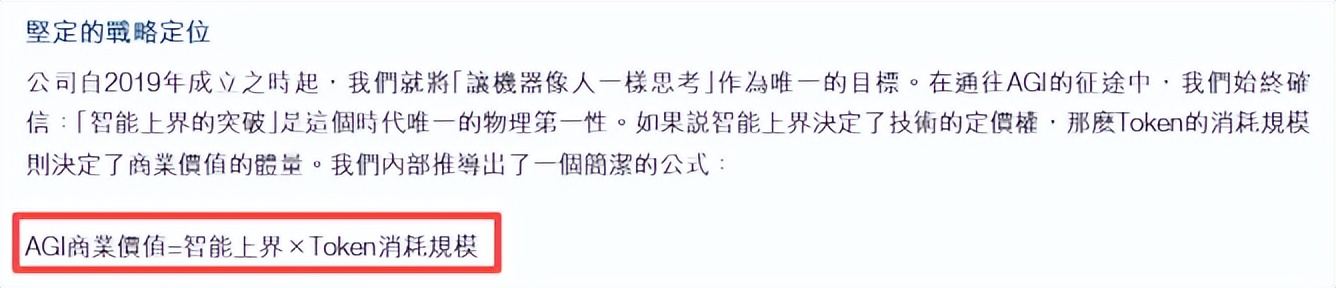

Summarizing this new commercial logic, Zhang Peng once used a precise formula: Commercial Value = Intelligence Ceiling × Token Scale.

In other words, the model's intelligence level sets the ceiling, while Token consumption acts as the channel to monetize that ceiling. APIs are the pathway to transform intelligence into tradable production factors.

What sounded like a slogan initially now forms a coherent capital narrative amid the exponential Token consumption driven by Agents.

Image Source: Zhipu's 2025 Financial Report

Once Zhipu's script of simultaneous volume and price growth proved viable, the market's imagination ran wild. Hot money began flooding in along the same logical chain—if Agents could revalue large models' commercial potential, Zhipu wouldn't be the only beneficiary.

Kimi became the first target pushed up by this sentiment.

Kimi's valuation has skyrocketed in recent times, with successive funding rounds of ever-larger amounts. Investors scrambled for shares in a "hop on first, ask questions later" manner. The logic is simple: Zhipu has proven that "price hikes can coexist with volume growth," so the market naturally believes front-runners in the Agent race can replicate this formula.

Latest Financing Status of Kimi from Tianyancha

Even DeepSeek, typically "flush with cash" and indifferent to external financing, quietly opened its financing window.

Backed by quantitative giant Fantuan, DeepSeek has long been known for its ample funding and had consistently signaled "no need for financing." However, in the face of industry paradigm shifts triggered by OpenClaw, "not short of money" and "not needing financing" became two distinct concepts. The exponential Token consumption driven by AI Agents directly fueled explosive growth in inference computing demand. Even with deep pockets, DeepSeek needed to stockpile resources and expand capacity in advance.

Viewed through this lens, Zhipu's revaluation and HK$600 billion market cap weren't purely sentiment-driven. Behind them lay a fundamental transformation in the large model industry—from storytelling based on Q&A traffic to earning real profits through execution.

OpenClaw inadvertently became the key fuse igniting market sentiment.

02. The 'Hidden Agenda' Behind Zhipu's Timely Return to A-Shares

Against this backdrop, Zhipu's abrupt "U-turn" to return to A-shares seems less sudden.

In fact, before listing in Hong Kong in 2025, Zhipu had initiated IPO counseling for the STAR Market but later voluntarily suspended it, likely due to persistent losses and an unclosed business model.

At the time, domestic large model firms generally relied on a "burn money for scale" growth model, with weak profitability and unclear commercialization paths. A-share capital markets had lower tolerance for valuing unprofitable tech firms, while Hong Kong's lax listing rules and international capital environment made it the optimal interim choice for Zhipu.

But the AI Agent boom completely rewrote Zhipu's fundamentals and valuation narrative.

Long-chain tasks with high Token consumption transformed large model services from per-session chat tools into consumption-based digital productivity. Gross margins surged, API revenues scaled, and even rare user stickiness emerged—where price hikes didn't dampen demand.

This was no longer a pure cash-burning internet story but resembled infrastructure businesses like water or electricity supply—bearing some "public utility" attributes while erecting barriers through intelligence ceilings. This hard-tech coloration precisely aligns with the STAR Market's preferred narrative.

Another nuance is that Hong Kong's pricing power remains heavily influenced by overseas funds, with geopolitical risks occasionally discounting valuations. Meanwhile, Zhipu's current client base includes numerous local government and critical industry Agents with stringent data security and localization requirements. The "domestic substitution" concept commands far higher emotional premiums in A-shares than in Hong Kong.

Simply put, the same high-Token-consumption story could fetch a higher and more stable valuation on the STAR Market than in Hong Kong.

Moreover, policy layers are paving the way for Zhipu's return to A-shares.

Regulators are continuously relaxing listing thresholds for unprofitable hard-tech firms, fully supporting the development of new quality productivity industries represented by large models and AI Agents. Zhipu's return, armed with stellar Q1 call data, pricing power advantages, and improved profitability, precisely addresses the commercialization gaps that hindered its previous STAR Market bid.

Beyond that, Zhipu's abrupt pivot may stem from a more pragmatic strategic consideration—competing for the title of "First Large Model Stock" on A-shares.

Currently, no pure large model company is listed on the STAR Market. The first to do so would gain an edge in pricing power and brand recognition. Zhipu clearly doesn't want to cede this opportunity to Kimi or other eager rivals.

While market sentiment remains high, Zhipu hopes to swiftly complete fundraising to stockpile ammunition for the next tech cycle—understandable given that despite its HK$600 billion market cap, Zhipu hasn't resolved its loss-making issue, and the pressure of continuous cash burn is real.

More critically, DeepSeek and Xiaomi have driven API prices to rock-bottom levels, with the risk of further price erosion mounting. Once the pricing logic fueled by Agents is undermined by aggressive cost-cutting, the sustainability of Zhipu's current high gross margins remains uncertain. Thus, completing its A-share return financing before strong rivals list serves both as a positioning move and a risk hedge.

Coincidentally, MiniMax announced its A-share return around the same time, confirming this isn't an isolated case.

As the Agent model scales large models' commercial value to Token consumption levels, these AI new elites realize that instead of competing with global giants in overseas markets, they should return to A-shares—where local scenarios are best understood and willingness to pay for execution capabilities is highest—to anchor the "Token as productivity" valuation first.

However, some market voices question Zhipu's "hasty" return to A-shares at peak valuations, but capital markets always remain loyal to core logic.

When AI Agents achieve order-of-magnitude jumps in Token consumption, when the "intelligence ceiling × Token scale" formula translates into tangible revenue, gross margins, and pricing power, and when industry-wide valuations undergo systemic upgrades, Zhipu needs a pool that offers sufficient premiums for this new type of production factor.

And the STAR Market is likely that pool.

Note: Some images in the text are AI-generated/sourced from the internet. Please notify us for removal if any infringement occurs.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once