Behind SpaceX's IPO: Musk, Boasting a Trillion-Dollar Net Worth, Still Grapples with a Severe 'Cash Crunch'

06/23 2026

06/23 2026

512

512

When the news surfaced that SpaceX was poised for a Nasdaq listing, the market reacted with keen interest. Subscriptions soared past $250 billion, marking an oversubscription rate exceeding fourfold. As of the press deadline, SpaceX's market capitalization has surged beyond $2.5 trillion.

Yet, amidst the excitement, a compelling truth emerges: Musk may not have taken SpaceX public because it was 'ripe' for listing, but rather because his sprawling 'business empire' is facing an acute cash shortage.

01. The Cash-Draining Giants Within the Empire

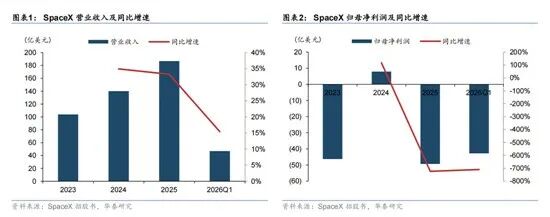

Delve into SpaceX's prospectus, and a startling revelation awaits: Despite being valued at over $2 trillion, the company reported a staggering net loss of nearly $5 billion in 2025.

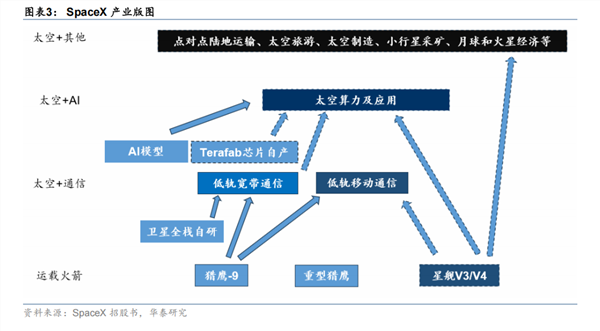

Only Starlink has managed to turn a profit, generating $11.4 billion in revenue and $4.4 billion in operating profit, single-handedly propping up the company's cash flow. While the rocket launch business has proven its mettle with Falcon, the colossal R&D investment in Starship keeps it in the red. Meanwhile, the AI venture xAI raked in $3.2 billion in revenue but suffered a nearly $6.4 billion loss, nearly erasing Starlink's entire profit.

The cash burn rate of Starship is particularly alarming. SpaceX has funneled over $15 billion into this project, with expenditures reaching approximately $3 billion in 2025 alone—double the previous year's outlay.

Beyond Starship, nearly every business under Musk's umbrella is a voracious consumer of cash. For instance, xAI opted for the most expensive route: constructing its own computing infrastructure. The 'Colossus 1' supercomputing cluster, boasting 230,000 GPUs, has incurred hardware costs that soar to astronomical levels. Neuralink, since its inception in 2016, has raised over $1.3 billion, achieving a $9 billion valuation after a $650 million Series E funding round in 2025. However, it remains mired in clinical trials, with each unit costing $40,000 and widespread adoption still a distant dream.

It's akin to navigating a canoe on a tightrope: Starlink toils relentlessly to fill the bottomless pits of Starship and xAI, while Neuralink stands nearby, its hand outstretched for more funds.

02. Cash Burn Isn't Losing Control—It's the Ultimate Moat

One might wonder: Why not adopt a more cautious approach? Why not expand only after securing profitability? The answer lies at the core of Musk's business philosophy.

Because in every sector he ventures into, not burning cash spells doom. Rocket launches, low-Earth orbit satellite internet, artificial general intelligence, brain-computer interfaces—these fields share a common trait: exorbitant fixed costs, minimal marginal costs, and a winner-takes-all dynamic. Whoever achieves technological breakthroughs and scales first can permanently shut out latecomers. Anyone lagging behind is effectively out of the race.

Consider rocket launches first. Traditional giants like ULA charge hundreds of millions per launch. SpaceX's Falcon 9 slashed prices to around $60 million, and now reports suggest single-launch costs have plummeted to about $15 million—a nearly 75% reduction. This feat was accomplished through reusable technology—developed over a decade, through hundreds of tests, and countless explosions.

Starship aims to reduce payload costs per kilogram to below $200. Once achieved, all disposable rockets globally will struggle to compete. But before that, SpaceX must absorb tens of billions in R&D and test flight costs. This is 'buying barriers with blood': If you dare burn through the money first to perfect the technology, no one can engage you in a price war later.

Starlink's business model is even more straightforward. Low-Earth orbit satellite internet is a 'constellation density race.' SpaceX has over 10,000 satellites in orbit, while rivals OneWeb and Amazon's Kuiper lag by orders of magnitude. Why so many? Because orbital and frequency resources are 'first come, first served,' and only with sufficient density can ground terminals become compact and low-cost. Starlink now boasts over 10 million users, generating positive cash flow. But to maintain its lead, SpaceX must launch over 1,000 new satellites annually. Competitors who want to catch up must either build their own launch capabilities (costing tens of billions and a decade) or rely on third-party rockets (at double the cost). Starlink's moat isn't patents—it's 'I've already spent $30 billion, and competitors lack the courage to follow.'

xAI adheres to the same logic. Training large models is an arms race in computing power. xAI's decision to build its own supercomputing cluster and purchase 230,000 GPUs may seem extravagant, but Musk's rationale is clear: Long-term reliance on cloud computing would lead to spiraling rental costs as usage grows. Self-built computing power is a capital expense—once completed, marginal costs plummet. It's akin to the difference between renting and buying a home: Renting means endless monthly payments, while buying requires a hefty upfront cost but becomes cheaper over two decades. xAI is betting that AI inference will become a utility like electricity and water, where only those with proprietary computing power can set prices. Until then, whoever first pushes their model close to artificial general intelligence thresholds will capture most of the market. Everyone else gets the leftovers.

Neuralink, though smaller in scale, operates on the same principle. Brain-computer interfaces require year-over-year, billion-dollar investments to build technical barriers. Once Neuralink achieves FDA long-term approval, latecomers will need 5–10 years to replicate clinical processes. This time gap is an invaluable moat.

Thus, Musk isn't a reckless spender. He knows full well: Every dollar spent is fertilizer for his moat. Today's massive losses are tickets to future monopoly status.

03. SpaceX's IPO: A Lifeline for the Empire, a 'Cash-Out' for Musk

But this strategy harbors a fatal flaw: It demands a constant influx of cash. If funding dries up, not only will moat construction halt, but even existing defenses may crumble from neglect.

A closer examination of SpaceX's IPO reveals a hint of 'forced listing.' All shares are newly issued, with proceeds going directly to the company—the most efficient 'lifeline' SpaceX could secure. While Starlink generates revenue, Starship and xAI's losses devour all profits.

For Musk personally, ownership of a public company offers greater flexibility: He can pledge SpaceX shares for liquidity to support other ventures, avoiding forced Tesla stock sales as in the past.

04. Conclusion: It's Not That He Doesn't Want to Wait—He Can't

Some may inquire: Why not wait until Starlink is more profitable and xAI turns a corner before going public? The answer is harsh: He can't afford to.

SpaceX now teeters on a precarious balance: Starlink toils relentlessly to offset Starship and xAI's massive losses. Goldman Sachs predicts xAI's revenue will surge from $3.2 billion in 2025 to $322 billion by 2030—but this hinges on xAI not falling behind OpenAI and Anthropic in the AI race. To stay competitive requires constant purchases of advanced GPUs, expansion of computing power, and model iterations—each step demanding billions.

It's like riding a unicycle on a tightrope: You can't stop, but you can't go too fast either. Stopping lets rivals overtake; going too fast risks breaking the chain.

Investors flocking to SpaceX's IPO are essentially paying for the 'Space + AI' grand narrative. But how much of this story will materialize depends on whether Musk has enough money to finish the blueprint. And on this point, he knows his weakness better than anyone—precisely because he's short on cash, he must go public; precisely because he's short on cash, he must push SpaceX's valuation to $1.77 trillion; precisely because he's short on cash, this unprecedented 'Planetary IPO' must proceed. The business model in his hands is essentially a high-stakes bet on the future: betting he can trade present money for time others can't buy, betting every moat he burns will be deep enough to despair rivals.

- End -

-

![]()

【OFweek Weike Cup】Fair Optics Officially Nominated for 2026 Outstanding Contribution Award in Optical Industry Application Solutions

-

![]()

The Competitive Landscape of Financial AI Agents in the 'Long Tail' Market: FinTech Subsidiaries, Financial Leasing, Consumer Finance, AMCs, and Other Players Making Quiet Strides

-

![]()

【OFweek Weike Cup】Fair Optical Officially Enters for the 2026 Optical Industry Annual Innovation Product Award

-

![]()

【OFweek Weike Cup】Wuhan Changjin Photonics Nominated for 2026 Optics Industry Outstanding Component Supplier

-

![]()

【OFweek Weike Cup】Xinyuan Optics Officially Enters for the 2026 Outstanding Contribution Award for Advanced Manufacturing Process Solutions in the Optical Industry

-

![]()

Who Dominates the World Cup: Lenovo, Hisense, or Mengniu?

-

![]()

【OFweek Weike Cup】Shijia Photonics Participates in the 2026 Excellent Optical Component Supplier Award

-

![]()

【OFweek Weike Cup】Dingxinsheng Optics Officially Enters for the 2026 Optical Industry Annual Innovation Product Award