Why Does Kunlunxin Opt for a "Live-Streaming-Inspired IPO" Approach?

07/03 2026

07/03 2026

518

518

Edited by Sun Jing

On June 29, Baidu experienced a much-anticipated rebound in the capital markets. By the pre-market trading session on July 1, Baidu's Hong Kong-listed shares had surged by 11% over the preceding two days.

The driving force behind this capital market rally was Baidu's AI chip subsidiary, Kunlunxin. According to The Information, Kunlunxin is planning to go public in Hong Kong with a target valuation of approximately $50 billion, significantly surpassing Baidu's current market capitalization of around $36 billion.

What makes this valuation even more intriguing is the unique subscription method reported for this IPO. As per The Information, potential investors are required to purchase chips worth three to seven times their subscription amount. This "allocation" requirement is notably substantial.

"It's quite rare for AI chip companies to screen investors in this manner during the IPO phase," a senior chip investor commented to NoNoise.

This strategy appears to blend equity subscriptions with product procurement, even resembling a "live-streaming-inspired IPO." However, interpreting it merely as securing orders before listing to bolster valuation might oversimplify Baidu's intentions.

The investor disclosed to NoNoise that the "procurement + subscription" model was only discussed during roadshow communications and was not a mandatory condition. "There's no fixed timeline or amount for procurement; it's more of a strategic arrangement," the investor explained.

Regarding the rationale behind this approach, the investor believes Kunlunxin aims to identify investors with sustained procurement capabilities rather than purely financial backers.

Firstly, Kunlunxin enjoys a relatively strong market position.

Currently, the AI chip market is experiencing supply-demand tensions, with accelerated adoption of domestic computing power. "Leading domestic AI chip companies like Kunlunxin are facing both tight capacity and robust demand. To some extent, the 'procurement + subscription' model offers benefits to its investors," the investor noted.

As previously mentioned in NoNoise's article "It's Tough to Be China's NVIDIA," domestic chips such as Huawei's Ascend 910 have encountered shortages. Cambricon's contract liabilities surged from RMB 1 million at the end of 2025 to RMB 396 million in Q1 2026, reflecting strong demand.

This trend is mirrored in Kunlunxin's performance. According to investment bank research, Kunlunxin's revenue reached approximately RMB 2 billion in 2024, with a net loss of around RMB 200 million. Revenue is projected to grow to RMB 3.5 billion in 2025, potentially achieving break-even, and could reach RMB 6.6 billion in 2026.

IDC data reveals that in the 2025 Chinese cloud AI accelerator market, Kunlunxin shipped 116,000 units, tying with Cambricon for third place among domestic vendors, trailing only Huawei's Ascend and Alibaba's T-Head in domestic AI chip shipments.

▲2025 Ranking of Domestic AI Accelerator Card Shipments in China

Source: IDC | Chart: NoNoise

From a stability standpoint, Cambricon's major client, ByteDance, is developing its own chips, which could introduce volatility in Cambricon's shipments. T-Head's AI chips primarily serve external clients indirectly through Alibaba Cloud. If Kunlunxin can secure more external orders through its IPO, it may achieve a more competitive market position.

Secondly, Kunlunxin needs external customers more than capital to demonstrate its independence.

Kunlunxin originated from Baidu's intelligent chip and architecture department. Upon completing independent financing and spinning off from Baidu in April 2021, it was valued at RMB 13 billion. However, as a Baidu-incubated AI chip product, Kunlunxin initially relied heavily on Baidu's internal demand for orders. While this allowed it to bypass some external market validation and scale faster, it also raised concerns about over-reliance on Baidu.

Thus, Kunlunxin needs to showcase sustained procurement interest from clients outside Baidu.

Going public is a strategic move for Kunlunxin to dilute Baidu's influence, while the "procurement + subscription" model strengthens the narrative of external customer engagement during the IPO process.

Publicly available information indicates that Kunlunxin has been accelerating its efforts to acquire external customers in recent years. Investment bank data shows that around 40% of Kunlunxin's 2025 revenue came from external clients. In November 2025, Shen Dou, president of Baidu Intelligent Cloud, revealed that Kunlunxin had over 100 clients, including China Merchants Bank, China Southern Power Grid, Geely Automobile, vivo, a major internet company, and a top-tier operator, with delivery scales ranging from dozens to tens of thousands of cards.

The internet giant was later identified as Tencent, and the operator as China Mobile. Tencent's open approach and delayed AI strategy are interconnected, while operators have a rigid demand for domestic computing power.

Notably, in 2025, China Mobile awarded Kunlunxin an inference chip order exceeding RMB 1 billion. In July of the same year, China Mobile's subsidiary, China Mobile Innovation, appeared among Kunlunxin's Series D investors, indicating that Kunlunxin had previously tested the feasibility of the "procurement + subscription" model.

For these clients, participating in Kunlunxin's subscription is also a strategic industrial layout around the domestic computing power supply chain.

Furthermore, the "procurement + subscription" model could create mutual benefits. If Kunlunxin performs well post-IPO, industrial investors may gain financial returns in the capital markets. Meanwhile, by procuring chips, these industrial players channel computing demand into Kunlunxin's revenue system. New orders raise expectations for revenue growth, further bolstering confidence in valuation, forming a virtuous cycle of "share subscription—procurement orders—revenue growth—valuation appreciation."

From a broader perspective, over the past two years, more AI industry transactions have adopted a "circular investment" model: chip companies invest in clients, who reciprocate by purchasing chips; cloud providers partner with large model companies, which then buy cloud computing power. Capital, orders, and capacity are integrated into a single growth flywheel.

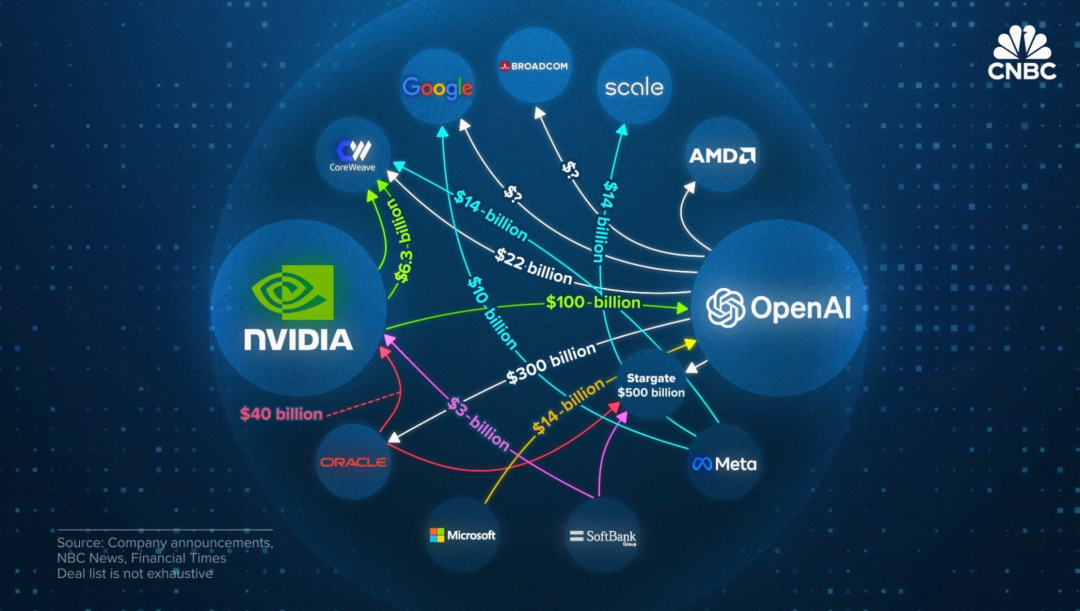

For instance, NVIDIA's investments, computing procurement, chip supply, and cloud service orders with companies like OpenAI and Microsoft are intertwined, forming an AI computing power interest network. AMD has also reached agreements with OpenAI, Meta, and others linking hardware sales to equity allocations. Before SpaceX's IPO, it was reported to have required underwriting banks or specific investors to purchase enterprise services for its Grok AI model.

▲U.S. AI Industry Trillion-Dollar Capital Transaction Network | Source: CNBC

These agreements bind upstream and downstream players through orders, amplifying demand, revenue, and valuation across the ecosystem.

While such formal bindings have yet to emerge in China's AI industry, alliance trends are evident. For example, SenseTime's "Xiwang" is backed by investors like Sany Group's Huaxu Fund, Fourth Paradigm, and Midea Holdings. Moore Threads' industrial investors include Tencent, ByteDance, Lenovo Capital, and Pony.ai.

From an industry trend perspective, Kunlunxin's approach of binding "capital + orders" during the IPO phase may set a precedent for subsequent Chinese AI chip companies planning to go public.

For Kunlunxin itself, in the short term, order releases, delivery cycles, and revenue recognition around the IPO will continue to support its valuation imagination.

However, long-term success hinges on the product itself. "The key is Kunlunxin's performance in application scenarios—how it performs across different scenarios and models varies, and it's difficult for outsiders to fully assess Kunlunxin's true capabilities based solely on public parameters," the aforementioned chip investor noted.

▲Kunlunxin's Current Product Matrix

Another implicit risk lies in the market itself. While interest bundling in the AI chip supply chain accelerates the industry's virtuous cycle, it also amplifies risks. Problems at any link in the chain can trigger systemic repercussions. The investor cautiously reminded that many U.S. investors have warned of an impending AI bubble peak. "There's definitely a bubble in China's AI market; it's just a matter of when it bursts."

Regardless of the future, Kunlunxin's IPO at this juncture is positive news for Baidu.

When Kunlunxin spun off, Baidu retained a 57% stake. If the reported $50 billion valuation materializes and procurement orders are locked in early, Baidu's own valuation will gain a new narrative.

Baidu is currently transitioning from a traffic distribution company to an AI infrastructure platform. Search has long been Baidu's valuation anchor, but during its business model transformation, Baidu's AI business has yet to justify a high valuation—its proprietary large models and AI applications have failed to maintain early advantages. While Baidu Intelligent Cloud is growing rapidly, the pace hasn't excited capital markets. The Robotaxi business under Luobo Kuaipao remains far from profitability and is highly policy-dependent. In contrast, the under-the-radar Kunlunxin is closer to a turnaround, finally giving Baidu's long-touted "chip-cloud-model-application" strategy new credibility.

From this perspective, the "live-streaming-inspired IPO" is both Kunlunxin's proactive lock-in of growth potential and Baidu's urgent need to "stand tall."

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan