The U.S. Edges Toward Oligopoly in AI, While China Dives into a Competitive Frenzy

07/10 2026

07/10 2026

554

554

Over the past two years, the large model industry has been wrestling with a pivotal question: Will large models, akin to cloud computing, eventually be dominated by a select few platforms?

At least for the present, China and the U.S. are providing two vastly different answers to this query.

In the U.S., the competition for large models is swiftly approaching a consolidation phase. A discernible trend is emerging where disparities in model capabilities are rapidly translating into gaps in commercial revenue. OpenAI and Anthropic have already secured the lion's share of revenue, making it increasingly arduous for other model companies to bridge the gap.

In stark contrast, the competition for large models in China presents an entirely divergent scenario.

Not only has the number of participants not dwindled, but it is, in fact, on the rise. On the text rankings of the international large model arena LMArena, Chinese companies constitute as many as 11 out of the top 20 labs.

Capital flows further corroborate this observation. On one hand, internet behemoths such as Alibaba and ByteDance continue to ramp up their AI investments and develop proprietary models. On the other hand, investors are still placing bets on large model startups.

Including the latest funding round of Zhipu, the cumulative financing scale of leading domestic large model startups has surpassed 130 billion yuan so far this year.

Facing the same AI wave, why has the competition for large models in the U.S. started to converge, while China's models are still embroiled in a chaotic frenzy? This divergence stems from two fundamentally different industrial logics.

/ 01 / U.S. Large Model Competition Consolidates, While China Remains in a "Feudal Free-for-All"

Over the past six months, the most prominent trend in large models in the U.S. has been differentiation.

Differences in model capabilities are swiftly translating into disparities in commercial revenue, with leading models capturing the vast majority of income.

Data previously released by Menlo Ventures indicated that in 2025, Anthropic and OpenAI together accounted for only 67% of enterprise LLM API spending.

This year, that proportion has surged significantly. According to a May report by The Information, among the 34 leading AI startups it tracked, OpenAI and Anthropic have already captured 89% of the revenue.

Particularly for new customers, nearly all are gravitating towards the leading players. Axios, citing Ramp data, stated that among enterprises purchasing AI products for the first time, Anthropic has captured over 73% of the spending.

The revenue differentiation in models has propelled leading model companies into a virtuous cycle: superior models lead to stronger commercialization, which in turn fuels model R&D. Coupled with the self-reinforcing cycle of AI accelerating AI R&D, this means the iteration speed of leading models will continue to accelerate.

Currently, leading models have essentially entered a rhythm of upgrades every 1-2 months.

OpenAI released GPT-5.1 in November 2025, followed by GPT-5.2 in December, and then GPT-5.3-Codex, GPT-5.4, and GPT-5.5 in February, March, and April 2026, respectively.

Anthropic's pace has also noticeably quickened. Claude Sonnet 4.6 was released in February this year, followed by Opus 4.7 in April, Opus 4.8 in May, and Fable 5 and Mythos 5 in June.

Under these circumstances, the competitive focus of overseas model companies has also begun to shift.

For instance, Musk's xAI recently unveiled Grok 4.5, placing greater emphasis on cost efficiency compared to its predecessors. According to calculations by Artificial Analysis, the cost of Grok 4.5 completing a single task is nearly 90% lower than models ranked ahead of it on the leaderboard.

In contrast to the consolidation of competition for large models abroad, the battle over large models in China is far from over.

If we examine the two largest global model capability rankings, China still boasts the most competitors. On the text rankings of the international large model arena LMArena, Chinese companies account for 11 out of the top 20 labs.

Artificial Analysis' Intelligence Index yields similar findings.

There are 99 models with an intelligence score exceeding 20, originating from 25 companies, of which 12 are Chinese companies, including DeepSeek, Baidu, Zhipu, Tencent, China Mobile, Yuezhi'anmian, Ant Group, Xiaomi, MiniMax, Alibaba, StepFun, and ByteDance.

Compared to model releases, capital flows offer a more accurate reflection of the competitive landscape of domestic large models.

On one hand, internet giants remain steadfast in increasing their AI investments.

Last year, Alibaba announced that it would invest over 380 billion yuan over the next three years to construct cloud and AI infrastructure. At this year's May earnings call, management further stated that the scale of AI investment would exceed previously planned levels.

ByteDance has also elevated its AI capital expenditure plan for 2026 to 200 billion yuan. Tencent similarly plans to continue augmenting its AI investments, with management clearly stating that it will continue to enhance the capabilities of its Hunyuan large model.

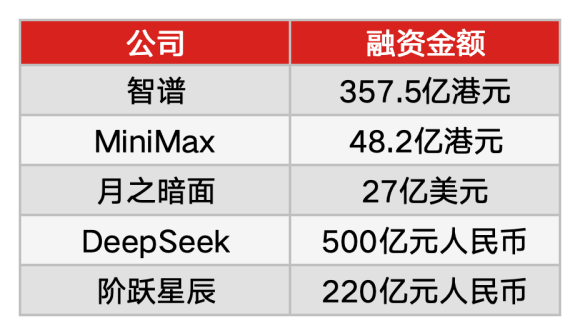

On the other hand, investors are still persistently increasing their bets on large model startups. Including the latest funding round of Zhipu, the cumulative financing scale of leading domestic large model startups has surpassed 130 billion yuan so far this year.

Among them, DeepSeek has raised approximately 50 billion yuan in cumulative financing; Zhipu has raised 35.75 billion Hong Kong dollars; Yuezhi'anmian has raised approximately 2.7 billion U.S. dollars; StepFun has raised approximately 22 billion yuan; MiniMax has raised approximately 4.82 billion Hong Kong dollars.

The fact that the primary market is still willing to continue betting signifies that capital still believes that the ultimate victor in the industry has yet to emerge.

In the AI wave, why has the competition for large models, which commenced almost simultaneously at home and abroad, veered in two entirely different directions?

/ 02 / Transforming Large Models into Building "Electric Vehicles"

To address this question, we must revisit the origins of the mobile internet.

In August 2011, Marc Andreessen penned his famous prediction in The Wall Street Journal: "Software is eating the world," heralding the dawn of the mobile internet era.

Since then, the internet in China and the U.S. has followed two diametrically different paths.

In the U.S., "software" propelled the wave of consumer applications, driving a comprehensive explosion in SaaS entrepreneurship. Between 2010 and 2015, more than 1,000 new SaaS startups emerged annually. During this period, venture capital gradually peaked, with annual investments reaching the level of tens of billions of U.S. dollars, most of which flowed into the SaaS industry.

In China, however, it was the consumer internet that truly transformed the era.

ByteDance reshaped global content distribution logic with information feeds, while Pinduoduo broke through from the lower-tier markets, bringing e-commerce into Amazon's backyard. Behind each success story was the rise of super apps and the control of traffic entry points. The domestic internet narrative was driven by traffic.

Behind the differences in the service objects of the internet in China and the U.S. lie divergences in two underlying paradigms: the U.S. emphasizes "interfaces," while China emphasizes "entry points." Such paradigm differences now also profoundly influence the attitudes of Chinese and U.S. companies toward AI.

The logic of U.S. tech companies is straightforward: standardize core capabilities, and they can be sold globally through interfaces.

This path dictates that competition will naturally concentrate at the top, as the winner becomes the default choice for all clients to call upon. Ultimately, under economies of scale, a winner-takes-all situation emerges. This was the case with cloud computing in the past, and it is the same with AI today.

China's AI, however, is charting a different course. Over the past decade, the core logic of Chinese tech companies has been to construct ecosystems around super scenarios.

Whoever controls the user entry point controls the commercial value. WeChat controls the social entry point, Taobao controls the transaction entry point, Douyin controls the content entry point, and Meituan controls the local life entry point. Behind these entry points lies not just traffic, but user relationships, transaction chains, and commercial closures.

But the AI era may alter all of this. When users order food, book hotels, shop, or search, they may all be handled by agents. If these entry points are usurped by external models, the value of the original business may be redistributed.

Therefore, for Chinese internet companies, developing models is not necessarily about becoming the "Chinese OpenAI" but more importantly, avoiding being marginalized by the "Chinese OpenAI."

Another reason is the emergence of DeepSeek, which has also ushered in new possibilities for model competition.

DeepSeek's greatest achievement has been proving two things:

First, good models do not necessarily have to rely on the most expensive chips or the highest training costs.

Second, a low-cost, good model is already sufficient to cover 80% of application scenarios.

To some extent, this has altered the competitive logic of models.

The emergence of DeepSeek has timely shattered the myth of computing power hegemony. It proves to all players that if you can't build a rocket, building a sufficiently cheap and usable "electric vehicle" is enough to keep you in the race.

As a result, competition for large models has begun to stratify: frontier models and what most companies are doing are no longer the same thing.

Leading model companies are still building rockets, while most model companies' logic is closer to building electric vehicles—creating a "good enough, cheap enough, and business-embeddable" model.

/ 03 / Conclusion

The evolution of technology is sometimes depicted as a romantic exploration of the unknown, but when it lands in the specific soil of commerce, it often becomes a ruthless fate.

Scientists across the ocean firmly believe in "winner-takes-all," attempting to monopolize the tickets to the future with the most expensive computing power. In China, however, competition for large models is sliding onto the historical track that is most familiar to us.

Looking back over the past decade, from the hundred-team battles in the consumer internet to the overtaking on curved roads in new energy vehicles, and then to the fierce competition in innovative drugs, the biggest trump card for the rise of Chinese industries in the past has been, without exception, an extremely large and efficient engineer dividend.

But behind this dividend lies the coldest cost of Chinese business: all industrial advantages are hard-won through the fiercest competitive environments.

This also foreshadows that the battle for large models in China will not conclude as swiftly as in the U.S. The path to success for AI in China will ultimately emerge slowly in this ruthless competition.

By Aqi

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech

-

![]()

Optical Communication and Robot Vision: OFILM’s Bold Transformation Amid a 460 Million Yuan Loss

-

![]()

From 100,000-GPU Computing Might to Industrial Efficiency: The Logic Behind AI4S-Driven Intelligence

-

![]()

OpenAI, Grok, and Meta Release Three Major Models: Who is the King of Cost-Effectiveness?