Word report dissects the secrets behind DJI and Xiaomi's robots

04/01 2025

04/01 2025

689

689

Compiled by: Amelie, Xuushan Edited by: Yifan

US think tank analyzes how China reversed the situation to become the heart of the global robotics industry

The debate over the commercialization of embodied intelligence is raging.

Recently, Zhu Xiaohu, managing partner of GSR Ventures, said in an interview with the media that GSR Angel Fund has invested in some early-stage embodied intelligence projects in the past few years, and has been exiting in recent months. The core doubt about embodied intelligence projects lies in their unclear commercialization path.

However, regardless of the debate over the commercialization of embodied intelligence itself, China's dominant position in the robotics industry chain has always been at the forefront of the world. For global robotics-related enterprises, as long as they involve hardware manufacturing, the Pearl River Delta is a must-visit "dock" - where there is the most comprehensive supply chain, the most cost-effective manufacturing, and faster iteration speeds. The focus of China and the US on robotics also illustrates this advantage. A senior industry insider once said that Chinese robots can achieve rapid iteration through hardware advantages, while the US focuses more on training robot models.

This SemiAnalysis report demonstrates China's competitiveness in the robotics hardware industry chain, from the birth of robotics technology, key robotics links, the situation of the global robotics market, the advantages of different countries in various robotics links, and how DJI defeated GoPro in the drone field.

The report also mentions several times the reasons for the US's lag in the robotics industry: turning a blind eye to supply chain issues; long-term outflow of manufacturing; unstable policies; the market not correctly seeing the industry potential of the robotics market, etc.

We may be able to re-examine China's leading position in the robotics market from a Western perspective and tap into the potential growth space of the global market.

Silicon Rabbit, without affecting the original text, recompiled and edited the SemiAnalysis report. The following are all SemiAnalysis viewpoints and do not represent the stance of Silicon Rabbit. Enjoy~

Robotics technology is currently undergoing a revolution, with all manufacturing and key industries set to achieve full automation.

Intelligent robots will be the first to create a 7*24-hour labor force with productivity far surpassing that of any human. This will also drive a massive expansion of production capacity. If the US does not follow suit, then the expansion of productivity will belong solely to China.

China is one of the world's most competitive economies and one of the countries skilled at mass manufacturing. At the same time, China's engineering quality has reached a leading level in several key industries such as batteries, solar energy, and electric vehicles. With these economies of scale, China can provide services in large developing countries such as Southeast Asia and Latin America, thereby expanding its advantages and influence.

Automation will produce more robots. As the production of each component increases, production costs will continue to decrease, production quality will improve, and their production speed will be enhanced, creating an infinite loop. With improved quality, it will be difficult for other countries to compete.

The birth rate crisis in South Korea and Japan is stifling their manufacturing capabilities, while the US focuses on sourcing cheap overseas products from other markets.

Source: SemiAnalysis, IFR.org

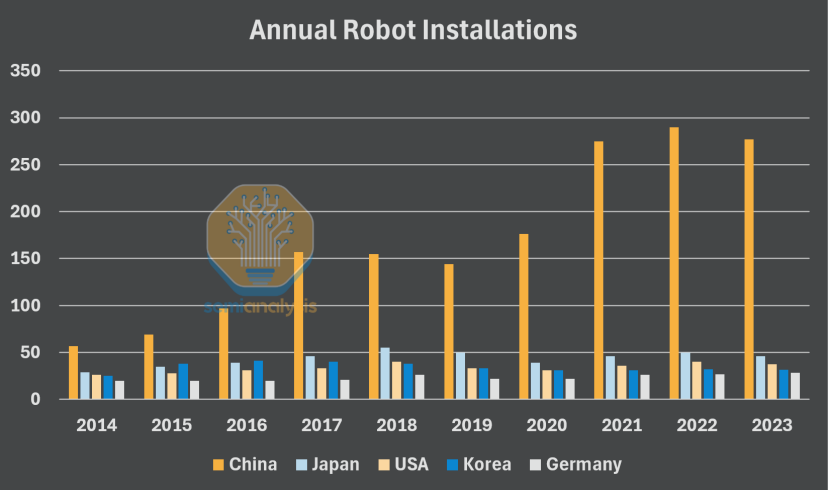

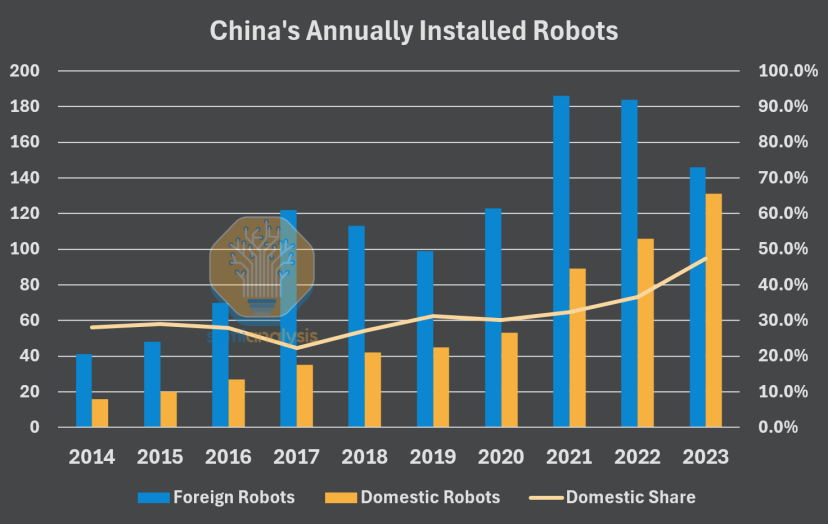

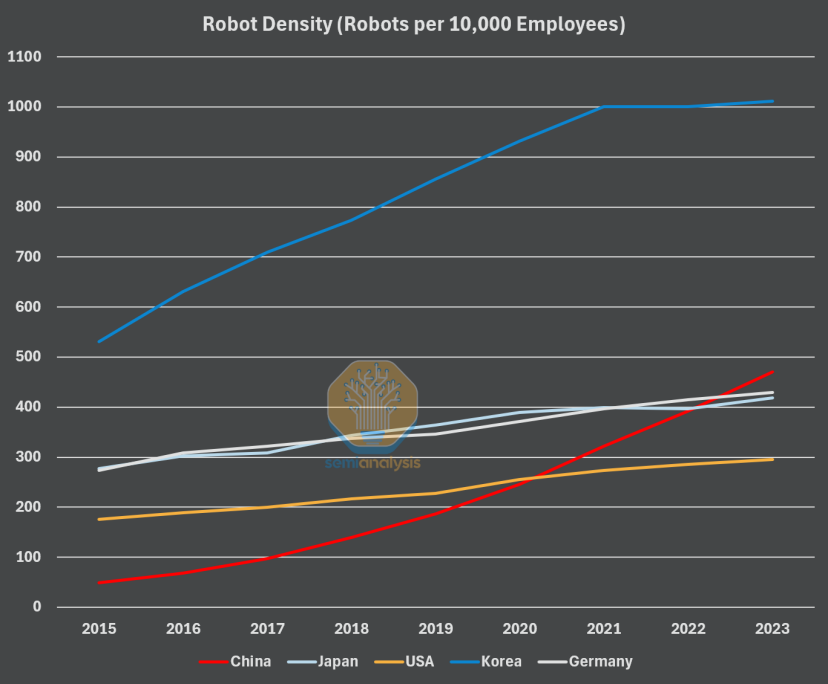

China's robotics localization efforts are progressing smoothly. Local enterprises are occupying the world's largest robotics market with a market share close to 50%, up from only 30% in 2020. Although Chinese manufacturers are currently on par with Western giants in the low-end market, Chinese local enterprises are beginning to occupy the high-end market. The rise of Unitree Robotics is a typical example of this transformation. On the other hand, the deployment of Chinese robots is also increasing. Today, the annual installed capacity of new robots in China has surpassed the combined total of the other four major giant countries. China's robot density has also surpassed that of all countries except South Korea after 2023.

Source: SemiAnalysis, IFR.org

Source: SemiAnalysis, IFR.org

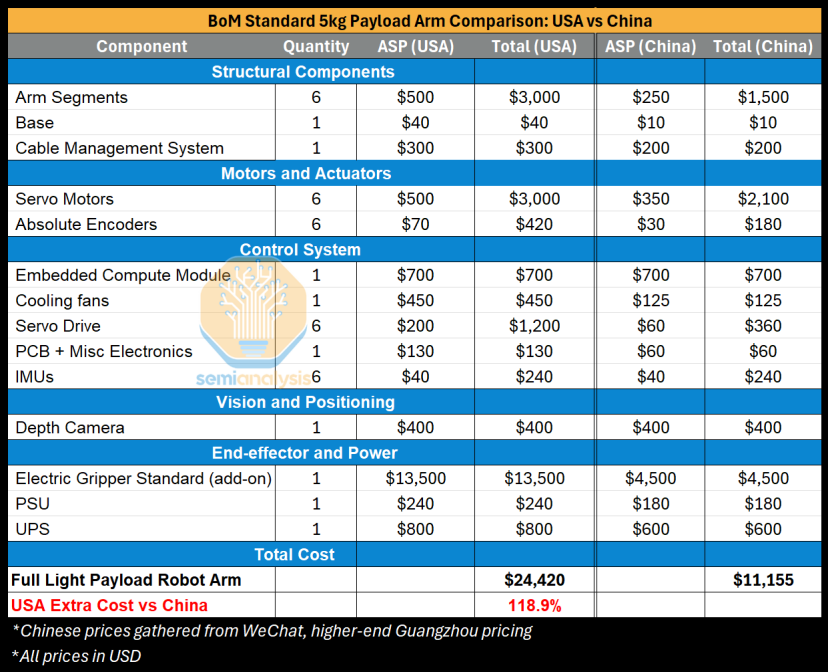

Cost advantage is an important reason for the rapid growth of China's robotics industry. Today, the cost of manufacturing an identical robotic arm (modeled after the Universal Robots UR5e) in the US is about 2.2 times higher than in China. Even if these components bear the "Made in USA" label, they heavily rely on parts and materials made in China because there are no alternatives outside of China.

Source: SemiAnalysis

How was robotics technology born?

a. The history of robotics technology and the birth of current robotics technology

Industrial automation through robotics has been brewing for decades. During this time, some countries have become models for the future of automation, while others have lost their previous advantageous positions. How did these countries gradually lose their advantages in the robotics industry? And how did newly emerging countries gradually gain their competitive advantages and stand out?

Let's first look at the traditional countries in robotics history. The robotics field has always been dominated by four countries: South Korea, Japan, Germany, and the US, with China becoming a new important force today. A closer look at these four countries that once dominated the robotics field reveals certain similarities in the factors driving their success.

Source: SemiAnalysis, IFR.org

• First, these four established robotics countries are historical players in heavy industries such as automobiles and electronics, which are easy to automate through robotics technology

• Second, they possess large industrial groups - such as Toyota, Siemens, Samsung, Emerson

• Third, they value a corporate culture of technology

• Fourth, demographic structure and labor cost pressures

Robotics technology is a systems engineering problem, with the ultimate goal being that one or more machines can create the same work value as humans at the same or lower cost.

A robot's hardware system consists of many interconnected individual components and is integrated with a software layer that will move and plan along with the hardware.

Designing reliability into a low-cost, high-performance, and scalable system can achieve a new type of system that has never existed before. Integrating mechanical capabilities with software intelligence brings the world closer to the ability to fully expand the industrial economy, similar to humans integrating sensory input and cognitive processing to understand and interact with the world. This is humanity's ultimate vision for robots. For example, embodied intelligence will perform the same operations and operate autonomously. However, even today, with the development of large models, the commercialization of embodied intelligence still faces insurmountable technical challenges.

The robotics industry has been emerging for many years and is not an emerging technology; it can even be said to be very old. However, this industry has always been fraught with pain, from manufacturing capabilities below standards to difficulties in scaling product management, and there have always been many bottlenecks:

• Limited hardware innovation, limiting the accuracy and efficiency of mobility and manipulation

• Software/AI functions have never achieved functional diversity and real-time understanding

• Excessively high upfront capital expenditures for installation

• Excessively high operating expenditures for system maintenance

These factors are intertwined, making automation a problem and not even a solution for automation. However, breakthroughs in hardware and AI models have finally opened the gate to the early stages of rapid development and unleashed the potential of general-purpose robots.

b. From industrial robots to collaborative robots

Let's step back and first understand the current state of the industry.

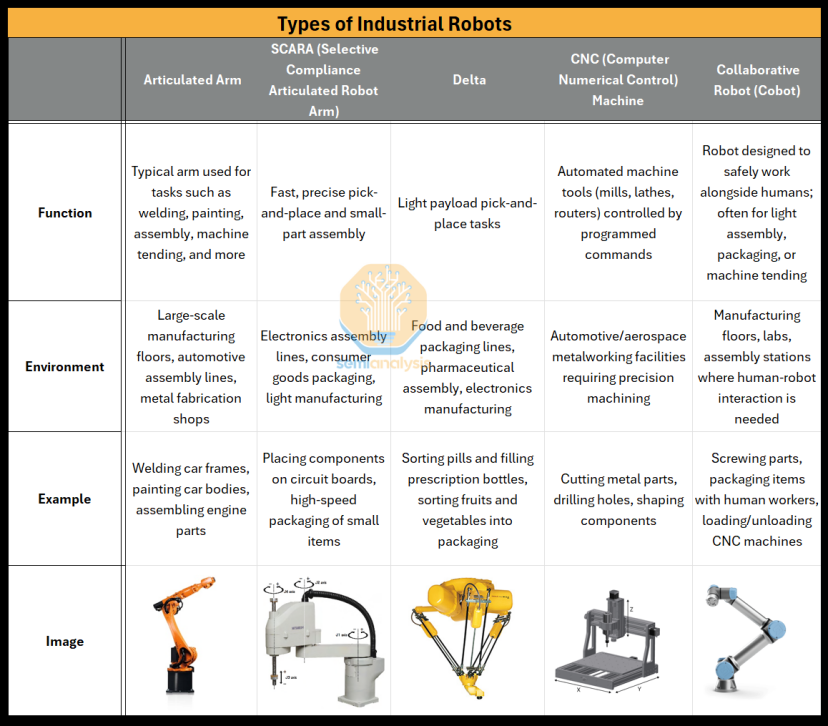

In the past few years, robots of various forms and uses have been landing and put into use. However, the most attractive robots for achieving large-scale automation in the past few decades have been industrial robots.

Source: SemiAnalysis

Traditional industrial robots, such as articulated robotic arms, prioritize speed, accuracy, and payload capacity. They are equipped with high-torque actuators and finely tuned high-frequency control systems to achieve precision and are typically used in heavy industrial environments requiring repetition and high throughput, such as automotive factories or electronics manufacturing.

These industrial robots need to be placed in separately isolated work units for two reasons:

1. The dangerous environment of the factory

2. Related work does not require high flexibility

The reason is that these robots cannot adapt to changes in the following environments: any slight deviation in the environment may disrupt their processes. For example, in the automotive industry, spot welding metal panels is usually automated. This task requires very high precision to ensure that the panels are correctly positioned with each other, and the force and time interval of spot welding need to be consistent. Due to the accuracy of the task, any slight deviation in positioning or timing may affect the welding, thereby affecting the structural integrity of the vehicle.

Therefore, to better adapt to the complex environment of the factory, collaborative robots have been introduced for use. Unlike traditional industrial robots, collaborative robots (cobots) are solutions for human living environments. Affected by the complexity of the existing physical world, they can achieve a higher level of automation within the factory. Similar to industrial robots but slightly smaller, they offer higher safety, flexibility, and programmability, bear payload capacity, and can be easily reassembled and moved around the factory when necessary. These are usually robots endowed with higher levels of AI capabilities for certain tasks today (higher precision grasping, placing, and sorting).

Source: Future Automation

Collaborative robots add safety hardware to enable more functions and adapt to complex environments: for example, force-torque sensors - to detect collisions; additional visual sensors - to build a more comprehensive view; and more onboard controllers - to achieve redundancy, but at the same time sacrificing payload capacity and speed. They can be programmed and trained through some user-friendly interfaces (usually tablets), lowering the operational threshold.

Typically, collaborative robots are used in links requiring fine control rather than high-load work. For example, they might handle lightweight materials in a factory, which are then taken away by industrial robots to perform heavier tasks. Collaborative robots can also serve as companions to other industrial machines, such as CNC (Computer Numerical Control), where they can load CNC raw materials, retrieve finished parts, and even perform routine support tasks such as cleaning or quality inspection. Below is an example of a robotic arm interacting with a CNC machine:

Source: Productive Robotic

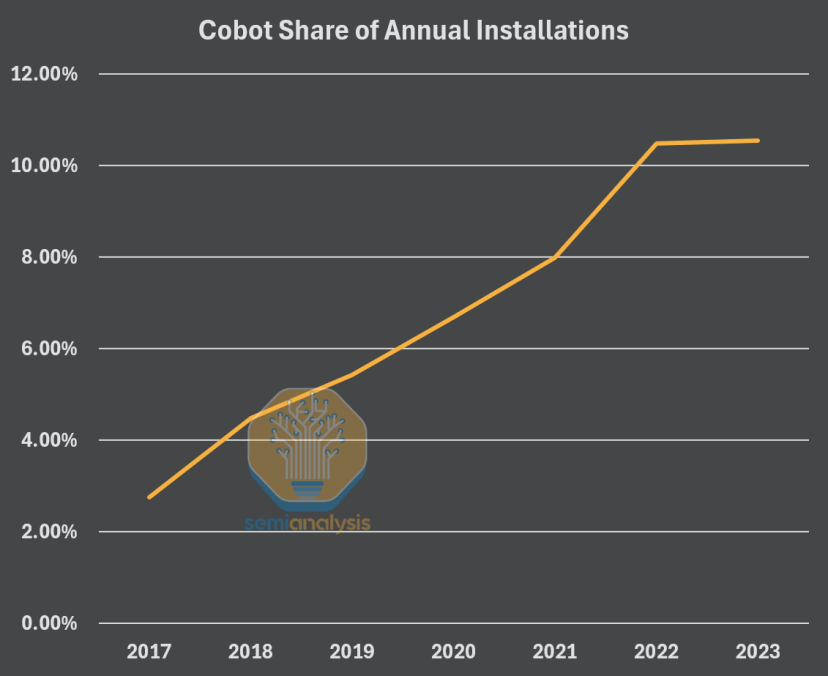

The share of collaborative robots in all industrial robot installations has been rising rapidly, as they enable higher levels of automation setup and improved factory return on investment, enhancing efficiency.

Collaborative robots are economically feasible in industrial environments because the environment can be structured enough to ensure that robots maintain high accuracy in tasks.

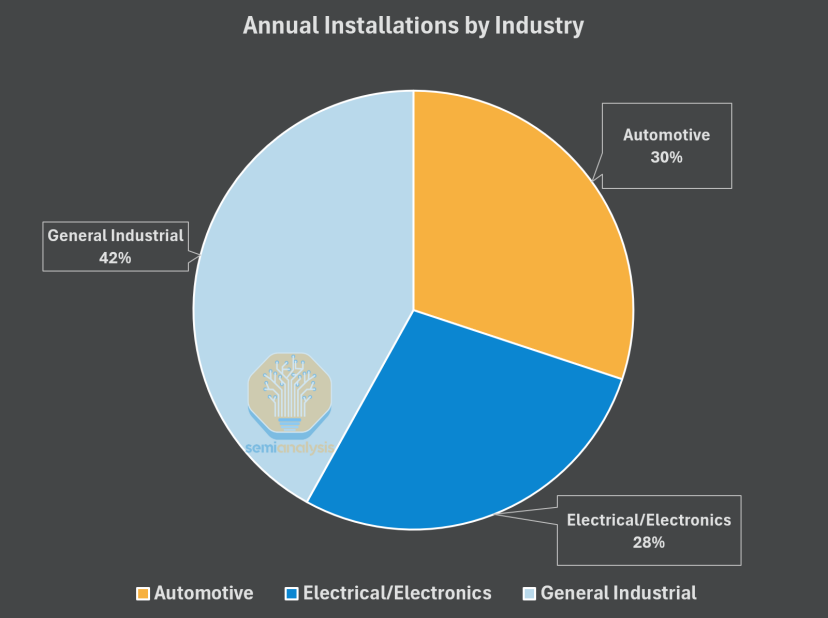

Currently, there are over 4 million robots installed and operating globally, with 90% of annual shipments being standard industrial robots and 10% being collaborative robots. Industrial robots are commonly used in the automotive industry, food and consumer goods packaging, and electronics manufacturing. Collaborative robots perform more complex tasks in the same industries, which require extremely high precision but need the guidance and instructions of human workers.

Source: SemiAnalysis, IFR

While the scale of automation is impressive, it is understandable that these robots are mostly found in factory environments, rather than others.

For these robots, not all manufacturing is easy. Factory production, especially customized small-batch production, is often accompanied by changes, making it difficult to fully automate tasks. Most tasks requiring fine motor skills and flexibility have operational requirements that are difficult to achieve today. Although collaborative robots are considered one of the solutions, in practice, the need for automation requires more flexibility and capability than any current robot can provide.

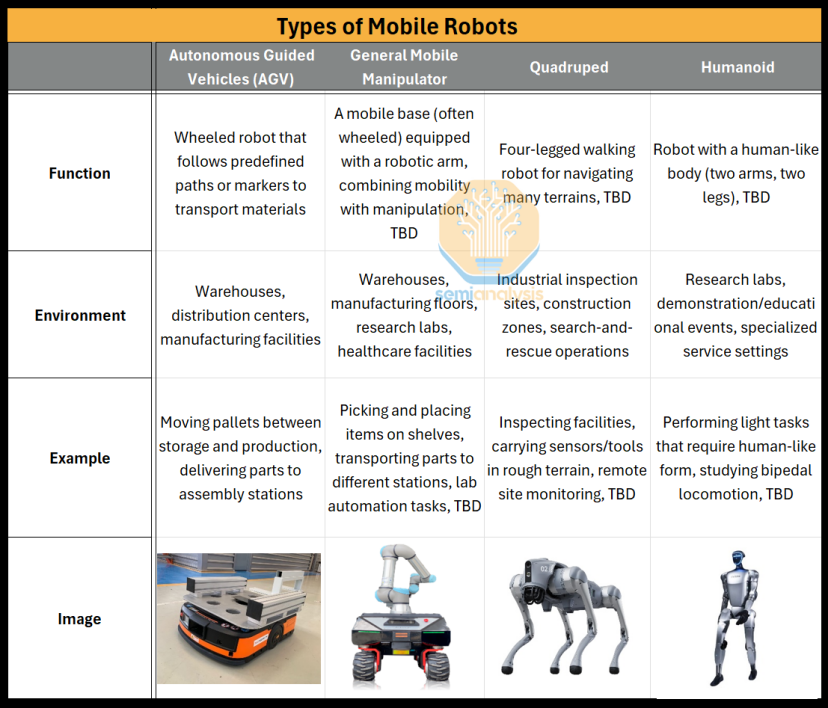

c. Rise of Mobile Robots

Source: SemiAnalysis

Mobile robots are the latest addition to the fleet of automated robots, utilizing their mobility to perform transportation tasks and coordinate with other robots. However, they all face different challenges, areas, and advantages in terms of mobility.

Autonomous Guided Vehicles (AGVs) entered the mobile robot domain roughly at the same time as collaborative robots. Their job is simple: transport objects (such as packages within Amazon fulfillment centers) to another location. Like most other robots, these are not flexible and require some form of guidance on the floor for the AGV to follow.

Source: Amazon

Mobile manipulators refer to robotic arms with wheels at the bottom, used in factories. These require a flat surface to navigate strictly and over short distances, from one station to another, to grasp and move objects. Quadruped robots are four-legged mobile robots commonly seen in more open environments, typically inspecting areas on construction sites or similar locations, but they are still in the prototyping phase.

Finally, humanoid robots can operate in the same environments as other robots, but they will be more frequently used in human-inhabited environments. These robots are currently in production.

However, all these form factors can still only function in closed, static, and structured environments. Currently, only AGVs are widely deployed and integrated. Thanks to advancements in AI technology, mobile manipulators, quadruped robots, and humanoid robots are still in the early stages of deployment in more complex and open-world environments.

d. Towards General Purpose Robotics

General purpose robotics is the holy grail of robotics: it means robots can perform any task in any environment, replacing the need for humans in industrial processes.

Currently, robots implemented on a large scale globally are functionally limited: the environment must be predefined, tasks must be static, and minor changes in any factor can disrupt the robot's overall planning and operation.

There is currently no solution to these existing technical bottlenecks. The only possible improvements for robots are small, iterative, and incremental developments. Any company that attempts to equip robots with capabilities beyond their current levels has failed, marginalizing many researchers and investors, especially in Western markets. The only ones attempting to bridge the gap into general purpose robotics are laboratory researchers. Building a functional replacement for humans, achieving the same level of accuracy as humans, typically requires about 99.99% accuracy and ensuring a cost advantage over a sufficiently long period is a pipe dream. But why do people believe it?

Let's first look at what researchers who have been deeply involved in this field have done.

The biggest bottleneck for robots is the scarcity of data. Unlike the data driving large language models, which is freely available text data on the internet, robotics requires multimodal data, which does not exist on the web, as it interacts with the physical world. Every researcher trying to train robots must collect all data themselves using functional robots in physical spaces. Hardware limitations exacerbate this problem – it is very difficult to build a sufficiently powerful robotic actuator system, and all of this must interconnect with non-standardized components.

Even Google could not overcome this problem. It built a "farm of robotic arms" consisting of 14 robots that ran continuously for 3,000 hours just to achieve reliable grasping. Due to the lack of hardware standardization, researchers are forced to build makeshift robots and then manually collect training data, a process that consumes a lot of time and resources.

Source: Google – Large-scale data collection with an array of robots

However, today, significant research and funding across the entire robotics stack have led to a series of breakthroughs. Advances in realistic simulation data, the ability to scale real-world training across multiple robots, and the rise of foundation models have opened the door to more intelligent systems. Meanwhile, hardware advancements, such as electric actuators, have significantly reduced costs and given robots higher efficiency to operate at the required levels of precision, unlocking previously impossible new movements.

General purpose robotics is finally becoming a possibility.

The first direction for general purpose robotics will be into the "partially unstructured" domain – initially in their most common environment, factories. In factories, this means operating outside their isolated, predefined environments and handling multiple tasks. As robots gradually move towards general purpose domains, they will replace increasingly difficult and diverse tasks in factory environments until they can achieve full automation.

A more challenging domain for robots is the human-inhabited domain. In this domain, robots need to be smart and safe enough to operate in completely unstructured and dynamic environments. Due to unpredictable human behavior, robots need to adapt to avoid safety risks. Besides full automation in industries, these robots will also alleviate shortages of elderly caregivers, improve hospital efficiency, enhance surgical accuracy, and perform dangerous construction tasks, thereby meeting almost all labor needs.

Cannot do without China's robot hardware manufacturing

a. What is needed to manufacture robots?

After understanding the development of robotics technology, we know the current bottlenecks of robots and their necessity for human society.

The robot components market is dominated by a few key players.

However, where robots require large-scale production capabilities – low cost, high volume, and high quality – most come from China. The United States has lost its leadership position in many aspects. We try to understand the key components of robots and the dominance of various countries in them from this section.

In hardware, actuators, motors, and drives are components that generate motion by converting electrical input into hydraulic, pneumatic, or more commonly, electrical output.

In factories, Programmable Logic Controllers (PLCs) determine how production lines will be automated, correctly sequencing each operation to ensure the entire automation process runs smoothly. Inside every robot, regardless of form factor, there is a Microcontroller Unit (MCU), or an embedded system with multiple MCUs, which is a specialized processor that handles low-level real-time tasks such as reading sensor inputs, generating motor control signals, and running fast control loops. These systems are the "brain" of most robotic systems.

Source: BizLink

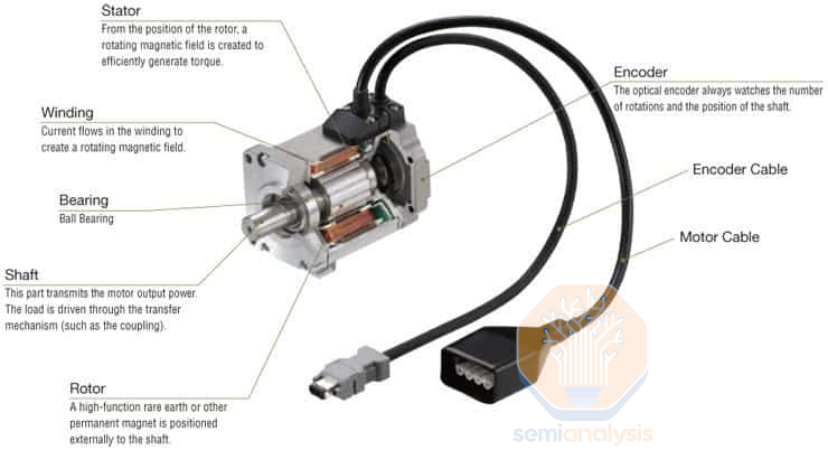

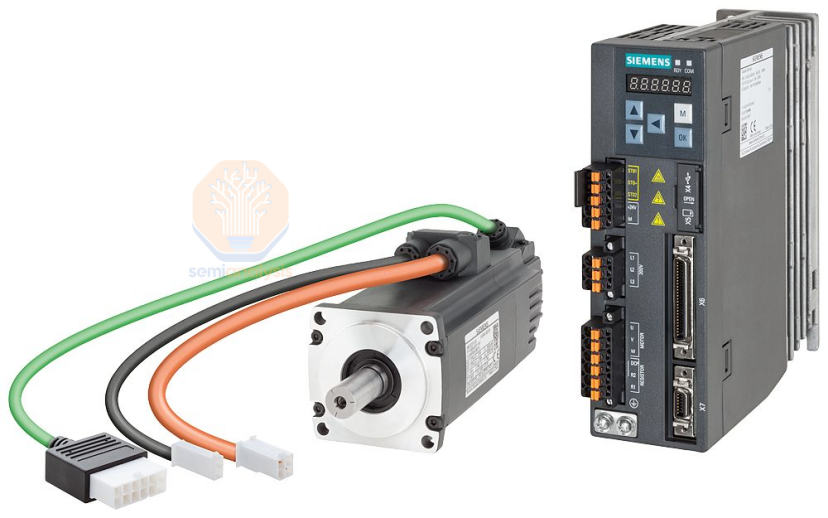

In the world of robotics, high-precision motors are needed to ensure that the appropriate torque is applied to avoid damaging the surrounding environment. Servo motors are the most common choice – they contain the system, motor, control circuit, and feedback mechanism. The motor can self-adjust and maintain the desired position or motion. Servo motors are one of the few components in robots not dominated by China.

Source: SolisPLC

The control circuit is called a "drive," an electronic power box designed to regulate the voltage sent to the motor through AC-DC-AC conversion (a component that converts AC voltage to DC voltage). Its main component is a power electronic switch, such as a MOSFET or IGBT, which, combined with a rectifier and capacitor, can electronically modify electrical signals.

Source: Polytechnic Center

Gearboxes are also common components in servo motors. They increase the motor's torque and improve accuracy. Essentially, gearboxes reduce the motor's speed, causing the torque to increase proportionally, which also allows the motor to make finer movements. Most gearboxes in robotic systems are produced by Nabtesco in Japan.

Source: Santram Engineers

Cameras and sensors are also crucial for robots as they are the primary medium for robots to understand their positioning and the steps needed to complete tasks.

Most industrial robots use standard machine vision 2D cameras, 3D depth cameras, or a combination of both to create a comprehensive spatial understanding of their environment. However, another trend is that robots tend to install lighter, cheaper cameras and are equipped with more powerful software to compensate for hardware deficiencies.

In environments closer to human life, LiDAR may be used to gain a more detailed understanding of the surrounding environment, although this is usually more costly.

Industrial and precision robots are equipped with joint encoders, allowing the robot to understand the angle, position, or rotational speed of its joints. They also include various sensors such as touch and tactile sensors to understand pressure, texture, etc.; proprioceptive sensors to understand the internal state of objects; balance, force-torque sensors to understand how much force-torque is applied to the joints, etc. This market is somewhat small and fragmented due to the novelty of the products. However, most Western companies that can design and assemble these sensors usually still purchase the main materials from China.

Source: Intel

Then there are "end effectors," typically deployed at the end of a robot arm. They are the tools or base units of most robots, with each end effector having its own purpose and payload capacity. The intended use of the robot will determine the type of end effector installed, which is a part of the robot. Most end effector manufacturers are German (Schunk, Zimmer Group, Festo, Schmalz), and some are even American (ATI Industrial Automation, Destaco). Chinese companies likely only produce their own end effectors and do not export them, as vertical integration is the primary strategy for Chinese companies. Although robotic arms are now receiving a lot of attention, they have not been widely deployed for practical use and are far from being sufficiently flexible.

Source: Global IPR

Source: Igus

b. Hardware supply chain issues

Bringing manufacturing capabilities online and mass-producing industrial robots to introduce automation into production lines is much more difficult and time-consuming than many people realize.

The supply chains for many industrial robots are complex, sourcing from many corners of the world where component production has often dominated the supply chain through competitive cost advantages. There have been many cases of supply chain disruptions in the robotics industry, which have shaken the Western economy. For example, during the COVID-19 pandemic from 2020 to 2022, the ports of Los Angeles and Long Beach experienced over 100 ships waiting outside the ports for cargo to be unloaded.

In stark contrast, during the same period (2020-2021), China underwent a transformation and increased its robot installations by 44%.

c. Mechanical Components: Reducers, Motors, Actuators

There are many types of motors that can be used for robotic motion, such as steppers with precise angular control used in 3D printers or CNC machines; brushless DC motors with a high power-to-weight ratio used in drones and electric vehicles, but often the most important in robotics are servo motors.

Most robotics companies, especially the Big Four, produce their own servo motors in-house and sell them separately. While these servo motors are not difficult to manufacture, they do create some moats for companies that mass produce them: actuators must have high reliability and performance, so scaling requires advanced manufacturing techniques to replicate almost perfectly and achieve mass production. Therefore, long-time manufacturers of robotic components with the necessary expertise have the largest market share, such as Yaskawa (Japan), Panasonic (Japan), Bosch (Germany), Kuka (now China), and Siemens (Germany). Also included is Rockwell from the US, as it holds around 7% of the servo motor market share, but this is also the only part of the supply chain where no single participant dominates.

Source: Moog Inc.

Nearly 60% of the world's medium and large industrial robot reducers are supplied by Japan's Nabtesco. The difficulty in manufacturing them lies in the fact that almost every order is likely to be highly customized and tailored to the customer's hardware specifications, yet they must still meet 99.99% accuracy to replace humans and be applied in production. Reducers are crucial for ensuring this accuracy, and therefore account for the largest share of the manufacturing cost of industrial robots at 14%. The manufacturing of these gearboxes must be highly precise, so usually, only mature players with years of manufacturing experience can refine their processes and technologies to achieve this quality.

Source: Curated Industries

There are even special types of reducers - harmonic drive gears, such as Harmonic Drive (Japan), founded in 1970, which uses a patented strain wave design with incredible precision. These components are more expensive but essential in ultra-precision settings such as semiconductor manufacturing. Green Harmonic was founded in China in 2003 with the aim of manufacturing its own ultra-precision strain wave gearboxes. In just 14 years, the company has produced over 100,000 units and captured 90% of China's domestic market for harmonic drive gears.

Source: makeagif

d. Magnets and Materials - Manufacturing Dependence

The supply of motors and gearboxes is not short, and prices are relatively cheap; however, today's motors have achieved a breakthrough. Most high-quality high-speed motors suitable for robotic use are now developed with permanent magnets (PM motors) to achieve higher power, efficiency, and power-to-weight ratio.

Permanent magnets effectively add more magnetism to the electromagnetic field of the motor, meaning less electricity is required for magnetization and can be used to generate motion.

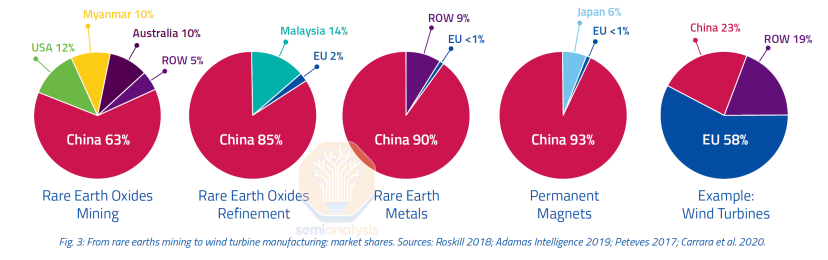

However, there is still an issue where the process and elements for manufacturing typical neodymium magnets (NdFeB) are almost entirely dominated by China, accounting for 90% of the global market share. Within this 90% share, there are approximately three Chinese manufacturers that hold a monopoly: Jingci, Jinli Permanent Magnet, and Ningbo Yunsheng.

Source: ERMA

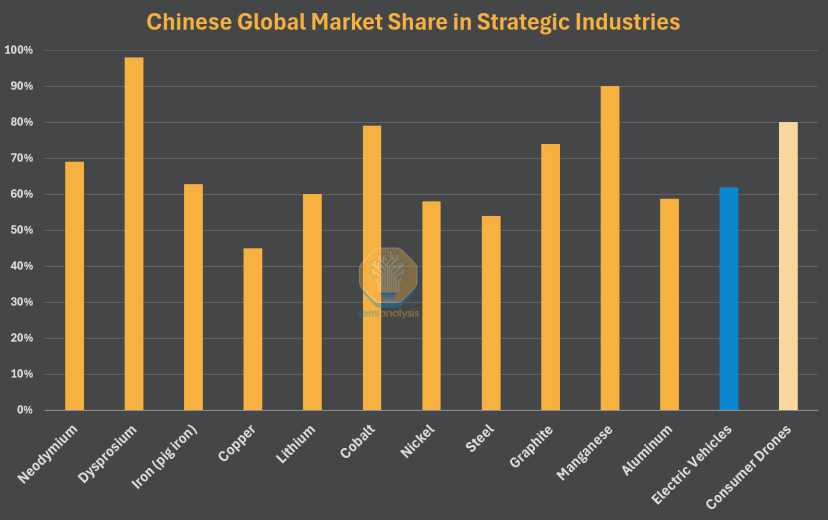

While 'rare earths' is a misnomer - they are as abundant as most other elements - the process required to refine neodymium and produce the final permanent magnet involves around 12 complex steps and robust industrial capabilities. China also dominates this process, accounting for 93%.

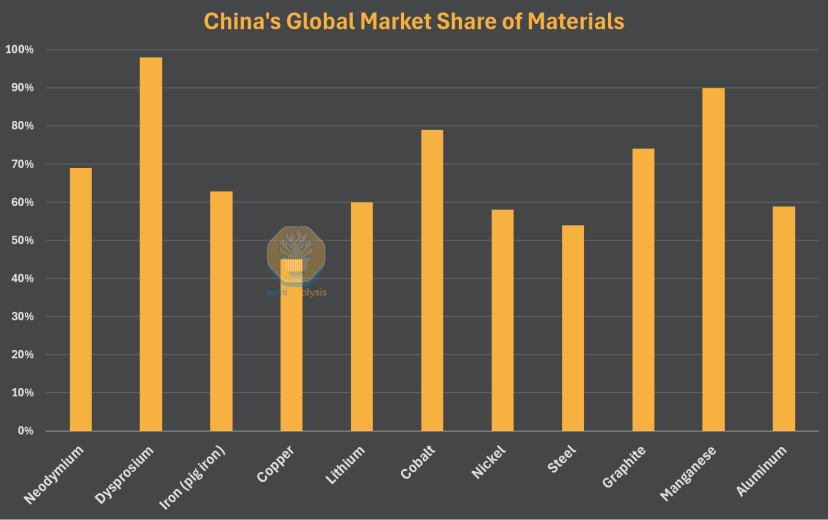

Mining and materials beyond rare earth elements are equally important, and while this usually does not suffer from bottlenecks, China also dominates this segment of the market. Many economies struggle to process these elements, and China excels in this area due to its advanced industrial economy. China's two major initiatives - the Belt and Road Initiative and Made in China 2025 - have invested and paved the way for dominance across the entire mineral processing industry.

Source: SemiAnalysis, Industry Estimates

e. Lithium and Batteries

All ores may come from different mineral-rich countries, but owning the ores is meaningless without the ability to refine them on a large scale and at high grades.

In fact, China only has abundant deposits of two minerals, lithium and graphite, but countries rely on China's processing to refine other minerals into usable materials.

- Copper typically comes from Chile and Peru, with around 76% of Peru's and 68% of Chile's copper exports going to China, accounting for 56% of the global total raw copper.

- Nickel is highlighted as a key mineral not primarily refined in China, with 37% refined in Indonesia and 'only' 28% in China. However, according to a recent report by the International Energy Agency, over 80% of Indonesia's battery-grade nickel production is owned by Chinese producers associated with the CCP.

- Cobalt is mined in the Democratic Republic of Congo, accounting for 80% of the world's cobalt production, but China has signed the Sicomines Treaty with them and now owns 80% of the Democratic Republic of Congo's cobalt production.

Source: Visual Capitalist

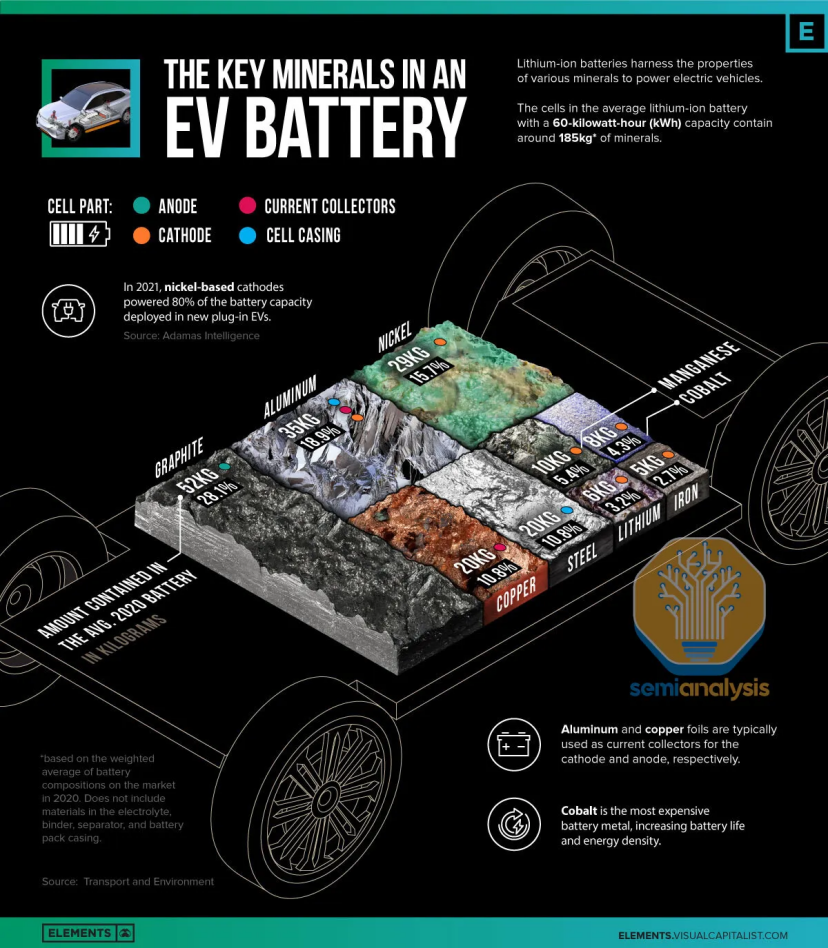

Batteries, particularly lithium-ion batteries, are crucial for mobile robots such as drones, service robots, autonomous guided vehicles in warehouses, mobile robotic arms, humanoid robots, and electric vehicles.

If you want to realize a future where robots are separated from connected power sources, you will most likely use Chinese batteries, as Chinese companies supply around 80% of global batteries. The cost of a Chinese battery pack is approximately $127 per kWh, while prices in North America and Europe are 24% and 33% higher, respectively.

The largest producer outside of China, LGES (South Korea), accounts for only around 13% of the global market share. And this is a relatively fixed market where overcoming barriers to entry is not easy, as evidenced by the recent bankruptcy filing of Swedish government-backed battery firm Northvolt. This is because it requires not only strong large-scale production capabilities but also sufficient cost advantages.

Building sufficient large-scale production capabilities is already challenging, especially in the US, where battery manufacturing costs in the US can exceed $100 million and cost per GWh is 46% higher than that of Chinese counterparts. LG has even paused construction of its $5.5 billion battery factory in Arizona, citing 'market conditions'.

In robotic applications, battery manufacturing is even more difficult. Batteries come in different sizes with no standardization, and they have different requirements. The power-to-weight ratio is a more stringent requirement because robots do not have the weight of a car to carry the battery, and often different robots have different power requirements. The battery used in a quadruped robot is different from that used in a humanoid robot, which extends to almost all form factors. The difficulty and cost of manufacturing pure and efficient batteries are already challenging enough, especially in the US, but the lack of standardized consistency in robotic batteries will be one of the biggest issues as the time for mass production has arrived.

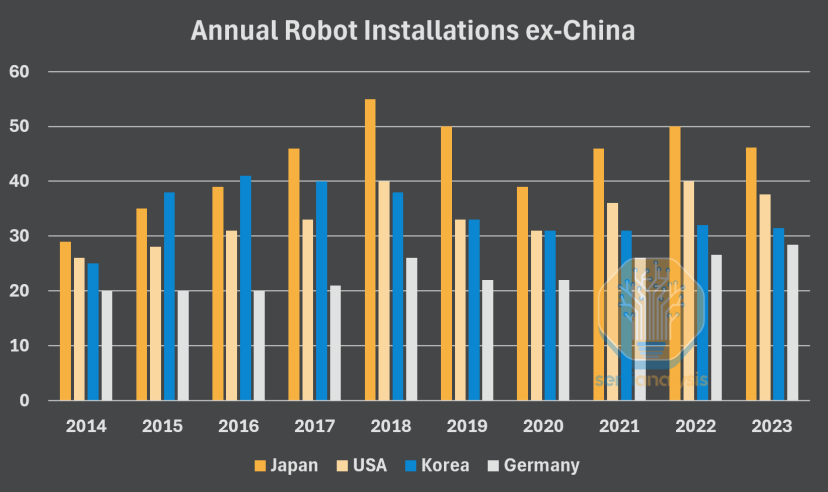

Germany has left the table, while Japan, the US, and South Korea persist

A closer look at automation growth in Western countries reveals a peak around 2016-2018. Japan's new automation rate in 2023 is still about 13% lower than the 2018 peak, and South Korea has seen no growth since 2016.

The only country among the top four to reach a new peak in 2023 is Germany, but their leading company, Kuka, has been acquired by the Chinese company Midea and is moving manufacturing to Asia.

Source: SemiAnalysis, IFR.org

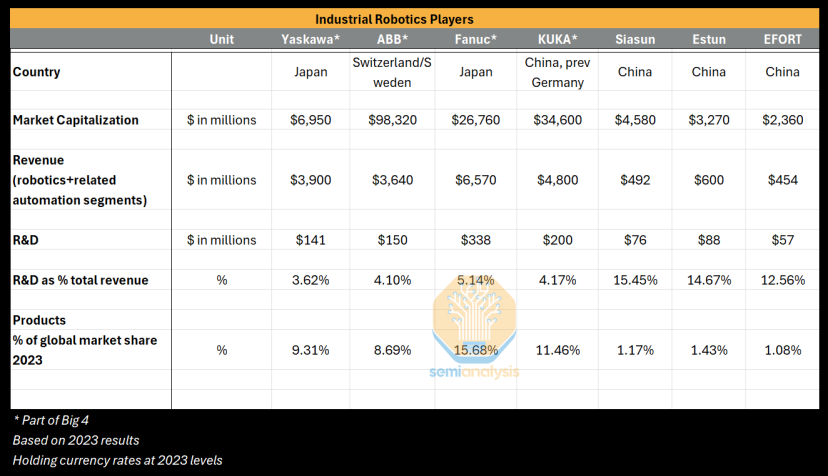

Kuka, once the representative of German robotics and now controlled by China's Midea Group, was once hailed as one of the 'Big Four' in robotics, dominating the industry for decades. These Big Four are FANUC (Japan), ABB (Switzerland/Sweden), Yaskawa (Japan), and Kuka (previously Germany, now China).

Source: SemiAnalysis

These four traditional robotics giants have decades of experience in the field and high-volume manufacturing capabilities across various industries such as collaborative robots and general-purpose robots. However, with relatively low R&D ratios, overall low willingness to participate in the industry, and capital-intensive operations, the Big Four struggle to sustain innovation in the next generation of robots. Additionally, their business is increasingly leaning towards mainland China, which of course comes with certain review risks.

In contrast, Chinese players are now catching up technologically and filling market gaps at an unprecedented rate.

a. South Korea and Japan: Automation is imperative due to demographic structure and labor shortage pressures

South Korea has already increased its labor force by 10% through automation.

By 2022, the economic value generated by high-tech manufacturing companies will account for 61% of South Korea's overall economy. South Korea has the highest e-commerce adoption rate in the world, with over 30% of retail sales conducted online, twice that of the US.

Both the South Korean government and chaebol groups are going all in. In 2021, Samsung announced their initiative to invest up to $163 billion in industrial automation and AI. Hyundai Motor has already acquired Boston Dynamics in 2021. After deploying autonomous airport guidance robots at Seoul Airport in 2017, LG identified robotics as a key growth area and recently increased its stake in Bear Robotics.

Furthermore, the South Korean government is increasing its investments. Since 2008 to 2030, the country has proposed four basic plans for intelligent robots, totaling $1.6 billion, and plans to invest approximately $2.26 billion by 2030.

However, South Korea is also dependent on other countries for industrial robot components, importing around 60% of them.

The reason behind South Korea's push for automation is the same as Japan's: an aging workforce and low birth rate.

Despite comprehensive government measures, the country's birth rate remains at an all-time low. For example, the lack of workers in rural areas forces factories to relocate near Seoul just to manage their operations. They have even had to lift decades-old bans on foreign workers in some manufacturing plants to compensate for the labor shortage. South Korea has the world's lowest birth rate, followed closely by Japan. However, Japan has a slightly better chance in the automation race due to its two leading companies.

b. Germany and the EU: Observers in the corner

Germany, a European industrial powerhouse with the world's fourth-highest robot density, has been committed to a strong industrial economy. In 2011, Germany introduced 'Industry 4.0' to the broader EU, hoping to integrate new technologies and automated processes into EU industries to enhance competitiveness. But this has not stopped the decline of European robots.

In 2016, German robotics company Kuka was sold to China's Midea Group. Following that, Italy also sold many robotics companies, such as EVOLUT, OLCI Engineering, and CMARobotics.

In February 2025, the European automation industry organization finally issued a call to action to the EU, hoping it would address the lack of competitiveness in the robotics sector. Industry 4.0 was a transformation plan, but it took the EU nine years to realize it needed the robotics market.

c. The US: A violent awakening of the American Dream

The situation in the US is different from that of Germany, South Korea, and Japan.

In the US, we see a strange phenomenon where some advanced technology sectors lack an overall national strategic plan and rely on outsourcing manufacturing.

The problem with US manufacturing mainly stems from the high cost of labor and the slow erosion of the country's once-strong 'quality' moat. China now has the capability to produce most goods of similar quality at cheaper prices. Despite having a large automotive industry, the US ranked only 10th globally in robot density in 2023.

A study shows that, in fact, robot adoption in the US is lower than expected at 49%. While the AI revolution in the US may benefit the robotics industry more than other industries, enabling the US to compete through technology and low-cost production, this will take time and is unlikely to happen in the short term.

The instability of US policies is also hindering the development of the robotics industry. For example, the CHIPS Act and the Inflation Reduction Act were initiated under the Biden administration, but during the Trump administration, the Inflation Act was abolished and the CHIPS Act was under discussion.

Furthermore, the US economic structure differs from China's. The US pursues digital innovation, cutting-edge technology, and services, outsourcing most of its production and manufacturing capabilities to countries with lower costs in the process.

In the US, many companies attempt to manufacture their own hardware, but internal hardware development implies the need for in-house design and assembly capabilities.

Everyone pretends to ignore the influx of materials and basic components from China. The US once had a solid foundation to drive the development of heavy industry, but these advantages gradually eroded as cheap overseas manufacturing crowded out US production and the US economy shifted toward frontier technologies and services. In the US, every dilapidated factory and every 'Made in China' label contribute to a portrait of a nation's depleted manufacturing sector.

Today, the US stands at a crossroads of unlimited labor expansion or elimination, with echoes of the industrial era beckoning.

Observing the Rise of China's Robotics Industry through Xiaomi and DJI

a. Xiaomi's Factory Achieves Unmanned Robotic Production

China has already achieved fully unmanned factories. Xiaomi's unmanned factory operates around the clock, producing one smartphone every second - without any human involvement. This is not an isolated case; China can achieve this level of automation without general-purpose robots.

When general-purpose robots emerge, their impact on production capacity cannot be underestimated. This is not to say that the US is falling behind, but rather to showcase the vast differences in manufacturing capabilities.

This has nothing to do with China's cheap labor; China is a manufacturing nation with a strong industrial base that has now created a robot capable of autonomously producing goods.

Source: Xiaomi

This is just the first step in creating fully automated robots to produce goods, and they will continue to evolve as AI foundational models become more reliable and accurate.

China has enabled the production of robots at the Kuka factory in Guangdong. A Kuka executive stated that they should be able to reduce production time from one robot every half-hour to one robot every minute. Soon, any complex manufacturing task can be completed by a general-purpose robotic system.

b. How DJI Stands Out Among GoPro Competitors

The development of the commercial drone market demonstrates that Chinese companies basically adopt a strategy of scale advantage and oversupply when entering a strategic industry.

DJI, the Chinese leader, now occupies over 80% of the global commercial drone market and 90% of the US consumer market. As a pioneer, DJI has maintained and consolidated its market position for over a decade due to China's dominant position in manufacturing, economies of scale, and oversupply strategy.

Source: SemiAnalysis, Industry Estimates

To correctly develop a fully functional and powerful hardware, it is essential to iteratively create and remanufacture rapidly to solve problems and refine the product before competitors do.

The Chinese market can immediately reward companies that expand the fastest. Therefore, Chinese competitors surpass their Western counterparts in cost before entering Western markets, leaving only quality refinement in subsequent iterations.

The US company GoPro attempted to compete with DJI in the consumer drone market, despite having most of its manufacturing operations in China, Malaysia, and Japan, which meant that each iteration of its drone products took weeks.

GoPro likely began design in California, sent details to Chinese manufacturers for production, shipped them back to the US, and then discovered issues that needed to be addressed during the process.

In contrast, DJI's headquarters are in Shenzhen, meaning the company can obtain any required parts from any factory in Shenzhen within hours of ordering and iterate at an astonishing speed. In 2016, GoPro's Karma Drone+ Hero5 was outpaced by DJI's drones. DJI's model was slightly cheaper at $999 compared to GoPro's $1099, offered 50% longer battery life, and included obstacle avoidance. The Karma's launch was plagued by hardware issues, and it had to be recalled due to defective products, with refund plans in place. Sometimes, the product would lose power during operation. GoPro might have been able to resolve these issues with sufficient effort, but the company simply didn't have the time, as DJI had already surpassed them in every aspect.

Shortly after entering Western markets, DJI quickly captured a significant market share with its incredible cost advantage and absolute production capacity, leading to an oversupply in the market. The advantages of all other major drone companies were quickly undermined by DJI's aggressive pricing. GoPro disbanded their Karma project citing 'profit challenges,' and many other companies followed suit. Only DJI understood that this was a competition of scale and prepared for it before entering Western markets.

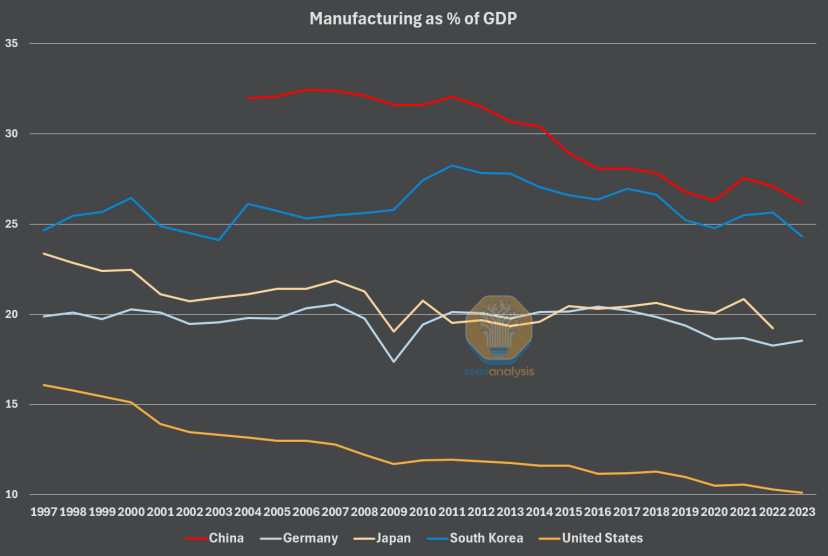

In the field of robotics, dominance in manufacturing is crucial. Creating a fully functional robot requires countless iterations and refinements, fine-tuning every minor error until a robust, scalable, and cost-effective product is produced. For those with affordable access to manufacturing plants nearby, this price advantage is readily available, while the lack of manufacturing capabilities means being at a disadvantage. China's industrial base accounts for three times the proportion of GDP compared to the US, outperforming the US in every aspect.

Source: Worldbank, FRED

China knows what will happen next. If it takes the lead in unlocking robotic productivity, it will iterate faster than the US, engage in large-scale price wars, and supply all global markets.

Our analysis indicates that China is rapidly capturing the market and is fully capable of leading the next generation of robotics technology - a field expected to generate higher macroeconomic benefits.

Original Article Link:

-

![]()

A Humanoid Robot Becomes an Office Intern: The 'Reinforcement Learning' Journey of a Former NVIDIA Engineer

-

![]()

Meta Plans to Launch Cloud Infrastructure Business: Is Computing Power Really in Excess?

-

![]()

Giants Enter the Arena One After Another: The Embodied AI Battle Commences

-

![]()

Is It More Profitable to Build 'Hands' for Robots Than 'Humans'?

-

![]()

Yunling Optoelectronics Accelerates Its Listing on the Beijing Stock Exchange: Secures 989 Million Yuan to Bolster Production of Computing Optoelectronic Chips

-

![]()

From Drill Bits to Optical Coatings: A 200-Billion-Yuan Behemoth Quietly Unveils a New Business Front!

-

![]()

New Energy Vehicle Growth Slows: Are 370 Million Existing Cars the Next Lucrative Market?

-

![]()

Is Baidu Now Fostering Its Own 'Yao Shunyu'?