The Autonomous Driving Profitability Conundrum: WeRide's Five-Year Profitability Goal Remains 'Uncertain', Peeking into the Future

04/03 2025

04/03 2025

601

601

Introduction

Autonomous driving technology stands as the beacon of transportation transformation, yet its commercialization journey is fraught with significant hurdles, profitability being the paramount challenge.

In a recent interview, WeRide's CEO Han Xu articulated the company's ambition to attain profitability within five years but conceded that due to uncertainties in policies, market reception, and business collaborations, pinpointing an exact timeline is "challenging".

This admission once again brings to light the profitability dilemma plaguing the autonomous driving industry.

WeRide is not an exception. Leading autonomous driving enterprises globally, such as Waymo, Baidu Apollo, and Pony.ai, are yet to turn a profit in their Robotaxi ventures.

Despite continuous technological advancements, the industry grapples with high R&D costs, a complex policy landscape, and public acceptance issues, presenting formidable barriers to commercialization.

Join us in discussing this topic at Unmanned Vehicles Incoming (public account: Unmanned Vehicles Incoming)!

(For further reading, please click:

I. WeRide's Financial Standing: Expansion Amidst Losses

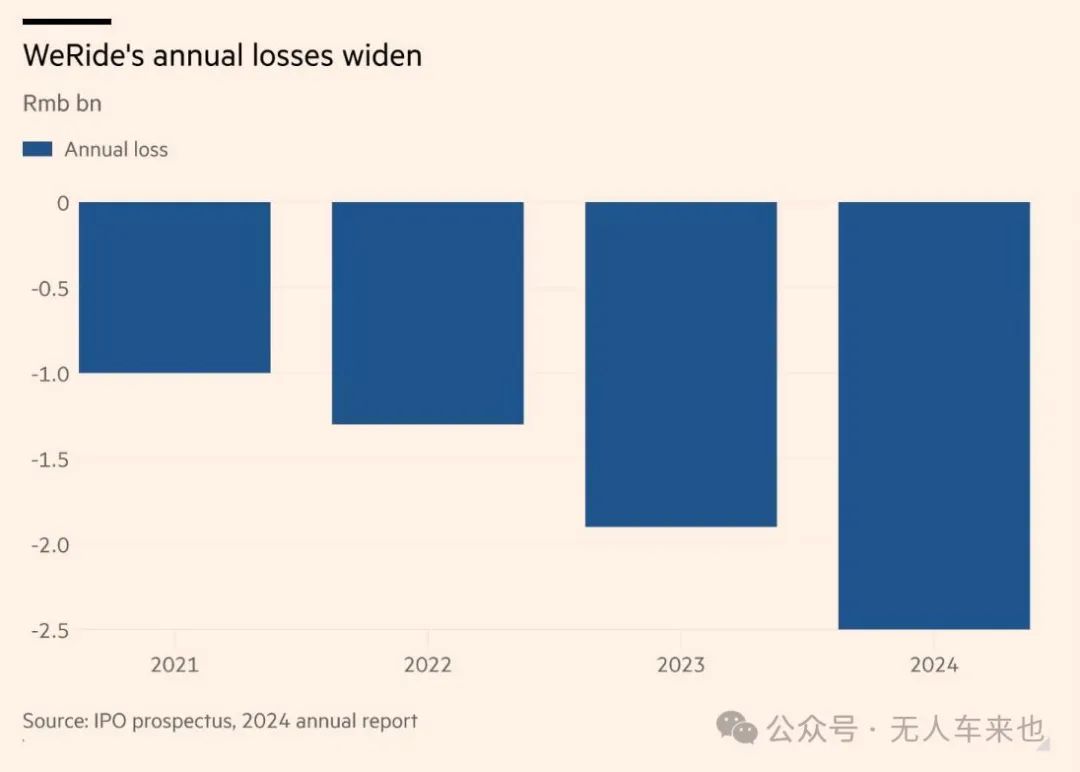

WeRide's 2024 financial report unveiled that the company's annual revenue amounted to 361.1 million yuan, marking a 10% year-on-year decline, while its net loss ballooned to 2.5168 billion yuan.

These figures underscore that amidst global expansion, the company remains entrenched in a "cash-burning" model.

1. Revenue Decline Factors:

- ADAS Business Contraction: Expiry of certain R&D contracts and a lag in new order acquisition.

- Service Income Reduction: A decrease in technical support services contributed to the overall revenue drop.

2. Factors Behind Expanding Losses:

- Persistent Rise in R&D Investment: Operating expenses surged to 2.2838 billion yuan in 2024, reflecting WeRide's commitment to heavy R&D investments.

- High Costs of Global Footprint: Conducting tests and operations across Europe, the Middle East, and various Asian regions incurs significant expenses in human resources, supply chains, etc.

Despite the mounting losses, WeRide emphasizes that its loss scale is "smaller compared to industry peers", indirectly highlighting the industry's overarching challenges. It's no surprise that for an emerging industry with immense market potential, initial cash burn is inevitable.

II. Industry-Wide Challenges: The Profitability Quandary for Autonomous Driving Firms

WeRide's predicament mirrors those faced by the entire autonomous driving sector.

Firstly, high technology costs: Core hardware such as LiDAR, high-precision maps, and AI chips remain expensive, with each vehicle modification costing tens of thousands to hundreds of thousands of dollars.

Software maintenance and updates necessitate continuous investments, which are challenging to recoup in the short term. Secondly, policy and regulatory uncertainties: Varying regulatory standards across countries and stringent approval processes for commercial licenses pose significant risks.

For instance, Cruise's operations were suspended in California following an accident, underscoring policy-related risks.

Thirdly, limited public acceptance: Consumers remain cautious about fully autonomous driving, and market education is a work in progress. Safety incidents (e.g., Tesla Autopilot accidents) further erode public trust.

Fourthly, immature business models:

- Robotaxi: Low order volumes and high operating costs hinder investment recovery.

- Technology Licensing: Automakers' increasing inclination towards in-house technology development (e.g., Huawei, Tesla) intensifies competition for third-party solution providers.

- Specialty Vehicles (e.g., unmanned minibuses, sanitation trucks): Limited market size impedes large-scale profitability.

Lu Daokuan, a mobile analyst at S&P Global, forecasts that Chinese Robotaxi companies might not attain profitability until 2028.

III. Potential Breakthrough Paths: Accelerating Commercialization

Despite the challenges, the industry is actively exploring viable profit pathways.

Cost Reduction and Efficiency Enhancement:

- Supply chain optimization and scaling up.

- Dedicated autonomous driving vehicles (e.g., Robotaxi developed in collaboration with Geely) offer cost advantages over modified vehicles and benefit from economies of scale in the long run.

- Price reductions in core components like LiDAR and chips will significantly lower hardware costs.

Policy Coordination: Advocating for a more permissive regulatory environment and collaborating with governments to facilitate autonomous driving legislation and relax testing licenses.

For example, WeRide has secured policy support in France, Switzerland, and other regions, expediting commercial pilot projects.

Diversified Business Models:

- Gradual Implementation of L2+/L3: Generating cash flow through advanced driver assistance systems (ADAS) before fully autonomous driving matures.

- Cross-Industry Collaborations: Exploring niche markets such as freight transportation and sanitation in partnership with Uber, logistics companies, etc.

(4) Technological Breakthroughs: End-to-End AI-Driven: WeRide has deployed end-to-end models in its L4 system, leveraging millions of hours of driving data for training to enhance its capability in handling complex scenarios.

As AI driving performance nears human-level, commercialization barriers will diminish, potentially shortening the timeline for profitability.

IV. Future Perspectives: The Crucial Window from 2025-2030

The autonomous driving industry stands at a pivotal juncture.

Short-term (2025-2028): Companies must balance R&D and commercialization, focusing on breakthroughs in cost reduction and policy bottlenecks.

Medium to Long-term (Post-2030): With technological maturity and regulatory perfection, Robotaxi and unmanned freight transportation could witness explosive growth.

WeRide's profit performance in recent years. Source: Financial Times

JPMorgan Chase projects that by 2033, WeRide could capture 3-8% of the Robotaxi market, with a potential valuation in the tens of billions of dollars, equating to hundreds of billions of yuan, positioning it as a commercial giant.

However, realizing this vision hinges on industry-wide breakthroughs.

V. Conclusion: Patience is Crucial for Autonomous Driving Commercialization

The road to profitability in autonomous driving is a marathon.

The current state of companies like WeRide underscores that technological leadership doesn't guarantee commercial success.

The industry necessitates lower costs, favorable policies, and mature business models to truly attain profitability.

Whether these obstacles can be overcome within the next five years will determine whether autonomous driving evolves into the next "Internet-level" industry or remains stagnant in the "laboratory stage" for an extended period.

For investors and practitioners, patience is arguably the most vital virtue at present.

In summary, Unmanned Vehicles Incoming (public account: Unmanned Vehicles Incoming) believes that WeRide's 2.5 billion yuan loss is merely the tip of the iceberg, and the entire industry is traversing "the darkness before dawn". Will Musk's "radical faction" emerge victorious, or will WeRide's "protracted war" culminate in a triumphant comeback? Share your predictions in the comments below!

References: Observer Network Report, "WeRide Warns that Profitability in Autonomous Driving Technology is 'Hard to Predict'"

-

![]()

A Humanoid Robot Becomes an Office Intern: The 'Reinforcement Learning' Journey of a Former NVIDIA Engineer

-

![]()

Meta Plans to Launch Cloud Infrastructure Business: Is Computing Power Really in Excess?

-

![]()

Giants Enter the Arena One After Another: The Embodied AI Battle Commences

-

![]()

Is It More Profitable to Build 'Hands' for Robots Than 'Humans'?

-

![]()

Yunling Optoelectronics Accelerates Its Listing on the Beijing Stock Exchange: Secures 989 Million Yuan to Bolster Production of Computing Optoelectronic Chips

-

![]()

From Drill Bits to Optical Coatings: A 200-Billion-Yuan Behemoth Quietly Unveils a New Business Front!

-

![]()

New Energy Vehicle Growth Slows: Are 370 Million Existing Cars the Next Lucrative Market?

-

![]()

Is Baidu Now Fostering Its Own 'Yao Shunyu'?