Robot Underworld Battle: Midea, Haier, and Gree in a 'Three Kingdoms War'

04/06 2025

04/06 2025

790

790

Source | Yuan Meihui

China's first domestic home appliance company with a market value exceeding 400 billion yuan has emerged.

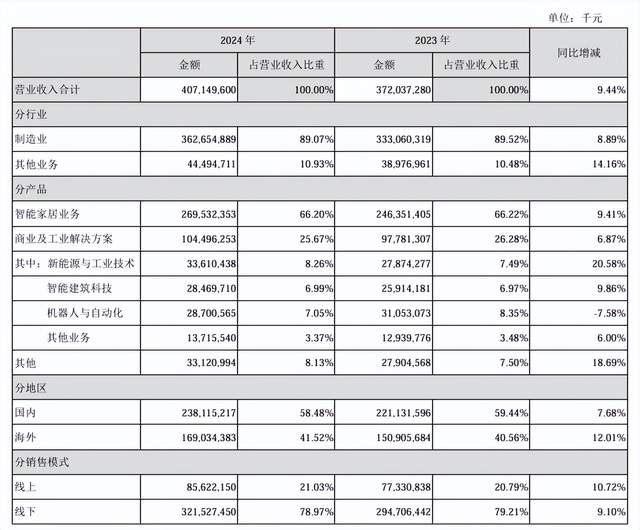

Recently, Midea Group and Haier Smart Home, two of the top three home appliance giants in China, released their 2024 annual reports, reporting revenues of 407.15 billion yuan and 285.981 billion yuan, respectively, and net profits attributable to shareholders of listed companies of 38.537 billion yuan and 18.741 billion yuan.

Although Gree Electric Appliances has yet to announce its 2024 performance, based on its revenue in the first three quarters, it is likely to trail behind Midea and Haier.

Behind the performance rivalry lies an even fiercer battle in the less visible realm: collectively venturing into the robot sector.

As the growth of the traditional home appliance market peaks and the benefits of the trade-in policy gradually diminish, Midea, Haier, and Gree have unanimously placed their bets on the robot sector. This seemingly 'convergent' choice of sector is actually an ultimate showdown of strategic genes—Midea wields the capital stick to 'buy globally,' Haier delves into scenario-based 'services,' and Gree focuses on independent research and development to 'hone its internal strengths.'

As robots become the 'Noah's Ark' for home appliance giants to navigate through cycles, whose strategy will be the first to break through the triple shackles of technology, cost, and market?

01

Achievements Through 'Buying'

Among the top three home appliance giants, Midea's robot business performs the best but also harbors the deepest anxieties.

Although Midea's robotics and automation business secured the domestic top spot with 28.7 billion yuan in 2024, its 7.58% year-on-year decline forms a 'glaring' contrast with the group's overall 14.29% increase in net profit attributable to shareholders.

Image Source: Midea Group 2024 Annual Report

Of course, the decline in the robotics business is not unique to Midea. Judging from the 2024 performance previews that have been released, a batch of leading industrial robot enterprises such as Estun Automation, Efort Intelligent Equipment, Topstar Robotics, and Siasun Robotics have all incurred losses to varying degrees. Among them, Efort Intelligent Equipment, which has released a performance quick report, saw its revenue decline by 27.79% year-on-year in 2024.

Behind the collective downturn of leading robot enterprises lies the tightening of domestic downstream application demand in the industrial robot market. For example, multi-joint robots, which account for the largest proportion of industrial robots, are significantly under pressure due to the tightening of demand in core downstream industries such as automobiles and new energy, showing a year-on-year decline.

The GGII research report shows that in 2024, the domestic production of industrial robots was 556,000 units, an increase of 14.2% year-on-year; during the same period, domestic sales of industrial robots were 302,000 units, a decrease of 4.5% year-on-year.

The automobile and new energy industries happen to be several major downstream application areas relied upon by Midea's Kuka robots.

Since acquiring a 5.4% stake in the German Kuka company from the secondary market in 2015 to initiate the 'robot strategy,' completing the acquisition of a 94.55% stake in Kuka in 2017, to announcing the full acquisition of Kuka's equity and privatization delisting in 2021, and finally completing the transaction in November 2023, ending this acquisition marathon that cost over 30 billion yuan and lasted eight years, Midea overnight ascended to the top four global industrial robots. This demonstrates its weight.

The acquired Kuka has also been 'very competitive.' Data shows that Kuka's revenue and profitability in 2023 both hit record highs. At that time, Midea's robotics and automation business achieved a year-on-year revenue growth of 24.49% to 37.258 billion yuan, accounting for 10.01% of the group's total revenue for that year. Among them, the income contribution of Kuka China increased from 15% in 2020 to over 22% in 2024.

In 2024, Kuka's industrial robots continued to increase their domestic market share, steadily rising to 8.2%.

Even so, it is still difficult to conceal the impact of shrinking demand in core downstream application areas. The slowdown in the expansion of the new energy vehicle industry chain, adjustments in photovoltaic and lithium battery capacity, and weak demand for 3C electronics have directly impacted order volumes. The year-on-year decline in Midea's robotics and automation business in 2024 mentioned earlier is the most direct result.

More severely, the concentration of the industrial robot market continues to increase, and giants such as Fanuc and ABB still suppress peers in the high-end market due to their technological barriers in core components. Yuan Meihui noticed that Midea also reduced its holdings in stocks of robot and industrial chain-related enterprises such as Efort Intelligent Equipment over the past year.

Image Source: Midea Group 2024 Annual Report

Perhaps to break the cycle curse, Midea is accelerating its advance into humanoid robots.

In 2024, Midea entered the humanoid robot sector and established a humanoid innovation center. In March 2025, Midea's humanoid robot prototype was exposed for the first time and was later dubbed the 'most beautiful humanoid robot' at the 2025 ITES Shenzhen Industrial Exhibition.

From the disclosure, this humanoid robot can not only perform 'flashy' actions such as handshakes, heart gestures, and dancing but also execute complex tasks such as opening bottle caps and screwing through voice commands. Behind these functions lies the fruit of Midea's acquisition of Kuka—deep accumulation in core components such as servo motors, reducers, and sensors.

However, the technological gap between industrial and consumer scenarios far exceeds expectations. The home environment that humanoid robots will face in the future requires coping with complex terrain, flexible interaction, and long battery life, and the rigid motion control technology accumulated by Kuka in automotive factories is difficult to directly transfer. Midea attempts to transform the 'high precision' of industrial scenarios into the 'high intelligence' of consumer scenarios, which may fall into the paradox of 'building a maid with machine tool logic.'

The attitude of the capital market has already diverged. Although Midea's R&D investment increased by 11.31% year-on-year to reach 16.2 billion yuan in 2024, the valuation of its robotics business is still classified as 'traditional manufacturing,' and compared with star projects such as Tesla's Optimus and Boston Dynamics' Atlas, its technological imagination is significantly limited.

02

The 'Weaknesses' of the Giants

Compared to Midea, Haier and Gree have their unique characteristics and 'weaknesses' in their robot sector layouts.

Looking back at the development history of Haier and Gree, the timing of their entry into the robot sector is not much different from that of Midea. According to Tianyancha, Haier Robot Technology (Qingdao) Co., Ltd. under Haier and Gree Intelligent Equipment Co., Ltd. (hereinafter referred to as 'Gree Intelligent Equipment') under Gree were both established in 2015. At that time, in addition to purchasing Kuka shares, Midea also cooperated with Yaskawa Electric, one of the 'Big Four' robot companies, to establish two robot joint ventures.

Judging from Haier's subsequent development in the robot sector, its products are better at capturing user pain points.

In the past year, Haier has made many moves in the robot sector. It first joined hands with the humanoid robot enterprise UBTECH to launch China's first humanoid robot 'Kuafu' specifically designed for households. In terms of functionality, this product can water flowers, wash and dry clothes; subsequently, Haier made a big move to acquire a controlling stake in the industrial robot giant Sintech; and at AWE 2025 recently, Haier signed a strategic cooperation with another humanoid robot enterprise Xingdong Jiyuan to jointly launch a service robot based on smart home scenarios, aiming to complete the last piece of the puzzle for household service robots in the direction of unmanned housework.

Behind this series of actions, Haier's purpose is already very clear: it intends to deeply bind with the smart home strategy and use robots to achieve full-house interconnectivity.

However, such scenario-based innovation will face another challenge—commercialization. Currently, the price of a humanoid robot butler will not be less than 100,000 yuan, which largely excludes the vast majority of households.

The Third National Time Use Survey Bulletin released by the National Bureau of Statistics shows that the average daily time spent on household labor activities by participants is 1 hour and 59 minutes, a decrease of 28 minutes compared to 2018. Of course, this includes the popularity of smart home devices and the widespread use of home services such as ordering takeout and finding housekeepers.

But in real life, a 'household butler' costing over 100,000 yuan has little cost-effectiveness to speak of.

It is understandable that Haier wants to strengthen its 'scenario brand' label through robots, but it will be difficult to stand out in the short term. And it may also face long-term losses due to technology investment.

Unlike Midea and Haier, Gree's 'obsession' with autonomy and controllability borders on paranoia.

In past financial reports, Gree often emphasizes independent research and development as well as load indicators. For example, in the 2022 financial report, Gree emphasized that its developed industrial robots have completed the development of industrial robot products ranging from 1-600KG; in the heavy-load series, it has developed the GR270/2.65 industrial robot and completed the development of its first robot motion control system with independent intellectual property rights.

Since 2015, Gree industrial robots have been used in various production bases within Gree and have gradually replaced manual operations in some positions. In 2017, Gree Intelligent Equipment's industrial robots began to be sold on a small scale and provided automation transformation services.

In addition, according to media reports, in Gree's intelligent equipment factory, its industrial robots can replace humans to complete various tasks such as welding, assembly, screening, arrangement, palletizing, and sorting.

Based on comprehensive reports, Gree's robot-related products are still mostly for internal use. Previously, Yuan Meihui also inquired with relevant personnel from Gree whether core component products such as servo motors are independently researched and supplied. The other party said that both self-supply and external sales are available, and the top few domestic robot companies are Gree's customers.

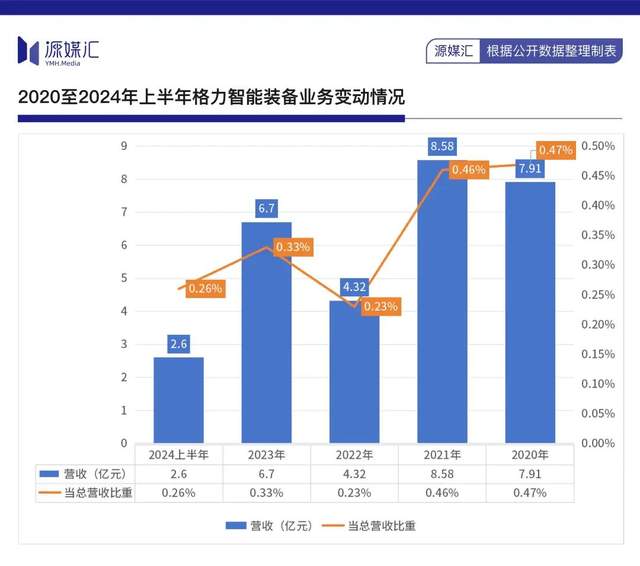

However, this is reflected rather cruelly in performance: in the first half of 2024, Gree's intelligent equipment segment revenue was only 260 million yuan, accounting for only 0.26% of the total revenue for the same period.

This may also reveal the fatal flaw under Gree's 'closed-loop logic' of independent research and development for internal use.

The strategy of prioritizing internal production lines, while ensuring technological iteration in scenarios such as air conditioning welding and automotive parts processing, has made the products lose market competitiveness. Gree robots are like 'greenhouse flowers' that perform excellently in their own factories but immediately face dimensionality reduction attacks from Fanuc and Kuka once they enter the external market.

Gree's conservatism in the robot sector is actually one of the epitomes of its failed diversification strategy.

The dissolution of the mobile phone business team, the explosion of Yinlong New Energy, and the premature end of prepared meal equipment—these failures have not only depleted Gree's funds but also the time window for technology transfer. When Midea taps into automobile manufacturing through Kuka and Haier infiltrates the industrial internet through COSMOPlat, Gree is still trapped in the 'air conditioning mindset' and views robots as production tools rather than strategic products.

03

Behind the Path Divergence

The differences between the traditional top three home appliance giants in the robot sector essentially stem from their exploration of three common ultimate propositions: technological belief, ecosystem construction, and cycle navigation.

AI-generated conceptual image of robotic appliances

From the perspective of technological belief, has Midea's ten billion yuan investment in R&D fallen into the trap of 'big but not strong'? Has Haier's scenario-based innovation degenerated into a victim of technological pragmatism? Can Gree's 'closed-door policy' survive the long night of market validation?

When Midea and Haier attempt to integrate the industrial chain with the industrial internet and Gree completes a closed loop through independent research and development, each company's choice of different ecosystems also exposes their shortcomings, such as coordination issues, missed cross-border opportunities, and integration dividends.

Industrial robots are significantly affected by macroeconomic fluctuations, service robots need to cultivate user awareness, and the autonomy of core components relies on long-term investment—under the superposition of these triple cycles, who can withstand the patience of the capital market?

The 'divergence' in path choices ultimately stems from different perceptions of downstream application scenarios. Taking humanoid robots as an example, industry insiders generally believe that humanoid robots must first be deployed in industrial scenarios and gradually enter household scenarios.

'When considering applications alone, I believe the industrial sector will be the easier path. However, for widespread adoption, particularly in commercial settings, households or similar scenarios are more likely to take the lead.' Liang Kaixiang, a senior product manager specializing in robots, shared his insights with Yuan Meihui on which scenario humanoid robots are most likely to make initial inroads.

Liang elaborated that in industrial environments, task objectives and working conditions are relatively fixed. In these defined settings, developers can more readily design humanoid robots to fulfill specific tasks, akin to the humanoid robots seen during this year's Spring Festival Gala or the logistics handling robots previously developed by Boston Dynamics. Hence, the closed and determined nature of industrial scenarios facilitates the deployment of humanoid robots. Nevertheless, for commercial adoption, humanoid robots must not only accomplish predefined goals and tasks but also surpass the threshold of cost-effectiveness.

'The existing industrial scenarios already boast cost-effective solutions, making it challenging for humanoid robots to compete. Their multi-sensor capabilities, multi-degree-of-freedom joints, and AI capabilities grant them an edge in handling complex and non-standard tasks. However, these types of tasks predominantly arise in daily life rather than industrial settings,' Liang noted. 'Therefore, from the perspective of product functionality, demand alignment, and market potential, if humanoid robots aspire to commercial success, they will likely depend on household scenarios characterized by non-standard and complex tasks.'

Another senior industry insider, who wished to remain anonymous, concurred with Yuan Meihui, stating, 'Based on current technological advancements and market trends, humanoid robots are more likely to achieve large-scale deployment in industrial rather than household scenarios.'

Amidst this backdrop, the robotics sector is redefining the valuation paradigm for home appliance giants.

Midea must demonstrate that its 28.7 billion yuan revenue from robots is not a 'Kuka dependency' but a growth engine fueled by both technology and market demand. Haier needs to break the spell of service robots being 'popular yet unprofitable' and translate scenario-based narratives into tangible financial returns. Gree, on the other hand, faces the harshest scrutiny: if technological advantages fail to translate into market success, will its closed-loop ecosystem degrade into an 'innovation graveyard'?

Notably, in 2024, while Midea achieved a net operating cash flow of 60.5 billion yuan, it used 70% of its repurchased shares for cancellation. Haier accelerated its global expansion yet fell short of Gree in net profits. Gree, despite ample financial reserves, has been cautious in investing in robotics.

These actions hint at a shift from 'scale expansion' to 'value defense' among the giants, signifying that the ultimate battle in the robotics sector has only just commenced.

Note: Some images are sourced from the internet. Please inform us of any infringement for prompt removal.

-

![]()

A Humanoid Robot Becomes an Office Intern: The 'Reinforcement Learning' Journey of a Former NVIDIA Engineer

-

![]()

Meta Plans to Launch Cloud Infrastructure Business: Is Computing Power Really in Excess?

-

![]()

Giants Enter the Arena One After Another: The Embodied AI Battle Commences

-

![]()

Is It More Profitable to Build 'Hands' for Robots Than 'Humans'?

-

![]()

Yunling Optoelectronics Accelerates Its Listing on the Beijing Stock Exchange: Secures 989 Million Yuan to Bolster Production of Computing Optoelectronic Chips

-

![]()

From Drill Bits to Optical Coatings: A 200-Billion-Yuan Behemoth Quietly Unveils a New Business Front!

-

![]()

New Energy Vehicle Growth Slows: Are 370 Million Existing Cars the Next Lucrative Market?

-

![]()

Is Baidu Now Fostering Its Own 'Yao Shunyu'?