Cloud and AI: Alibaba's Catalyst for Growth

09/01 2025

09/01 2025

762

762

Written by | Hao Xin

Edited by | Wu Xianzhi

Alibaba's financial report for the first quarter of FY2026 arrived late but with promising news.

Concerns about substantial subsidies for instant retail dragging down profits were swiftly overshadowed by the robust growth in cloud computing and AI.

For the quarter ended June 30, 2025, the Cloud Intelligence Group's revenue stood at 33.4 billion yuan, marking a 26% year-on-year increase and setting a new high for growth over the past three years. Excluding consolidated subsidiaries, revenue growth also reached 26%, primarily fueled by the surge in public cloud revenue. Notably, AI-related product revenue maintained triple-digit year-on-year growth for the eighth consecutive quarter.

Chief Financial Officer Xu Hong noted that the strong demand for AI has spurred demand for other public cloud services, such as computing and storage. Consequently, the department's adjusted EBITA increased by 26% year-on-year to 2.95 billion yuan.

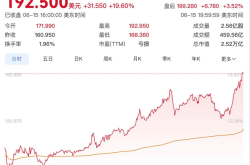

The exceptional performance of cloud computing, akin to a market catalyst, propelled Alibaba Group's stock price up by 13%.

In this quarter's financial report, Alibaba's "1+6+N" structure became a thing of the past, with the six major groups consolidated into four core businesses, focusing solely on e-commerce and the "Cloud + AI" strategy. Within a short span, these two main businesses formed a complementary force, with financial fluctuations stemming from Taobao Flash Sales mitigated by the vast potential unlocked by cloud and AI. The growth signal from the cloud business, functioning as a stabilizing factor, alleviated concerns about Q3 (the intense phase of the food delivery war) to some extent.

Despite ample financial resources, the initial signs of a two-front war have already exerted considerable pressure.

The financial report revealed that Alibaba Group's free cash flow experienced a net outflow of 18.815 billion yuan this quarter, compared to a net inflow of 17.4 billion yuan in the same period last year, resulting in a significant gap of 36.2 billion yuan. This was primarily due to increased spending on cloud infrastructure and massive investments in "Taobao Flash Sales".

Whether considering the short-term or long-term perspective, Alibaba Cloud appears to bear a heavier burden.

MVP Player

How did Alibaba Cloud, as the MVP (Most Valuable Player) of this quarter's financial results, perform?

Compared to previous quarters, Alibaba Cloud's revenue growth rate hit an all-time high. Q1 FY2025 (April-June 2024) marked a turning point in Alibaba Cloud's development. Prior to this, revenue growth had stagnated. In Q1 FY2025, investments in large models and AI began to bear fruit, with Alibaba Cloud's revenue increasing by 6% year-on-year. Since then, it has achieved sustained year-on-year growth, rising from 7%, 13%, 18% to 26% in Q1 FY2026.

The growth trajectory of Alibaba Cloud's revenue indirectly underscores the driving force of the AI cloud market. The financial report highlights that, fueled by eight consecutive quarters of triple-digit growth in AI-related revenue, AI revenue accounted for over 20% of external commercialized revenue this quarter.

When compared horizontally, as an established cloud vendor spanning multiple time cycles, Alibaba Cloud's revenue growth rate is also impressive. In the quarter ending in June, AWS's revenue increased by 17.5% year-on-year, Google's revenue increased by 13.9% year-on-year in the second quarter, and Microsoft's overall cloud sales increased by 27% year-on-year.

Analyzing Alibaba Cloud's revenue growth in the first half of the year, it primarily stemmed from two sources: the explosive growth driven by DeepSeek during the Spring Festival and the new post-training demand sparked by the Agent application paradigm.

As the first quarter to fully benefit from DeepSeek in China, the growth rate in Q2 2025 better reflects normal business trends. Wu Yongming revealed during the previous quarter's earnings call that customer projects related to the DeepSeek effect were largely launched in Q2, encompassing both traditional computing power demand and some inference demand.

Another component of the growth came from the transformation of customers' model training methods. Instead of relying on data flooding for model training, enterprises now optimize them for specific business scenarios. They first label scenario data and then perform SFT (Selective Fine-Tuning) on open-source or closed-source models. Like pre-training, post-pre-training consumes substantial tokens and computing power and necessitates profound industry expertise, presenting a new opportunity for cloud vendors.

Wu Yongming mentioned that they have also observed new opportunities in the training direction. Some education and healthcare companies are performing post-training based on open-source Tongyi models. Alibaba Cloud views this as a new commercialization opportunity for open-source models and plans to provide post-training-related services in the future.

"Combining the rapid growth of inference demand, we anticipate Alibaba Cloud's overall growth rate to continue rising in the coming quarters."

In terms of profitability, Alibaba Cloud's adjusted EBITA margin increased slightly to 8.8% quarter-on-quarter in the new quarter. However, capital expenditures surged from approximately 11.9 billion yuan in the same period last year to approximately 38.7 billion yuan this quarter. Due to heavy investments, it has yet to recover to its peak profit margin level.

From Profit to Market Capture

Wu Yongming believes that compared to traditional cloud computing, the transformation brought about by AI will significantly increase the concentration of the cloud computing market. The advent of AI technology has led developers to require more technology stacks when developing applications, thereby pushing them to choose vendors with comprehensive technology product portfolios, "especially those with leading capabilities in individual products".

Currently, Alibaba Cloud directly benchmarks Google Cloud from infrastructure, model research to products and platforms.

The latest news is that Alibaba will independently develop a new generation of AI chips, manufactured by domestic foundries and compatible with NVIDIA's software ecosystem, primarily targeting AI inference tasks.

From a strategic perspective, Alibaba Cloud has finally completed the crucial link of "autonomous and controllable computing power". Developing its own AI inference chips can reduce dependence on external suppliers like NVIDIA, enhance supply chain resilience, and ensure the supply of computing power. Additionally, it can bolster pricing power and cost control capabilities, continue to reduce inference costs, and increase gross margins leveraging Alibaba Cloud's existing scale advantages.

Leading cloud vendors abroad, such as Amazon, Google, and Microsoft, all follow the "Cloud + Self-Developed Chips" approach, providing a reference for Alibaba Cloud's decision-making. By strengthening the vertical integration of "Cloud + AI + Chips", Alibaba Cloud will form a trinity of "cloud platform + large models + chip infrastructure", facilitating the establishment of higher market barriers in the future.

At the model level, Alibaba's Tongyi large model family benchmarks Google's Gemini and has established a reputation in open-source communities both domestically and internationally. The Qianwen open-source model series has become the choice of many enterprises. Compared to Google, the current Tongyi large model series is slightly weaker in multimodal and video generation fields and has yet to produce a "blockbuster" video generation model akin to Veo 3. However, in the field of video generation, it has been preempted by products such as Keling and Hailuo.

In terms of the AI application ecosystem, Google is promoting the integration of new and old businesses. For instance, Workspace (Docs, Meet, Gmail, etc.) and Chrome have become core AI landing scenarios, with features like Meet meeting records, Google Vids, and photo-to-video functions driving AI penetration.

Under Wu Yongming's active promotion, Alibaba's top-down advancement is not slow. Tongyi large models have been integrated into Alibaba's ecosystem, including DingTalk, Taobao, Gaode, and Quark. For example, DingTalk AI incorporates the Tongyi large model to provide capabilities such as intelligent writing, meeting minutes, to-do generation, and knowledge Q&A; Taobao, Tmall, and 1688 enhance user experience through AI customer service, product recommendations, and marketing copywriting generation; Quark AI search and smart browsers offer functions like AI search, summarization, and Q&A, creating a new generation of AI-native entry points.

Alibaba has emerged as one of the companies with the most comprehensive AI narrative logic chain in China.

Over the past four quarters, Alibaba has invested over 100 billion yuan in AI infrastructure and research and development, with plans to add 380 billion yuan in capital expenditures over the next three years.

After several quarters of earnings calls, Alibaba Cloud has gradually de-emphasized gross margin and shifted its focus to keywords like "expanding market share", "growth rate", and "competing for users".

This three-step approach will lay the foundation for reassessing Alibaba Cloud in the AI era: cloud revenue and sustained growth to boost market confidence in Alibaba; full-stack investment to bring new scale effects and cost reductions, leading to an increase in cloud profit margins; ultimately, enabling Alibaba Cloud to convert higher profits and facilitating Alibaba's comprehensive transformation into an AI-driven company.

Alibaba Cloud Needs Synergy

In terms of investment, Alibaba Cloud has entered the ranks of military competition. In the short term, Alibaba Cloud can indeed elevate the imagination space, but like many vendors, the AI cloud is still in the stage of value demonstration.

Market sentiment is polarized. Some are optimistic, believing that the incremental market of AI cloud can hedge against short-term risk fluctuations. Others remain cautious, believing that burning money to exchange growth in the e-commerce market cannot be alleviated by the potential of cloud computing.

Although Alibaba Cloud is indeed very close to or even surpasses Google Cloud in strategic and single-point technical capabilities, at this stage, Google Cloud is demonstrating a trend of "value exchange".

An interesting phenomenon is that OpenAI initially intercepted Google's new product launches. However, over time, OpenAI has become a promoter of Google's new products, with customers viewing demos at OpenAI and then placing orders with Google Cloud.

The Q2 2025 financial report revealed that the number of Google Cloud contracts exceeding $250 million doubled year-on-year, and the number of contracts exceeding $1 billion was the same as the entire year of 2024, indicating that major customers' trust and investment in Google's AI product portfolio continued to increase. This quarter, GCP's new customer base increased by nearly 28% month-on-month, with over 85,000 enterprises using Gemini, and usage increased by 35 times year-on-year, demonstrating that its AI large models have been deeply adopted by leading customers across various industries.

Google Cloud has organically integrated single-point capabilities to form a set of "integrated commercialization capabilities" for customers that can be scaled and implemented. In contrast, domestic cloud vendors, including Alibaba Cloud, are still in the exploration stage and have yet to find a deterministic path.

For example, DingTalk AI and Taobao AI have a vast user base but are more concentrated at the level of efficiency tools and have not yet widely formed benchmark cases like Google AI Agent, which deeply integrates into business processes and brings quantifiable business benefits. Alibaba Cloud's AI capabilities have landed in multiple industries, but compared to Google's AI Agent, which is deeply integrated into Cloud products and delivers clear "ROI", Alibaba Cloud's AI value is mostly still in the "capability provision" and "preliminary application" stages.

To draw an analogy, Google Cloud has integrated engines, batteries, navigation, smart cabins, and other components to create an "autonomous luxury sports car". Customers only need to specify the destination and can arrive efficiently, comfortably, and safely. Alibaba Cloud now has top-tier engines, batteries, tires, and other components, but it still needs to help customers "assemble" or "find a third party to help" before it can hit the road.

This year's first-half financial report set a promising start but cannot stop here.

Beyond reveling in the success of Tongyi Qianwen topping the charts, Alibaba Cloud needs to enhance its integration capabilities.

-

![]()

In-depth | Survival Transformation of 38 Million Freight Drivers: How Platformization Defines the Next Decade?

-

![]()

Why Have ‘Computing Power Rental’ Companies Emerged as the Biggest Winners in the AI Era Amid Soaring Chip Prices?

-

![]()

DeepSeek's Financing Details Revealed! How Liang Wenfeng Secured Control

-

![]()

Valued at 210 Billion Yuan, Generating 42 Billion Yuan in Annual Revenue, Xiaohongshu May Proceed with IPO

-

![]()

Three Straight Months of Growth in Heavy Truck Sales: Both New and Veteran Players Are on the Same Wavelength!

-

![]()

AI Rewrites the Logic of Going Global: Cross-border E-commerce Reaches a New Turning Point

-

![]()

DeepSeek Secures Over 50 Billion Yuan in Initial Funding Round: Tencent and CATL Among Investors

-

![]()

Trillionaire Musk