"AI" Google: No Ghost Stories, Just Bumper Harvests

04/30 2026

04/30 2026

622

622

Google's Q1 results have once again "blown up," with 40% of its revenue growth coming from AI-related cloud income. It might be time to shed Google's advertising label and brand it as an AI company.

Key takeaways:

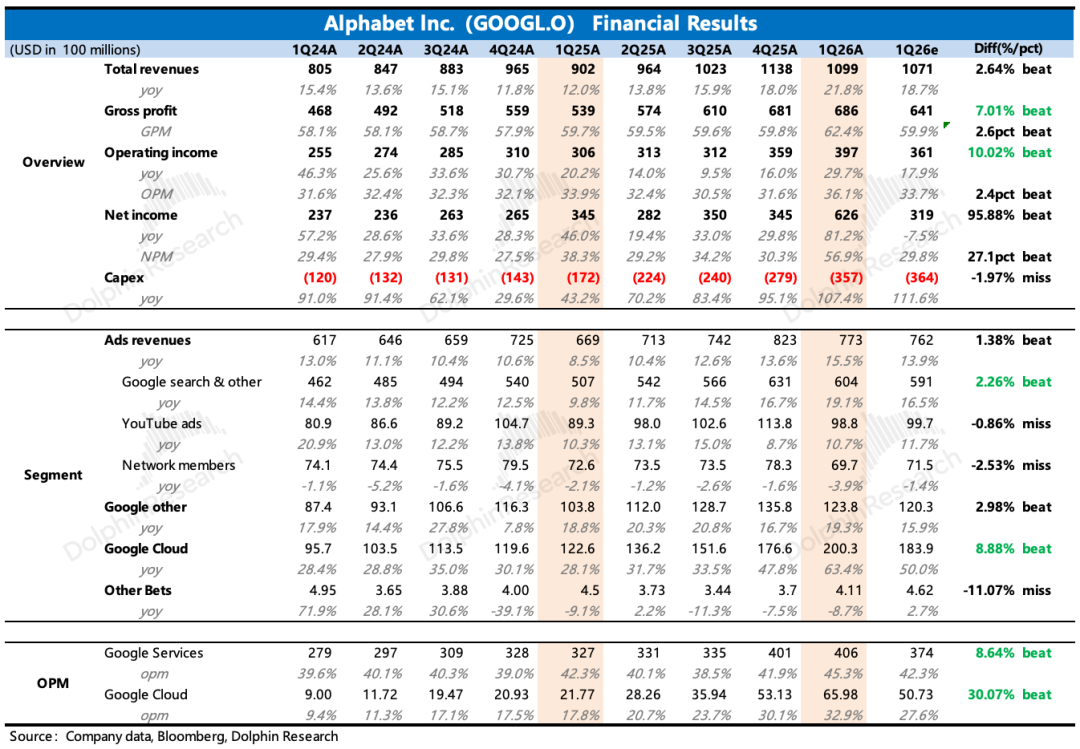

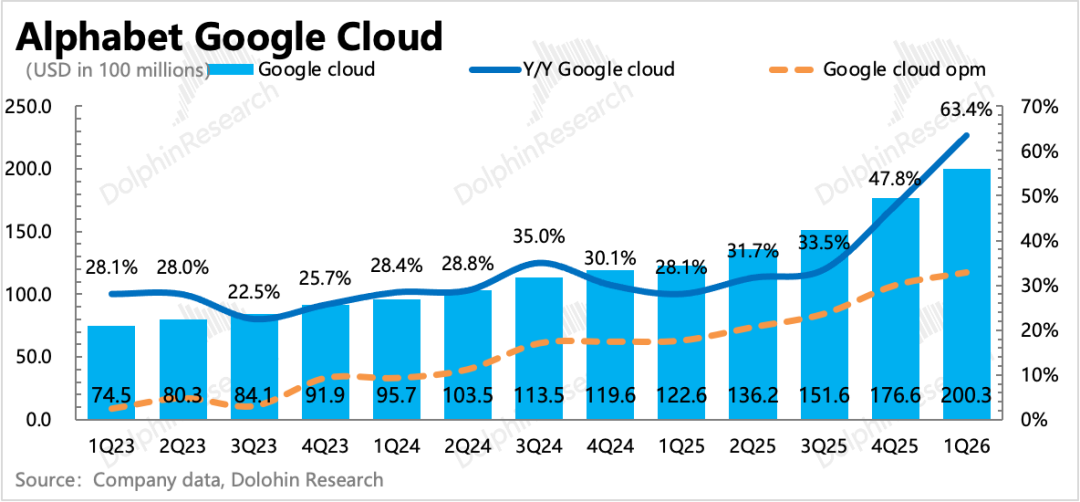

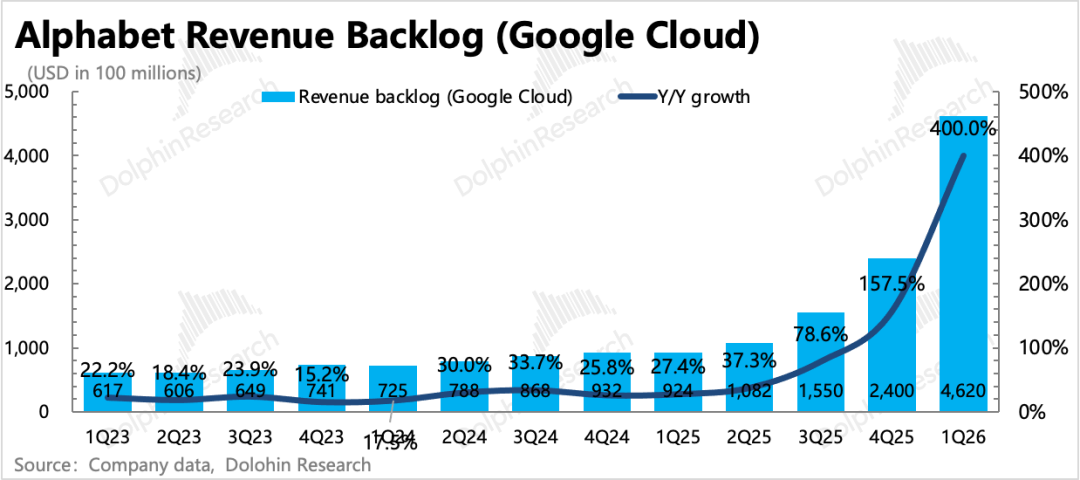

1. Explosive cloud business, solid valuation foundation: With revenue of $20 billion and a 63% growth rate, the performance was a pleasant surprise even from a more optimistic buyer's perspective (+60%), far outperforming peers. Critically, the current backlog stands at $462 billion, nearly doubling from $240 billion at the end of last year. The majority consists of cloud contracts, with a smaller portion from direct TPU hardware sales (for customer-built data centers).

Of the net increase of $220 billion, Anthropic and Meta are likely the main contributors, but among other clients, several new billion-dollar deals were signed, along with additional new demands from existing clients.

The substantial backlog, coupled with the recently released eighth-generation TPU, brings more comprehensive AI infrastructure solutions, ensuring high revenue growth for at least 1-2 years (half of the orders will be recognized as revenue within two years).

The company also highlighted that Gemini Enterprise, launched in Q4 last year, showed strong momentum in Q1, with a 40% quarter-over-quarter increase in monthly active paying users. Additionally, direct API calls by clients surged from 10 billion tokens per minute at the end of last year to 16 billion.

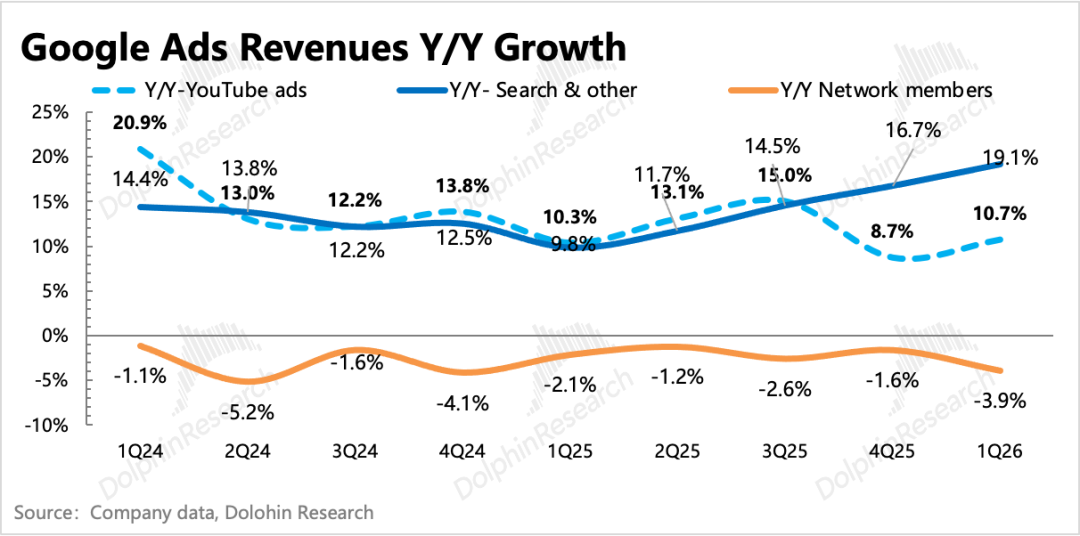

2. No ghost stories, search remains strong: Revenue grew by 19%, and even accounting for a potential foreign exchange tailwind of less than 2 percentage points, there was no slowdown from the previous quarter. This reflects two aspects: first, the impact of internal and external AI erosion is still limited, and the company is still enjoying the benefits of increased user search volume and improved conversion rates driven by AI; second, it confirms the robust U.S. macroeconomic environment in Q1 and the industry's brand marketing boost from the Winter Olympics.

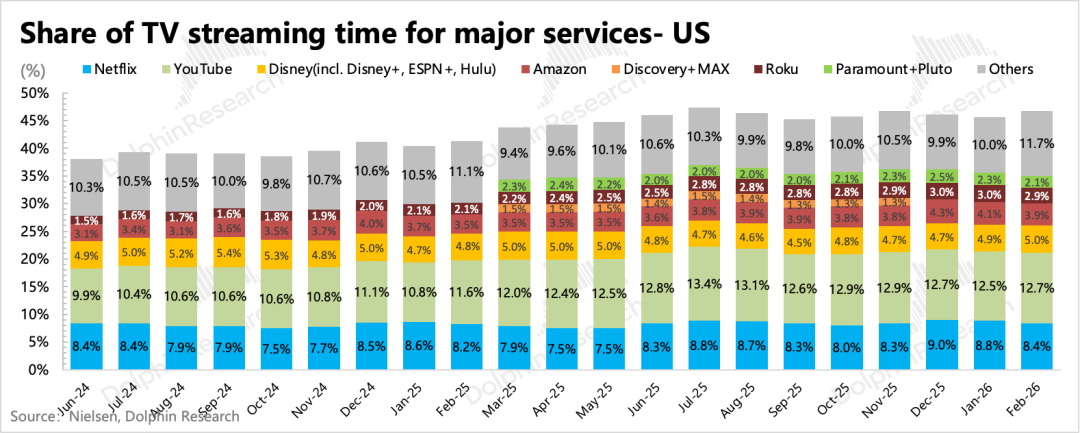

3. Slow recovery in YouTube advertising: YouTube's ad revenue grew by 10%, again missing consensus expectations. While there was a slight sequential recovery, growth remained burdened, representing an inevitable adjustment period as long-form video integrates short-form video to adapt to industry transformation.

Competition in the traditional long-form video pre-roll ad market has also intensified, with Netflix, Disney, and Amazon Prime all ramping up ad-supported packages in recent years. Meanwhile, Shorts, facing stronger short-form video competitors like Reels and TikTok, has yet to fully compensate for the long-form video growth gap in the short term.

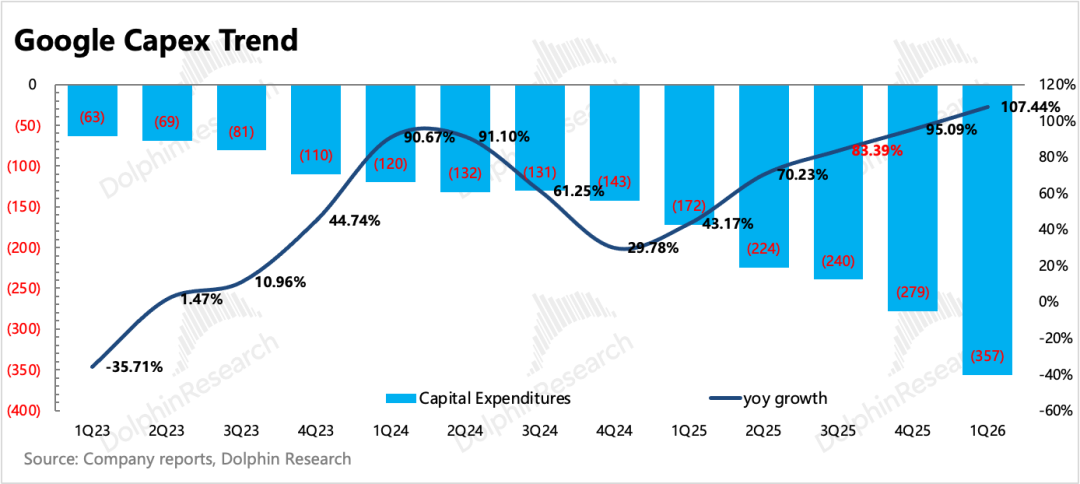

4. Slight increase in Capex: This year's Capex guidance was raised slightly from $175-$185 billion to $180-$190 billion, representing a year-over-year doubling. Q1 confirmed $35.7 billion, a 107% increase year-over-year, slightly below the consensus expectation of $36.4 billion. However, strong demand ensures continued Capex expansion, with management expecting significant growth to persist through 2027.

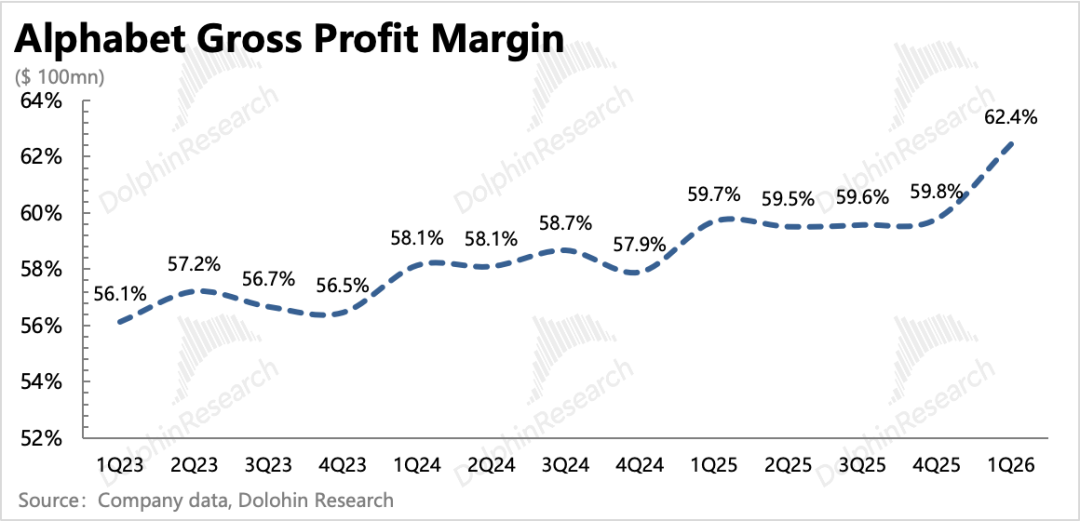

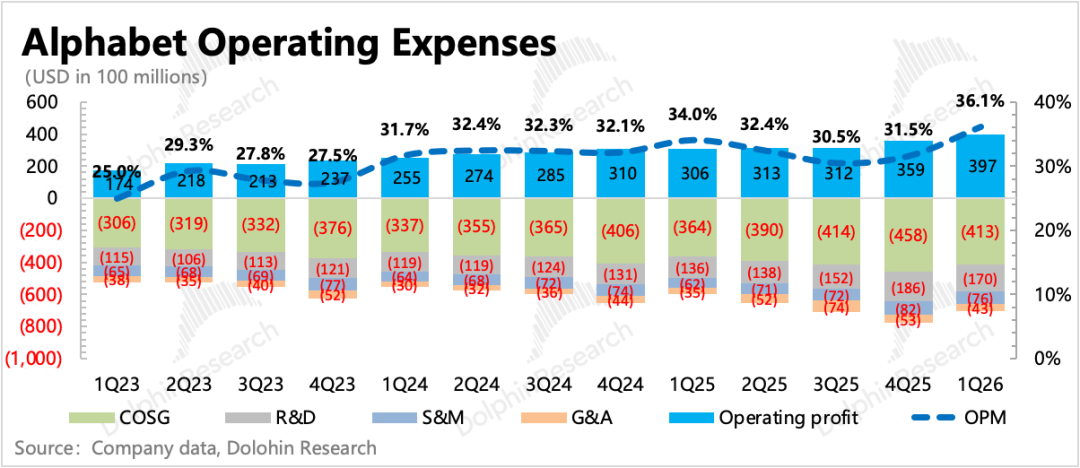

5. Short-term profit margin tailwind: Q1 operating profit margin climbed to 36%, up 2 percentage points year-over-year, primarily driven by gross margin improvement, while operating expenses increased slightly by 0.5% year-over-year. This phenomenon of simultaneous heavy investment and margin expansion is intriguing.

In the short term, AI demand has Continuously fulfilling (sustained and rapidly become a key growth driver, with cloud business contributing 40% of total revenue growth), but at the same time, Capex investments, which reaccelerated in the second half of last year and are expected to double this year, are still being depreciated quarterly, with a gradual impact on costs. Therefore, a short-term window for margin improvement exists due to the severe supply-demand imbalance.

Conversely, starting in the second half of the year, the suppressive effect of high investments on profit improvement is expected to emerge, unless the current boom and supply-demand gap continue to widen, allowing cloud providers to raise prices further.

6. Suspension of buybacks, slight increase in dividends: Due to high investments, to ensure sufficient cash flow for flexible investments (including internal and external investments), buybacks were suspended in Q1, and debt financing was issued. Dividends increased slightly by 5% year-over-year starting this year, but the scale remains too small to make a significant difference.

7. Key metrics vs. expectations

Dolphin Research's View

Similar to last quarter, Google once again demonstrated explosive growth, validating the imagination behind its AI narrative. Meanwhile, the consistently reliable management team showed firm commitment to investment through a substantial Capex increase, indicating a promising future.

AI has moved beyond the stage where mere promises and valuations could propel it to new heights. The model of investing while delivering results is the most convincing approach for attracting capital. Therefore, Google's current phase—where AI activates revenue acceleration, fuels growth imagination, and ensures non-deteriorating profit margins—is precisely what investors want to see.

However, we also note that profit margins are benefiting from a short-term window, and whether they can continue to improve steadily will depend on tracking changes in the AI supply-demand gap. Based on our estimates, some pressure from high investments is expected to emerge in the second half of the year. Potential mitigation strategies could include workforce optimization and developing more high-value products or services.

As long as the "investment for growth" narrative holds, capital will continue to offer a premium. However, Google's post-market surge of 7% has pushed its valuation to $4.5 trillion, reaching 28x/25x P/EBIT for this year and next year's expectations. Whether measured against Google's historical valuation range or its current growth rate, this valuation sits above the median.

We remain optimistic about Google's growth prospects and endorse its mid-term logic. However, considering the potential profit margin pressure in the second half of the year and the high-valuation listings of OpenAI and Anthropic this year—which could intensify competition due to their own monetization needs or impose higher financial requirements after disclosing operating data—any disappointment could trigger sentiment contagion within the industry.

Therefore, from a risk-reward perspective, we prefer to seek more comfortable entry points during adjustments caused by industry sentiment divergences.

Below is a detailed analysis of the financial results:

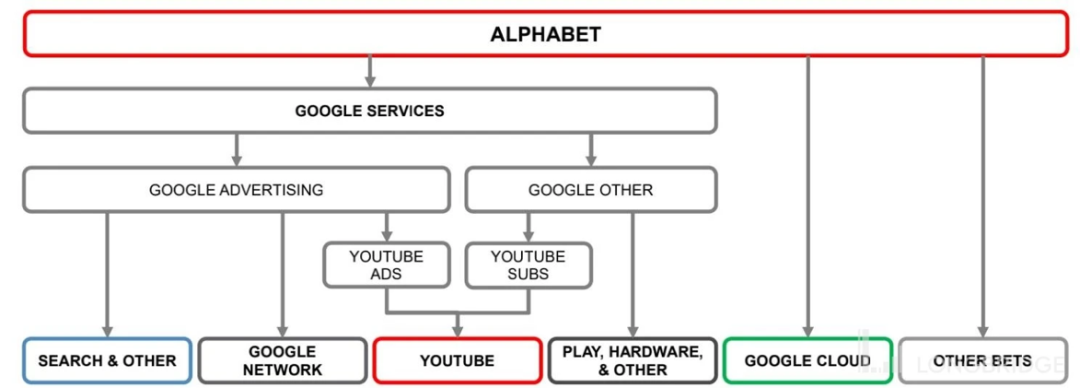

1. Google Overview

Google's parent company, Alphabet, has a diverse business portfolio, and its financial reporting structure has undergone multiple changes. For those unfamiliar with Alphabet, here's an overview of its business architecture.

Briefly outlining Google's long-term fundamental logic:

a. Advertising remains the primary revenue contributor and profit driver. Search advertising faces medium- to long-term erosion risks from feed-based ads, with high-growth streaming platform YouTube serving as a complement.

b. The cloud business has become the company's main growth driver and narrative, as well as the most direct beneficiary of AI.

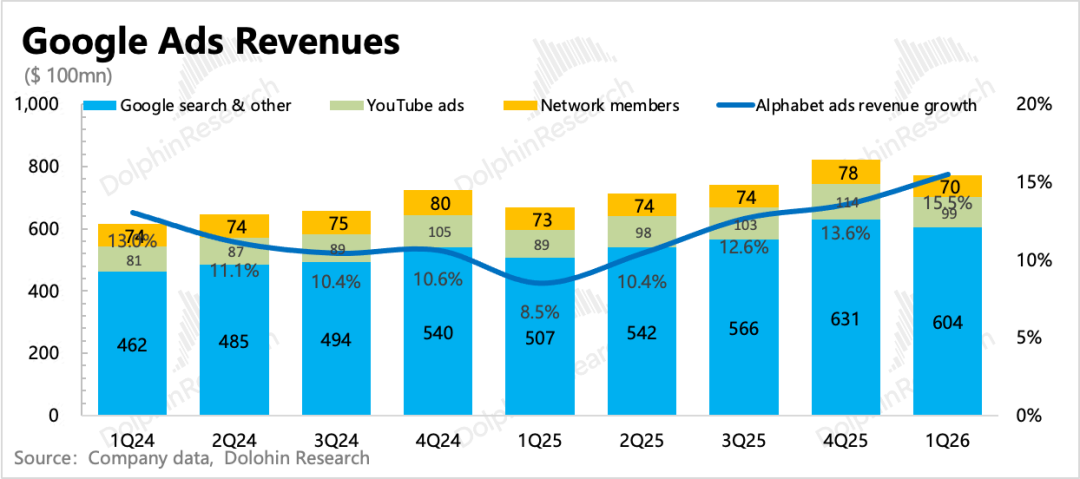

2. Advertising remains robust overall, with search outperforming YouTube

Q1 advertising revenue reached $77.3 billion, up 15.5% year-over-year. The industry performed well, driven by macroeconomic resilience and increased brand advertising budgets and spending due to the Winter Olympics, particularly for travel-related ads. Leading companies, benefiting from AI technology enhancements, generally maintained strong growth.

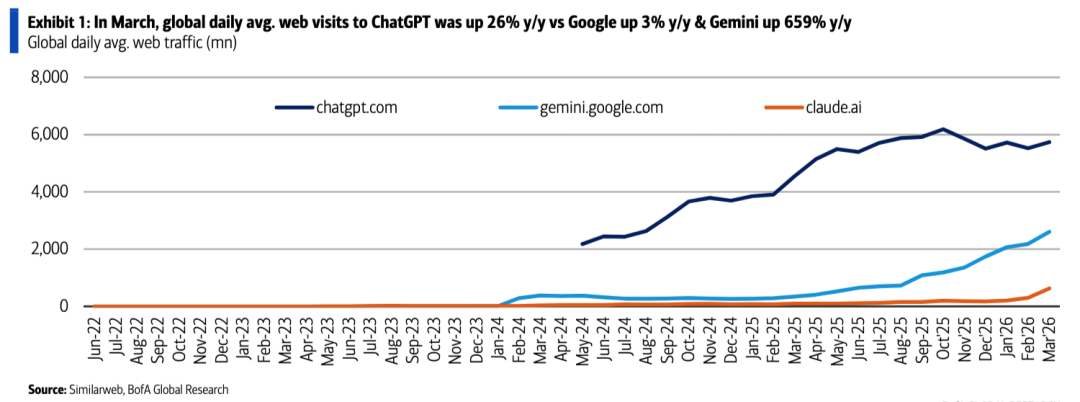

Google's core search business accelerated with 19% growth in Q1, indicating sustained positive penetration of Gemini 3. However, YouTube advertising showed no significant recovery. Dolphin Research believes that under the trend of short-form video consumption, while YouTube has Shorts, balancing it with long-form video within the ecosystem remains a challenge and an inevitable transition pain.

Meanwhile, Shorts, when viewed independently, also faces competitive gaps with Instagram Reels and TikTok, leading to short-term internal cannibalization by lower-CPM Shorts content.

Q2 may face short- to medium-term macroeconomic impacts from U.S.-Iran frictions, potentially affecting performance-based search advertising slightly less. However, the World Cup starting in June and midterm elections in Q3 are expected to offset some of these effects.

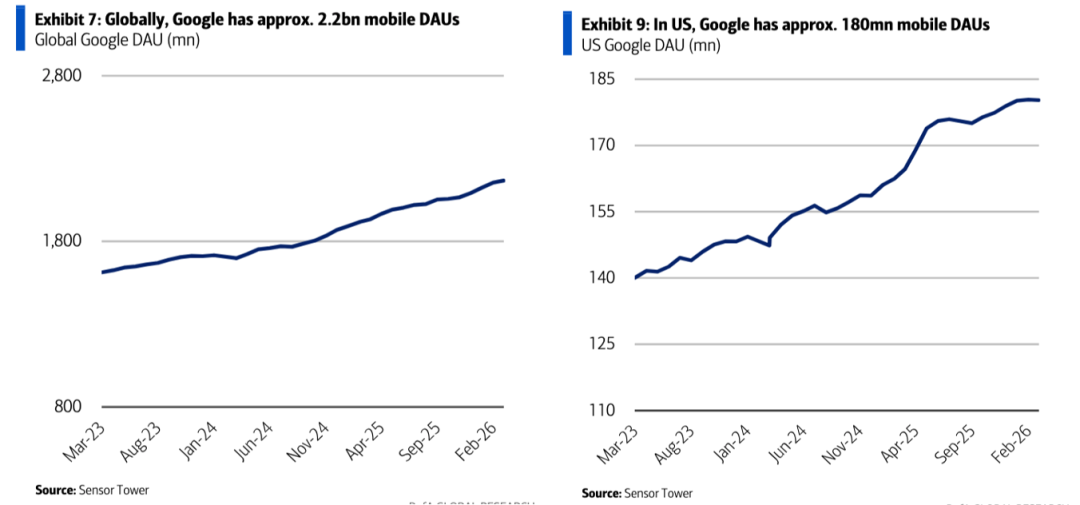

Currently, YouTube's user ecosystem, while not matching Instagram and Facebook at the top, remains solid: user numbers have grown slightly, and average daily usage has steadily increased.

3. Cloud: Doubling backlog + firm high investments confirm booming demand

The cloud business is a critical pillar in Google's AI revaluation, and from a forward-looking perspective, the market focuses more on backlog growth.

Q1 cloud performance once again exceeded expectations, with a key sentiment indicator—remaining backlog—reaching $462 billion, a net increase of $220 billion sequentially (implying new contract value of $240 billion). Over half of the backlog will be recognized as revenue within two years, providing ample "inventory" to sustain high cloud business growth for 1-2 years.

Enterprise demand for AI is rising sharply. For example, Google disclosed at its Next conference that its proprietary models now process 16 billion tokens per minute via direct APIs, up significantly from 10 billion at the end of Q4 last year.

Cloud business growth aligns with the current AI era, bolstered by Google's "full-stack technological advantages" in the enterprise segment (TPUs, Gemini foundation models, Gemini Enterprise agents, etc.). The recent release of the eighth-generation TPU, with performance doubling compared to the previous v7 (higher throughput, larger storage, better bandwidth), further enhances the cloud business's product strength in complete AI infrastructure platforms. Key features:

(1) Dedicated chips for different scenarios: The eighth-generation TPU introduces, for the first time, specialized chips tailored to training and inference scenarios (high computational throughput vs. low latency + high concurrency + agentic workload optimization). TPU 8t targets large-scale training, while TPU 8i focuses on inference.

Similar scenario-specific divisions existed as early as v5 (v5p for ultra-large-scale training, v5e for cost-effective medium-scale inference), but this iteration offers clearer scenario classification and distinct chip performance characteristics.

In terms of single-chip performance, TPU v8 supports FP4 computational precision for the first time, maintaining energy efficiency while improving throughput. Memory and bandwidth have also been significantly expanded to reduce latency.

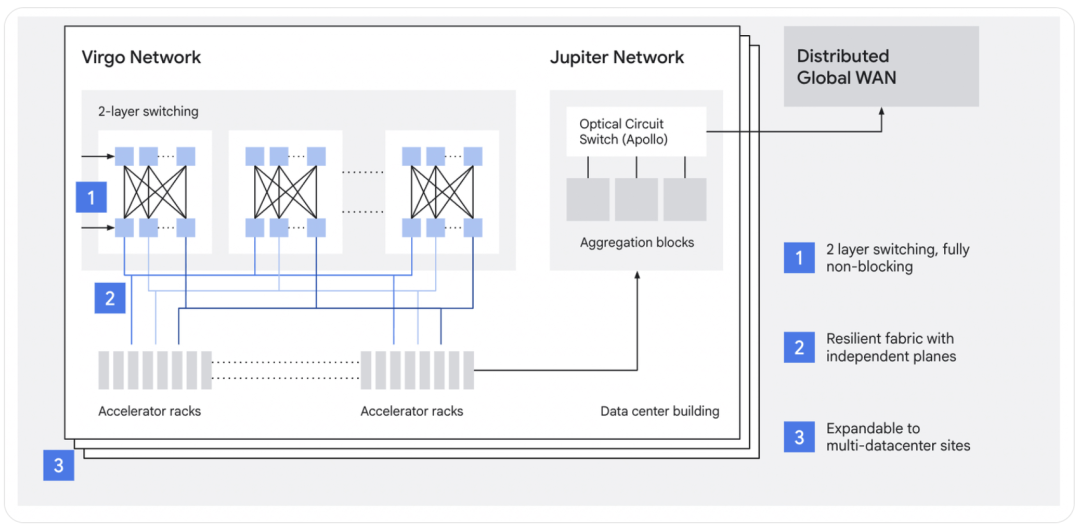

(2) Stronger interconnectivity: Compared to GPUs' standalone capabilities, TPUs excel in "teamwork," which tests system interconnectivity.

TPU v8 further pushes interconnectivity limits—increasing chip count per Pod (from 9,216 in v7 to 9,600 in 8t) while innovating beyond Pod-level interconnects. It connects upward to Virgo via rack-level ICI/SPOCS, then to Jupiter within the same data center, and further expands to distributed wide-area networks, enabling scaling to 134,000 or even millions of TPUs.

After refining the overall AI infrastructure solution (including capabilities in GPU, Jupiter/OCS networking, Hyperdisk/Cloud Storage, Cluster Director, DWS, Pathways, and other scheduling and software layers), TPU, as a competitor to GPU, will be officially available for large-scale sales in the future.

Currently, most of the direct sales revenue from TPU chips in the sales orders will be recognized in 2027, largely corresponding to the 1P data centers that Anthropic and Meta plan to establish in that year.

In April, Google announced a $40 billion strategic investment in Anthropic, with an initial investment of $10 billion and a commitment to provide 5GW of computing power over five years. Additionally, mid-sized contracts worth $100 million to $1 billion have also made significant contributions.

Besides basic computing power, most of the orders in hand are cloud contracts, with demands including Gemini's API, Workspace, Vertex AI, and cybersecurity services.

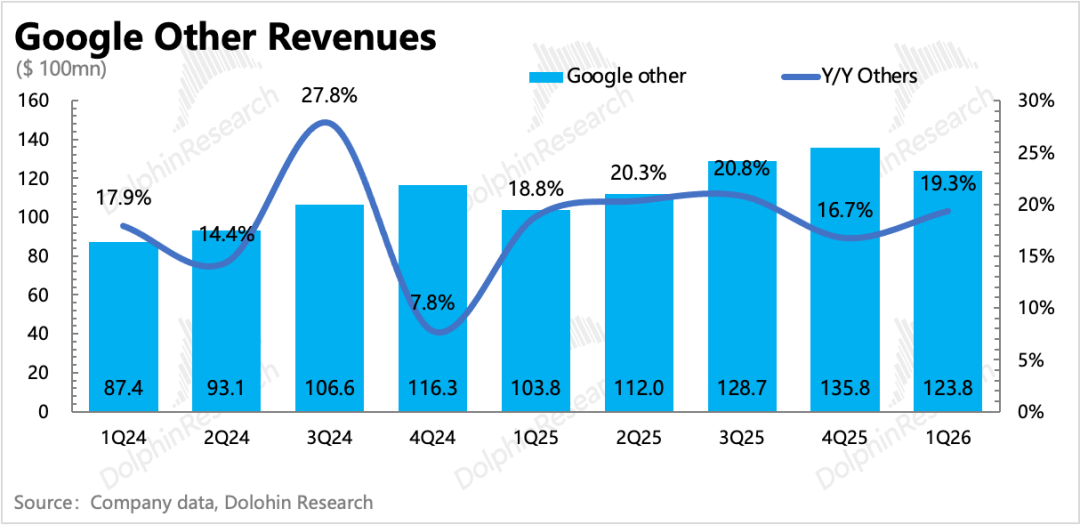

IV. Other Businesses: CTV & Google One Continue to Drive 25 Million New Subscribers

This revenue primarily comes from YouTube subscriptions (ad-free membership, TV, music, etc.), Google Play, Google One, hardware (Pixel phones and Nest smart home devices), etc.

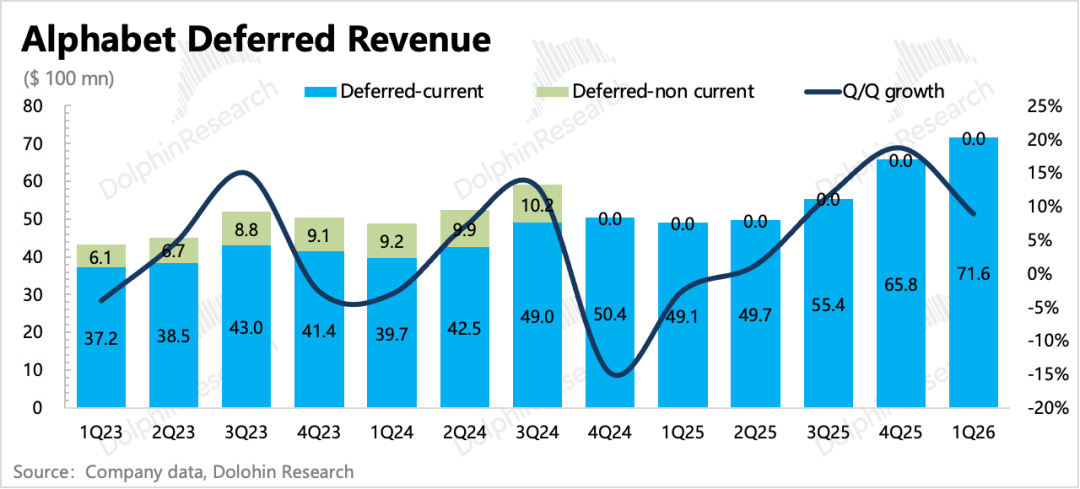

In the first quarter, other revenues reached $12.4 billion, up 19% year-on-year, showing accelerated growth. This indicates a recovery from the disruption caused by the Pixel sales cycle last quarter. Management disclosed that YouTube and Google One drove the growth of subscription members to 350 million, a net increase of 25 million quarter-on-quarter.

According to Nielsen's data, the revenue growth from YouTube CTV and Google One subscriptions has been the main driving force. The deferred revenue situation also reflects a significant increase in subscription-based advance revenue.

V. Profitability Enjoys a Dividend Window

In the first quarter, the operating profit of the core business reached $39.7 billion, with the profit margin rising to 36%. At first glance, how does Google manage to expand investments while simultaneously achieving profit growth?

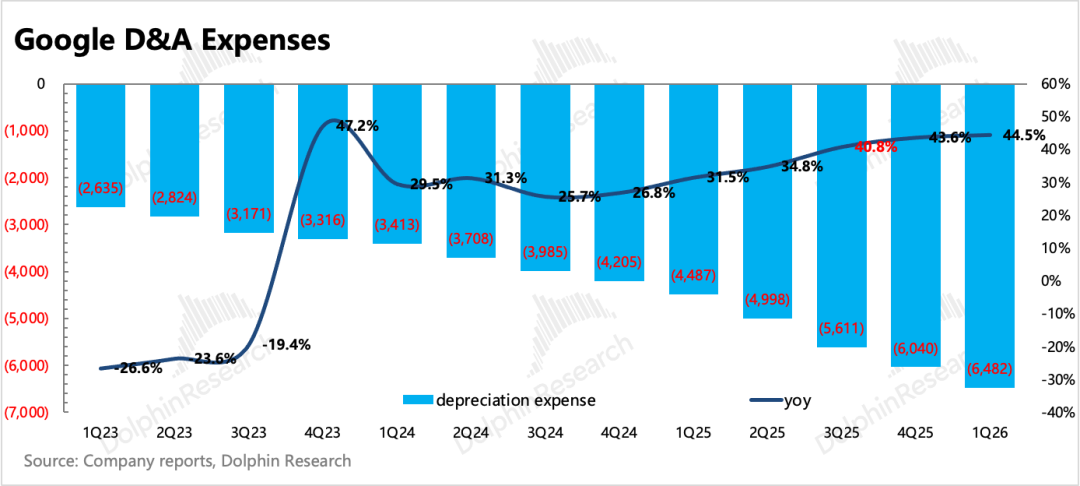

The better-than-expected profit margin primarily stems from the gross margin, and more specifically, the variance mainly lies in depreciation and amortization. There exists an alternative "mismatch" period: on one hand, the surge in revenue demand is rapid, especially after the popularity of Agents/Skills; on the other hand, the increase in depreciation costs due to high investments over the past two years is reflected gradually quarter by quarter.

During this window, the cloud business, by transitioning from pure computing power to comprehensive solution services to meet the demand for rapid user access, has seen increasing per-deal amounts and average revenue per user, leading to a significant optimization of the economic model.

Conversely, it is expected that starting in the second half of the year, the suppressive impact of high investments on profit improvement will become evident, and the company has also expressed expectations for a significant increase in Capex in 2027. Unless the current prosperity and supply-demand gap continue to widen, providing cloud providers with more room for price hikes.

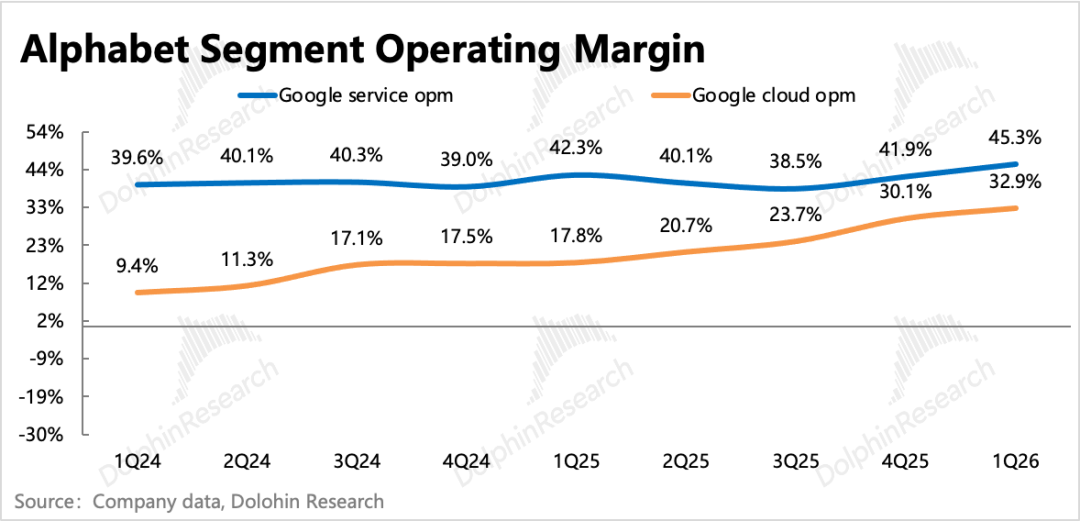

In terms of business segments, not only did Google's services business see a quarter-on-quarter increase, but the cloud business's profit margin also further improved to 33%, while the market originally expected the profit margin to decline quarter-on-quarter under investment pressure.

In the first quarter, capital expenditures reached $35.7 billion, slightly lower than market expectations. However, the company projects capital expenditures for the year to be in the range of $180-190 billion, representing a doubling of growth. Management's firm commitment to investment over the past two to three years indicates that the current growth trend in AI demand shows no signs of cooling down.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting is only allowed with authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute advice, inquiries, or recommendations regarding relevant securities or related financial instruments. The information, tools, and data contained in this report are not intended for or intended to be distributed to jurisdictions where the distribution, publication, provision, or use of such information, tools, and data contradicts applicable laws or regulations, or to citizens or residents of jurisdictions where Dolphin Research and/or its subsidiaries or affiliated companies are required to comply with any registration or licensing requirements in that jurisdiction.

This report only reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Computing Power Supplier Bags Orders Worth Over 600 Million Yuan, Yet Receives Only 4.5 Million Yuan in Actual Payments!

-

Alibaba Is Just Five Months Away from Securing Two Consecutive AI Coding Titles

-

![]()

Less Investment Isn't Apple's Get-Out-of-Jail-Free Card

-

![]()

The 'King of Africa' Tecno Mobile: What Is the Market Hesitating About After Its 'V-shaped' Rebound?

-

![]()

ByteDance Restructures Feishu, What Signals Does It Send?

-

![]()

ByteDance Overhauls Feishu: What Strategic Signals Are Being Sent?

-

![]()

Pay $39 a Month with Apple Upgrade: Apple's New Business, Your Old Wallet

-

![]()

The Open-Source Debate Dividing Silicon Valley