AI Cloud Midfield Battle: Alibaba Bets on Scale, Volcano Showcases Traffic, Baidu Deepens Moat

06/02 2026

06/02 2026

573

573

Since 2026, the narrative of the cloud market has been undergoing a restructuring. The old ranking system, which prioritized "size" and inertia (inertia) in thinking, may still influence customer decisions—where bigger scale and broader coverage indicate leadership.

However, with the arrival of the age of intelligent agents, everyone understands that this logic is increasingly unable to explain current events.

Over the past decade, the logic for evaluating cloud providers has been simple: public cloud market share, revenue scale, and customer count. Whoever had the larger scale would win the market's mindshare—this was almost an iron law.

But as the age of intelligent agents arrives and AI truly enters real-world scenarios to deliver results, the way cloud services are evaluated is changing. Banks no longer just want elastic computing power; they want thousands of AI applications to run stably, compliantly, and deliver results.

Automakers don't just want storage; they want autonomous driving to be ready for mass production. Manufacturing bosses want AI to monitor production lines, not just a stack of API documents. The focus of demand has shifted—large industries like energy no longer just need a "backend" but hope to leverage resource integration to bring AI to the "frontend."

Today, more and more customers' demand for AI cloud services has shifted from "renting resources" to "demanding results," from "what resources do I need" to "what problems do I want to solve." While this may seem like a mere difference in wording, it is rewriting the evaluation system of the entire cloud market.

Demand influences supply, which in turn affects market dynamics. Since 2026, as the most fundamental infrastructure for AI deployment, the capabilities, strategies, and corresponding market prospects of providers like Baidu Intelligent Cloud, Alibaba, Volcano, and Huawei Cloud have all been reshaped by this force.

The market is changing, and the cloud must inevitably change with it.

From Roughly Comparing "Size" to Refining "Precision"

The concept of "cloud" has been in China for nearly two decades, evolving from early cloud computing to today's AI domain. However, the value metrics chosen by providers and even customers have rarely changed.

Market share has always been a snapshot of "how much was sold in the past," suitable for markets with stable products and clear demand.

The cloud market of the past was exactly like this—competition was a typical land grab: whoever had the larger scale won.

This is somewhat similar to the early real estate and construction industries, where companies relied on land acquisition and project completion as support for their performance and strength.

However, in the middle and late stages of industrial development, as user requirements for buildings and projects become increasingly demanding, differentiated services, refined engineering capabilities, and cost control gradually become the core of competition among enterprises—especially under industry cycle fluctuations and technological iterations.

Today, in the AI era, a similar transformation is underway. The old logic of competing on market share has a glaring blind spot—it cannot measure how well customers are using the services.

In the age of intelligent agents, this blind spot is being amplified.

First, the deliverables have changed: customers want intelligent agents capable of running businesses. Deliverables have shifted from "components" to "finished products," from one-time purchases to business systems requiring continuous operation. Industry know-how has become the new moat.

Second, the evaluation timeline has changed: in the past, delivery meant settlement. Now, the launch of an intelligent agent is just the beginning; the real test is whether it can continuously deliver value.

The competitive logic of the cloud is shifting from "land grab" to "intensive cultivation." Market share is not wrong, but it can only tell you "how well you sold in the past," not "who will win in the future."

Under this new logic, the strategies of several leading domestic cloud providers are quietly changing.

Alibaba Cloud is betting on full-stack scale. It has integrated "chip-cloud-model" into a technology chain: self-developed Zhenwu AI chips, Qianwen large models, and extended enterprise-grade intelligent agents and flagship applications on top.

To meet demand, they have raised capital expenditures on AI infrastructure to well over 380 billion yuan. Large investments, broad scale, stable full stack, and comprehensive services—this is the AI cloud narrative they have crafted for themselves.

Huawei Cloud, on the other hand, is betting on self-developed depth and localization. Its Ascend chips, Pangu large models, MindSpore framework, and CloudMatrix supernodes form a full-stack self-developed soft-hard integration, combined with "cloud-network-security" integration capabilities.

In markets with strict localization and compliance requirements, such as government, state-owned enterprises, and operators, this forms an unshakable barrier.

In contrast, Volcano Engine, a later entrant, is betting on traffic and consumer-facing scenarios. ByteDance's numerous applications serve as a billion-user-scale high-pressure testing ground for AI cloud.

It packages this foundation into the "Doubao large model + Feishu ecosystem" for external output, continuously showcasing its strength in consumer-facing inference and content generation.

As a veteran technology giant and the earliest domestic player in AI, Baidu Intelligent Cloud has entered another phase.

On the full-stack front, they completed their layout (layout) early, achieving end-to-end integration of chips, cloud, models, and agents. Based on self-developed advantages, they have established a solid market barrier and shifted their service anchor early to the dimension of "intelligent deployment."

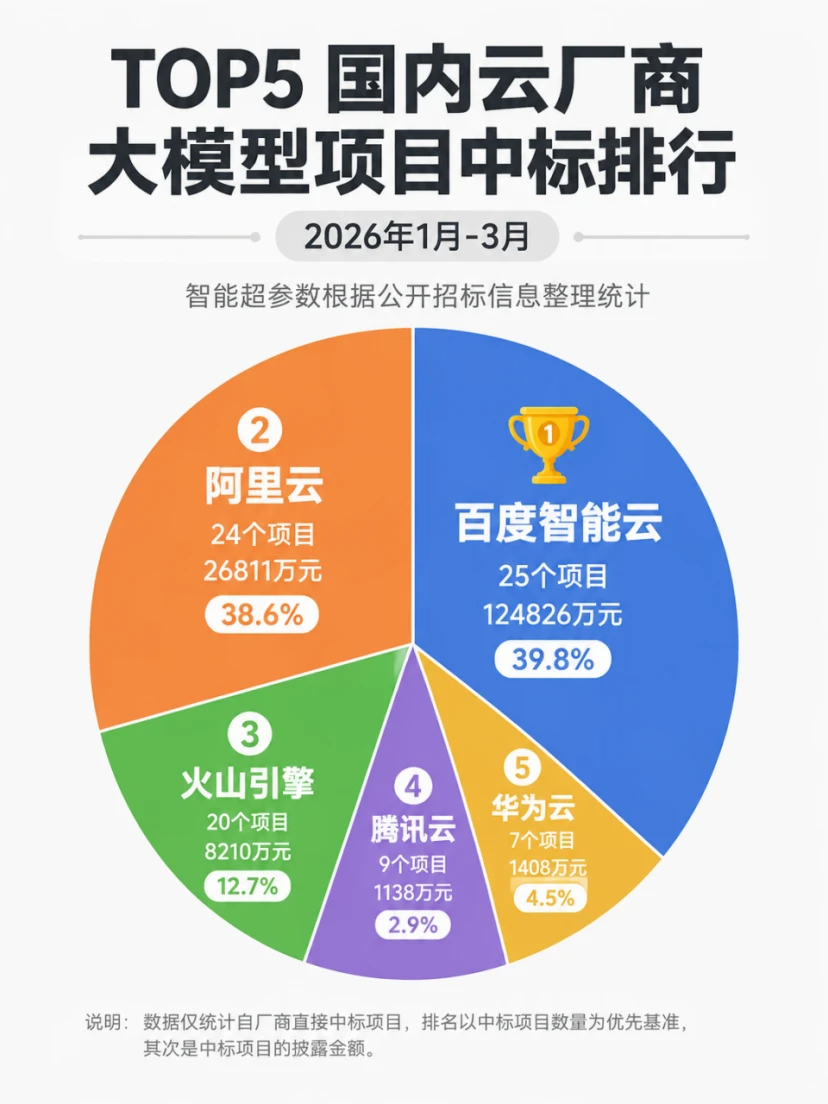

This strategy has allowed Baidu Intelligent Cloud to achieve a rare "balanced" track record in the public market—on one end, ultra-large intelligent computing infrastructure deals like Shandong Unicom's 1.129 billion yuan contract, positioning them as an "intelligent computing infrastructure operator" with full-stack capabilities.

On the other end, hundreds of micro-deals in AI capabilities across finance, industry, government, and intelligent driving, breaking down large models, maps, data annotation, and digital humans into independently purchasable modules.

This approach of "selling AI capabilities" rather than "selling cloud resources" has allowed them to maintain a dual first-place ranking in both deal value and project count in the large model market since 2025.

This comprehensiveness has become Baidu Intelligent Cloud's natural moat. Of course, its starting point is also unique: Baidu began betting on AI in 2010, then worked backward to develop cloud capabilities, proposing the "new full stack" logic of "chip-cloud-model-agent" four-layer synergy.

From this perspective, what Baidu Intelligent Cloud is betting on in the age of intelligent agents is actually AI-native practice and deployment.

This route aligns with Baidu's overall AI strategy. At the recent Baidu Create conference, Baidu founder Robin Li first proposed the DAA (Digital Agent Architecture) concept, arguing that in the age of intelligent agents, the metric to prioritize should not be consumption but how many agents are truly working and delivering results.

Correspondingly, Baidu Intelligent Cloud announced its upgrade to a new full-stack AI cloud for large-scale intelligent agent applications on the same day.

Many may only notice the "new" in this upgrade while overlooking the prefix—"for large-scale intelligent agent applications"—which may be Baidu's true answer. How to deploy intelligent agents across thousands of industries?

Their focus has shifted from the rough comparison of size in the past to how to "refine" and truly integrate AI into the capillaries of thousands of industries.

The "Old" and "New" of Full Stack: From On-Demand Services to Delivering Results

The shift from providing services to delivering results may not seem complex, but it represents a holistic restructuring of the cloud industry.

The term "full stack" has been discussed in cloud circles for years, but the AI era has given it new meaning. In the past, full stack referred to coverage—like building a computer: you bought a CPU, graphics card, and memory separately and assembled them to run. The new full stack is more like an iPhone—the chip, system, and applications are designed to exist for each other from the start, with Collaborative optimization (collaborative optimization) rather than assembly.

Take Baidu's self-developed Kunlun chip as an example: recently, they announced that the Kunlun Chip P800, paired with ERNIE 5.1 for training, achieved a 97% effective training rate in a 10,000-card cluster—a result of joint chip-model optimization rather than single-point improvement. When agent pressure rises, underlying computing power and model scheduling can automatically scale.

This kind of "grown-together" synergy is difficult to replicate through layered procurement or assembly integration. It requires considering model needs from the chip design stage and rebuilding data center networks around AI workloads.

In short, this upgrade aims to optimize intelligent agent capabilities.

This is the essence of the so-called "new full stack." It represents a shift from "hierarchical supply" to "systemic supply" in approach, not just stacking technologies but considering product deployment from the outset.

Of course, the cost is real: long cycles, heavy investments, and extremely high replication barriers for providers without an AI genetic starting point.

Capabilities are the foundation, but industry penetration depends on depth. In the past, cloud providers could thrive by simply selling computing and storage resources—resources are commodities, and the cheapest, most stable provider won the business.

But AI has rewritten this logic: when customers demand results rather than resources, whether a cloud provider has its own AI capabilities becomes the dividing line.

Only with AI capabilities can they "translate" AI into industry-usable solutions; without them, they can only sell standardized computing power and remain stuck at the shallowest layer of the industrial chain.

Using Baidu Intelligent Cloud as a case study, its public figures point not to "how much it sold" but to "how deeply it penetrated": in the automotive industry, Baidu covers the entire industry chain from chip manufacturing to OEMs and component suppliers, supporting over 20 million L2 autonomous driving vehicle deliveries last year. In finance, over 800 financial institutions use Baidu's solutions, with 100% coverage of systemically important banks. Around 80 central state-owned enterprise customers use its services, with State Grid deploying intelligent agents in over 40 scenarios across 800+ substations. It holds the largest market share in embodied AI cloud, exceeding the combined share of the second and third players (Omdia).

Supporting this penetration is the synergy of its "chip-cloud-model-agent" ecosystem. State Grid inspection uses "small model on-site preliminary judgment + large model cloud-based re-judgment," raising accuracy from ~50% to over 80% and reducing inspection time from 2.5 hours to 45 minutes. Over 800 AI applications launched by China Merchants Bank run half on domestic Kunlun chips—none of these are achieved through generic computing power.

Thus, large deals are results, not causes: AI capabilities must first take root, creating "vascular-level" business dependency, before the most demanding institutions like finance and energy are willing to entrust their core systems.

While others sell cloud to industries, Baidu lets AI grow into industries. Institutions like CCID, Frost & Sullivan, Forrester, and Omdia also rank it first across dimensions like AI cloud full-stack services, self-developed GPU cloud, product capabilities, and industry penetration in automotive, energy, and embodied AI.

When evaluation criteria shift from "general market share" to "AI deployment depth," the rankings have already deviated from pure market share comparisons—after all, customer choices speak loudest. These choices require looking not just at breadth but also at depth. From this perspective, Baidu Intelligent Cloud is not only deepening its moat but has quietly entered a harvest period.

According to Baidu's latest earnings report, AI cloud revenue grew 79% YoY, and GPU cloud revenue surged 184% YoY. Thanks to this rapid growth, AI business revenue now accounts for 52% of Baidu's general business revenue, surpassing 50% for the first time.

Deep Industry Penetration: The New Proposition for Cloud in the AI Era

In today's AI-centric discourse, a prerequisite is often overlooked: AI must land on infrastructure to deliver value.

Model release competitions are just the starting point—for an intelligent agent to truly operate in financial risk control, energy scheduling, or autonomous driving, it requires holistic support from chips, networks, data centers, inference, and compliance. The maturity of this infrastructure determines how deeply AI can penetrate industries.

In May of this year, the Cyberspace Administration, National Development and Reform Commission, and Ministry of Industry and Information Technology jointly issued the "Implementation Opinions on Standardized Application and Innovative Development of Intelligent Agents." AI is being treated as industrial infrastructure rather than an optional technological upgrade—and cloud is the core carrier of this infrastructure.

Market demand and industry regulations are ushering in a new blue ocean market for AI cloud, where the essence lies in who can reconstruct all industries with AI.

Against this backdrop, Alibaba, Volcano, Huawei, and Baidu each have their solutions. For the industry, old metrics are failing, and excessive displays of strength are actually signs of development anxiety.

In the future, who better meets the real needs of AI deployment will not be found in today's rankings but in whether customers still use these solutions three years from now. The old cloud wars were about occupying more land; the new cloud wars are about taking deeper root.

The battle for AI cloud has only just begun.

【Original by Tech Cloud Report】Please indicate "Tech Cloud Report" and include this article's link when reprinting.

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action