Alibaba Goes Big, Baidu Goes Deep: The 2026 Cloud Battle Between Two Full-Stack Giants

06/12 2026

06/12 2026

642

642

Author|Chang Yuan

Editor|Focus Editor

In The Nature of Technology, technical thinker Brian Arthur makes a penetrating argument: the true power of a technology lies not in the moment it is invented, but when it begins to 'combinatorially evolve' and integrate into the existing economic structure.

Standing in mid-2026, AI large models are experiencing this very moment. When 'ERNIE Bot' and 'Tongyi Qianwen' are no longer confined to chat boxes but start operating your mouse and keyboard, taking over your workflow, and penetrating into bank risk control systems and power grid inspection routes, a battle over who can truly build an Agentic cloud has quietly begun.

After years of competition in the cloud computing market, no year has excited all players as much as 2026.

According to the latest IDC report, the market size of China's AI cloud full-stack services reached RMB 28.09 billion in the first half of 2025, up 195.7% year-on-year. The demand generated by enterprises 'using AI' is real, but on the other hand, AI demand is reshaping the logic of industry cloud selection. The bidding market represents new trends in customer demand. In the first quarter of 2026, large model bid-winning projects were highly concentrated in finance, government, energy, and transportation. Enterprises' core demands are no longer about renting hundreds of GPU cards for training but about AI truly solving business pain points. Banks want thousands of AI applications to run stably, automakers want assisted driving to be ready for mass production, and energy companies want AI to enter front-end operations.

Meanwhile, policies are also fueling the trend. In May of this year, the Cyberspace Administration, National Development and Reform Commission, and Ministry of Industry and Information Technology jointly released the Implementation Opinions on the Standardized Application and Innovative Development of Intelligent Agents. AI is officially treated as industrial infrastructure, and the cloud is the core carrier of this vast 'intelligent transformation across all industries' opportunity.

When customers demand not just resource rental but tangible results, the competitive dimension of cloud vendors has changed. The past cloud competition was about who occupied more land; the new cloud war is about who takes deeper root. Bid amounts and customer numbers are just the surface; the real deciding factor is penetration depth.

Therefore, the current competition among major cloud players is transcending the literal meaning of products and services. The real decisive battle in the 2026 AI cloud war is who can build an Agentic cloud that truly supports intelligent transformation across all industries.

What Are the Giants Competing for in Agentic Cloud?

Let's zoom in on specific players. Taking vendors that completed full-stack layout (layout) early as examples, Baidu and Alibaba have similarities but are also starkly different. Essentially, both are trying to transform AI from 'talkative' to 'capable.'

In the past few years, discussions centered around large models, with debates over parameters, leaderboards, and inference costs. But entering this year, 'Agent' has become the absolute buzzword at every company's launch event. Alibaba talks about AI Native; Huawei proposes Pangu + Ascend + CloudMatrix; Baidu upgraded its 'Cloud-AI Integration' to 'Chip-Cloud-Model-Agent.'

As IDC points out in its latest Global Cloud Computing Architecture Forecast 2026, AI is reshaping cloud computing architecture and value proposition, with the cloud evolving from a 'compute pool' to a 'neural hub for AI operation and collaboration.' The competition for Agentic cloud among major players is no longer about 'speaking with scale' as in the traditional cloud market but is differentiated by AI capabilities and industry solutions.

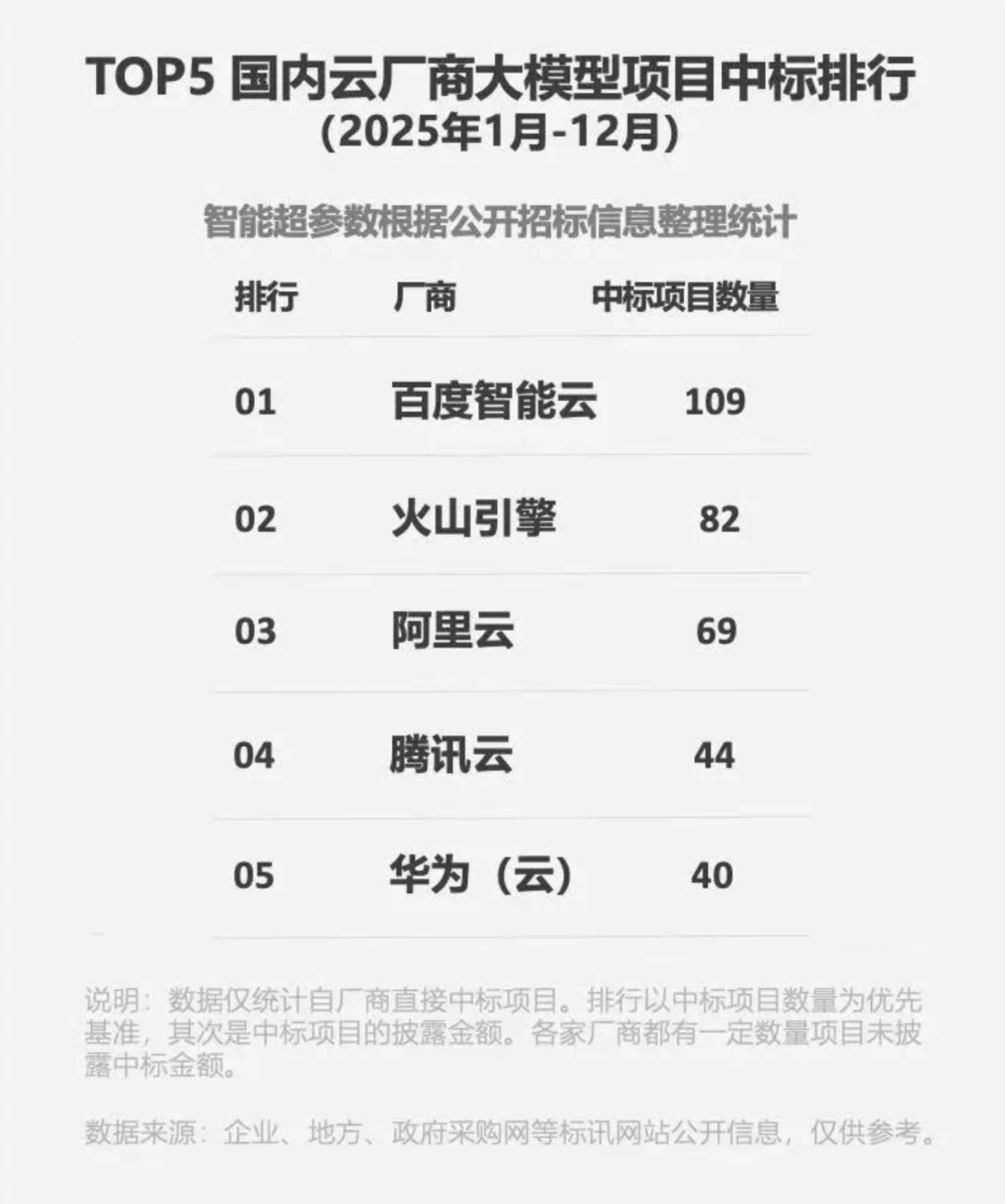

Alibaba is betting on scale. From its self-developed chip Hanguang and Tongyi Qianwen to the Bailian platform and the recently launched AI Native Agent platform, Alibaba is trying to replicate its success path from the mobile internet era, building an ecosystem of 'chip-cloud-model-application.' According to Omdia, Alibaba Cloud has maintained over one-third market share in China's cloud market and 38.1% in the AI cloud market. The underlying logic of this approach is scale advantage. Like Taobao and Alipay in the past, it establishes a larger territory through ecosystem and investment, thereby driving more customer recognition.

In comparison, Baidu Intelligent Cloud has a similar approach in full-stack self-development and ecosystem scale but differs in application deployment and industry penetration—the definition of its 'territory.' Baidu takes another path.

As the earliest player in China to work backward from AI to cloud capabilities, Baidu began deploying deep learning in 2010, opened its cloud business in 2015, first proposed 'Cloud-AI Integration' in 2020, and further upgraded to the new full-stack 'Chip-Cloud-Model-Agent' by 2026. Over more than a decade, Baidu's cloud business layout (layout) has not followed the traditional cloud vendor path of building resources first, then intelligence, and scaling through resources. Instead, based on the judgment of 'building a cloud adaptation (adapted) to the Agent era,' it makes endpoints themselves carriers of Agents.

This trend is evident from Baidu Intelligent Cloud's endpoint customer list, which includes global Top 10 smartphone manufacturers, China's Top 5 AI glasses companies, Top 5 AI toy manufacturers, Top 5 robotic vacuum brands, and even over 5 million smart home appliances. Behind these endpoints lies a vast imagination. IDC predicts that by 2028, over 1 billion Agents will run across different devices and business systems globally.

Agents will become new digital labor, and endpoints will be the largest carriers of intelligent agents. In other words, every hardware device in the future may have its own 'brain.' Future Agents are unlikely to be just an App but assistants in smartphones, guides in glasses, companions in toys, household managers in robotic vacuums, and even in every refrigerator, air conditioner, and washing machine. Baidu is aiming not just for a single super Agent but to connect the most scenarios.

This leads to a concept recently much discussed in the industry—FDE, Field Deployment Engineer.

This field, fiercely competed for by Anthropic and OpenAI in early May, has become key to the last-mile deployment of AI. Baidu Intelligent Cloud, with over a decade of industry deployment experience from search and autonomous driving to energy and finance, has accumulated possibly the largest FDE group in China. These people don't write papers or chase leaderboards; they work daily at customer sites, tuning models, aligning data, and fixing errors. When the industry began to realize the scarcity of FDEs, Baidu had already overcome the toughest phase.

An interesting divergence has emerged. In summary, Alibaba is building a bigger cloud, while Baidu is building a deeper cloud. The former competes on scale and ecosystem; the latter competes on industries and endpoints. In a sense, this is the biggest difference between Baidu Intelligent Cloud and other cloud vendors.

Three Criteria for Building an Agentic Cloud

At any intelligent cloud conference this year, the questions from industrial CIOs and CTOs are all based on specific workflow details, down to 'Can the approval process be completed within three months?' or 'How to ensure no downtime or errors when integrating into core business systems within six months?' This on-site sense is unseen in the past 'resource-selling' cloud market. Take banks as an example: introducing an intelligent approval system requires handling millions of concurrent requests, private deployment within the bank, seamless integration with core host systems, and meeting security and compliance requirements—a complete system integration project, not just compute stack.

These demands divide cloud service providers into two camps: those still competing on resource scale and those capable of integrating AI capabilities into business processes. To build a true Agentic cloud, cloud giants must meet three hard criteria: chips, platforms, and industry penetration.

The first criterion: Are the chips self-developed and proven in real business?

In the Agent era, compute power is not just about size but stability, adaptability, and long-term operation. The core logic is that if chips are unstable, Agents cannot run continuously, and enterprise operations will stall. Thus, the first threshold for an Agentic cloud is ensuring Agents can run stably in real environments over the long term. According to IDC's China AI Chip Market Report 2025, no more than three domestic vendors have an overall delivery stability rate exceeding 90% for enterprise-grade AI chips, and Baidu's Kunlunxin is one of them.

Today, the Kunlunxin P800 has completed large-scale validation of a 10,000-card cluster. In 2026, the Tianchi 256-card super-node completed ERNIE 5.1 large model training, improving throughput by 25% and inference efficiency by 50%, while supporting on-demand construction of extra large (ultra-large) clusters with hundreds of thousands or even millions of cards. In real business scenarios, Kunlunxin has run through core banking processes and financial risk control. For example, China Merchants Bank deployed a P800-based AI chip cluster, with over 800 AI applications running in production, of which over 50% run on domestic compute power.

The second criterion: Can the Agent platform withstand large-scale deployment?

After all, the real test for Agents is not running demos but operating long-term in error-intolerant scenarios like power grid inspections and bank risk control, handling millions of requests. If chips are the first hurdle for Agentic cloud deployment, Harness capability is the second. Simply put, when you have a smart brain (large model), how do you give it capable limbs and ensure it behaves? This system of 'adding limbs and setting rules' is Harness.

Especially in real industrial scenarios, an Agent faces problems a hundred times more complex than in labs to complete a task. Harness ensures the large model works efficiently and compliantly. Take power grid inspections: when an inspection Agent receives the task 'Check equipment defects in this substation,' its workflow is not simple. It must remember inspection standards (long-context management), then call the infrared camera's API (tool invocation). If one identification is uncertain, it takes another shot from a different angle (multi-step reasoning). Finally, it compares the results with defect records from the past three months (persistent memory) to determine if the defect is new or known. One mistake in any step—calling the wrong camera, forgetting historical records, or getting stuck in reasoning—will cause a missed inspection.

This is what Harness solves. In its actual deployments, Baidu Intelligent Cloud breaks down this capability into several modules: long-context management, persistent memory, tool invocation, sub-agent scheduling, evaluation feedback, and Runtime environment. Through Harness Engineering at each stage, the Agent remembers tasks, operates tools, thinks step-by-step, and corrects mistakes. This has reduced inspection time from 2.5 hours to 45 minutes, deployed in over 40 substation scenarios, covering more than 800 substations nationwide.

The third criterion: Has industry penetration formed a moat?

This is the most critical of the three criteria. Chip R&D progress is always a race, but penetration into core industry scenarios, once established, is hard to replace. For example, Shanghai Pudong Development Bank recently fine-tuned a financial analysis model with Baidu Intelligent Cloud in the core business process of corporate loan due diligence, compressing financial analysis from hours or even days to minutes, turning expert experience into engineerable and scalable capabilities. Not long ago, SPDB signed a strategic cooperation agreement with Baidu Group, deepening their partnership first established in 2020.

These customers are not piloting a single AI application but running AI in their main business processes or even specific scenarios. By analogy, for industry intelligence, future 'scale' should not just mean entering many industries but making an impact in specific scenarios and delivering results.

If market share is the facade, penetration depth is the foundation. Once formed, the latter becomes a moat. Baidu Intelligent Cloud's penetration data in several industries is also noteworthy. In the automotive industry, it covers 100% of China's mainstream automakers, supporting over 20 million L2 assisted driving vehicle deliveries in 2025. In embodied AI, according to IDC, Baidu Intelligent Cloud ranks first with 36.7% market share, exceeding the sum of the second and third players, with clients including leading firms like Beijing Humanoid and Unitree. Additionally, it partners with over 800 financial institutions, covering 100% of systemically important banks, and about 80 central SOE clients in the energy sector. The significance of these numbers is not just breadth but depth.

Take finance as an example. According to IDC's latest report, even in the decision tools and services market for retail credit intelligent risk control, Baidu Intelligent Cloud maintains a leading market share, with its revenue and user base both doubling in the past year.

The 2026 Decisive Point: From 'Bigger' to 'Deeper'

Over the past two years, large model vendors have been fiercely competing around Agents. The early popularity of OpenClaw confirmed that today, almost any company with basic model capabilities can build an Agent demo capable of calling tools, operating browsers, and completing complex tasks within weeks. However, the real challenge is getting these Agents into the real world and running stably over the long term.

After all, for banks, power grids, and automotive factories operating at high speeds daily, the usability and reliability of Agents face stricter scrutiny in actual workflows. In banking, one misjudgment could mean a loan approval error; in automotive factories, one failure could halt production lines; and in power grids, one malfunction could affect millions of people's power supply.

On the surface, everyone is building Agents, but if you zoom out, what several major players are competing for is the discourse power (discourse power) over the next generation of cloud infrastructure.

Looking at the past two decades of cloud computing development, the factors determining success have been different at each infrastructure upgrade. The difference is that a decade ago, software entered enterprises; today, it's Agents.

In the PC era, competition centered on hardware performance; in the mobile internet era, it focused on traffic access points. Over the past decade, the key phrase in China's cloud market has been 'bigger is better'—whoever had more servers and more customers held greater influence. Today, the question is: what kind of cloud can support these Agents? Perhaps we can predict that in the 2026 showdown of China's AI cloud market, success will not hinge on catchy slogans, massive traffic, or high rankings on model leaderboards. Instead, it will depend on who can truly integrate intelligence into the intricate fabric of every industry.

The biggest difference between Agents and mobile internet applications lies in their inherent reliance on industries. Agents must operate within real-world scenarios—whether it's bank risk control systems, power grid inspection processes, automotive R&D frameworks, or robot training platforms. Only by deeply embedding into these contexts can Agent intelligence be amplified to generate greater value.

Once Agents enter industries, the competitive logic shifts. For cloud providers, market share is no longer the sole metric; penetration depth becomes the new defensive moat. This explains why, since this year, companies like Alibaba, Huawei, and Baidu have increasingly focused on scenarios rather than technical parameters. The industry now recognizes that the greatest challenge in the Agent era is not creating intelligence but integrating it seamlessly into industrial operations.

In some ways, this resembles the early days of the mobile internet boom fifteen years ago.

The dividends of the mobile internet surge went to those who integrated the internet into consumer, payment, retail, and logistics systems. The same holds true today: opportunities will belong to those who can embed intelligence into industrial sectors.

In the past, cloud providers sold computing power. In the future, they will deliver productivity. The game has essentially restarted with new rules. This time, only players who take root in industries, prioritize implementation, and truly infuse the intelligence into industrial ecosystem will earn a seat at the center of the table.

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action