Oracle Plummets? The Irreparable Damage That AI Infrastructure Can't Fix—'High Interest, High Debt + Failing Software'

06/12 2026

06/12 2026

636

636

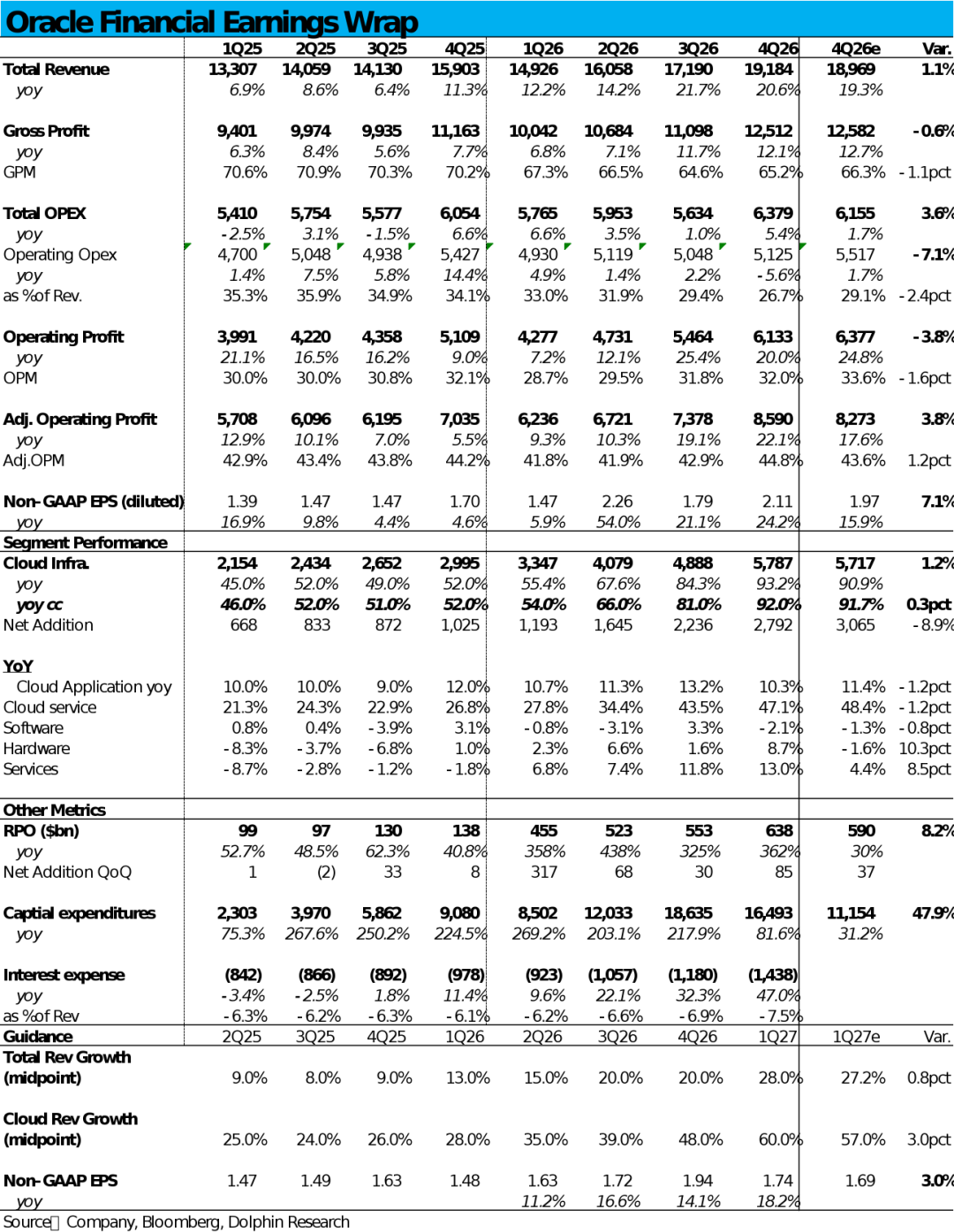

Oracle, the most closely watched and controversial player in the new cloud landscape, released its Q4 FY26 results for the period ending in late May after the U.S. stock market closed on June 11. Overall, the results were a mixed bag. For example, while the OCI business accelerated, growth in traditional pan- software (pan-software) business weakened. Additionally, gross margins improved sequentially from the bottom but still fell significantly short of expectations. Although the guidance for the next quarter was better than expected, the full-year guidance for FY27 was relatively conservative. As a result, the overall performance for the quarter was relatively plain (uneventful). Details are as follows:

1. Core Business—OCI Accelerates as Expected: Under the cloud segment, the IaaS-type OCI business generated nearly $5.8 billion in revenue this quarter, up about 93% year-over-year. After adjusting for favorable exchange rates, the actual growth rate was 92%, continuing to accelerate from 81% in the previous quarter, albeit at a slightly slower pace. Moreover, the actual growth rate was largely in line with expectations, offering no surprises.

In other words, while the absolute growth rate remains strong, from a relative perspective, the performance of the critical OCI business this quarter cannot be considered 'good.'

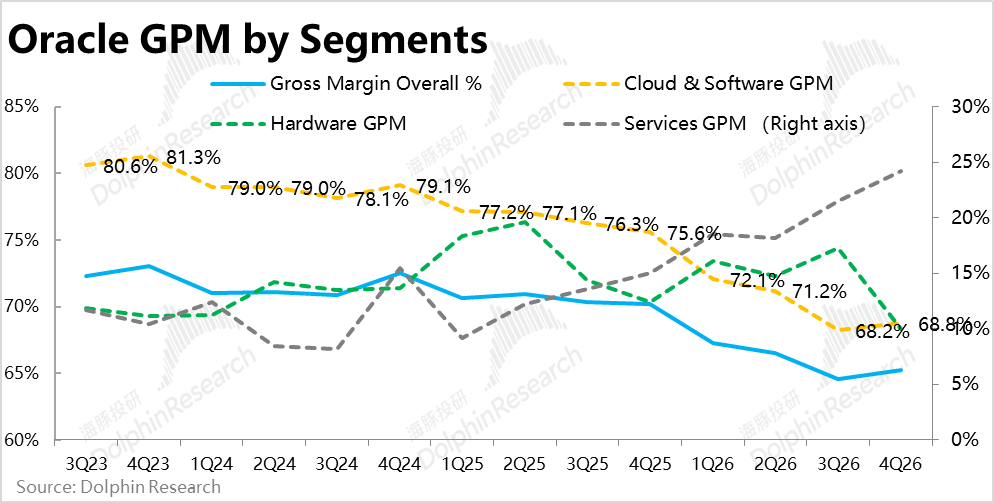

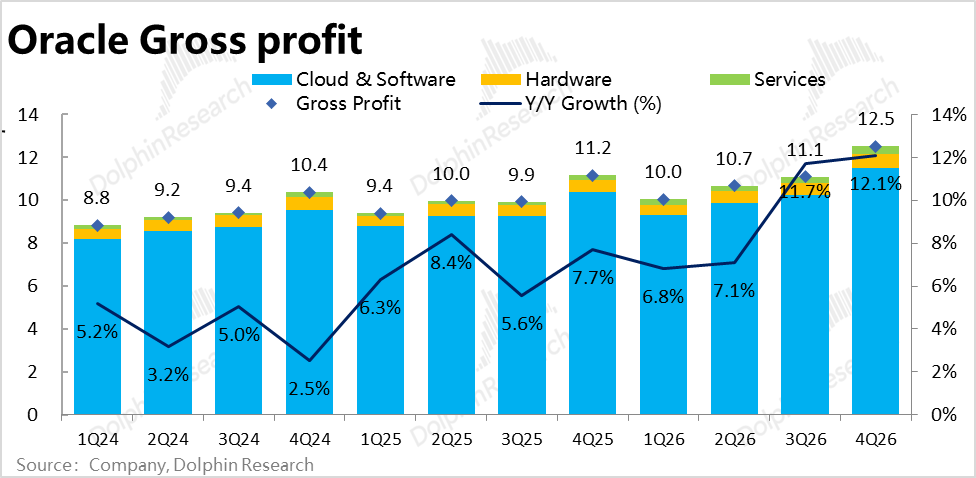

2. Gross Margin Bottoms Out Sequentially but Still Falls Short of Expectations: The combined gross margin for the cloud + software business was 68.8% this quarter, showing signs of bottoming out and rebounding from 68.2% in the previous quarter. Although the year-over-year decline was still 6.8 percentage points, it narrowed from the previous quarter.

However, since this figure encompasses multiple businesses, including OCI, SaaS, and traditional software, it is difficult to determine whether the improvement was due to OCI's gross margin stabilizing or an increase in the gross margin of the pan- software (pan-software) segment.

From an expectations perspective, the market anticipated an overall gross margin of over 66%, but the actual figure was 65.2%, still below expectations. Therefore, the overall gross profit performance this quarter remains slightly negative.

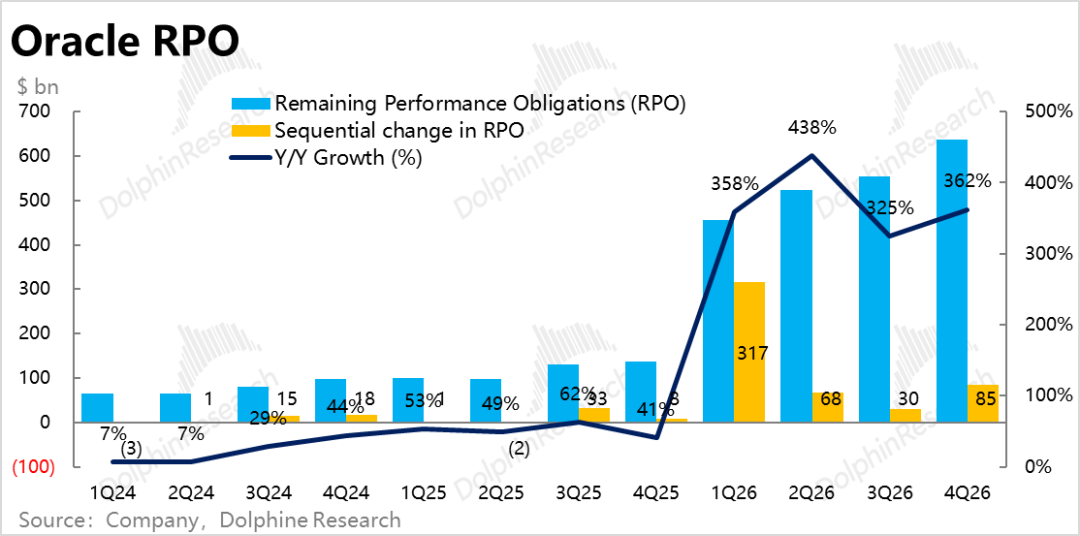

3. RPO New Orders Exceed Expectations, Capex Sharing Model Implemented: The remaining performance obligations (RPO), which reflect new order demand, reached $638 billion after an actual sequential increase of $85 billion. Since there were no rumors or reports of significant new contracts signed by the company before the results, market expectations were low, around $590 billion. Based on recent news reports, this increase may stem from newly announced government contracts.

Additionally, it is noteworthy that the company stated that approximately $75 billion in orders are now based on the Capex sharing model—where a portion of the Capex requirements for these orders is covered by customer prepayments or self-procured hardware. This is positive news for the company's cash flow and balance sheet structure.

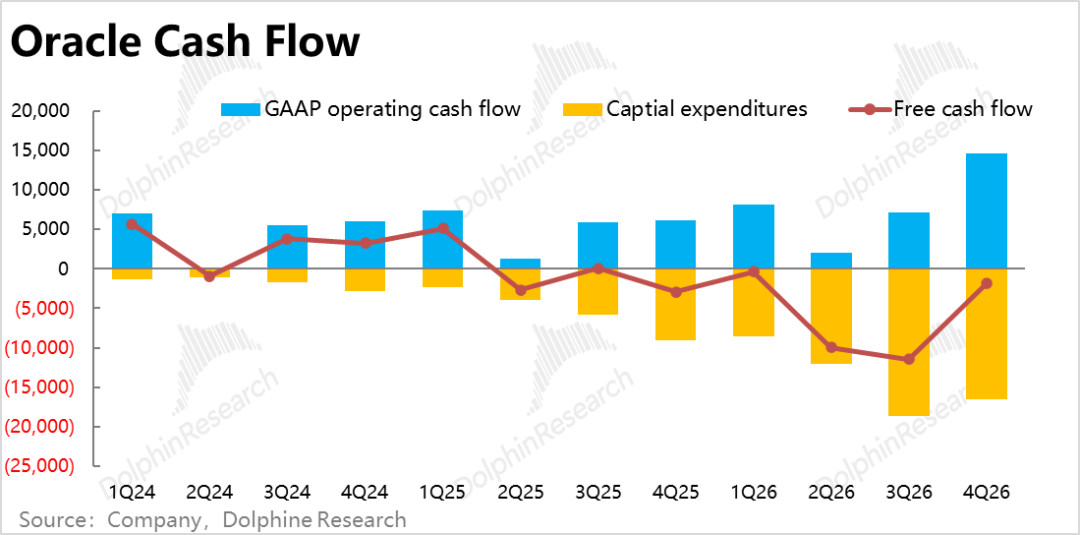

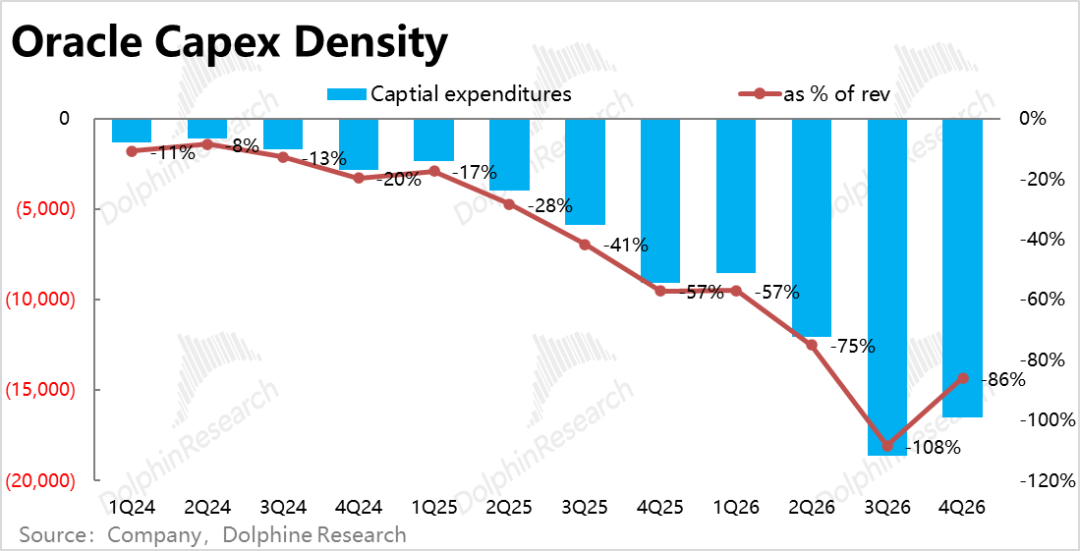

4. Capex Higher Than Expected but Cash Flow Improves Significantly: Correspondingly, Capex for the quarter was nearly $16.5 billion, down from $18.6 billion in the previous quarter. The market's expectation of $11 billion was mechanically derived from the full-year Capex guidance of $50 billion, making it seem significantly higher than expected, but its reference value is limited.

More notably, the sharing model covered approximately $4.6 billion in Capex expenditures this quarter. As a result, the company's free cash flow improved from an outflow of $10 billion per quarter previously to a net outflow of $1.9 billion this quarter, indicating a real reduction in cash flow pressure.

5. Reduced Financing Needs?: The company stated that it would conduct $20 billion in debt and equity financing (totaling $40 billion) in FY27 (previously disclosed), less than the approximately $48 billion in financing for the current fiscal year. This locks in funding sources for most Capex investments in the next fiscal year.

Furthermore, the market and Dolphin Research generally expected a free cash flow gap of over $50 billion in 2027. We believe this is likely because some funding needs are now shared with customers, reducing the company's own financing requirements.

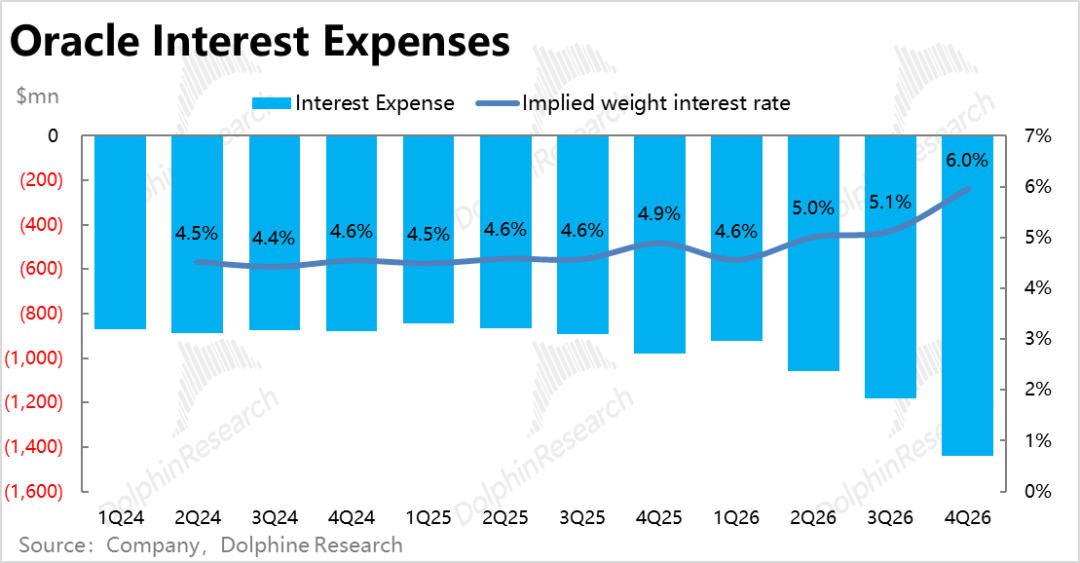

However, long-term fundamentals remain positive, while current pressures persist. Actual interest expenses reached $1.44 billion this quarter, up nearly 22% sequentially. Interest expenses as a percentage of total revenue also increased to 6%.

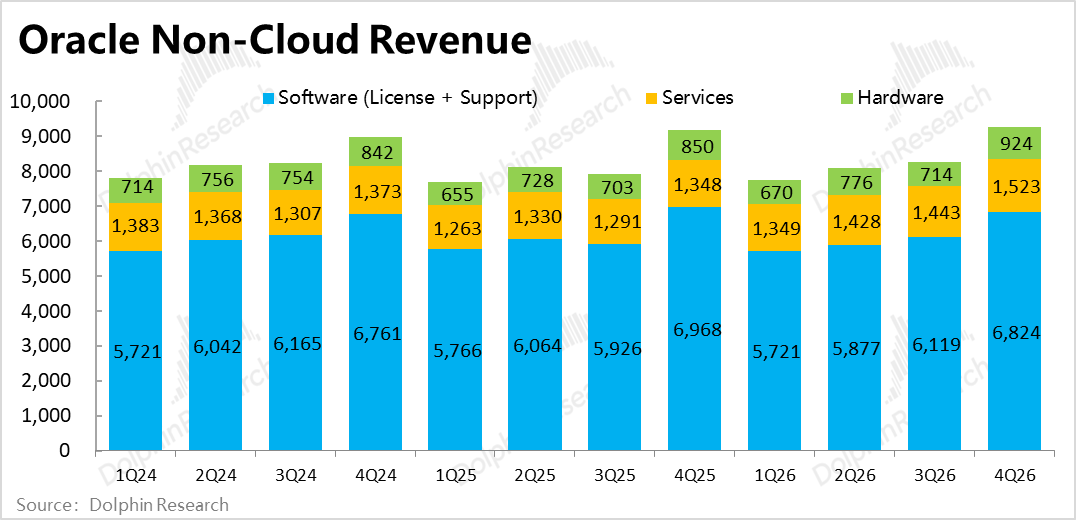

6. Other Businesses Further Weaken: The traditional business segment, still accounting for about 75% of total revenue, continued to deteriorate. Revenue from SaaS and software businesses grew by +10% and -2%, respectively, with growth rates slowing sequentially and falling short of market expectations. Although revenue from hardware and services grew significantly better than expected, these two businesses combined account for just over 10% of total revenue, limiting their impact.

7. Overall Performance

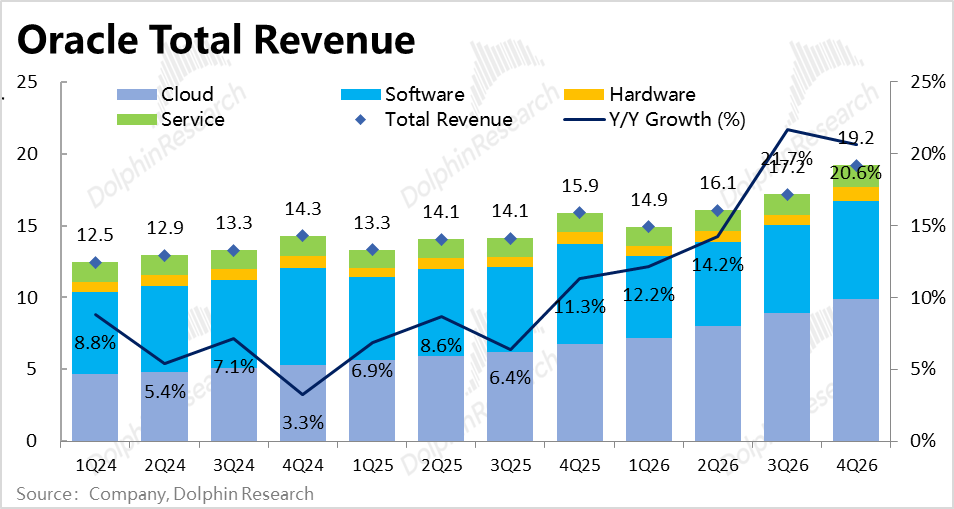

The company's total revenue grew by 20.6% this quarter, or 20% after adjusting for exchange rates, accelerating slightly by 2 percentage points sequentially.

Due to the significant year-over-year decline in gross margins mentioned earlier, the year-over-year growth rate in total gross profit was 12%, still significantly lower than revenue growth and slightly below market expectations.

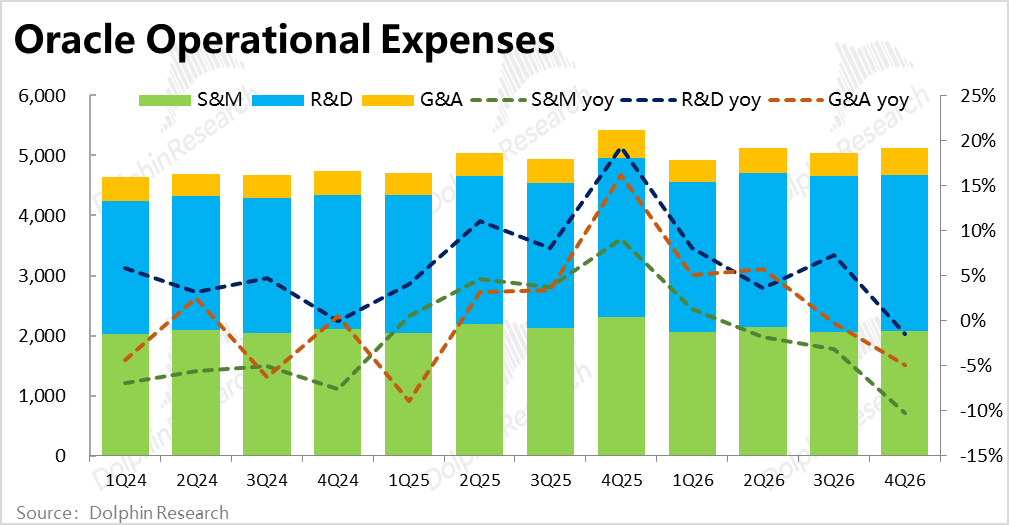

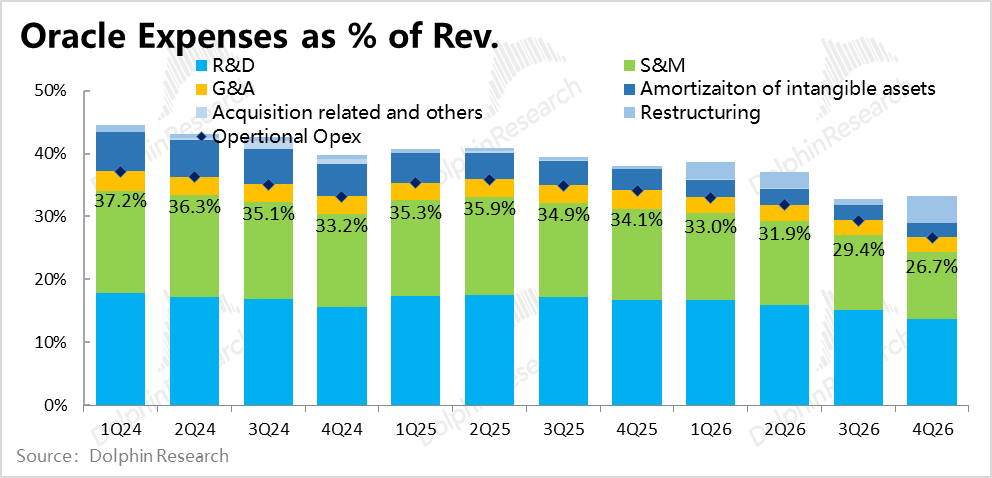

Fortunately, excluding one-time expenses from layoffs and focusing on the three regular operating expenses, actual expenses decreased by about 5.6% year-over-year, 7 percentage points lower than market expectations. Under strict cost control, despite the significant decline in gross margins, the adjusted operating margin stopped declining year-over-year and returned to positive growth of about 0.5 percentage points, better than market expectations.

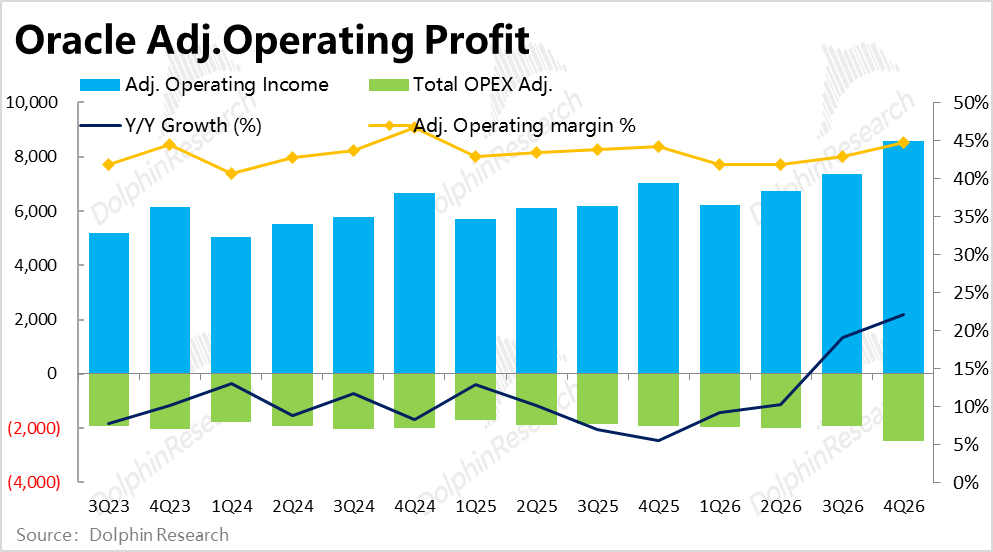

Ultimately, adjusted operating profit reached $8.6 billion, up about 22% year-over-year. Despite gross profit falling short of expectations and revenue, profit growth outpaced revenue and expectations.

Dolphin Research's Viewpoint:

1. Currently, the market's focus on Oracle's short- to medium-term performance primarily includes: a. The pace and acceleration of OCI revenue growth, which reflects the speed and rhythm of computing power construction. In comparison, there is less recent focus on newly signed orders (i.e., RPO). b. Whether the issue of declining profit margins as AI business revenue scales up has been resolved. c. The pace of Capex investment and ramp-up, as well as the ability to secure corresponding financing.

However, attitudes have shifted from previously negative (disliking high Capex due to ROI concerns) to more positive (high Capex indicates rapid progress in computing power construction).

Regarding these key points, the results of this earnings report are as follows:

a. The OCI business did accelerate as expected, but the pace of acceleration was entirely in line with expectations, making it unremarkable. At the same time, while OCI benefits from AI, the larger traditional pan- software (pan-software) business is logically an 'victim' of AI. Therefore, Oracle cannot be considered a pure 'AI beneficiary.'

b. Gross margins did show signs of bottoming out, but on the one hand, it is temporarily impossible to accurately attribute the cause, and on the other hand, they still fell short of market expectations. More quarters of observation are needed to determine whether the bottoming out of gross margins is temporary or a true inflection point.

Given that cloud business profit margins for Amazon and Google have not significantly declined in recent quarters, the widely accepted 'underlying assumption' that AI cloud business profit margins are significantly lower than traditional cloud business profit margins is now open to question. However, for NeoCloud players like Oracle, the trend of higher AI business composition leading to lower gross margins is more pronounced. This earnings report makes the issue even more worthy of discussion.

c. The most positive signal this quarter is actually the company's adoption of a Capex sharing model with customers. In the long term, this significantly reduces the pressure and risks the company would otherwise face in using its own cash flow and balance sheet to bear massive Capex investments and computing power construction for downstream AI customers.

Dolphin Research views this as a significant shift in logic. However, in the short to medium term, the company's net debt and interest expenses will likely continue to rise. It is important to monitor how much of the Capex can be shared with customers in the future.

2. From an investment perspective, as we noted in our last commentary, the successful completion of $50 billion in equity + debt financing alleviated concerns about the company's ability to secure funds for continued large-scale computing power construction. Additionally, with the explosive growth in Token/computing power consumption driven by Agents, market concerns about potential overbuilding of computing power or insufficient end-user demand have significantly diminished.

With improvements in these two areas, Oracle's investment logic has undergone a certain reversal. The company's stock price has rebounded more than 40% from its early April low, while recent macro risks and market volatility have resurfaced. Therefore, before the earnings report, investment banks generally believed that the market would have relatively high expectations for these results.

As a result, the truly mixed performance of this earnings report may disappoint funds with higher expectations.

In terms of guidance, the company expects cloud segment (including IaaS and SaaS combined) growth to have a median of 60% next quarter, continuing to accelerate sequentially and slightly exceeding market expectations of 57%. The median guidance for next quarter's Non-GAAP EPS is $1.74, implying year-over-year growth of 18%, also slightly exceeding market expectations by about 3%.

However, while the guidance for the next quarter is solid, the company maintained its full-year revenue guidance for FY27 at $90 billion and updated its full-year Non-GAAP EPS guidance to $8.05, merely in line with current market expectations. The full-year guidance is uninspiring, preventing the market from overly rewarding the solid next-quarter guidance.

In response, Dolphin Research speculates that the company may lack clarity on its full-year outlook and is therefore aligning its guidance with market expectations for now.

In recent developments, Oracle has remained relatively 'low-key' since its last earnings report, with no particularly significant new moves or announcements. However, two notable trends persist:

a. Introducing AI into software businesses: Recently, the company has not made many moves in its IaaS business but has consecutively introduced AI capabilities into its SaaS and database businesses, launching Fusion Agent Application and Agentic AI for Database.

Dolphin Research views this as a typical defensive move. After all, as of FY26, the OCI business, which directly benefits from AI, accounts for only about 25% of revenue. The remaining larger portion comes from software, SaaS, and databases—areas seen as potential 'victims' of AI. However, judging from the example of peer company Salesforce, introducing AI capabilities into traditional businesses has a limited positive impact. Whether it can help maintain current growth or even accelerate it again requires cautious observation.

b. Promoting government collaborations: In late March and early May, Oracle announced consecutive contracts with U.S. federal agencies and the Department of War, providing various services including OCI, AI Database, and Enterprise AI. Before the earnings report, the market generally believed that government collaborations would have limited actual impact on performance compared to enterprise orders worth hundreds of billions. However, it now appears that government orders may contribute tens of billions in actual value. Moreover, the significance of government orders may not lie in their direct performance contribution but in reflecting government support, which is also positive for market sentiment.

3. From a valuation perspective, two viewpoints can be considered: one is the short- to medium-term valuation that fluctuates with the company's quarterly performance; the other is the valuation based on the company's long-term prospects or steady-state conditions, which does not change significantly with short-term performance unless there are major logical shifts or adjustments to long-term guidance.

In the short to medium term, the market generally prices the company directly based on its Non-GAAP EPS for FY27. In other words, the company can already be supported by its near-term visible performance, offering room for returns through potential upward revisions in earnings/profits even without an increase in valuation multiples.

However, Dolphin Research still prefers to evaluate the company based on long-term steady-state conditions. After rebounding significantly from its lows, the current valuation relatively neutrally reflects the company's guided mid- to long-term performance space. Therefore, it is reasonable for the stock price to decline somewhat after these less-than-stellar results.

Of course, the implied valuation multiples are still not high. Additionally, the reduction in the company's own cash flow needs and financing/debt pressure conveyed this time may fundamentally improve its narrative logic. Barring systemic issues in AI, Dolphin Research believes that while Oracle may not be a high-conviction top pick, it is worth paying attention to at current levels.

Below is a detailed commentary.

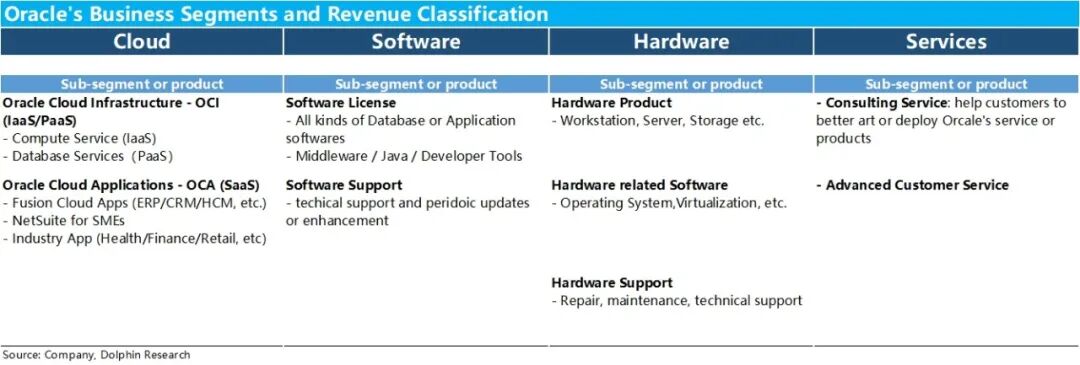

I. Oracle's Business & Revenue Segmentation

As a software industry 'veteran' established in the 1980s, Oracle's historical core business has primarily focused on databases and software services (traditional license model). However, in recent years, with the company's cloud transformation efforts and the AI boom, cloud services have surpassed other segments to become the most important and closely watched business.

In FY26, the company adjusted its financial reporting segments to more clearly categorize its business and revenue into four segments: Cloud, Software, Hardware, and Services. Further details are as follows:

a. Cloud Business: This can be subdivided into two business lines: IaaS-type OCI and SaaS-type OCA. OCA primarily includes SaaS-based ERP/CRM and other general management tools, as well as some vertical industry tools. OCI mainly comprises the company's signature database services and computing power leasing business.

Historically, OCA accounted for a higher proportion of the cloud segment, but OCI's share has gradually surpassed OCA over the past 1-2 years of rapid growth.

b. Software: This refers to traditional software businesses deployed and managed by customers themselves, which once accounted for the largest portion of the company's revenue but has now been surpassed by the cloud segment.

It can be divided into two main parts: one-time license sales revenue (Software License) and accompanying recurring service and support revenue (Software Support), such as providing usage support and regular updates/maintenance.

c. Hardware: Similar to the software business, this includes one-time sales revenue from servers and other hardware, as well as accompanying hardware maintenance and support revenue. It accounts for the smallest portion of total revenue.

d. Services: This includes other service businesses beyond the above software and hardware segments, such as consulting services or other customized services. In recent years, it has accounted for a high single-digit percentage of total revenue.

II. Core Focus: OCI Performance

1. Key Business—OCI Continues to Accelerate as Expected

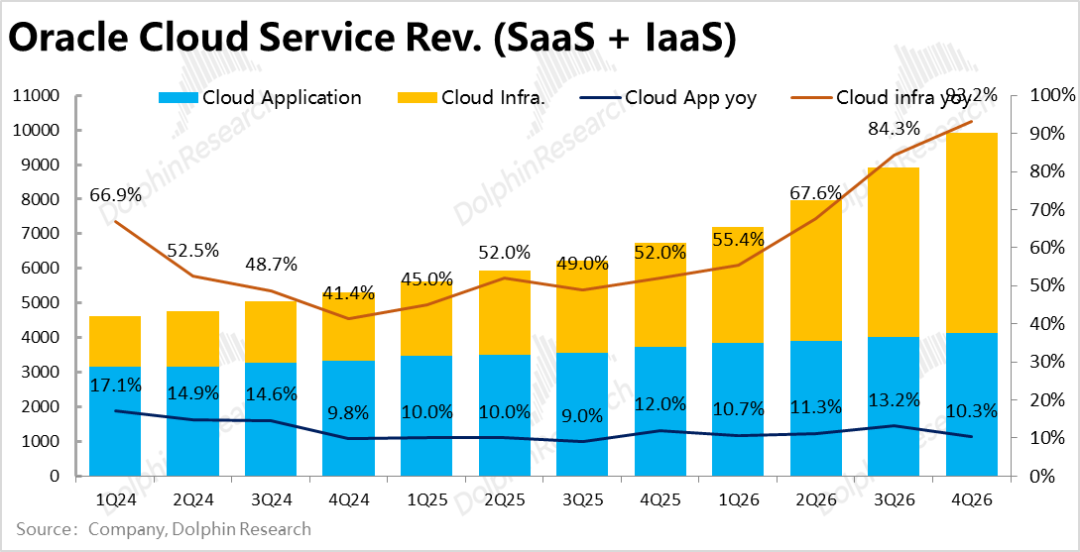

The most critical IaaS/PaaS-type OCI business generated nearly $5.8 billion in revenue this quarter, up about 93% year-over-year. After adjusting for favorable exchange rates, the actual growth rate was 92%, continuing to accelerate from 81% in the previous quarter. However, the pace of acceleration slowed slightly, from 16 percentage points last quarter to 11 percentage points this quarter.

The market consensus expectation for growth was also nearly 92%. Therefore, while OCI has indeed been accelerating, there was no upside surprise. In contrast, growth in the SaaS-type business under the cloud segment deteriorated. After adjusting for exchange rates, actual revenue declined by 3% year-over-year this quarter, with the decline widening from 1% in the previous quarter. This indicates that while AI benefits upstream infrastructure, the company's downstream SaaS business still faces significant growth pressure.

2. Is gross profit still under pressure, but showing signs of bottoming out?

It is widely accepted in the market that the revenue growth of AI businesses will be accompanied by a decline in gross profit margins, especially for new cloud companies like Oracle. The combined gross profit margin for the cloud + software businesses was 68.8% this quarter, showing signs of rebounding from the previous quarter's 68.2%. Although the year-over-year decline was still a significant 6.8 percentage points, it was narrower than the previous quarter.

However, since it includes both cloud and software businesses, it is not easy to determine whether the rebound in gross profit margin is due to the stabilization of OCI's gross profit margin or improvements in other businesses' margins. From an expectations perspective, the market expected an overall gross profit margin of over 66%, but the actual figure was only 65.2%. Therefore, the overall gross profit performance this quarter was still negative and did not fundamentally alleviate market concerns about profit margins.

3. Leading Indicator – RPO Exceeds Expectations, Capex Sharing Model Becomes Mainstream?

Since there were no rumors before the earnings release about the company securing large new orders, the market's expectations and focus on RPO this quarter were not high, at only 590 billion, with a slight quarter-over-quarter increase of less than 40 billion. However, after an actual increase of 85 billion, the total RPO reached 638 billion, making it one of the few bright spots this quarter.

The company still did not disclose specifics about the new orders, but given its recent announcement of cooperation with the U.S. federal government and the Department of War, it is speculated that the unexpectedly high volume of new orders may have come from the government.

Additionally, it is worth noting that last quarter, the company mentioned that some orders' Capex investments would be partially covered by customer prepayments or self-purchased hardware. This quarter, the company announced that approximately 75 billion in orders are now based on this Capex-sharing model.

Considering that most of these orders were likely signed in the last two quarters, it implies that more than half of the recent new orders may have adopted this Capex-sharing model. This is a positive signal for the company's own cash flow and balance sheet structure.

III. Recent Balance Sheet Continues to Deteriorate, but Medium- and Long-Term Positive Signs Emerge?

With the continued acceleration of the company's OCI revenue growth, Capex this quarter was nearly 16.5 billion, down from the previous quarter's 18.6 billion. However, since the market, based on the previous earnings report, expected the company to maintain its full-year Capex guidance of 50 billion without raising it, it "mechanically" deduced that this quarter's spending would only be around 11 billion, making the actual spending significantly exceed expectations. But given the accelerated capacity deployment, it is more accurate to say that expectations were too low rather than actual Capex being too high.

Additionally, the company disclosed that the Capex-sharing model mentioned earlier covered approximately 4.6 billion in Capex spending this quarter. As a result, the company's free cash flow improved from outflows of 10 billion per quarter previously to a net outflow of only 1.9 billion this quarter, clearly reflecting a reduction in the company's cash flow pressure.

To support large capital expenditures, the company stated that it completed 43 billion in bond and 5 billion in equity financing in FY26, and in the new FY27, it will conduct 20 billion each in debt and equity financing (totaling 40 billion), as previously disclosed, securing funding sources for most of the next fiscal year's Capex investments.

In fact, this financing target is lower than the free cash flow deficit originally expected by Dolphin Research and the market (over 50 billion). Dolphin Research believes that this is likely because some funding needs have been borne by customers themselves, reducing the company's own debt burden, which is also a positive signal from a long-term perspective.

However, these positives are not yet apparent, as actual interest expenses reached 1.44 billion this quarter, up nearly 22% sequentially, with interest expenses accounting for a further increase to 6% of total revenue. Based on the balance sheet, the company's net interest-bearing debt also increased by over 16 billion year over year.

In the current medium- to short-term perspective, the company's balance sheet and debt repayment pressures are still expanding.

IV. Traditional Segments Continue to Decline

Unlike the accelerated growth of OCI businesses, the performance of traditional segments, which still account for about 75% of total revenue, is deteriorating. The revenue growth of the secondary critical SaaS and software businesses slowed to +10% and -2%, respectively, with growth rates decelerating and falling short of market expectations. Although hardware and service revenue growth was significantly better than expected, these two businesses combined account for just over 10% of total revenue, making the decline in software and SaaS businesses the primary issue.

Therefore, while the company's infrastructure-layer OCI business benefits from the rise of AI, its larger traditional pan- software businesses face increasing pressure.

V. Overall Performance Mixed

1. Strong Infrastructure, Weak Software, Steady Overall Growth

Summarizing the four major business segments, the accelerating OCI segment and the weakening software segment offset each other, with the company's overall revenue growing by 20.6% this quarter, appearing to decelerate sequentially. However, after excluding exchange rate impacts, the true growth rate was 20%, still a slight acceleration of 2 percentage points compared to the previous quarter.

2. Gross Profit Margin Continues to Decline

As mentioned earlier, the company's overall gross profit margin showed initial signs of stabilization sequentially but remains in a clear contraction trend year over year. As a result, the year-over-year growth rate of total gross profit was 12%, still significantly lower than revenue growth and slightly below market expectations by about 0.6 percentage points.

3. Good Expense Control Helps Profit Growth Outpace

In terms of expense spending, overall expenses grew by 5.4% year over year this quarter, significantly higher than the previous quarter's 1% growth and above market expectations of 1.7%, suggesting a potential increase in expense investment. However, this was due to the recognition of approximately 800 million in "restructuring" expenses, likely related to news reports of the company planning to lay off nearly 30,000 employees (about 19% of the workforce, though the company did not confirm this directly).

Excluding these three routine operating expenses, actual spending decreased by about 5.6% year over year, 7 percentage points lower than market expectations. All three expense categories saw negative year-over-year growth, with marketing expenses declining by over 10%. This shows that despite margin pressures and tight cash flow due to Capex, the company's expense control efforts and results have been commendable.

Thanks to excellent expense control, despite a significant decline in gross profit margin, the adjusted operating profit margin stopped declining year over year, returning to positive growth of about 0.5 percentage points, better than market expectations.

Ultimately, adjusted operating profit reached 8.6 billion, up about 22% year over year, outpacing revenue and expectations despite gross profit falling short of expectations.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reprinting is only allowed with authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, product preferences, risk tolerance, financial situation , or special needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of the data in this report. The information and data in this report are based on publicly available sources and are for reference only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or views mentioned in this report shall not be regarded as or construed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction, nor do they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and data in this report are not intended for distribution to or use in jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations or requires Dolphin Research and/or its subsidiaries or affiliates to comply with any registration or licensing requirements in those jurisdictions.

This report only reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or distribute any copies or reproductions in any form, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action