Huawei Makes a Comeback in the Sub-1000 Yuan Smartphone Market: Who Will Face Elimination?

04/03 2026

04/03 2026

605

605

China's smartphone industry, which has been embroiled in fierce competition for over a decade, stands as arguably the most challenging sector within the tech landscape.

This formidable difficulty arises from two primary factors. On one hand, the overall market demand remains sluggish or is even experiencing a decline, with the momentum for growth noticeably slowing. On the other hand, each manufacturer is engaged in an intense, cutthroat battle to capture market share from rivals, launching numerous new models annually in a tug-of-war over specifications and features...

As if these challenges were not daunting enough, the industry is now grappling with soaring costs—a blow that could be nearly fatal for a smartphone industry already operating on razor-thin profit margins of around 10%. Meizu, for instance, was compelled to exit the market gracefully under these immense pressures.

However, this is far from the end. With Huawei reclaiming its dominance in the mid-to-high-end market and re-entering the sub-1000 yuan segment, coupled with AI technology reshaping the competitive landscape of the industry, the era of sub-1000 yuan smartphones—which once bolstered half of China's smartphone industry through their cost-effectiveness—is gradually drawing to a close.

Delving deeper, we find that a new era of significant reshuffling in the smartphone industry is upon us.

| The Final Struggles of the Old Era |

During the industry's blue ocean phase, smartphone manufacturers primarily competed in niche areas such as screens, communications, cooling systems, and photography capabilities. This trend persisted even into last year, as exemplified by Honor's launch of a smartphone boasting a 10,000mAh large-capacity battery.

However, this year's sharp increase in memory costs (ranging from 50% to 100%) has disrupted the strategies of many manufacturers. Faced with soaring memory costs, fluctuating storage chip prices, and increased R&D expenses for on-device AI, the industry has been divided into three distinct camps: those that raised prices first, those that held out for a while, and those that have not yet increased prices.

In other words, the direct consequence of this price hike trend is the infinite amplification of the Matthew effect within the industry.

Manufacturers like OV and Honor were among the first to raise prices (e.g., OPPO's A-series, K-series, and OnePlus brands). According to incomplete statistics, most models saw price increases ranging from 300 to 500 yuan.

Mr. Zhu, a seasoned veteran in the smartphone industry with many years of experience, stated, "The smartphone industry comprises upstream and downstream distribution and agency links. Once raw material costs rise, the proportion of memory costs in a model can reach one-third. Some models become scarce resources, leading upstream distributors to hoard inventory and only release it after prices reach a certain level. They may also bundle these with high-inventory models to clear stock."

This is hardly a secret within the industry. Conventionally, premium models from Huawei and Apple command higher margins, but this year is different—even mid-to-low-end sub-1000 yuan smartphones could become targets for "heavy positioning."

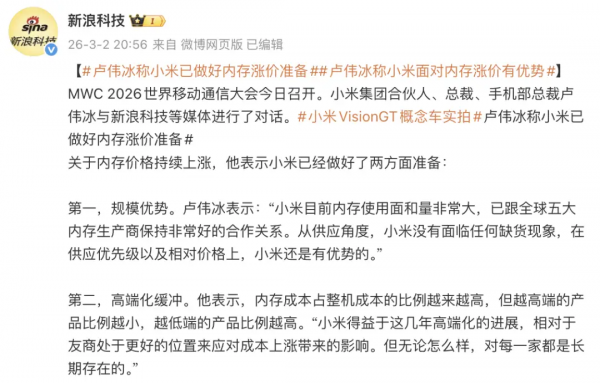

Xiaomi is a typical example of a manufacturer that held out before raising prices.

Lu Bingwei previously stated, "We'll try to absorb costs for consumers as long as possible. When we can no longer hold out, we'll have to raise prices. I hope consumers will understand us when that time comes."

Xiaomi's strategy is closely related to its business situation. On one hand, Xiaomi has established strong cooperative relationships with global supply chains over the years. Additionally, the growth of Xiaomi's automotive business has made it more resilient in the face of price hikes. However, Xiaomi's smartphone revenue declined by 2.8% in 2025. Lu Bingwei also mentioned that Xiaomi has certain advantages in dealing with memory price hikes.

Nevertheless, price increases arrived swiftly. Recently, Xiaomi announced adjustments to the prices of three smartphone models: the REDMI K90 Pro Max increased by 200 yuan, while the Turbo 5 and Turbo 5 Max canceled their New Year promotions, though the 512GB large-memory versions continue to receive a 200 yuan subsidy.

Among mainstream manufacturers, Huawei is the only one that has not yet adjusted its prices.

Huawei appears to be completely rewriting the rules of the sub-1000 yuan smartphone market. In late March, it released the new Enjoy series, equipped with the "Kirin 8-series chip + HarmonyOS 6 + Whale large-capacity battery," priced starting at 1,299 yuan, up to 2,399 yuan. The intention is clear: after topping the domestic market last year, Huawei is leveraging new selling points like HarmonyOS to quickly penetrate the low-price segment.

This represents the last struggle of old-era players and the prelude to industry restructuring.

Some outsiders believe that manufacturers with supply chain bargaining power and high-end market profit support can still barely survive; while small and medium-sized manufacturers, lacking the ability to absorb costs, can only cling to survival in the cracks.

More awkwardly, as all manufacturers shift resources to the mid-to-high-end market, sub-1000 yuan smartphones—once the industry's foundation—have become a "tasteless yet hard to discard" dilemma. The old-era logic of relying on cost-effectiveness is slowly losing its effectiveness.

The dilemmas faced by other manufacturers are clear: they cannot compete with Huawei and Apple in the high-end market to secure sufficient profits; now, their survival-dependent sub-1000 yuan market is being disrupted by leading manufacturers leveraging ecological advantages. Trapped between two fires, they face dual pressure on market share and profit margins, risking a vicious cycle of "intensifying competition leading to losses, and losses leading to even fiercer competition."

Ultimately, the old-era approach of relying on cost-effective hardware stacking in the smartphone industry has reached its limit. However, the challenges do not stop there—new variables are emerging one after another.

| Uncertainties on the Eve of a New Transformation |

Persistent market sluggishness has pushed internal competition in the mid-range market to extremes, while the high-end market's oligopoly remains nearly unshakable. The AI technology boom has brought unprecedented uncertainty to this teetering industry. Everyone is betting on the future, but no one knows if their bets will pay off.

The overall smartphone market has been in a cold spell for too long.

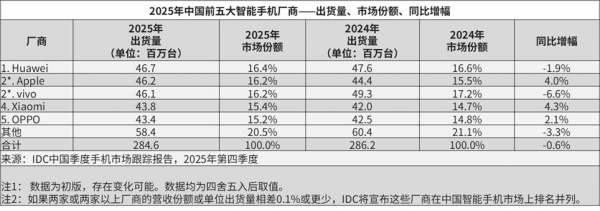

IDC data shows that in 2025, China's smartphone shipments reached approximately 285 million units, down 0.6% year-on-year—marking another decline. Even with government subsidies last year and manufacturers launching flagship products with features like over 100-megapixel cameras, growth momentum weakened in the second half of the year, leading to an overall market decline.

The harsh industry reality does not end there.

More alarming than declining shipments is the prolonged user replacement cycle, which has stretched from 18 months to over 36 months on average, with many users now waiting over four years to upgrade.

Smartphones have become increasingly durable, with performance excess becoming the norm. Users lack compelling reasons to upgrade, transforming the market from incremental growth to a zero-sum game. Every additional unit sold by one manufacturer means one fewer unit sold by a rival, leaving no room for luck.

In this saturated market, all manufacturers have made the same choice: not abandoning high-end breakthroughs while pouring key resources into the mid-range market for fierce competition. The reality is that in today's high-end market, Huawei and Apple dominate around 80% of the 4,000+ yuan price segment, with all other manufacturers combined accounting for less than 20%.

The barriers to the high-end market are the moats built by Huawei and Apple through differentiated advantages like independent operating systems and strong brand perception. Even if latecomers offer competitive products (e.g., Honor's Magic8 series with an industry-leading AI visual experience through "YOYO Seeing"), brand沉淀 (brand precipitation), ecological accumulation, and user mindset occupation cannot be achieved overnight.

With limited high-end market share gains, manufacturers must revert to defending the mid-range. The 2,000-4,000 yuan price segment accounts for nearly 50% of industry shipments and is a battleground for all manufacturers.

Objectively speaking, the intensity of this mid-range competition surpasses even the sub-1000 yuan price wars of the past. Features once exclusive to 5,000-6,000 yuan flagship models—such as imaging configurations, chip performance, and frame quality—are now being introduced in 2,000 yuan mid-range devices, including satellite communication, large batteries, and flagship-grade screens.

As a result, manufacturers face a dilemma: not competing means losing market share and being eliminated; competing means sacrificing profits, leaving no funds for R&D and falling behind in future technological shifts.

Then, new variables emerged.

While mid-range competition rages on, the AI technology boom has triggered a complete rule reshuffle in the industry. Although AI smartphones are still in their experimental phase—with some exploring on-device intelligence and others attempting to integrate embodied AI with smartphone hardware—even tail-end manufacturers are re-entering the race through partnerships with AI large model providers, striving to create new hit products.

However, the "iPhone moment" for AI smartphones has yet to arrive, and every manufacturer still has an equal opportunity, making this the next frontier for intense competition and elimination.

In summary, in the saturated market, the most fearsome threat isn't visible competitors but invisible era-defined barriers. Smartphones stand at a crossroads: ahead lies insurmountable technological barriers, behind a shrinking market—trapped between a rock and a hard place.

| Who Will Be Eliminated Next? |

Meizu was the first among existing smartphone companies to hit pause in the Chinese market.

However, Lei Jun previously stated publicly that it's unlikely all seven major Chinese players will survive in the long run.

This conclusion is not unfounded. Beyond insufficient market growth, the smartphone industry increasingly resembles the previous fuel-powered vehicle industry. When market saturation meets technological disruption, elimination can happen almost instantly. Meizu's exit is certainly not the end.

Looking back at the past three years, every quarter and year has been marked by intense competition.

We find that Huawei, Xiaomi, Vivo, OPPO, and Honor have all ranked fourth or fifth on IDC's lists at various points. Specifically, in 2023, Vivo ranked fourth with a 16.5% share, while Huawei was absent from the top five.

In 2024, the rankings shifted, with OPPO and Honor tied for fourth, while Xiaomi fell out of the top five. By 2025, Xiaomi claimed fourth place, and Honor disappeared from the rankings again.

Despite these rotational changes, the gaps between manufacturers remain small. IDC data shows that in 2025, domestic manufacturers' market shares mostly hovered between 15%-16%, with differences so narrow that a single quarter's hit product could completely reverse rankings.

This suggests that the new growth drivers for smartphone products have not truly arrived. In contrast, the new energy vehicle sector has grown continuously in recent years due to electrification, intelligence, and purchase tax incentives.

It's clear that Meizu's exit from the mainstream smartphone market is just the beginning of this elimination race. Next, manufacturers lacking core technologies, ecological layouts, and surviving solely on cost-effectiveness will become the next casualties.

In this era of saturated competition, the market leaves no room for middle-ground players. Either become an industry leader through technology and ecology, or be eliminated by the times and fade into history.

And the final whistle of this elimination race is drawing ever closer.

Image sourced from the internet. Rights reserved for the original author.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once