Apple Boosts Foldable iPhone Orders by 30%! Is the Foldable Display Market on the Brink of Transformation?

07/06 2026

07/06 2026

512

512

The scarcer the chips become, the more aggressive Apple gets.

Author|Yixiu

Editor|Xiaobai

Produced by|Qiangdiao Next

Recently, supply chain sources have revealed that Apple has significantly increased its stock target for its inaugural foldable iPhone this year. Initially expected to be 7-8 million units by the market, the target has now been raised to approximately 10 million units, marking a nearly 30% increase. Concurrently, Apple has secured components for around 80 million new iPhone units from its supply chain. Including existing models, Apple's total iPhone production for 2026 is projected to surpass 220 million units.

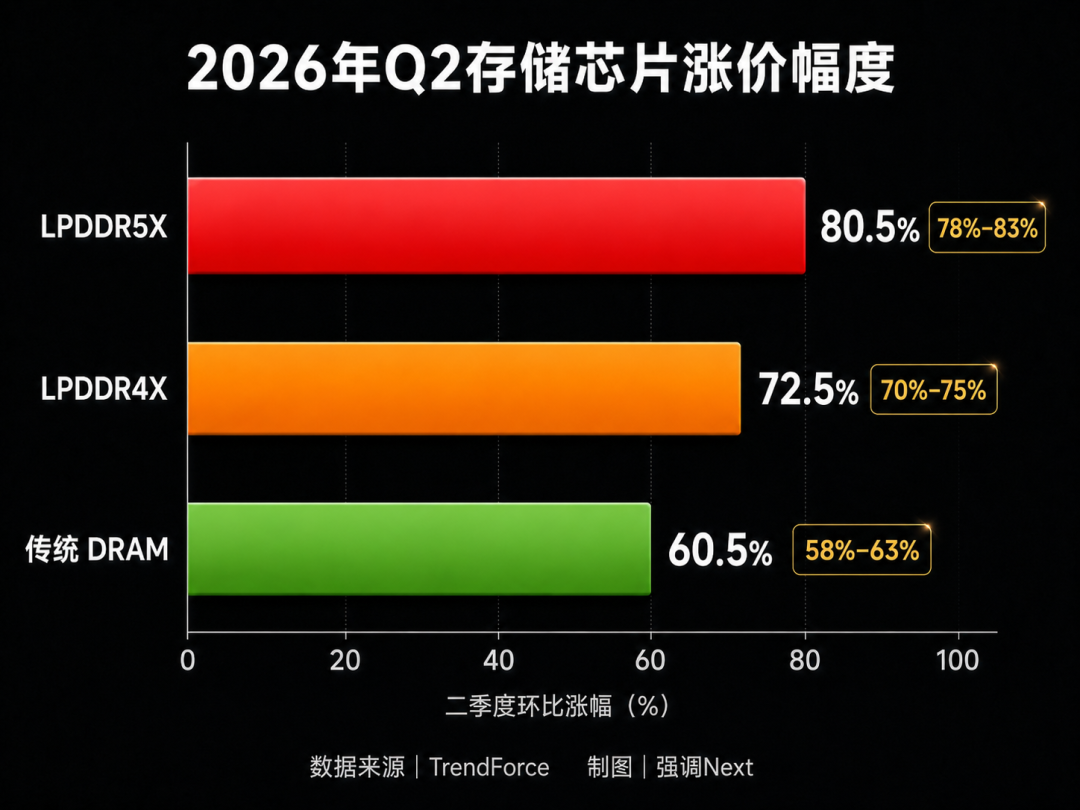

As the world grapples with the most severe memory chip price hike in a decade, DRAM contract prices have soared by 50%-60% quarter-over-quarter, with some older-generation products seeing increases exceeding 80%. Several domestic smartphone manufacturers have been compelled to raise prices in March, with hardware profit margins for some budget models dipping below safe levels.

Amidst this challenging period of shortages and price hikes, Apple is not retreating but rather doubling down on the costly new category of foldable screens. What is the source of its confidence?

01. The Scarcity Fuels Aggressive Market Capture

On the surface, the memory chip shortage spells trouble for all smartphone manufacturers. Currently, material costs constitute over 20% of a smartphone's total cost, up from the usual 10%-15%, with storage costs for mid-to-low-end models nearing 30%. However, for a behemoth like Apple, the shortage presents an opportunity to widen its lead.

The rationale is straightforward: when the entire industry is vying for chips, those with greater purchasing power, longer payment terms, and stronger bargaining leverage can secure production capacity first. Reports suggest that Apple's counter-cyclical order increase aims to leverage its supply chain bargaining power to expand market share amid widespread memory shortages and further widen the gap with Android manufacturers.

Apple, Huawei, and Samsung, with their robust supply chain control, economies of scale, and brand premiums, can effectively offset cost impacts through dynamic pricing, supply chain optimization, and deeper strategic cooperation with memory manufacturers.

Meanwhile, mid-range foldable players like Xiaomi and Honor face both cost pressures and capacity squeezes from top-tier rivals. Some have delayed or canceled new product launches. Counterpoint data indicates that Xiaomi's global foldable smartphone shipments plummeted 54% year-over-year in Q3 2025, with its global share dropping from 6% to 2%. Xiaomi has paused large foldable updates, relying mainly on small foldable models for sales. While product strategy plays a role, cost pressures exacerbated by top-tier rivals are an undeniable reality.

Apple's product cadence this time also reflects unusual aggressiveness. The company plans to launch at least five new iPhone models in less than a year: three high-end models (iPhone 18 Pro, iPhone 18 Pro Max, and the first foldable, codenamed iPhone Ultra) this fall, targeting the flagship market, while the standard iPhone 18, iPhone 18e, and second-gen iPhone Air are delayed until spring 2027.

This "high-end first, standard later" approach aligns with the initial ramp-up of 2nm chip capacity, prioritizing limited production for the highest-margin models—foldables and Pro series.

02. Apple's Well-Prepared Move

The market anticipation for the foldable iPhone stems from its near-elimination of previous shortcomings.

Rumors had suggested delays until 2027 due to hinge yield issues, but recent supply chain information indicates that liquid metal hinge noise tolerance problems have been largely resolved, and screen crease control meets Apple's internal mass-production standards. Foxconn is set to commence mass production in late July, prioritizing initial capacity for September launch deliveries, with large-scale shipments starting in Q4.

In terms of hardware, the model features a horizontal book-style inward fold, with a thickness of approximately 4.5mm when unfolded and 9.2mm when closed. It boasts a 5.5-inch outer screen and a 7.8-inch 4:3 OLED inner screen supporting 1-120Hz LTPO adaptive refresh rates. Powered by TSMC's 2nm A20 Pro chip with 12GB RAM, a titanium frame, and IP68 water/dust resistance. To control thickness, it sacrifices the telephoto lens, Face ID, and MagSafe, opting for a power button with integrated Touch ID.

Samsung has secured exclusive orders for the OLED panels and hinges, signing a three-year supply agreement with panel prices nearing RMB 1,000 each.

Pricing-wise, the overseas starting price is widely expected to exceed $2,000, with the Chinese version priced between RMB 14,999 and 15,999, and the top-tier model potentially breaking RMB 20,000.

03. Domestic Players' "Asymmetric Encirclement"

Domestic foldable competition began long ago. In recent years, Huawei, OPPO, Vivo, and Honor have strived to establish price benchmarks and technical standards before Apple's official entry.

Huawei's competitive edge now extends to patents. It dominates 60%-70% of China's foldable market, with a 71.8% share in 2025, covering nearly all form factors (horizontal large fold, triple fold, wide fold, vertical small fold). Its pricing strategy—exemplified by the upcoming Mate XTs Ultra Master, priced around RMB 15,000 (down from RMB 19,900)—directly targets Apple's rumored $2,000 (~RMB 14,500) price point. The rivalry is palpable.

OPPO and Vivo adopt a different tactic: undermining Apple's ecosystem barrier. Vivo's new foldable enables data connectivity with Apple Watch and iCloud access—cross-ecosystem functions. OPPO has even trademarked "OPhone," with product leaders openly expressing hopes to convert Apple users.

These domestic players are also waging a collective price war, slashing average foldable prices from "luxury" levels to below RMB 10,000, with the domestic market average now around RMB 8,500.

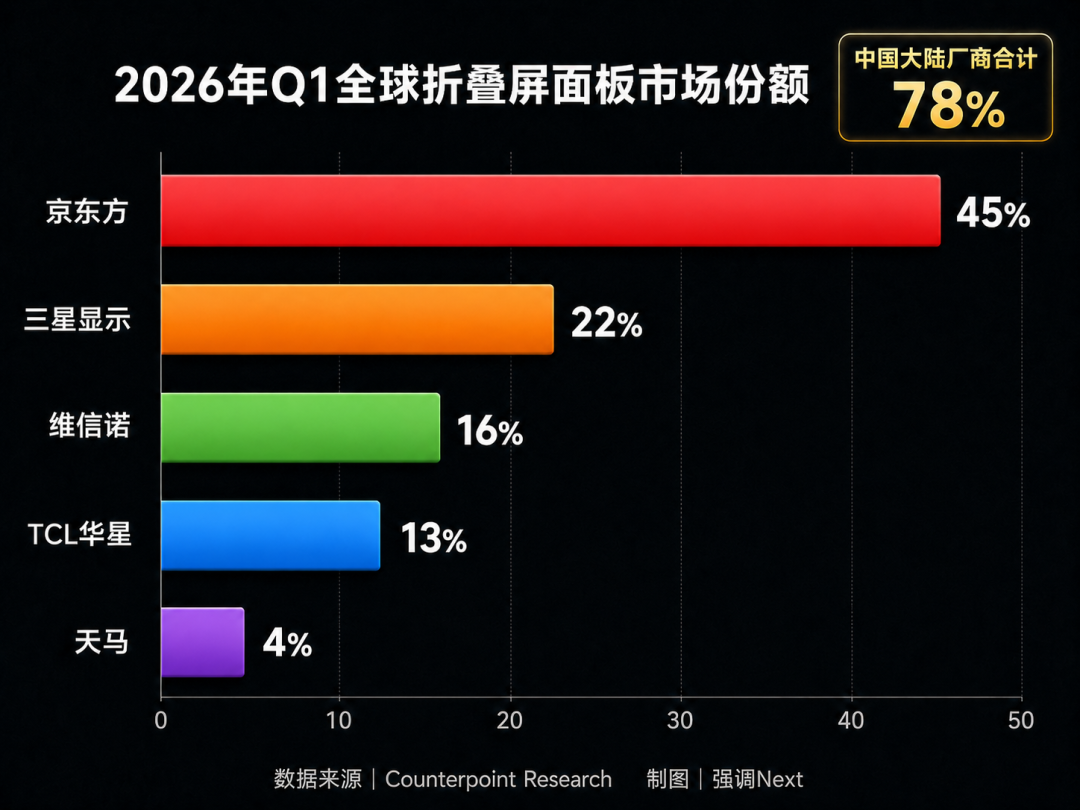

Supply chain competition is equally fierce, even reaching courtrooms. Samsung, holding exclusive panel orders for Apple's foldable, sued BOE in the U.S. for trade secret theft and won. Meanwhile, domestic players account for approximately 78% of global foldable panel shipments, with BOE leading at 45%. Domestic supply chains have evolved from "chasers" to "volume leaders" in foldables, though they still face Samsung's dual patent and capacity pressure for top-tier orders.

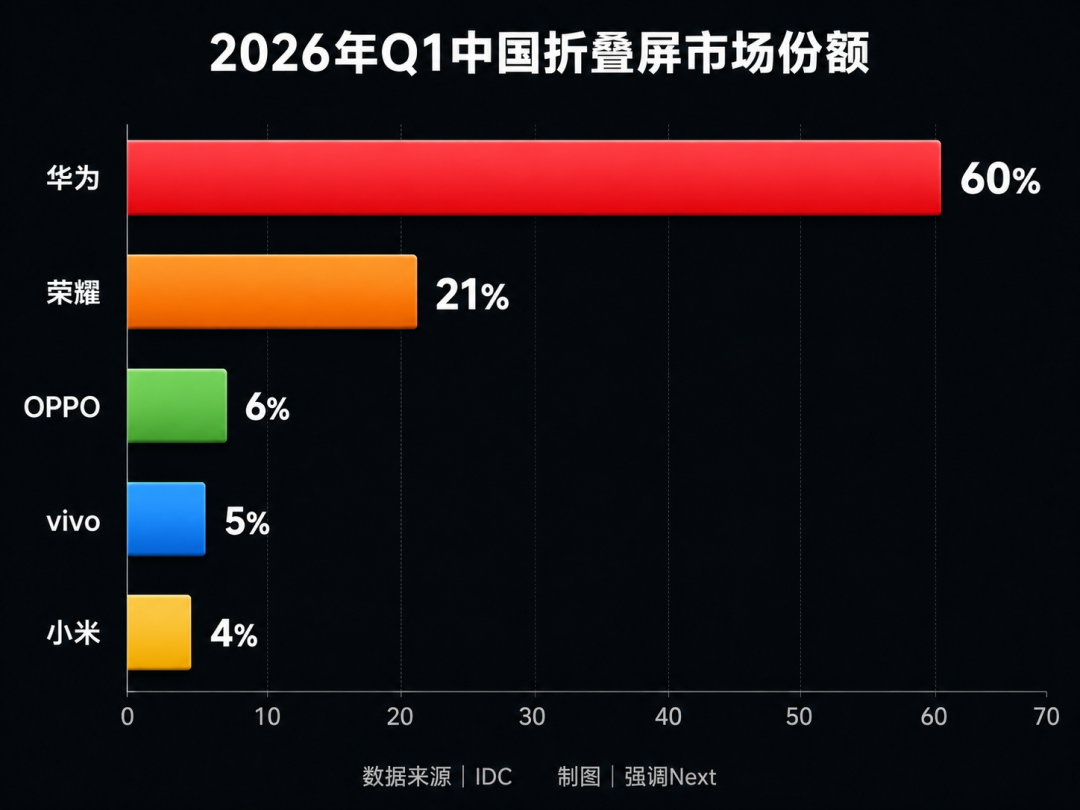

Domestically, Huawei held 60% of China's foldable market share in Q1 2026, with Honor at approximately 20%, followed by OPPO, Vivo, and Xiaomi. Domestic foldable sales surged 65% year-over-year in the same period.

No matter how well-prepared Apple is, it enters not a "blue ocean" but a mature market where domestic brands have spent six years building deep technical barriers and user loyalty.

04. 10 Million Units: Confidence or Gamble?

10 million units approach China's total foldable shipments for 2026. However, industry analysts caution that this represents Apple's annual production capacity ceiling, not guaranteed sales. Some supply chain analysts predict first-year foldable iPhone production will fall far short of regular iPhone volumes, reflecting doubts about market acceptance of the high pricing strategy. With Android foldable prices down 18% year-over-year and domestic averages at RMB 8,500, Apple's potential >RMB 14,500 starting price faces obvious pressure.

Crease control, software optimization, and after-sales repair costs (mainstream foldable screen replacements cost RMB 3,000-5,000, equivalent to a mid-to-high-end bar phone) are all areas where Apple's first-gen product must prove itself—areas where domestic players have refined their offerings over five to six generations.

Apple's true ace is its base of over 1.5 billion iPhone users and the ecosystem loyalty built through Macs, iPads, and Apple Watches. If even a fraction of users upgrade for the "Apple foldable," the 10 million target is plausible.

For the entire supply chain, regardless of Apple's bet's ultimate success, its substantial orders are propelling foldables from an "Android-only" niche to the global premium smartphone mainstream.

- END -

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models