Will Tesla's autonomous driving compete fiercely with domestic new energy intelligent driving in the next three years?

08/06 2024

08/06 2024

651

651

Text / San Dian

'In the face of time, all technical obstacles are paper tigers.' Ten years ago, new energy vehicles were still a new concept. Today, ten years later, new energy vehicles are already running everywhere. What will happen in another ten years is truly worth looking forward to.

In the development process of new energy vehicles, the first half of 2024 is destined to leave a lasting impression.

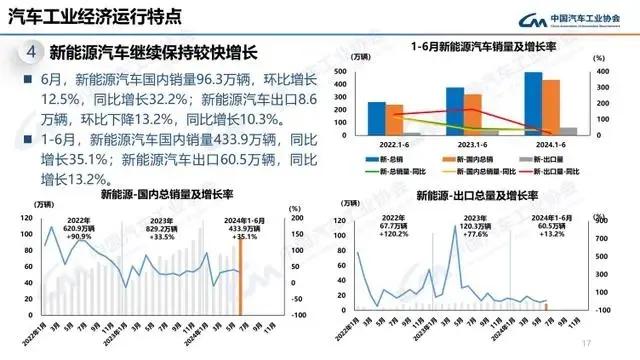

According to the latest data released by the China Association of Automobile Manufacturers, as of the end of June this year, the cumulative production and sales of domestic new energy vehicles have officially surpassed the 30 million mark. Specifically, from January to June this year, domestic new energy vehicle production and sales totaled 4.929 million and 4.944 million units, respectively, with year-on-year growth of 30.1% and 32%, and a market share of 35.2%. In the just-passed July, new energy vehicle retail sales are expected to reach 860,000 units in a single month.

This trend is still accelerating. Specifically, in June alone, new energy vehicle production and sales reached 1.003 million and 1.049 million units, respectively, with a market share of 41.1%. It is not difficult to predict that the market share of new energy vehicles will continue to rise in the future.

So, looking back at the first half of 2024, what are the development trends worth paying attention to behind the rapid development of new energy vehicles?

01 Market share soars, gas-powered cars on the decline?

Corresponding to the rapid expansion of the new energy vehicle market is the gradual retreat of the traditional gasoline-powered vehicle market, a trend that is almost inevitable. Data shows that from January to June this year, retail sales of conventional gasoline-powered vehicles were 5.73 million units, a year-on-year decrease of 13%.

The rapid decline of gasoline-powered vehicles has surpassed the expectations of many people.

In the view of JieDian Auto, the reason why the sales of new energy vehicles have increased year by year lies first and foremost in the unparalleled advantages that new energy vehicles have over gasoline-powered vehicles, such as the all-new intelligent technology and driving experience offered by electric vehicles, which far surpass those of traditional gasoline-powered vehicles. A smart electric car costing 200,000 to 300,000 yuan can offer a driving experience that might not have been achievable with a million-yuan gasoline-powered car in the past, prompting a large number of former gasoline-powered car users to switch.

Moreover, in the race for new energy vehicles, major brands are stepping up their efforts, with new products launched continuously like mushrooms after rain. In contrast, the traditional gasoline-powered vehicle sector appears less energetic.

The latest data from the China Passenger Car Association shows that a total of 11 gasoline-powered car models were launched in the first half of this year, 31 fewer than the same period in 2018, while 60 new models of new energy vehicles were launched in the first half of the year, almost six times as many as gasoline-powered cars.

Furthermore, the lack of new product launches has also put gasoline-powered cars at a disadvantage in the competition for "price wars."

In the "price war" that began at the beginning of this year, gasoline-powered cars also participated. However, new energy vehicles relied on a large number of newly launched products to offset the negative impact of some price drops. In contrast, gasoline-powered cars struggled to maintain price stability due to the significant reduction in new models, facing greater pressure.

Currently, after large-scale price cuts earlier this year, the discount rates of many new energy vehicle brands have shrunk compared to before, but the discount rates of gasoline-powered cars have become increasingly larger, as they have had to lower prices.

However, even so, it is unlikely that gasoline-powered cars can reverse their decline. In the second half of this year, various favorable policies such as trade-ins and new energy vehicle rollouts in rural areas will continue to be implemented, and new models of new energy vehicles will also be launched intensively, making it likely that sales will rise further. Industry insiders predict that new energy vehicle production and sales are expected to reach 11.5 million units this year.

Such a market size provides ample room for the development of domestic new energy vehicle brands. So, how have new energy vehicle brands performed in the past six months?

02 The pattern of independent brands, "Wei Xiaoli" no longer exists

According to JieDian Auto, from the perspective of the entire automotive market, the market share of independent brand passenger cars is continuously increasing. This is due, on the one hand, to the rapid growth in sales of new energy vehicles, and in this trend, the speed of transformation towards electrification and intelligence by independent brands is significantly higher than that of joint venture brands; on the other hand, it is due to the rapid growth in automobile exports, which are dominated by independent brands.

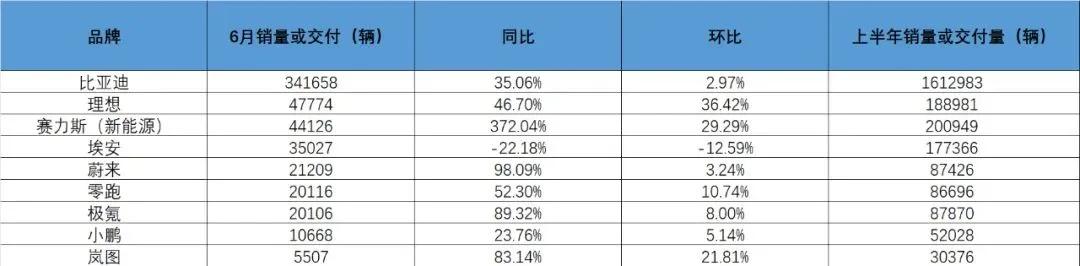

Specifically, BYD's sales remain ahead of the pack. Data shows that BYD sold 340,000 new energy vehicles in June, an increase of 30.6% year-on-year; cumulative sales in the first seven months of this year were approximately 1.96 million units, an increase of 28.83% year-on-year.

Apart from BYD, several new automotive forces also performed well in the first half of the year. In the first tier, NIO encountered a brief downturn in the first half of the year but rebounded strongly, taking the sales crown among new forces in July with a delivery of approximately 51,000 vehicles, setting a new monthly delivery record and achieving a year-on-year growth of 49.4%. In the first seven months of this year, it delivered approximately 240,000 vehicles.

However, at the beginning of this year, NIO set a full-year delivery target of 480,000 vehicles. In comparison, NIO will need to work harder in the second half of the year to achieve its annual target.

Outside of NIO, the one that can compete with it is SERES. Data shows that SERES sold 42,200 new energy vehicles in July, a year-on-year increase of 508.25%. Vehicle sales in the first seven months were 282,600 units, a year-on-year increase of 171.19%.

SERES' sales are mainly composed of its AITO M5, which is also the absolute mainstay of HarmonyOS SmartRide, and the latter delivered a cumulative total of 238,300 vehicles in the first seven months of this year.

In the second tier of new forces, NIO is gradually emerging from its downturn, delivering a total of 20,500 new vehicles in July, exceeding 20,000 units for three consecutive months. In the first seven months of this year, NIO delivered a total of 108,000 new vehicles, a year-on-year increase of 43.85%.

It is worth noting that throughout the second quarter, NIO delivered a total of 57,400 new vehicles, a significant increase of 143.9% year-on-year, far exceeding market expectations. Therefore, NIO's performance may be even stronger in the second half of the year.

Also breaking through the 20,000-unit mark in July was Leapmotor, which delivered 22,100 vehicles in July alone, a year-on-year increase of 54.1%, setting a new record. Following closely behind NIO is ZEEKR, which delivered 15,700 new vehicles in July, a year-on-year increase of over 30%.

In contrast, XPeng, once one of the "Wei Xiaoli" trio, lags significantly, delivering approximately 11,100 vehicles in July and 63,100 vehicles in the first seven months of this year, a year-on-year increase of 20%.

Lastly, it is necessary to mention Xiaomi Automobile, the top player in the automotive industry in the first half of the year. In June and July, Xiaomi SU7 deliveries exceeded 10,000 units. Xiaomi Automobile stated that August deliveries will continue to exceed 10,000 units, and it is expected to complete its annual delivery target of 100,000 units ahead of schedule in November.

Based on the sales performance of new energy vehicles in the first half of the year, BYD's scale remains unique, while NIO and XPeng are in the first tier among new forces, with Leapmotor, ZEEKR, and NIO in the second tier. Xiaomi's performance needs further observation, and XPeng risks falling behind from the "Wei Xiaoli" trio.

Compared to previous years, the landscape of the entire new energy vehicle market is undergoing significant changes.

03 The next three years: a decisive battle for intelligent driving in the new energy sector

On the one hand, there is the rapid expansion of the market size, which also means increasing competition. This is not only reflected in the competition between gasoline-powered and electric vehicles but also in the "involution" among electric vehicle brands. The "price war" that began at the beginning of this year exemplifies this fierce competition.

Not long ago, FAW Toyota posted on its official WeChat account: "From January to June this year, the most influential, longest-lasting, and widest-reaching keyword in the automotive market has remained the price war."

In this regard, the view of BYD Chairman Wang Chuanfu is more representative. He believes that the new energy vehicle industry has entered a knockout stage, and 2024 to 2026 will be decisive battles for scale, cost, and technology.

"Chinese automakers are accelerating the launch of new energy products, which will erode the market share of joint venture brands. In the next 3 to 5 years, the share of joint venture brands will drop from 40% to 10%, with 30% of this decline representing growth potential for Chinese brands."

Wang Chuanfu's view will be validated in the next three years.

From a short-term perspective, JieDian Auto has observed that the ongoing "price war" has had a significant impact on the terminal market. While continuous heavy promotions in the first half of the year drove sales, they may have had an overdraft effect on consumer spending for car purchases in the second half of the year, potentially weakening the effectiveness of the "price-for-volume" strategy in July, and further observation is needed to see if production and sales volumes in the second half of the year can maintain the momentum of the first half.

Of course, as Chinese new energy vehicle independent brands expand their presence in global markets, new growth drivers are emerging.

Currently, for core export regions such as Southeast Asia and Central Asia, exports of independent brands continue to grow rapidly. For markets with strong local brands, such as Europe, independent brands are also beginning to explore new joint venture models centered on technology exports. For countries with low consumption capacity, such as Africa, where the penetration rate of independent brands is still low, direct exports remain the primary mode of operation.

According to the latest report by AlixPartners, by 2030, Chinese brand automobiles are expected to sell 9 million units outside of China, with their market share growing to 13%. The development prospects of Chinese new energy vehicles remain promising.

JieDian Auto has observed that the decisive battle for future new energy vehicles will center around intelligent driving technology.

Just a few days ago, during Tesla's earnings call, Elon Musk stated that Full Self-Driving (FSD) has made significant progress and is expected to enter the Chinese market by the end of this year. Additionally, he announced that Tesla will unveil its Robotaxi on October 10, with the goal of having it operational globally within this year.

With Tesla, the "catfish" in this industry, coming in with such momentum, it is not difficult to predict that autonomous driving will become a new battleground for global technological strength and comprehensive national strength. Time waits for no one, and it remains to be seen who will emerge victorious in the end.

*The cover image is generated by AI

-

![]()

A Humanoid Robot Becomes an Office Intern: The 'Reinforcement Learning' Journey of a Former NVIDIA Engineer

-

![]()

Meta Plans to Launch Cloud Infrastructure Business: Is Computing Power Really in Excess?

-

![]()

Giants Enter the Arena One After Another: The Embodied AI Battle Commences

-

![]()

Is It More Profitable to Build 'Hands' for Robots Than 'Humans'?

-

![]()

Yunling Optoelectronics Accelerates Its Listing on the Beijing Stock Exchange: Secures 989 Million Yuan to Bolster Production of Computing Optoelectronic Chips

-

![]()

From Drill Bits to Optical Coatings: A 200-Billion-Yuan Behemoth Quietly Unveils a New Business Front!

-

![]()

New Energy Vehicle Growth Slows: Are 370 Million Existing Cars the Next Lucrative Market?

-

![]()

Is Baidu Now Fostering Its Own 'Yao Shunyu'?